Nebraska’s economy generally remained strong throughout 2015, but some signs of weakness have steadily emerged. Through November, Nebraska’s unemployment rate was one of the lowest in the nation and job gains were steady among the state’s various service-providing firms. Businesses have expressed general optimism about prospects for future growth and real estate markets have continued to strengthen. Nevertheless, employment growth in Nebraska, compared with the United States overall, was somewhat sluggish in 2015, primarily due to job losses in the manufacturing sector. In addition, agricultural and export-oriented businesses have faced persistent headwinds from low commodity prices and a stronger U.S. dollar, factors that may continue to pressure Nebraska’s economy in 2016.

Signs of Strength

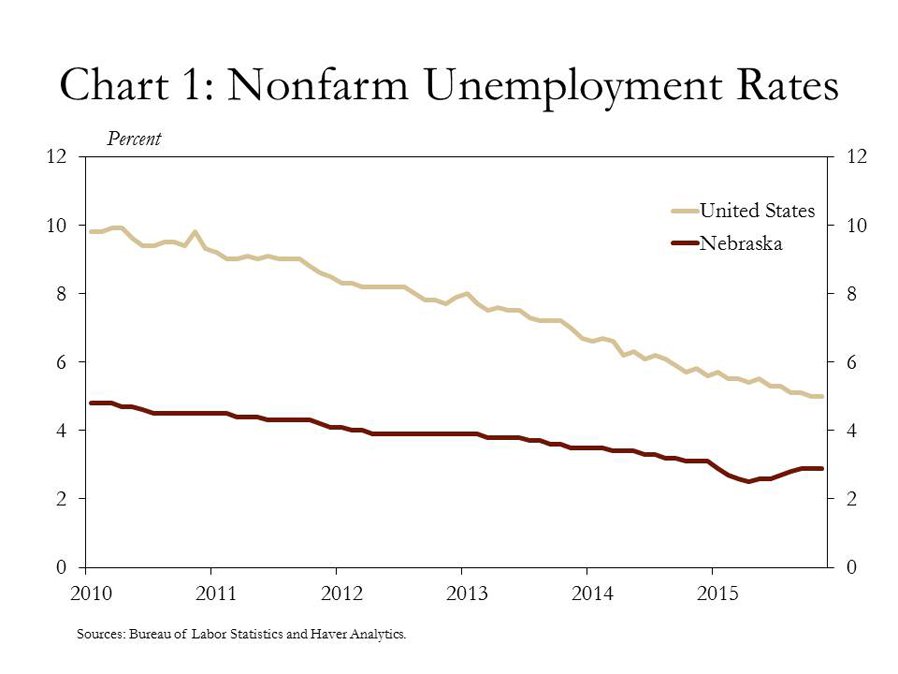

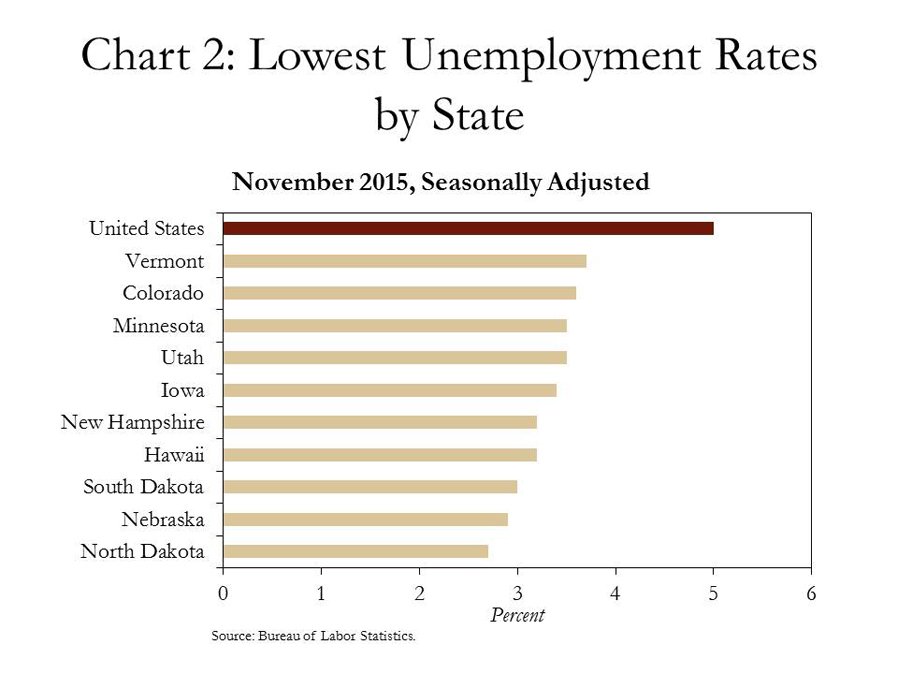

Reflecting a generally solid labor market, overall unemployment in Nebraska remained low in 2015. Despite some recent increases, Nebraska’s unemployment rate of 2.9 percent was significantly lower than the national rate of 5.0 percent through November (Chart 1). Moreover, Nebraska has remained one of only two states with an unemployment rate lower than 3.0 percent (Chart 2).

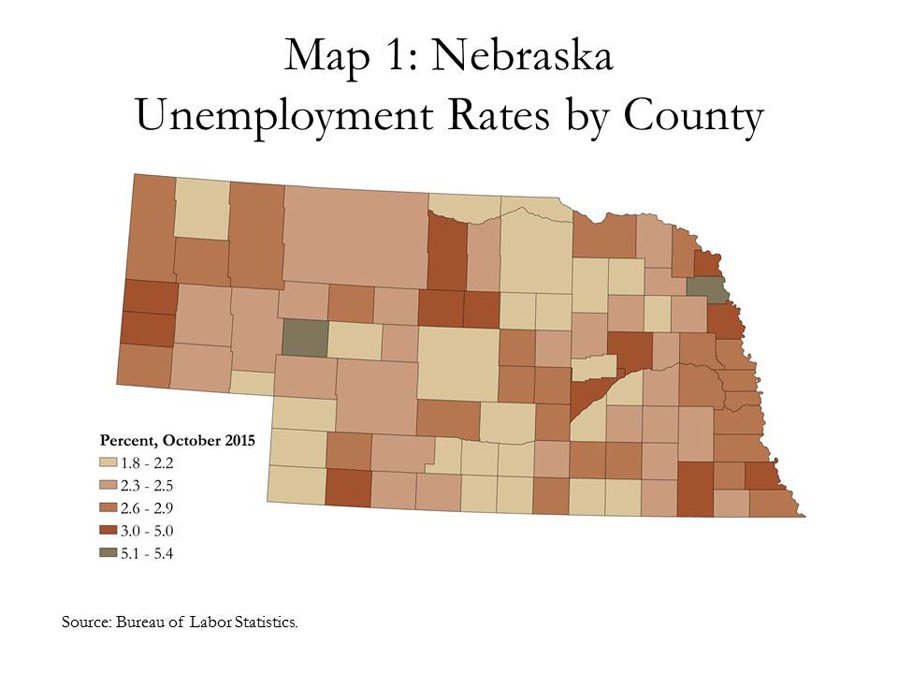

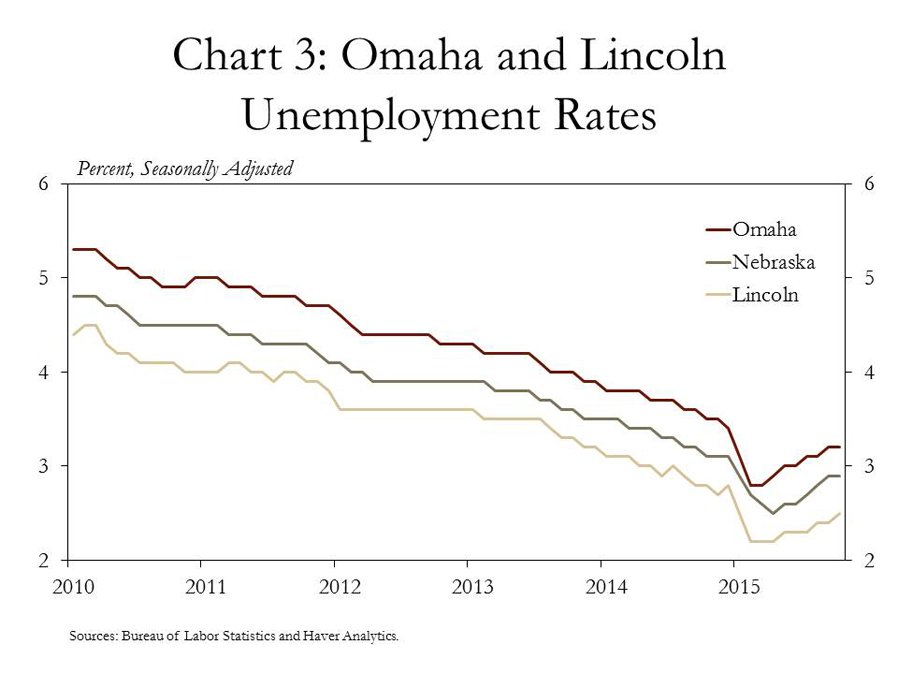

Statewide, the unemployment rate in all but two of Nebraska’s 93 counties was below the national average through October. Only Arthur County (5.4 percent) and Thurston County (5.2 percent) were above the national average (Map 1). The unemployment rate in Thurston County, however, was significantly lower than a year ago, and Arthur County is the state’s least-populated county, meaning small changes in employment may amplify the overall effect on the county’s unemployment rate. In addition to low unemployment across counties, unemployment rates in both the Omaha and Lincoln metro areas were lower than a year ago (Chart 3).

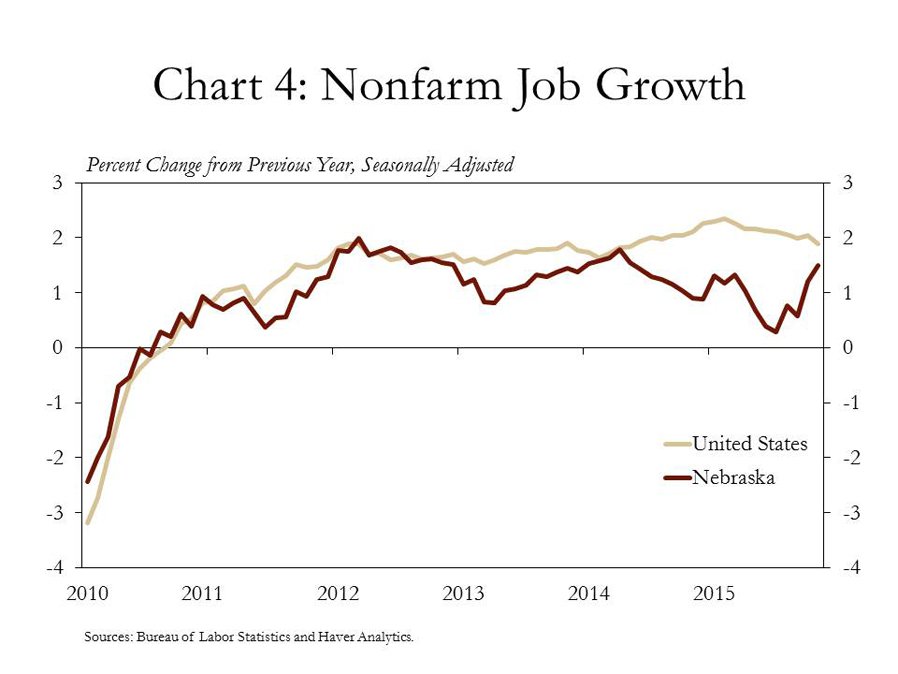

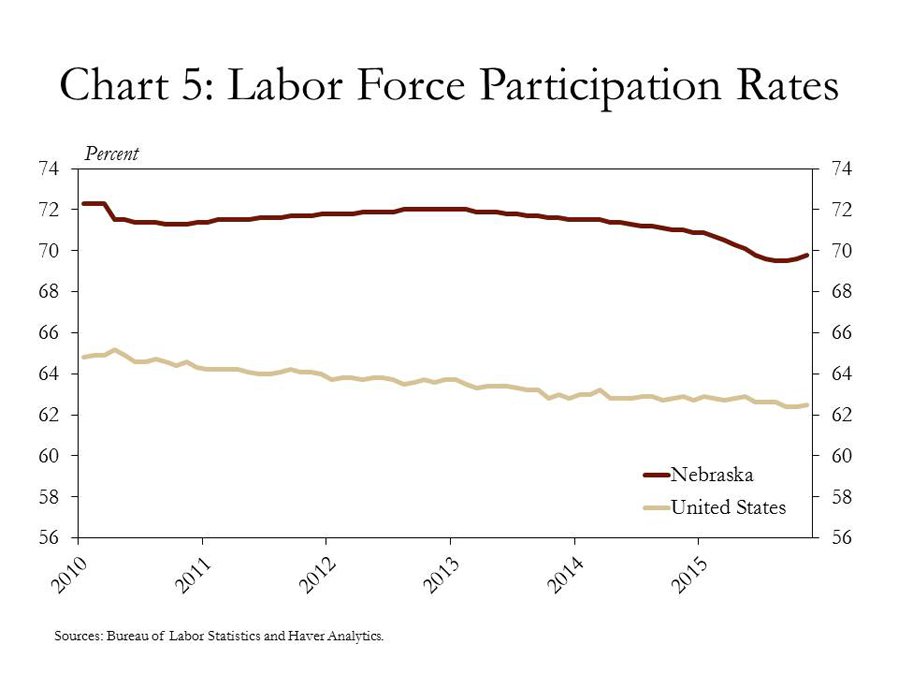

Other indicators also have pointed to a relatively strong labor market. Job growth in Nebraska, which averaged only 0.5 percent during the summer, picked up to 1.5 percent in November (Chart 4). And while the labor force has declined somewhat over the past year, the labor force participation rate edged up slightly toward the end of 2015, and Nebraska continued to post a substantially higher participation rate than the nation (Chart 5). Initial weekly unemployment insurance claims were also 35 percent lower at the end of November compared with a year earlier, another sign of strengthening conditions in the labor market.

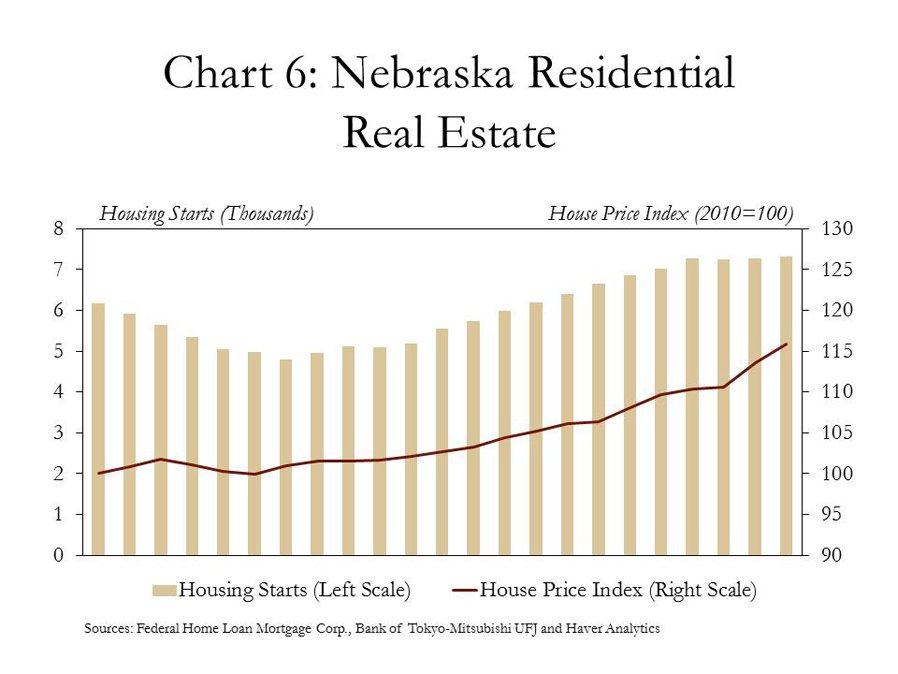

Outside of labor markets, business sentiment and real estate markets also have supported an optimistic view of Nebraska’s economy. The University of Nebraska-Lincoln College of Business Administration’s “Leading Economic Indicator,” which seeks to predict the state’s economic growth six months ahead, increased 1.7 percent in October._ In the previous five months, the indicator had gained an average of only 0.2 percent. Moreover, although growth in housing starts slowed in 2015, the level has remained relatively high and residential home prices have continued to rise steadily (Chart 6).

Nascent Cracks

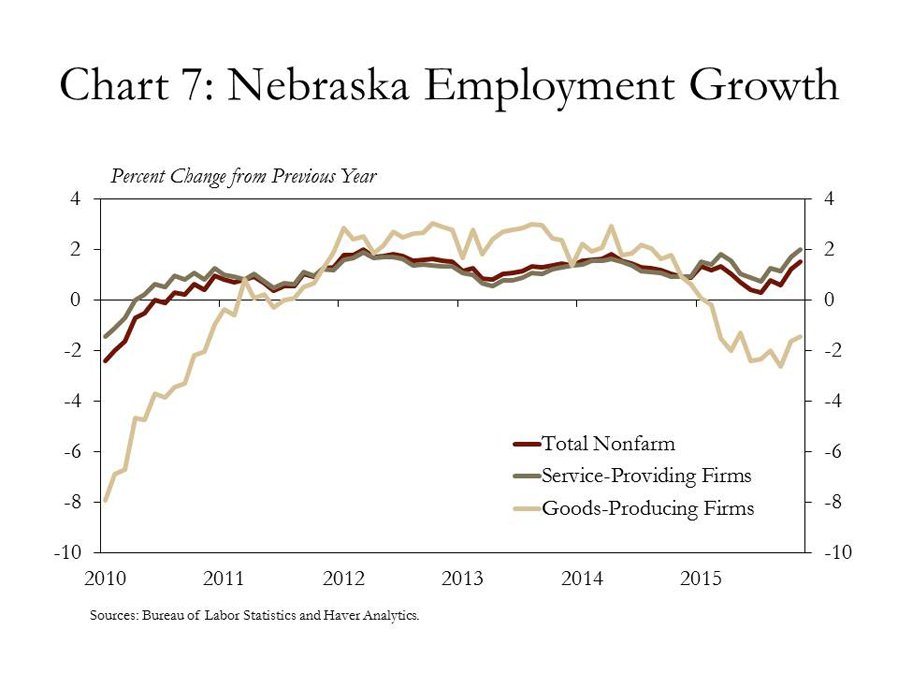

Across industries in Nebraska, some firms continued to add jobs in 2015 while others scaled back. Employment growth among service-providing firms continued to drive job gains in the state, with monthly growth through November averaging 1.4 percent (Chart 7). In contrast, job losses continued to mount at Nebraska’s goods-producing firms, where employment has declined 0.9 percent since the beginning of 2015.

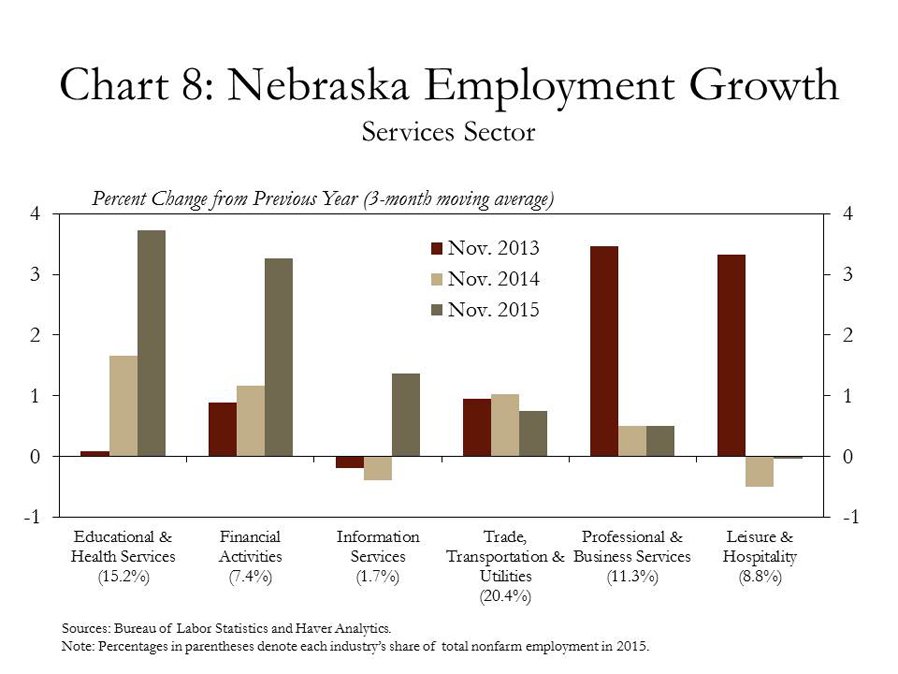

Although some service-providing firms in Nebraska continued to expand, the rate of job growth has been less than the nation and some industries have weakened noticeably. Consistent with recent trends, job gains among education and health services firms continued to drive employment growth in the services sector (Chart 8). In fact, gains in this industry accounted for about half of the state’s net job growth through November. Finance companies also significantly increased hiring toward year’s end. Employment growth at professional and business services firms, however, faltered in 2015, and growth softened considerably in the leisure and hospitality industry, in contrast to national trends.

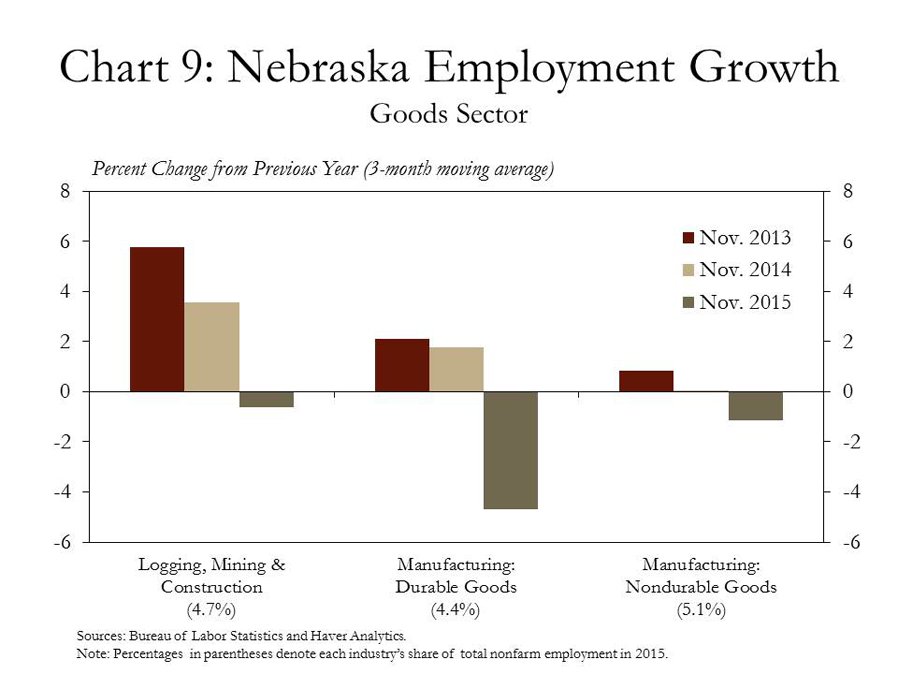

In addition to sluggish growth among some service-providing firms, job growth in the manufacturing sector has been poor. Since January 2015, Nebraska manufacturers have cut 2,300 jobs, or 2.4 percent of the workforce, whereas manufacturing employment nationally has remained relatively steady (Chart 9). The majority of Nebraska’s job losses in manufacturing occurred among producers of durable goods, a sector that includes manufacturing of agricultural and industrial equipment.

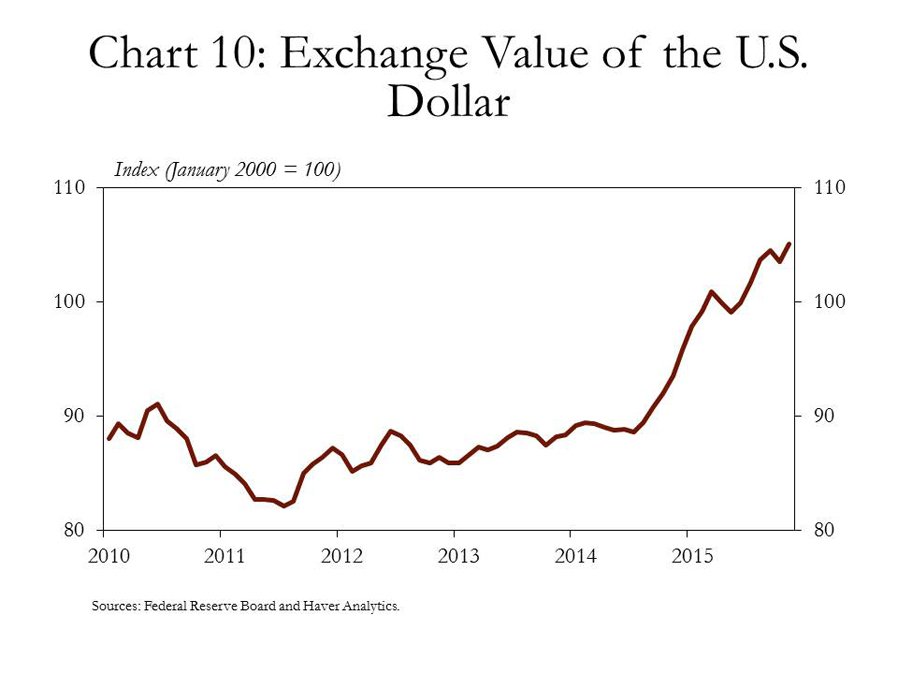

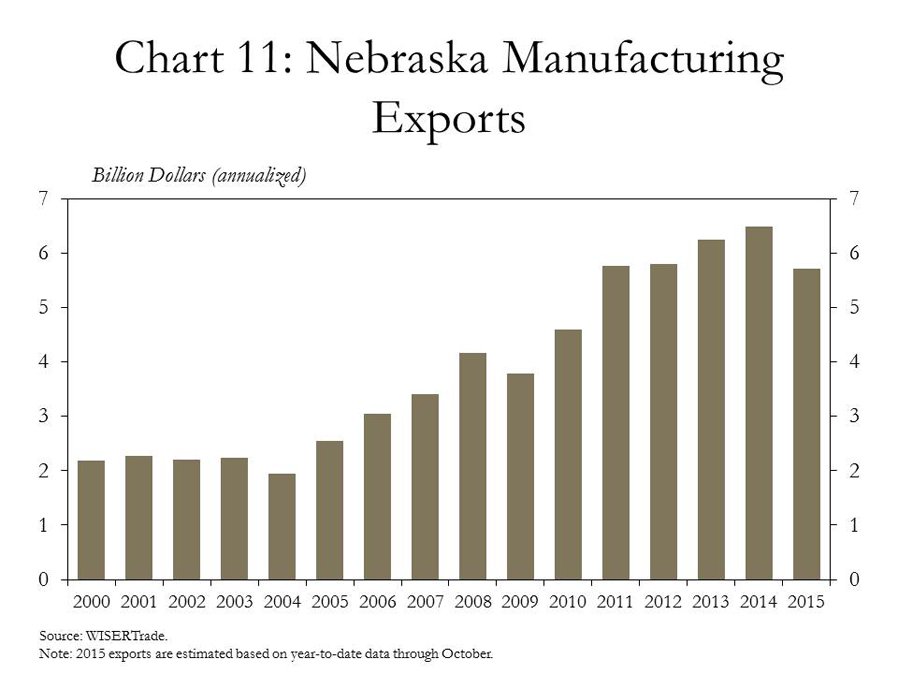

Due in part to a stronger U.S. dollar, manufacturing exports originating from Nebraska were notably weaker in 2015. Since November 2014, the dollar has surged 12 percent as a broad index against other currencies, continuing to make U.S. exports more expensive for foreign buyers (Chart 10). Alongside a stronger dollar, manufacturing exports in 2015 were on pace to decline nearly 12 percent from the previous year (Chart 11).

Downturn in the Farm Economy

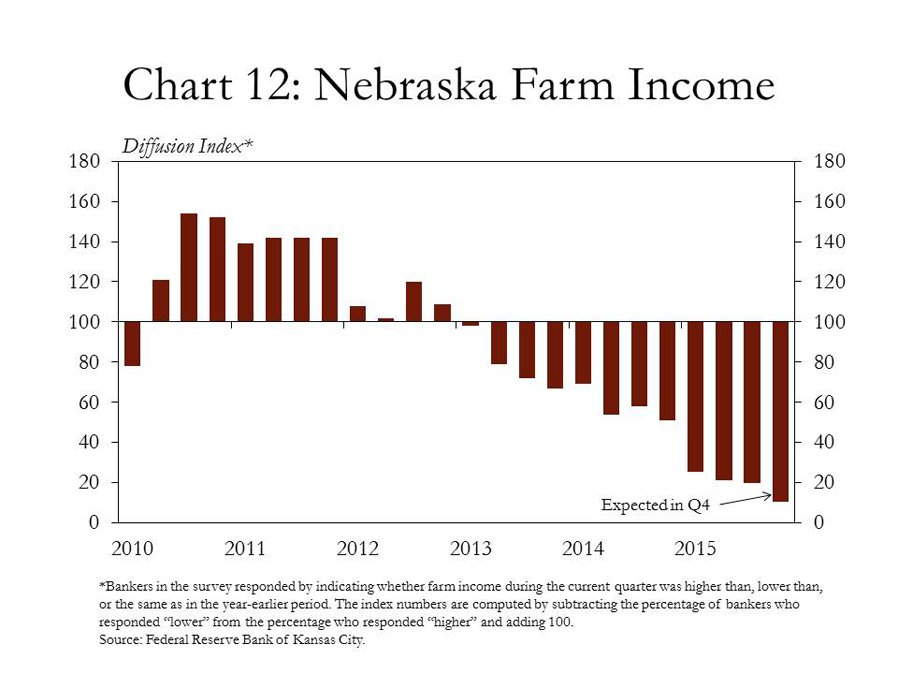

Also dependent on foreign export markets, Nebraska’s agricultural economy continued to weaken in 2015. Following several years of strong profit margins driven by high crop prices, farm income in Nebraska continued to languish in 2015. Bankers in Nebraska indicated income in the state’s farm sector declined in each quarter over the past year, and they expected income in the sector to weaken further in the fourth quarter of 2015 (Chart 12).

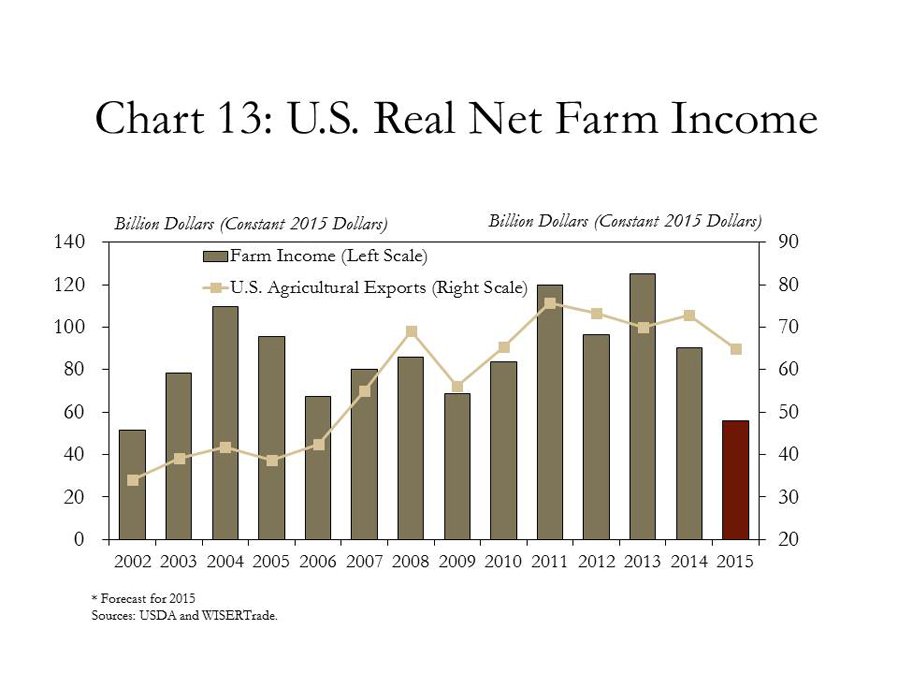

The softening in Nebraska’s agricultural economy has mirrored that of the nation. Since 2013, the forecast for U.S. farm income was a decline of 55 percent in 2015, primarily due to lower profits in the crop sector, but also some softening in the livestock sector (Chart 13). Similar to sluggish manufacturing exports, the value of U.S. agricultural exports also dropped by approximately 12 percent in 2015 from the previous year. If the year’s pace through October continued to year’s end, the annual value of agricultural exports for 2015 would be the lowest since 2009.

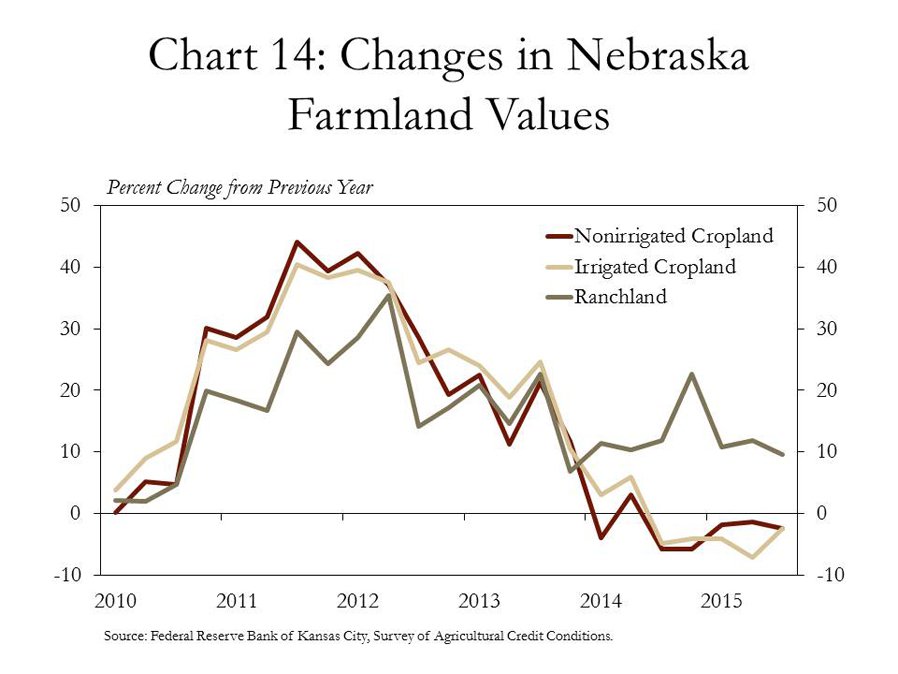

Unlike residential real estate markets, prices for farm real estate have weakened alongside changes in the state’s agricultural economy. Although the value of ranchland has continued to increase modestly, the values of both irrigated and nonirrigated cropland dropped throughout 2015, continuing a trend from mid-2014 (Chart 14). Expectations that crop prices may remain low in 2016 also have led bankers to expect cropland values to continue to soften in the coming months as well.

Conclusion

Overall, Nebraska’s economy remained relatively strong throughout 2015, but parts of the state’s economy have steadily diverged. Labor markets have held steady alongside modest job growth, and residential real estate markets also continued to improve. However, service-providing firms accounted for most of Nebraska’s employment gains in 2015 and some service-based industries have expanded much more than others. In addition, the state’s manufacturing sector and agricultural economy continued to weaken throughout the year, hampered by relatively weak foreign demand for exports. Looking ahead, Nebraska’s economy generally appears well-positioned, but perhaps not in all industries, and rural areas may continue to face headwinds that have intensified over the past 12 months.

Endnotes

-

1 Eric Thompson and William Walstad, “Nebraska Monthly Economic Indicators: December 18, 2015.” University of Nebraska-Lincoln College of Business Administration, Department of Economics.

The views expressed are those of the authors and do not necessarily reflect the positions of the Federal Reserve Bank of Kansas City or the Federal Reserve System.

Authors

Nate Kauffman

Senior Vice President, Economist, and Omaha Branch Executive; Executive Director of the Center for Agriculture and the Economy