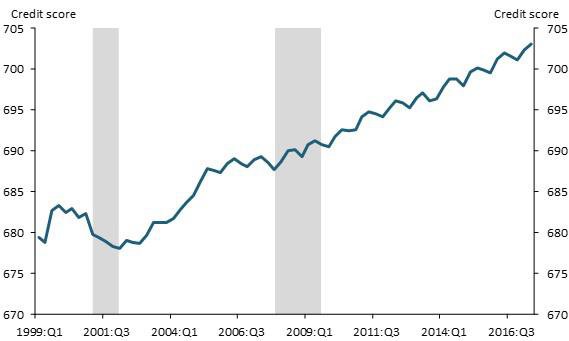

Credit scores for U.S. consumers reached a record high recently. The average consumer credit score hit 700 in the first quarter of 2016 and gradually increased thereafter. As of 2017:Q2, the average score was 703 according to Consumer Credit Panel data from Equifax and the Federal Reserve Bank of New York (FRBNY)._

Equifax credit scores—known as the “Equifax Risk Score”—range from 280 to 850: consumers with scores above 700 are typically classified as having good credit, while consumers with scores below 660 are considered subprime borrowers. Chart 1 shows the evolution of the average credit score from 1999:Q1 to 2017:Q2._ While the average credit score declined noticeably during the 2001 recession, it generally trended up thereafter with only occasional deviations. Interestingly, the Great Recession of 2007–09 did not reverse this long-term trend.

Chart 1: Average Consumer Credit Score

Source: Equifax and FRBNY Consumer Credit Panel.

The long-term upward trend challenges the view of some media commentators that the uptick in credit scores has been driven by the rebound from the Great Recession._ But if cyclical forces aren’t at play, what might explain the trend? One likely candidate is an aging population. Older people tend to have much higher credit scores on average than younger people: indeed, the average credit score in 2017:Q2 increased monotonically from 643 for people younger than 25 to 761 for people older than 64._

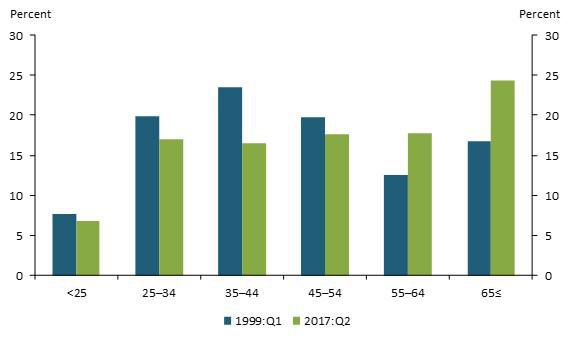

Demographic trends support this interpretation. Chart 2 shows changes in the demographics of U.S. credit applicants from 1999:Q1 to 2017:Q2 based on Consumer Credit Panel data. The share of the oldest age group (people older than 64) in the entire population of credit applicants increased dramatically from 16.7 percent in 1999:Q1 to 24.4 percent in 2017:Q2. In addition, the population share of the next oldest age group (people age 55 to 64) increased from 12.5 percent to 17.8 percent over the same time period. The population shares for all other age groups declined.

Chart 2: Population Share of Age Groups

Source: Equifax and FRBNY Consumer Credit Panel.

To isolate the effect of an aging population on the average credit score, I decompose changes in the average credit score holding either credit scores or the population shares of each age group fixed. Note that the average credit score for the entire population is an average of age-group-specific average credit scores (CSi) weighted by the share of each age group (Popi) in the whole population. The decomposition is as follows:

6

∑ (Popi,2017Q2 * CS i,2017Q2 - Popi,1999Q1 *CSi,1999Q1)=

i=1

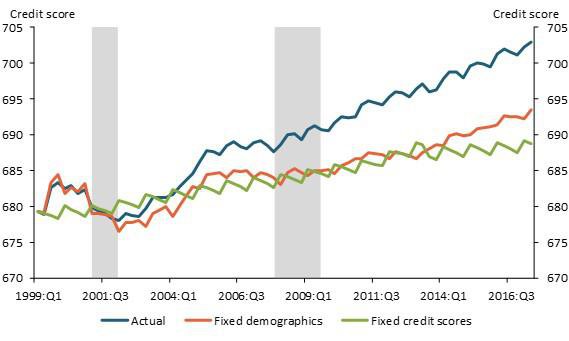

The last term in this decomposition represents the interaction between changes in population shares and changes in age-group-specific average credit scores and is typically very small compared with the other terms. Chart 3 shows two counterfactual average scores along with the actual average credit score. The green line, which takes into account only population changes, explains 43 percent of the increase in the average credit score from 1999:Q1 to 2017:Q2. The orange line, which reflects the upward trend in average credit scores for each age group, explains the remaining 57 percent.

Chart 3: Actual and Counterfactual Average Consumer Credit Score

Note: Gray bars denote National Bureau of Economic Research (NBER)-defined recessions.

Source: Equifax and FRBNY Consumer Credit Panel.

Since consumer debt balance generally peaks at the middle age (about 45) and gradually decreases as people age, people older than 55 are unlikely to increase credit demand. Therefore, the recent improvement in the average consumer credit score might have a somewhat limited effect in boosting consumer credit demand to the extent that an aging population explains a significant portion of that improvement.

Additional Files: Data

Taeyoung Doh is a senior economist at the Federal Reserve Bank of Kansas City. Amy Oksol, a research associate at the bank, helped prepare the bulletin. The views expressed are those of the author and do not necessarily reflect the positions of the Federal Reserve Bank of Kansas City or the Federal Reserve System.

Endnotes

-

1 The Consumer Credit Panel is a nationally representative sample of individual credit scores covering 5 percent of all adults with a Social Security number and a credit report. Each quarter, 9 to 11 million individual observations are available.

-

2 I focus on the average score to simplify the counterfactual analysis to isolate the role of changing demographics. But the median credit score is highly correlated with the average score, with a correlation coefficient of 0.96.

-

3 For example, see External Linkhttps://www.wsj.com/articles/credit-scores-hit-record-high-as-recession-wounds-heal-1496055600

-

4 Another possible factor is that consumers might have increased efforts to keep their credit scores in a good shape, as these scores are used more widely in evaluating the credit quality of consumer loans.

The views expressed are those of the author(s) and do not necessarily reflect the positions of the Federal Reserve Bank of Kansas City or the Federal Reserve System.

Author