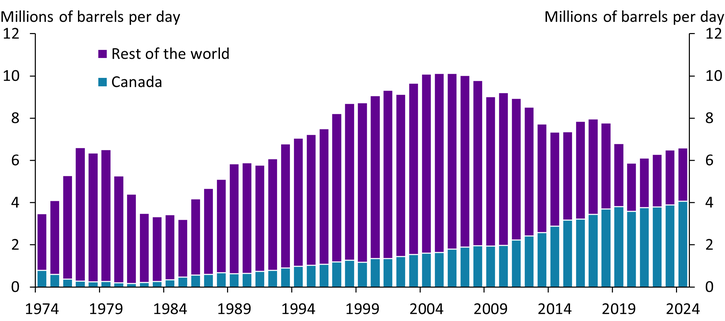

Although total U.S. imports of crude oil have fallen over the past two decades, U.S. imports of Canadian oil have steadily increased. Chart 1 shows that U.S. crude oil imports from Canada (blue bars) averaged 4.1 million barrels per day in 2024, which represents 62 percent of total oil imports. Any trade disruption involving Canadian oil would likely result in higher prices for oil and refined petroleum products such as gasoline, particularly in areas more reliant on Canadian crude.

Chart 1: U.S. imports of Canadian crude oil have steadily increased

Sources: U.S. Energy Information Administration (EIA).

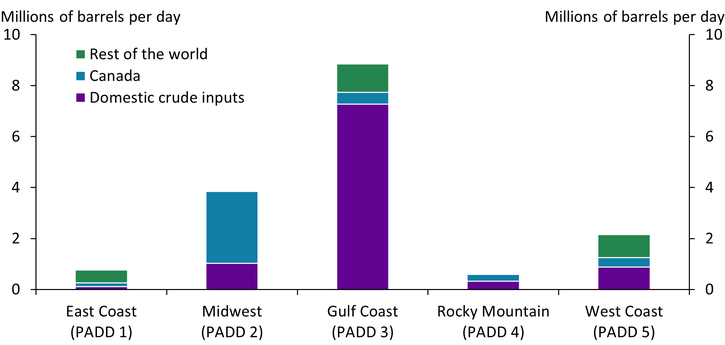

Midwest refineries are likely to be most affected, as most Canadian oil imports are currently refined in the region. Over decades, U.S. refineries have specialized based on type of crude stock and cost of acquiring it. Chart 2 shows the regional variation in where crude oil is sourced for refining. Refineries in the Gulf Coast, the region with the largest refining capacity, primarily process domestic crude (purple bar), with Canadian crude accounting for less than 0.5 million barrels per day or about 5 percent of total crude inputs. In contrast, refineries in the Midwest process 2.8 million barrels per day of Canadian oil, which represents 73 percent of crude inputs in the region. Overall, more than 70 percent of U.S. imports of Canadian crude oil are refined in the Midwest.

Chart 2: Canada is the largest input source for Midwest refineries

Notes: Data are for 2024. PADD (Petroleum Administration for Defense Districts) refers to the five geographic regions into which the United States is divided for petroleum administration purposes.

Sources: U.S. EIA.

This regional variation in input sourcing reflects that refineries have become more specialized over time to receive and process certain types of oil. Most of the crude oil extracted in the United States is high quality, referred to as light sweet crude, while the oil imported from Canada is a heavy sour crude that requires additional processing to remove sulfur and break down its heavy molecules into lighter, more valuable products (EIA 2022). The refining equipment for heavy sour crude is significantly more complex and extensive than for light sweet crude. As a result, a refinery with equipment to process heavy sour crude cannot easily switch to refining a different type of oil.

Pipeline infrastructure is also a key factor in why refiners have become specialized in sourcing crude inputs. Although the capital cost of installing pipelines is higher compared with transporting via rail, barge, or truck, a pipeline has lower operating costs (Wilkerson and Cakir Melek 2014). The pipeline system used to move crude oil is mostly concentrated in the Midwest down to the Gulf Coast, which means the transportation cost of crude oil is typically lower in the Midwest. The commodity share of the total cost of refinement is higher in the Midwest, which means oil price changes have more direct effects on the price of gasoline compared with other parts of the country (Kilian and Zhou 2024). Because most refined products produced in the Midwest are also consumed in the Midwest, changes in input costs for Midwest refiners most directly affect Midwest consumers and businesses.

Midwest refiners thus would potentially face a tradeoff if the price of Canadian crude increases: either pay the higher cost of Canadian crude oil or find another source of heavy sour crude. However, other potential sources of heavy sour crude oil in South America or the Middle East would likely be more expensive to import into the Midwest for processing as the transportation costs would be higher.

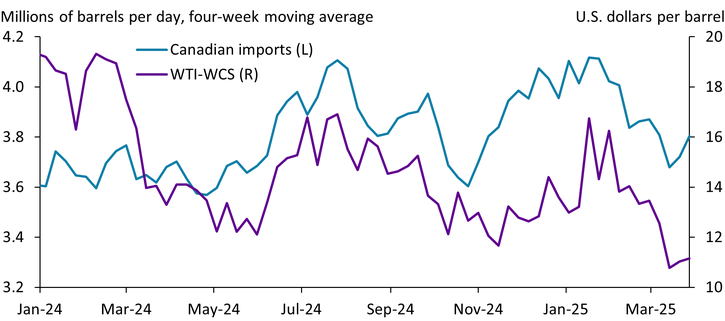

As a result, refiners may not reduce their imports of Canadian crude after tariffs, as the higher price may still be lower than alternatives. Due to differences in the quality of oil, Western Canadian Select (WCS) trades at a discount relative to the U.S. benchmark West Texas Intermediate (WTI). Chart 3 shows that the spread between WTI and WCS was around $19 per barrel in January 2024 but narrowed to around $11 per barrel in March 2025 (purple line). Despite a lowering in the price spread, U.S. imports of Canadian oil have remained in a narrow band between 3.6 and 4.1 million barrels per day (blue line). Although the proposed tariffs on Canadian oil may cause the price spread to increase, the actual effect on prices would depend on how Canadian sellers and U.S. refineries split the cost, which in turn is likely to depend on the availability of substitute buyers for Canadian sellers and the cost of substitute suppliers for U.S. refineries. Importing oil through the existing pipeline infrastructure between Canada and the United States may still be the most profitable option for refineries, even with tariffs.

Chart 3: The WTI-WCS price spread has narrowed over the past year

Note: Imports and prices as of March 28, 2025.

Sources: U.S. EIA and Bloomberg.

Canada’s planned expansions for its own pipeline infrastructure could further reduce the price spread making it more profitable to export to other countries. Recently, Canada has made significant investments in expanding its pipeline infrastructure to its western coast, aiming to diversify its oil export markets beyond the United States. The most notable project is the Trans Mountain Expansion Project (TMX), which increased the pipeline’s capacity from 300,000 to 890,000 barrels per day (Lincoln, Rheault, and Malkin 2025). Completed in May 2024, the TMX enables Canadian crude to reach international markets via the Port of Vancouver, reducing reliance on U.S. refineries and potentially further narrowing the discount between WTI and WCS.

Thus far in 2025, the WTI price of oil has trended lower due to slowing global growth and increases in the supply of oil. As a result, U.S. average and Midwest gasoline prices have also moved lower. In the near term, Midwest refineries likely have limited ability to find non-Canadian sources of heavy sour crude at low cost. Similarly, Canadian oil producers are reliant on the U.S. market. Although Canada has added additional pipeline to its western coast for shipping to export markets, in 2024 it exported around 95 percent of its crude oil to the United States (Statistics Canada 2025). The incidence of any tariffs are likely to be split between Canadian producers, Midwest refiners, and Midwest consumers. The split will likely be determined by the availability of substitutes across all three groups.

Article Citation

Brown, Jason P., and Bobby Beckemeyer. 2025. "Canadian Oil Important for Midwest Gasoline Prices." Federal Reserve Bank of Kansas City, Economic Bulletin, May 9.

References

EIA (U.S. Energy Information Administration). 2022. “External LinkThe United States Produces Lighter Crude Oil, Imports Heavier Crude Oil.” October 11.

Kilian, Lutz, and Xiaoqing Zhou. 2024. “External LinkHeterogeneity in the Pass-Through from Oil to Gasoline Prices: A New Instrument for Estimating the Price Elasticity of Gasoline Demand.” Journal of Public Economics, vol. 232, April.

Lincoln, Daniel, Phillippe Rheault, and Anton Malkin. 2025. “External LinkTCI Energy Brief: Early TMX Pipeline Expansion Data Reveals China's Emerging Role as a Significant Buyer of Canadian Crude, Offering Some Diversification from the U.S. Market.

Wilkerson, Chad, and Nida Çakır Melek. 2014. “Getting Crude to Market: Central U.S. Oil Transportation Challenges.” Federal Reserve Bank of Kansas City, The Main Street Economist, no. 1.

Statistics Canada. 2025. “External LinkAnother Record Year for Canadian Crude Oil: Crude Oil Year in Review, 2024.” March 20.

Jason P. Brown is a vice president and economist at the Federal Reserve Bank of Kansas City. Bobby Beckemeyer is a research associate at the bank. The views expressed are those of the authors and do not necessarily reflect the positions of the Federal Reserve Bank of Kansas City or the Federal Reserve System.

Authors

Jason P. Brown

Vice President and Economist