The unemployment rate across the country remained low over the past year, with labor demand still in excess of the available supply of workers. Job gains were generally solid. Since the beginning of the year, employers across the United States added 285,000 jobs each month, on average. However, employment growth has been somewhat slower in the Rocky Mountain region. During the first quarter of this year, the number of job postings fell while the number of jobless claims picked up in certain pockets of the regional labor market. In this edition of the Rocky Mountain Economist, we describe the softening in labor markets across the Rocky Mountain region, highlighting industry-specific factors driving the recent declines. Ongoing job gains in sectors like leisure and hospitality and manufacturing, were offset by layoffs in industries like construction, real estate, finance, and, most recently, in technology-related jobs. The substantial tech footprint in several parts of the region has led to a heavier burden from layoffs at large tech firms. The share of workers in tech-related jobs is even higher than it was in previous cycles, suggesting that the emerging challenges in the tech sector could be even more of a drag on the regional economy than during the burst of the tech bubble at the turn of the century.

Slowing Job Growth in the Region

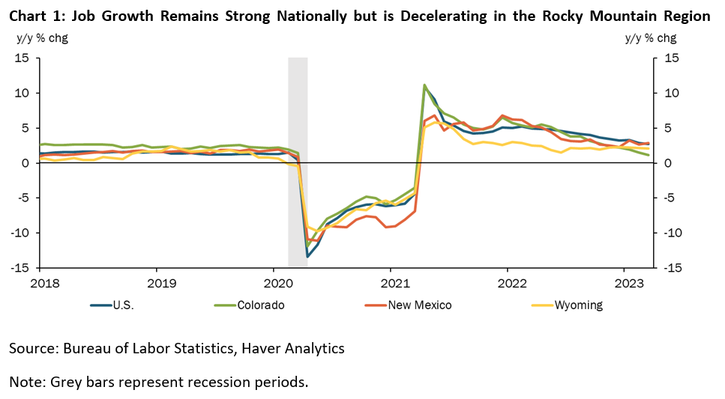

Employment growth in Colorado and New Mexico exceeded the national average for much of 2021 and 2022. Over the past year, and especially during the last 3 months, job growth slowed in the Rocky Mountain region while remaining strong across the rest of the nation (Chart 1). The pace of job growth decelerated in the middle of last year, such that employment growth in Colorado (green) and New Mexico (red), like in Wyoming (yellow), dipped below the national average (blue). During the first quarter of 2023, the pace of employment growth stalled in Colorado.

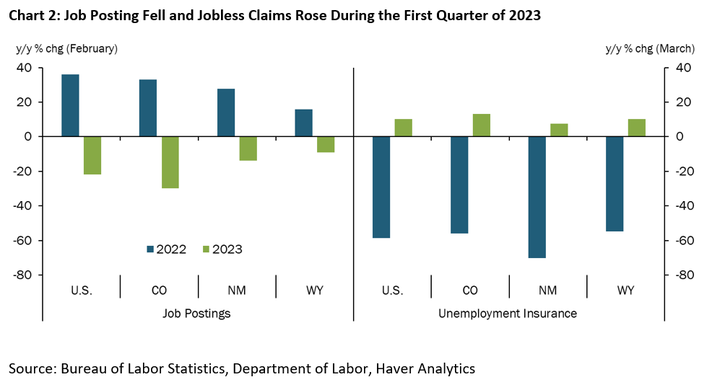

The slower pace of net job gains and broader softening conditions in regional labor markets result from a combination of changes in employment activities, including fewer job postings and rising layoffs. As a result, jobless claims have also picked up (Chart 2). Looking across Rocky Mountain states, Colorado is experiencing a swift pace of declines in job postings with 30% fewer postings in February compared to the previous year, a larger fall than the national decline of 21%. Job postings declined by roughly 13% in New Mexico, while Wyoming experienced a 9% decrease in the number of job postings. Conditions in Colorado have softened to the extent that unemployment insurance (UI) claims rose in March by 13% above the previous year, albeit from historically low levels. Colorado’s labor market is showing signs of slowing, both in employers’ waning desire to hire (job postings) and in rising job losses (UI claims).

Slower Hiring in the Region is Linked to Certain Industries

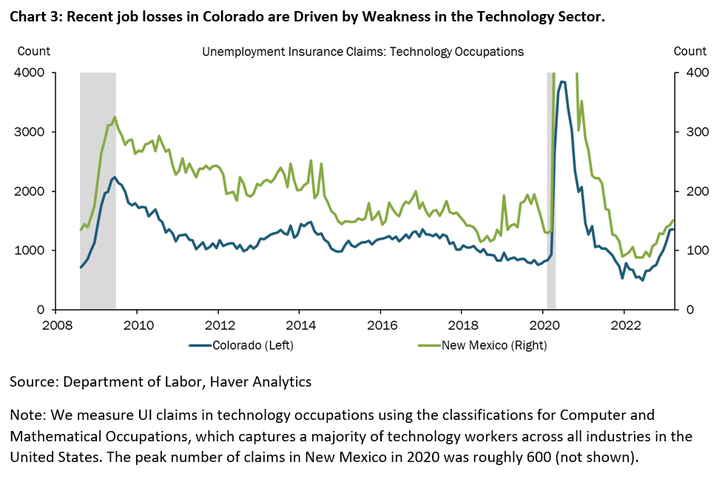

Job losses in finance, real estate, and construction were primary drivers of softening regional labor market conditions over the last year. However, the most recent surge in losses is emerging among technology jobs, predominantly at large firms. Chart 3 shows continued UI claims for technology workers in Colorado and New Mexico. Continued UI claims for technology occupations in Colorado rose by 35% since December of 2022, compared to total UI claims increasing at a more modest pace of 15% over that same period. New Mexico also saw an uptick in technology UI claims, 17% since December, but tech-related UI claims remain a relatively low contributor to total claims across the state. However, in Colorado, tech UI claims continue to increase as a share of total claims, suggesting that technology industry woes are now a contributing factor to overall softening labor markets in Colorado.

A Historical Precedent for Declining Tech Employment

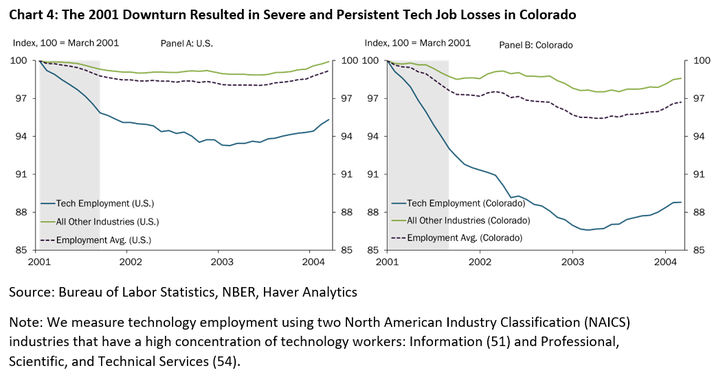

As declines in activity among technology businesses contribute to labor market headwinds, particularly in Colorado, it is natural to ask how this episode compares to historical downturns in the technology industry. Although the 2001 recession is not a perfect analog for the current tech industry downturn, there are some insights from that episode that may prove useful for understanding current conditions. Chart 4 shows technology industry employment levels compared to other employment for the U.S. (panel A) and Colorado (panel B), indexed to their March 2001 levels. The burst of the 2001 tech bubble posed acute challenges for tech industry employment in Colorado and across the nation (blue lines), with all other industries (green line) being somewhat insulated from that recession. However, tech employment losses were a larger drag on total employment (dotted line) in Colorado compared to the rest of the U.S.

The more significant spillovers in Colorado resulted from three features of the regional labor market. First, a larger share of Colorado’s labor force was employed in tech occupations. Second, technology job losses during the 2001 bubble were relatively more pronounced in Colorado, with employers in the state shedding more than 13% of their tech jobs, compared to the U.S., which lost 7% on average. Third, the duration of the drawdown in tech employment lasted over two years before tech employment reached its nadir. A continued downturn in technology employment today could similarly be more severe in the Rocky Mountain region compared to the rest of the nation.

Looking Ahead

Although historical examples are a helpful benchmark, structural shifts in regional labor markets may make a downturn within the technology industry today more challenging for overall economic conditions in the region. Over the past decade, Colorado experienced a steady increase in technology industry concentration, with the share of labor in technology jobs rising from 4.1% in 2012 to 4.8% in 2022, compared to the U.S. which saw technology labor move from 2.8% to 3.4% over the same period[1]. As Colorado became more concentrated in the technology industry, it may also be more sensitive to a sector-specific downturn. Yet, technology industries, and other industries employing technology workers, are much more mature than they were 25 years ago. More businesses now employ workers in technology occupations, potentially making workers’ skills more transferable. As a result, the sector may prove more resilient than during the episode at the turn of the century, even if the sector has continued to grow in prominence.

____________________

[1] The share of labor in employed in tech occupations does not account for peripheral workers in tech-related jobs or industries, and so understates the overall footprint within the region. An additional measure of concentration in tech employment is a location quotient, which is a measure of an industry’s concentration in a given location (e.g., state or county), relative to that the United States (External LinkBLS). Colorado’s technology labor quotient remained steady over the last decade – 1.49 in 2012 and 1.41 in 2022.

The views expressed are those of the authors and do not necessarily reflect the positions of the Federal Reserve Bank of Kansas City or the Federal Reserve System.

Authors

Bethany Greene

Research Associate II

David Rodziewicz

Advanced Economics Specialist