Many low-income households in the United States lack access to essential services, such as home internet, a bank account, and health insurance. Households that lack any one of these services encounter hardships, but households that lack more than one of these services may be particularly disadvantaged—not only vulnerable to financial or health shocks but also unable to fully participate in society. In this briefing, we examine the degree to which low-income households are excluded from digital, financial, and health insurance services as well as the characteristics of households (specifically, their education level and race) excluded from multiple services. This information may assist with government, community, and industry initiatives to more effectively advance inclusion in health insurance coverage and digital and financial services.

Data on Types of Exclusion and the Characteristics of Low-Income Households

In this article, we focus on three types of exclusion: digital exclusion, financial exclusion, and health insurance exclusion. We define digital exclusion as the lack of home internet access, financial exclusion as the lack of a bank account, and health insurance exclusion as the lack of health insurance coverage. To cover all three types of exclusion, we use two nationally representative survey datasets. The 2019 Federal Deposit Insurance Corporation Survey of Household Use of Banking and Financial Services (FDIC survey) contains data on digital and financial exclusion, and the U.S. Census Bureau’s 2019 American Community Survey (ACS) contains data on digital and health insurance exclusion._

Together, the surveys suggest low-income households are most likely to experience multiple types of exclusion. Data from the FDIC survey and ACS suggest that over 10 percent of low-income households (those with annual household income under $30,000) experienced multiple types of exclusion in 2019, compared with at most 2 percent of higher-income households (those with annual household income of $30,000 or greater). According to the FDIC survey, 11 percent of low-income households experienced both financial and digital exclusion, compared with only 1 percent of higher-income households. And according to the ACS, 3 percent of low-income households experienced both health insurance and digital exclusion, compared with less than 1 percent of higher-income households.

Education, Race, and Multiple Types of Exclusion among Low-Income Households

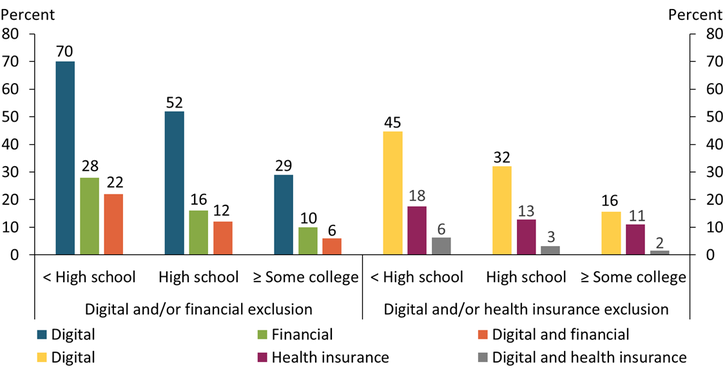

Low-income households from certain educational or racial backgrounds may be more likely to experience multiple types of exclusion than others. Previous studies have found that education and race are highly correlated with any one type of exclusion (Hayashi and Minhas 2018; McMorrow, Skopec, and Thomas 2019; Perrin and Atske 2021). To examine how education is correlated with digital, financial, and health insurance exclusion, we divide low-income households into three groups based on their educational attainment: no high school diploma (< high school), a high school diploma (high school), and some college or a college degree (≥ some college). The left side of Chart 1 shows the shares of households that experienced digital exclusion (blue bars), financial exclusion (green bars), and both digital and financial exclusion (orange bars) for each of the three education groups according to the FDIC survey. The right side of the chart shows the shares of households that experienced digital exclusion (yellow bars), health insurance exclusion (maroon bars), and both digital and health insurance exclusion (gray bars) for each of the three education groups according to the ACS.

Chart 1: Exclusion among Low-income Households Declines as Educational Attainment Increases

Notes: Digital and/or financial exclusion rates (left side of the chart) are calculated from the FDIC survey. Digital and/or health insurance exclusion rates are calculated from ACS (right side of the chart).

Sources: FDIC, U.S. Census Bureau, and authors’ calculations.

Consistent with prior research, low-income households with lower educational attainment are more likely to experience any one type of exclusion. According to both surveys, the digital exclusion rate (blue and yellow bars) substantially declines as educational attainment increases. The FDIC survey’s digital exclusion rate declines from 70 percent for households with no high school diploma, to 52 percent for households with a high school diploma, to 29 percent for households with some college or a college degree. Both the financial exclusion rate (green bars) and health insurance exclusion rate (maroon bars) also decline as educational attainment increases, but modestly compared with the digital exclusion rate.

Low-income households with lower educational attainment are also more likely than those with higher educational attainment to experience multiple types of exclusion. As educational attainment increases, the share of households that experienced both digital and financial exclusion (orange bars) declines from 22 percent to 12 percent to 6 percent. The share of households that experienced both digital and health insurance exclusion (gray bars) also declines, from 6 percent to 3 percent to 2 percent, as educational attainment increases. We cannot assess to what degree households experienced both financial and health insurance exclusion due to the lack of data. Nevertheless, the results suggest that at least 22 percent of low-income households with no high school diploma experienced two or more types of exclusion. In contrast, the share of low-income households with some college or a college degree that experienced two or more types of exclusion is significantly lower—at most 12 percent._

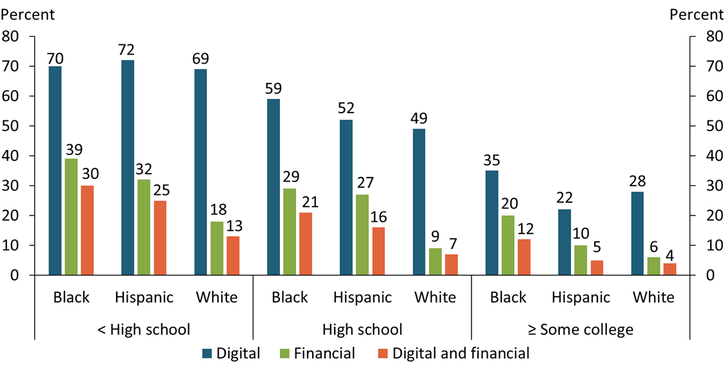

The FDIC survey shows that race and ethnicity are also correlated with digital and financial exclusion rates, even after controlling for educational attainment. Chart 2 shows digital and financial exclusion rates for Black, Hispanic, and white low-income households by education. Within each education group, the digital exclusion rate (blue bars) varies slightly across Black, Hispanic, and white households, but the financial exclusion rate (green bars) varies significantly. Across all three education groups, the financial exclusion rate is the highest for Black households, followed by Hispanic households; white households have a markedly lower rate. For example, the financial exclusion rate for households with no high school diploma is 39 percent for Black households, 32 percent for Hispanic households, and 18 percent for white households. The pattern is similar for households that experienced both digital and financial exclusion (orange bars): the exclusion rate is the highest for Black households and the lowest for white households across all education groups. Black households are about three times more likely than white households to experience both digital and financial exclusion.

Chart 2: Digital and Financial Exclusion Rates Vary by Race but Decline with Education Level

Sources: FDIC and authors’ calculations.

Although digital and financial exclusion rates vary by race and ethnicity, the exclusion rates within each race or ethnicity group decline as educational attainment increases. For example, the share of Black households that experienced both digital and financial exclusion is 30 percent for those with no high school diploma, 21 percent for those with a high school diploma, and 12 percent for those with some college or a college degree. Interestingly, as educational attainment increases, the gap between the share of Black and white households that experienced both digital and financial exclusion also narrows, from 17 percentage points (30 percent − 13 percent) for households with no high school diploma, to 14 percentage points (21 percent − 7 percent) for households with a high school diploma, to 8 percentage points (12 percent − 4 percent) for households with some college or a college degree.

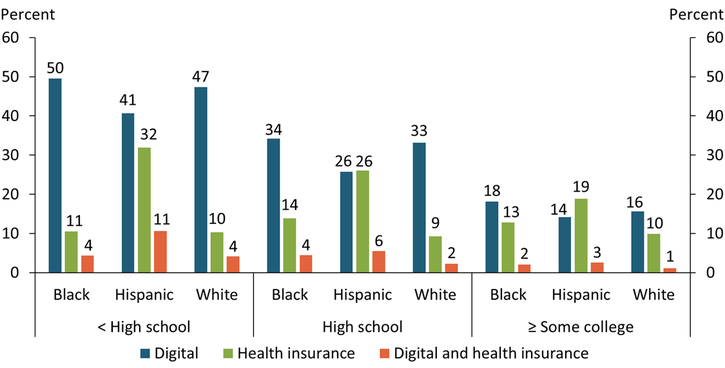

In contrast to the results for digital and financial exclusion, the ACS shows a weak correlation between race and both digital and health insurance exclusion. Chart 3 shows digital and health insurance exclusion rates for Black, Hispanic, and white low-income households by education. The digital exclusion rate (blue bars) varies only slightly by race within each education group. In contrast, the health insurance exclusion rate (green bars) is noticeably higher for Hispanic households in all three education groups. For example, the health insurance exclusion rate for households with no high school diploma is 32 percent for Hispanic households and about 10 percent for both Black households and white households. Although Hispanic households have the highest health insurance exclusion rates, their rates of digital and health insurance exclusion (orange bars) are only moderately higher than Black and white households among the two lower education groups and scarcely vary across race and ethnicity among households with some college or a college degree. Thus, households that experienced digital exclusion may not overlap with households that experienced health insurance exclusion.

Chart 3: Race Is Weakly Correlated with Both Digital and Health Insurance Exclusion

Sources: U.S. Census Bureau and authors’ calculations.

Overall, Charts 1 through 3 yield three findings. First, educational attainment is strongly correlated with digital and financial exclusion rates, even after controlling for race and ethnicity._ Second, as educational attainment increases, racial gaps in digital and financial exclusion rates narrow. And third, race is weakly correlated with both digital and health insurance exclusion despite higher health insurance exclusion rates for Hispanic households.

The higher health insurance exclusion rate among low-income Hispanic households may be partly explained by a relatively larger share of non-U.S. citizens in these households (30 percent of Hispanic low-income households are non-U.S. citizens). Non-U.S. citizens are unlikely to be eligible for Medicaid, a government program that helps with health-care costs for people with limited incomes. Consistent with this explanation, a counterfactual calculation based on the ACS shows that if households receiving Medicaid were no longer covered by the program and had no replacement plan, their health insurance exclusion rates would increase substantially, especially among households with no high school diploma and Black households of any education level. For households with no high school diploma, the rate would increase by 58 percentage points for Black households, 42 percentage points for Hispanic households, and 41 percentage points for white households. For households with some college or a college degree, the rate would increase by 38 percentage points for Black households, 33 percentage points for Hispanic households, and 26 percentage points for white households. These findings suggest that government programs such as Medicaid may improve health insurance inclusion for households with low educational attainment and reduce racial disparities between Black and white households in health insurance coverage.

Initiatives to Advance Inclusion and the Role of Education

Knowing more about the types of exclusion, household characteristics, and the degree to which low-income households experience exclusion may be helpful in addressing them. Various initiatives are already underway, led by federal, state, or local governments; legislators; community groups; industries; or partnerships across multiple parties.

Digital inclusion initiatives

To provide or maintain internet access for low-income households during the COVID-19 pandemic, many broadband and telephone service providers took the Federal Communications Commission’s (FCC) “Keep America Connected Pledge” (Toh and Tran 2020). More recently, the Consolidated Appropriations Act 2021 directed the FCC to establish the Emergency Broadband Benefit Program, which grants qualifying low-income households a discount on the cost of broadband service and certain connected devices until either the $3.2 billion fund runs out or six months after the public health emergency ends (FCC 2021a). In April 2021, federal legislators introduced the “Promoting Access to Broadband Act of 2021,” which would help states increase awareness and enrollment in the FCC’s current Lifeline Program, which provides a monthly $9.25 subsidy to qualifying low-income households to help them pay for their broadband and telephone service (Benton Institute for Broadband & Society 2021; FCC 2021b).

Many state and local governments have been actively promoting digital inclusion._ For example, in 2020, the California Broadband Council published the “Broadband for ALL” action plan, which includes the goal of all Californians having access to affordable high-speed broadband, with necessary devices, training, and support (California Broadband Council 2020). At the city level, the Cleveland Foundation and T-Mobile partnered to create the Greater Cleveland Digital Equity Fund to address the digital divide (Cleveland Foundation 2020)._ Digital inclusion programs may also become increasingly supported by banks; the Office of the Comptroller of the Currency (OCC) added such programs to its list of qualifying activities for consideration under the Community Reinvestment Act (OCC 2020).

Financial inclusion initiatives

Financial institutions and local governments are collaborating under the Bank On movement, which is led by the Cities for Financial Empowerment (CFE) Fund, a national nonprofit organization. Bank On is designed to improve the financial stability of Americans currently outside of the mainstream banking system by making safe, low-cost transaction accounts accessible to all. The CFE Fund certifies bank and credit union accounts that meet the Bank On National Account Standards, which include low costs, no overdraft fees, and robust transaction capabilities through debit and prepaid cards, online bill pay, and greater access to out-of-network ATMs. The CFE Fund certified 60 bank and credit union accounts as meeting newly updated standards for 2021 and 2022, and these accounts are available in all 50 states and the District of Columbia (CFE Fund 2021).

In addition, financial technology companies, or fintechs, have increasingly offered consumers accounts that function like a bank account. These fintechs include PayPal, neobanks, and providers of general purpose reloadable (GPR) prepaid cards. PayPal enables U.S. consumers who have a PayPal Cash Plus account or Venmo account to receive direct deposits. Neobanks such as Chime and Current offer consumers digital accounts through partnerships with depository institutions (Bradford 2020). Typically, neobank accounts are FDIC-insured and have features such as no minimum balance requirement, faster access to direct deposit funds, free overdrafts up to a certain amount for qualifying customers, and tools to meet account holders’ savings goal. GPR prepaid cards have similar features to neobank accounts, though many prepaid cards have no overdraft capability. These fintech products do not necessarily reduce the financial exclusion rate as defined in this article; nevertheless, they enable unbanked consumers to access digital financial services.

Health insurance inclusion initiatives

Federal and state governments play an important role in improving health insurance inclusion. As discussed previously, Medicaid is a key program to address low health insurance coverage or racial disparity in health insurance coverage among low-income households. Although a provision in the Affordable Care Act (ACA) called for the expansion of Medicaid eligibility to adults below age 65 with income up to 133 percent of the federal poverty level, states have been allowed to decide individually whether to participate. Participating states pay a small portion of the cost of expanding Medicaid, and the rest is financed by the federal government. As of May 2021, 38 states and the District of Columbia have participated in the Medicaid expansion, and 12 states have not (Kaiser Family Foundation 2021)._ The ACA also created the Health Insurance Marketplace (or Exchange), a shopping and enrollment service for health insurance mainly for low- or moderate-income individuals and families. Marketplace plans are relatively low cost and those enrolled may qualify for tax credit and other cost savings.

Community-based charitable care programs, which historically provided affordable health care to people without health insurance coverage, now focus more on assisting low-income individuals with enrolling in Medicaid or Marketplace plans (Crawford 2016). These programs also reach out to hard-to-reach populations and educate them about health insurance coverage options.

The potential role of education in promoting inclusion

Although our results cannot establish causality between educational attainment and digital, financial, and health insurance exclusion, if causality exists—and higher educational attainment leads to lower exclusion rates—government or community initiatives that encourage low-income households to earn a high school diploma or higher degree may help reduce exclusion in the future. These initiatives may be particularly helpful for Black and Hispanic low-income households for two reasons. First, as we showed, the racial gap in exclusion rates is narrower for households with higher educational attainment, which may suggest that increasing educational attainment could do more to reduce exclusion rates for Black and Hispanic households than for white households. Second, Black and Hispanic low-income households tend to have lower educational attainment compared with white low-income households. According to the FDIC survey, the share of households with no high school diploma is the highest among Hispanic households (40 percent), followed by Black households (21 percent) and white households (14 percent)._ Thus, a relatively large share of Black and Hispanic households may have an opportunity to improve their educational attainment and thus reduce exclusion (again, if causality between education and exclusion exists).

Although higher educational attainment might reduce various types of exclusion in the future, existing digital exclusion may be a barrier to higher educational attainment. The COVID-19 pandemic has forced many students to attend online classes, creating learning challenges for children in low-income households—particularly Black and Hispanic households—that are more likely to lack home internet access. Digital inclusion is a key component for improving educational attainment and narrowing the racial divide in education.

Conclusion

In this article, we uncover the degree to which low-income households experience digital, financial, and health insurance exclusion and assess how multiple types of exclusion are correlated with education and race. We find that more than 10 percent of low-income households experienced multiple types of exclusion in 2019. Among them, those with lower educational attainment were more likely than those with higher educational attainment to experience multiple types of exclusion. This correlation between educational attainment and exclusion is common across all races and ethnicities, though Black and Hispanic households are more likely to experience multiple types of exclusion than white households.

Knowing these detailed statistics may help policymakers and community and business leaders assess the progress of initiatives to advance digital, financial, and health insurance inclusion and develop effective future policies and strategies. Due to the COVID-19 pandemic, low-income households that experienced digital, financial, and health insurance exclusion may have incurred disproportionally severe hardship. By collaboratively developing effective policies and strategies for the inclusion of low-income households, governments, community groups, and industry participants may also help minimize the longer-term negative effects of the pandemic on those households.

Endnotes

-

1 Although our definition of digital exclusion is common to both surveys, the FDIC survey, which is a supplement of the Current Population Survey (CPS), estimates the rate of digital exclusion to be higher than the ACS. This is due to differences in survey question wording, data collection methods, and the weights given to individual responses. See Ryan (2018) for details.

-

2 Among these households, 4 percent experienced financial exclusion but not digital exclusion, and 9 percent experienced health insurance exclusion but not digital exclusion. Thus, no more than 4 percent of households experienced both financial and health insurance exclusion but not digital exclusion. If households that experienced both digital and financial exclusion (6 percent) and households that experienced both digital and health insurance exclusion (2 percent) are mutually exclusive, all three groups of households are mutually exclusive, suggesting that the maximum percent of households that experienced multiple exclusions is 12 (4 + 6 + 2) percent.

-

3 This is consistent with Hayashi and Minhas (2018), who use the 2015 FDIC survey and find that education and race are highly associated with low-income households’ probability of being unbanked.

-

4 The Pew Charitable Trusts maintains the State Broadband Policy Explorer, an online database that includes state statutes related to broadband as of January 1, 2021 (Pew Charitable Trusts 2021).

-

5 See Partners Bridging the Digital Divide (2021) for a list of digital inclusion initiatives.

-

6 According to the 2019 ACS, the health insurance exclusion rate is significantly lower for low-income households residing in states that have participated in the Medicaid expansion than for those residing in states that have not, even after controlling for educational attainment and race: the rate for the former is about half the rate of the latter. State participation varies by census region; as of May 2021, eight of 12 states that have not participated in the Medicaid expansion are in the South, three are in the Midwest, and one is in the West.

-

7 Educational attainment among Hispanic low-income households varies significantly between those with householders who were born in foreign countries (foreign-born households) and those with householders who were born in the United States (U.S.-born households). According to the FDIC survey, the share of households with no high school diploma is 53 percent among foreign-born Hispanic low-income households and 26 percent among U.S.-born Hispanic low-income households. Among Hispanic low-income households, foreign-born households account for slightly more than 50 percent. Younger households (those with a householder who is younger than 35 years old) are more likely to have higher educational attainment than those with middle-age or older householders, and the racial disparity in educational attainment is narrower for younger households than for middle-age or older households.

References

Benton Institute for Broadband & Society. 2021. “External LinkBill to Increase Access to Broadband Service for Low-Income Americans.” Press release, April 14.

Bradford, Terri. 2020. “External LinkNeobanks: Banks by Any Other Name?” Federal Reserve Bank of Kansas City, Payments System Research Briefing, August.

California Broadband Council (CBC). 2020. External LinkCalifornia Broadband for All. Sacramento: CBC.

CFE Fund. 2021. “External LinkBank On Certified Accounts Help Hundreds of Thousands of Residents Receive Stimulus and Other Emergency Payments Safely and with Social Distance.” Press release, January 27.

Cleveland Foundation. 2020. “External LinkCleveland Foundation, Cuyahoga County and T-Mobile Partner to Launch the Greater Cleveland Digital Equity Fund.” Press release, July 16.

Crawford, Maria. 2016. “External LinkThe Evolution of Charity Care Programs to Support Enrollment in Health Coverage.” Center for Health Care Strategies, July.

FCC (Federal Communications Commission). 2021a. “External LinkEmergency Broadband Benefit Program.”

———. 2021b. “External LinkLifeline Program for Low-Income Consumers.”

Hayashi, Fumiko, and Sabrina Minhas. 2018. “External LinkWho Are the Unbanked? Characteristics Beyond Income.” Federal Reserve Bank of Kansas City, Economic Review, vol. 103, no. 2.

Kaiser Family Foundation (KFF). 2021. “External LinkStatus of State Medicaid Expansion Decisions: Interactive Map.” KFF, June 29.

McMorrow, Stacey, Laura Skopec, and Tyler W. Thomas. 2019. “External LinkEducation and Health: Long-Term Trends by Race, Ethnicity, and Geography, 1997–2017.” Urban Institute, May.

OCC (Office of the Comptroller of the Currency). 2020. “External LinkOCC Finalizes Rule to Strengthen and Modernize Community Reinvestment Act Regulations.” Press release, May 20.

Partners Bridging the Digital Divide. 2021. “External LinkPublic Policy Initiatives.”

Perrin, Andrew, and Sara Atske. 2021. “External Link7% of Americans Don’t Use the Internet. Who Are They?” Pew Research Center, April 2.

Pew Charitable Trusts. 2021. “External LinkState Broadband Policy Explorer.” Pew Charitable Trusts, April 12.

Ryan, Camille. 2018. “External LinkComputer and Internet Use in the United States: 2016.” U.S. Census Bureau, August.

Toh, Ying Lei, and Thao Tran. 2020. “External LinkHow the COVID-19 Pandemic May Reshape the Digital Payments Landscape.” Federal Reserve Bank of Kansas City, Payments System Research Briefing, June.

Fumiko Hayashi is a research and policy advisor at the Federal Reserve Bank of Kansas City. Rebecca Ruiz is a former research associate at the bank. The views expressed are those of the authors and do not necessarily reflect those of the Federal Reserve Bank of Kansas City or the Federal Reserve System.

Author