Summer is approaching and bringing with it better weather. The number of consumers receiving the COVID-19 vaccines continues to grow and restrictions on restaurant capacities are beginning to ease. With an eye toward these improving conditions, consumers have pent-up demand for travel, the chance to dine in at restaurants and attend public events. These factors support the outlook for a swift recovery in employment for leisure and hospitality workers. However, a return to pre-pandemic levels of employment for these workers may take more than a surge in consumer spending. Declines in business travel, reduced office occupancy as workers continue to work from home, and limited attendance at conventions may stall the return to peak levels of demand for food and accommodation businesses. This issue of the Rocky Mountain Economist highlights the different factors that support the employment outlook for restaurant, hotel and entertainment workers, as these are the workers that continue to face the most significant levels of job loss due to the pandemic.

Although activity in most sectors continues to approach pre-pandemic levels, with many employees back to work, more than 98,000 jobs at leisure and hospitality businesses in the Rocky Mountain region remain outstanding. Some of these job losses are due to reductions in workforces, but many are due to recent business closures. In New Mexico, 60% fewer small businesses in the leisure and hospitality sector were open this January compared with a year prior; likewise 50% and 40% fewer were open in Colorado and Wyoming, respectively, at the beginning of 2021.

A recovery within the leisure and hospitality sector is important for the region not just because it is where the largest number of jobs are outstanding, but also because workers previously employed in this sector may have fewer opportunities to shift to other industries. Looking to the recovery period over the last decade, if restaurant and hotel workers switched to jobs in other industries, those jobs tended to be in the retail or health-care sectors. However, these sectors also face significant challenges due to the pandemic, limiting the potential for businesses to absorb any flows of workers from the leisure and hospitality sector. In short, the reviving demand for dining and traveling will be key to supporting households tied to the industry.

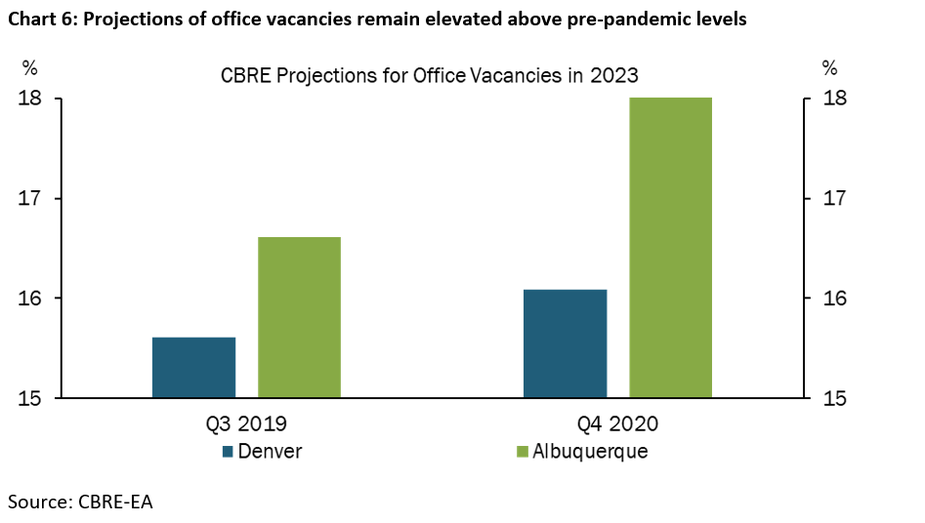

Overall demand for dining and travel includes both consumer activity and demand tied to business activity. And while consumers appear ready to get back out, several factors suggest that the reduction in demand tied to business activity could be more persistent. Before the third wave of COVID-19 washed over the region this past winter, employment at restaurants was picking up. However, that rising swell of employment was not as strong at restaurants and hotels in urban areas, which often are supported by office workers and business travel. Looking ahead, projections for office occupancy in metro areas are elevated for coming years. For example, reported expectations for office vacancies in Denver and Albuquerque in coming years are well above pre-pandemic levels, reducing the potential patronage for downtown restaurants. Thus, after an initial surge in hiring to support pent-up consumer demand, recovery in leisure and hospitality employment may slow to more typical levels seen following historical economic downturns, delaying the return to peak employment.

Leisure and Hospitality Job Losses in the Rocky Mountain Region

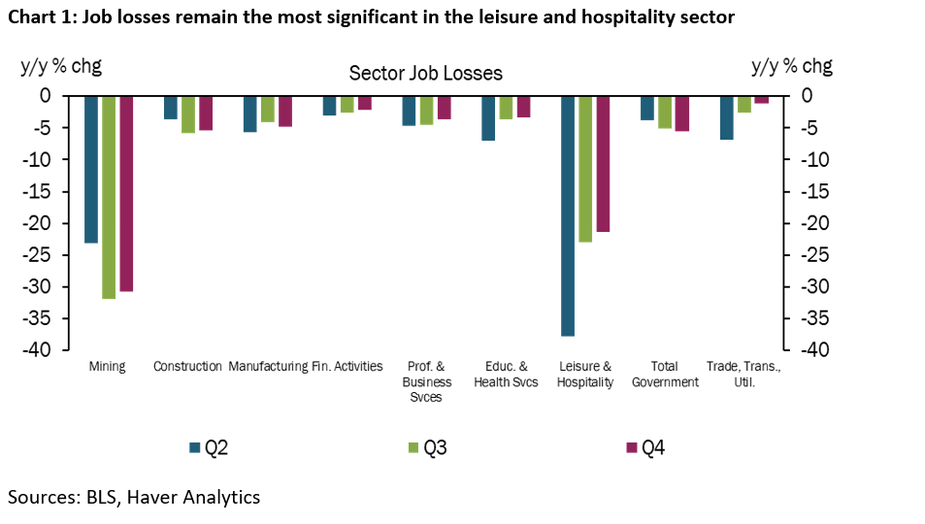

Several sectors of the regional economy experienced steady, though incomplete, recoveries in employment over the past year, yet leisure and hospitality employment stands out with 20% of pre-pandemic employment yet to be recovered. Chart 1 shows the percentage of employment still to be regained in leisure and hospitality exceeds other major industries. Between the second and third quarters of 2020, a significant portion of employment at restaurants or hotels was regained on the heels of support from fiscal policy, adaptations by businesses to serve customers remotely, gains in consumer confidence and eased capacity restrictions before the third wave of the pandemic. But, unlike other portions of the regional economy, recovery in leisure and hospitality stalled through the end of 2020, resulting in about 100,000 fewer jobs compared with the previous year. The outstanding job losses at restaurants, hotels and entertainment venues is contrary to previous recessions, when the percentage decline in leisure and hospitality employment roughly was on par with overall declines in employment on average.

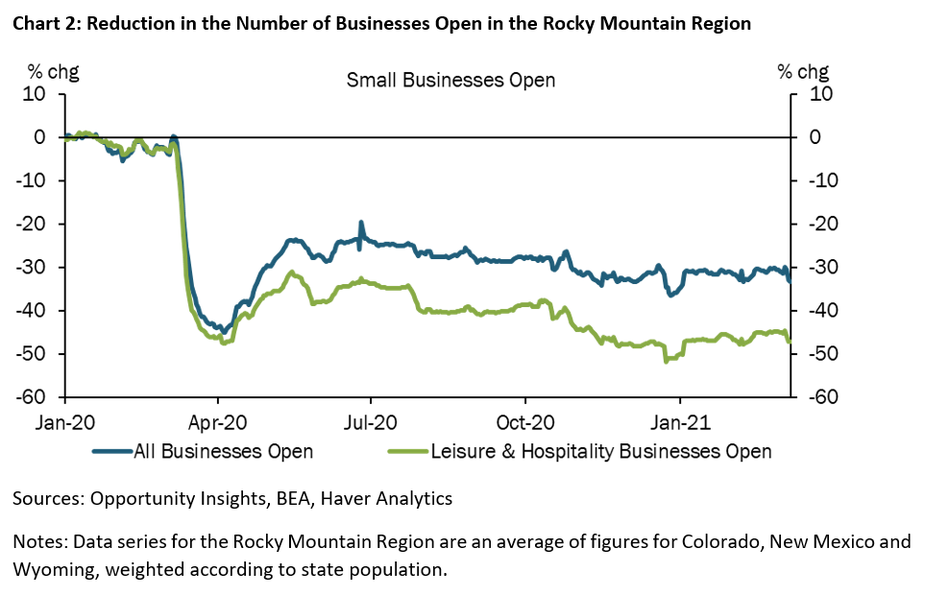

Job losses in leisure and hospitality occurred in part because businesses reduced the size of their workforce as they served fewer customers. Many of the job losses occurred because establishments in the sector closed their doors entirely. Chart 2 contrasts the relative share of businesses that closed in the leisure and hospitality sector to the extent of closures in other sectors. After experiencing a decline that roughly was on par with all businesses at the start of the pandemic, the number of leisure and hospitality businesses open remained depressed as relatively more business in other sectors were able to reopen. Looking to the recovery, the challenge will be both to bring employees back on board and to facilitate new or reopening of businesses that have been unable to serve customers amid the pandemic.

The disproportionate job losses for workers in the leisure and hospitality sector is not typical for economic cycles, and the outlook for recovery may not follow historical patterns either. Chart 3 shows the ebbs and flows of employment for leisure and hospitality workers over the last three decades. In each of the three previous recovery periods following an economic downturn (indicated by gray shading), the pace of jobs recovered throughout the Rocky Mountain region averaged 600 to 900 jobs a month. However, following the fiscal stimulus and fleeting progress in curtailing the pandemic between its second and third waves, in 2020 the Rocky Mountain region added 139,000 jobs within a couple of months.

In February, 14,800 leisure and hospitality jobs were added in the Rocky Mountain region. This is nearly 20 times the pace of recovery over the last three recessions. The potential for the regional economy to bring leisure and hospitality employment back quickly is a welcome turn from the typical historical pattern. Were regional employment to recover at a similar pace, say 900 jobs a month, employment would not return to peak levels for several years.

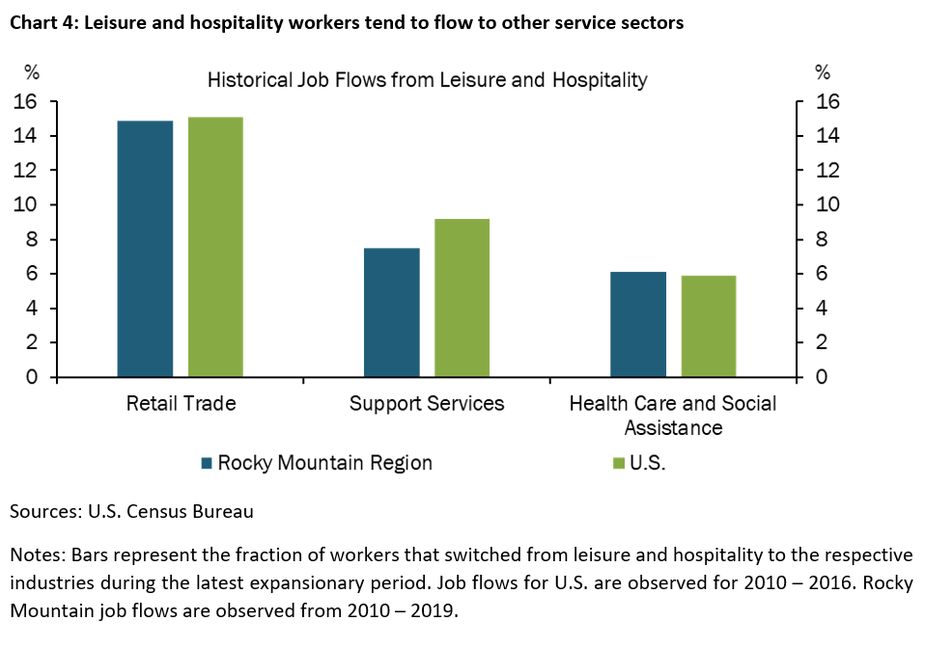

As employment in the sector remains depressed, another potential avenue of recovery for households may be for workers to seek employment in other sectors. Chart 4 shows that, historically, if restaurant or hotel workers flow into other industries they tend to seek employment in the retail or health-care sectors. During the decade-long recovery after the global financial crisis, more than 20% of leisure and hospitality workers that found employment outside the sector, did so at retail establishments or in health-related businesses.

Unfortunately, regional employment in other service sectors where leisure and hospitality workers frequently find employment also have been hit hard by the pandemic (recall Chart 1 above). Thus, the best prospects for these workers, and regional employment overall, is a swift and sustained recovery in demand at local restaurants, hotels and entertainment venues. Several factors suggest that the region will experience a swift recovery in employment in coming months, but significant uncertainty remains about the duration of the surge in employment. As we look ahead, the distinction between demand from consumers and demand resulting from business activity may be helpful in charting the course of recovery.

Pent-up Consumer Demand

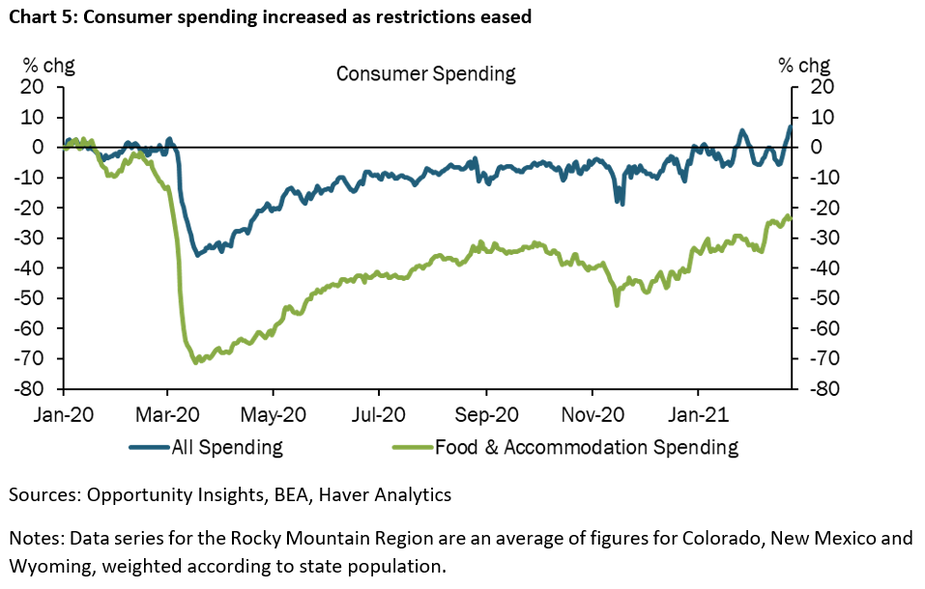

Consumers appear poised to travel, dine out and attend public events. Already, we have seen consumers respond to easing restrictions on capacity at restaurants or social gatherings during the last year by resuming spending at leisure and hospitality businesses. Last year, when restaurants reopened through the summer and fall, consumer spending rebounded quickly. After a 70% decline on spending at hotels and restaurants in April, spending was down 30% in October, a significant improvement. Due to this quick rebound in consumer spending, by the end of October roughly half of all leisure and hospitality workers across the region were back to work. This pattern was repeated again in November as the third wave of COVID-19 eroded consumers’ ability to convene safely and additional restrictions were put in place. Once restrictions began to loosen at the start of 2021, consumer spending rebounded again. Chart 5 shows the increase in spending in January and February, after its decline in December. This willingness to support leisure and hospitality businesses once restrictions are lifted will be important to the sector’s recovery.

Additionally, consumers’ accumulation of savings during this economic downturn is indicative of their ability to spend on travel and other leisure activities in the near future. The savings rate has increased beyond levels seen in previous recessions. In fact, the personal savings rate is greater than it was just prior to the pandemic, which was on the heels of the longest economic expansion on record. The significant shock to incomes experienced at the start of the pandemic, may have prompted households to take extra precaution in shielding themselves from future unprecedented income loss, given the sentiment of uncertainty that the pandemic created. Moreover, many households used their fiscal stimulus payments to increase their precautionary savings this year, and so may have disposable income to support the leisure and hospitality industry’s recovery. The pandemic may have permanently altered the savings habits of households as they remain wary of further shocks to their income. The motives behind household savings are important as recent research by Smith 2020 shows that historically, when precautionary motives drive increases in the savings rate, persistent declines in consumption tend to follow. However, as we move toward minimizing the risk of COVID-19 and the potential devastating effect that it can have on the economy, consumer confidence will likely increase, and prompt households to have a looser grip on their savings.

COVID-19 infection rates and vaccination distribution and administration have improved, which has allowed businesses to operate at greater capacity and prompted authorities to roll back restrictions on restaurants and gatherings. In Colorado, public health authorities have eased the conditions for counties to qualify for fewer restrictions on business operations. In New Mexico, more businesses continue to move toward limited restrictions under their tiered framework. Businesses in roughly 70% of New Mexico counties now can operate in the Turquoise tier, which requires the least restrictions on occupancy. Widespread vaccinations also are expected to prompt the further rollback of restrictions that will support the sector’s recovery. Currently, 18% of the Rocky Mountain region is fully vaccinated. The minimization of COVID risk through vaccinations likely may lessen public health concerns, as well as increase consumer confidence and willingness to spend in the leisure and hospitality sector.

The Uncertain Future of Business Travel and Office Presence

Restaurants in metro areas with a significant office footprint likely face a more uncertain outlook than those in resort areas, suburban locations or others that predominantly serve household consumers. Likewise, hotels near business districts, by conference centers, or adjacent to airports that attract business travelers may face more persistent declines in demand. The uncertainty for these pockets of the leisure and hospitality sector stems from the potential changes to the future of onsite work that would otherwise attract office workers or require face-to-face meetings. The number of workers commuting to metro-area offices remains subdued, and expectations for office vacancies continue to rise. Chart 6 shows current expectations for office vacancies for 2023 in Albuquerque and Denver are elevated above their pre-pandemic levels, according to projections from CBRE. As some business adopt hybrid workforce models – limiting staff presence in metro area offices – patronage at downtown restaurants could also be slow to recover as fewer workers commute to offices on a daily basis.

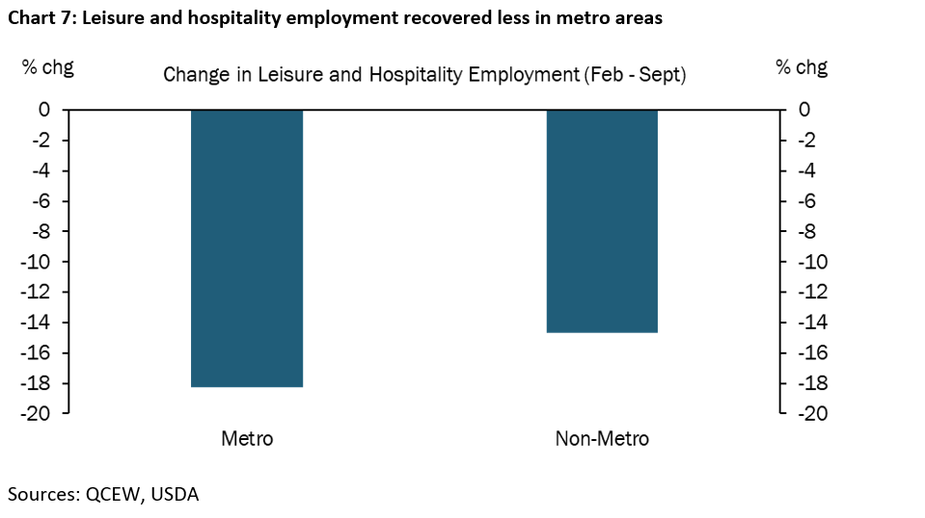

The uncertainty associated with shifts in work posture for many businesses may inhibit certain leisure and hospitality businesses from hiring at any faster rate than observed during previous recoveries. One fact that hints at the potential slower rate of recovery in demand that is tied business activity, rather than consumer demand, is the relative rates of recovery between metro and non-metro areas over the past year. Chart 7 shows leisure and hospitality employment recovered somewhat faster in non-metro areas of the region at the tail-end of the second wave of COVID-19. In metro areas where few workers were commuting to their offices at the time, more than 18% of jobs in the industry remained lost at the end of September 2020, 3 percentage points higher than in non-metro areas. That difference in recovery could persist even as COVID-19 vaccines continue to be administered throughout the region if metro-area employers continue to keep workers at home to some extent.

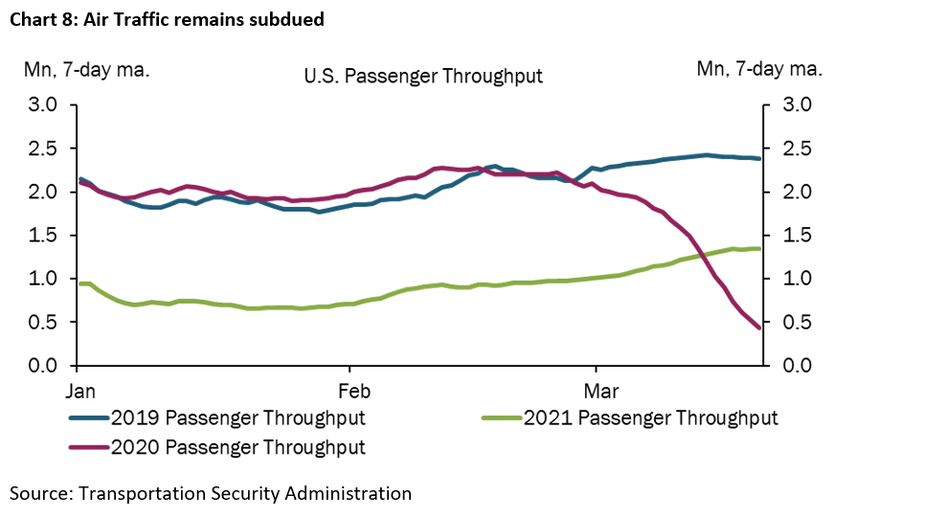

In addition to shifts in local work postures between homes and offices, business travel may be slow to recover. Chart 8 shows the number of passengers passing through U.S. airports remains well below pre-pandemic levels, much of this likely due to lower levels of business travel. Though consumer demand has several factors supporting a swift recovery in employment for restaurants and vacation destination lodging, the uncertainty around business travel could delay the return to peak employment levels for the leisure and hospitality sector overall.

Reference

A. Lee Smith. 2020. “Why are Americans Saving So Much of Their Income?,” Federal Reserve Bank of Kansas City, Economic Bulletin.

The views expressed are those of the authors and do not necessarily reflect the positions of the Federal Reserve Bank of Kansas City or the Federal Reserve System.

Authors

Nicholas Sly

Vice President, Economist, and Denver Branch Executive