Frequently referenced labor market indicators point to the enduring tightness of the labor market in the Rocky Mountain region. Unemployment is low. Layoffs are subdued. Job gains are healthy. Nominal wages continue to grow at historically high rates, while little relief from worker shortages is apparent. However, slowing global growth, heightened economic uncertainty and tighter financial conditions hint at potential softening of labor market conditions. As the current tightness of the labor market is a major source of inflationary pressure, eyes are peeled for any indication that some slack is emerging. Metrics such as job gains and wage growth tend to lag business cycles, providing delayed information about changes in labor market dynamics. Other labor market indicators such as part-time work, overtime hours and self-employment, offer additional insight into labor market dynamics, and may be key in identifying preliminary signs of labor market cooling. In this edition of the Rocky Mountain Economist, we highlight a few labor market indicators we are monitoring to peer through the uncertainty surrounding the trajectory of labor market conditions as we head into 2023. While several measures of labor market health show that the labor market is still historically tight, and ongoing tightening appears to have slowed, a broad number of labor market indicators suggest slowing momentum recently.

Lower Quits Rates are Likely to Put Downward Pressure on Wage Growth

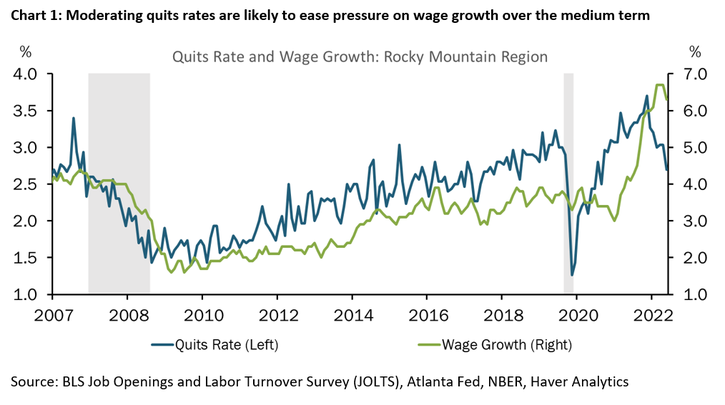

Changes in quits rates often precede changes in wage growth. The close alignment of employee confidence and business cycle fluctuations explains this relationship. An employee’s willingness to voluntarily leave their employer is informed largely by their confidence in their ability to obtain employment elsewhere, a confidence that is either bolstered or weakened during economic downturns and expansions. For example, in the beginning of 2020, quits rates plummeted, as employees were more inclined to hold onto their positions as the threat of pandemic-induced layoffs were looming. This lowered confidence in job market prospects was accompanied by slowing wage growth. Conversely, beginning in 2021, quits rates accelerated. Supported by an abundance of job openings, employees left their jobs in pursuit of higher wages or remote work positions, a phenomenon referred to as the “Great Resignation.” Job switchers enjoyed pay bumps that greatly exceeded their job stayer counterparts, as many employers competed to attract workers to fill open positions.

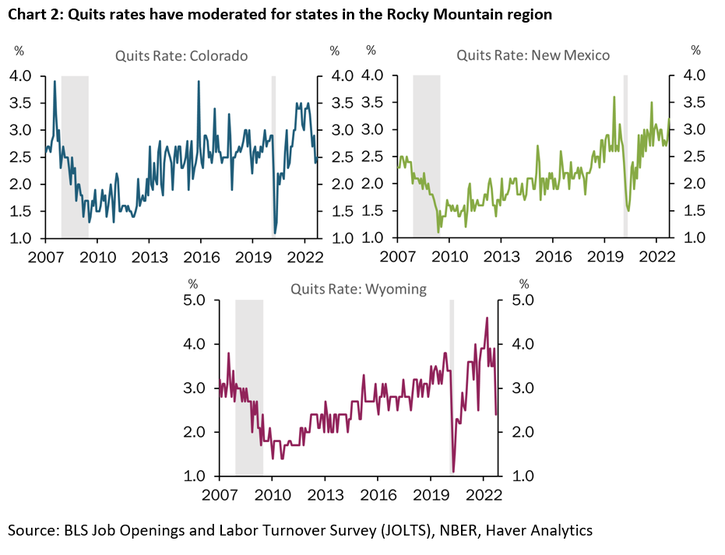

These labor dynamics appear to have been short-lived, as quits rates quickly reverted to historical trends soon after the Fed began raising interest rates. Chart 1 shows that quits rates moderated in all three states in the region over the past few months. As of October, quits rates declined 1.0%, and 2.2% in Colorado and Wyoming, respectively, relative to March of this year. Moderating quits rates could simply be a return to normalcy or a shift in employee sentiment representing a greater inclination to hold on to their current positions and an increased willingness to seek and maintain employment. This shift in the labor market is likely to translate to some alleviation of hiring pressure, putting downward pressure on wage growth as employers compete less to attract and retain employees.

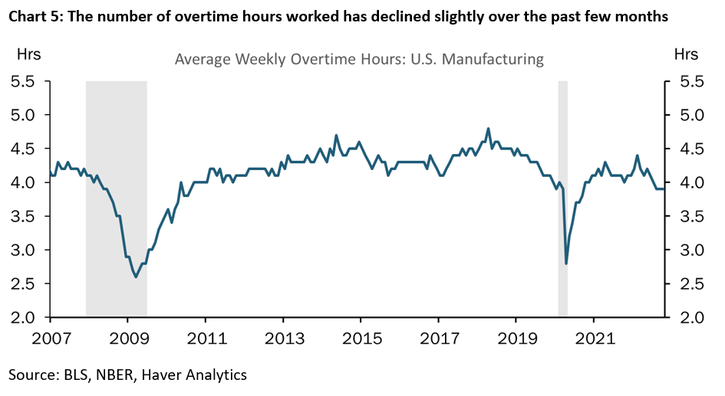

Changes in Average Weekly Hours is a Barometer for Changes in Business Activity

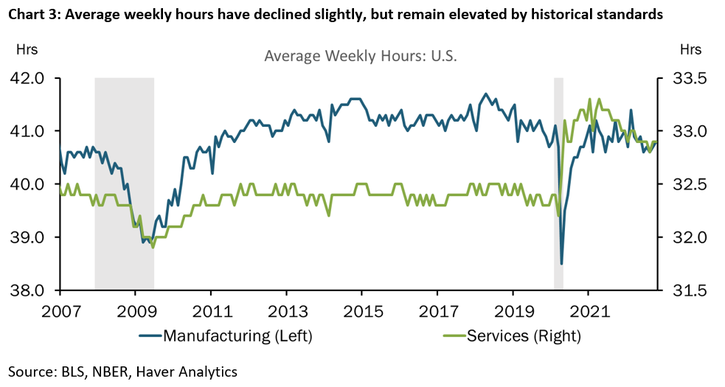

Another metric to monitor near turning points is the average weekly hours worked by employees. A notable decline in weekly hours may be an indication that businesses are utilizing less of their workforce capacity for production. In response to slowing demand, employers are likely to reduce the hours of their employees before laying off workers completely. As such, average weekly hours closely follow business cycle fluctuations. For example, if manufacturing businesses were experiencing a slowdown in demand, they would no longer require additional employee hours to increase production capacity to reduce backlogs. Additionally, the number of overtime hours worked are even more sensitive to changes in demand as hours worked beyond a full-time schedule are often the first to be cut.

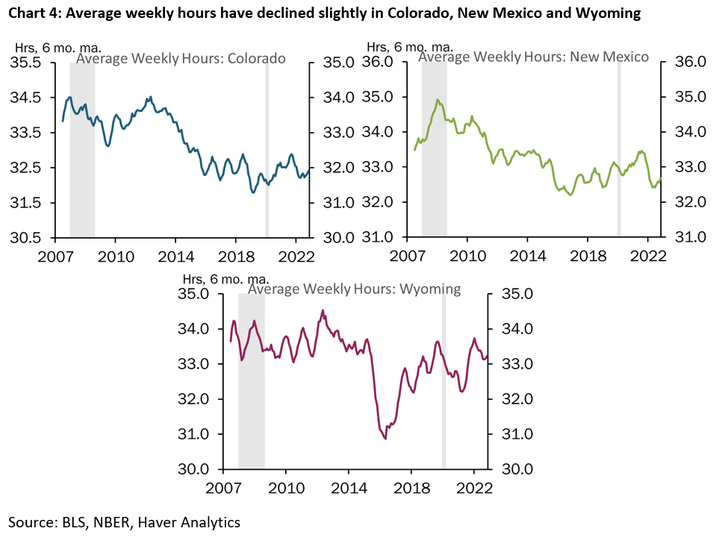

Businesses in the Rocky Mountain region are showing some signs of actively reducing their employee hours, an indication that labor demand may be softening somewhat. Chart 3 and Chart 4 show that average weekly hours have declined slightly for all three states in the region since the Fed started raising interest rates this year. Service hours remain elevated nationally compared to pre-pandemic norms, but structural changes in the labor market, such as the greater availability of remote work, may render the pre-pandemic comparison less useful. More importantly, the number of service hours has declined somewhat over the last several months as financial conditions have tightened and economic uncertainty has grown. While the average number of hours worked in manufacturing sectors has remained steady nationally, the number of overtime hours worked declined slightly in recent months to a level below historical periods of economic expansion.

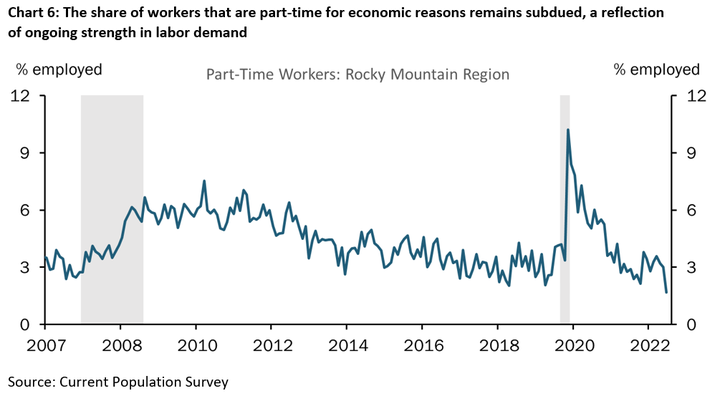

Increases in Part-Time Work for Economic Reasons Signals a Decline in Labor Demand

The share of employed people working part-time also provides some insight into changing labor dynamics. The Bureau of Labor Statistics (BLS) separates part-time workers into two groups: part-time for economic reasons and part-time for non-economic reasons. Most workers are part-time for non-economic reasons, voluntarily opting for less than full-time hours. Conversely, workers who are available to work full-time, but whose employers are unable to provide them with those hours, are part-time for economic reasons. As such, movement in the number of individuals working part time for economic reasons can provide some insight into changes in labor demand. An increase in the share of employed persons working part time for economic reasons often precedes layoffs, as employers will often reduce their employees’ hours to part-time before they reduce their payrolls, which echoes the aforementioned dynamic with average weekly hours. For example, the share of workers who were part-time for economic reasons reached a high of 10% during the second quarter of 2020 as workers reduced their hours due to declines in business activity during the pandemic. It declined sharply as employers’ demand for full-time work increased significantly over the past year as consumer demand was restored. Currently, the share of workers who are part time for economic reasons remains subdued, therefore providing no indication that businesses are trying to cut costs by reducing their employees’ hours yet, an indication of continued strength in labor demand.

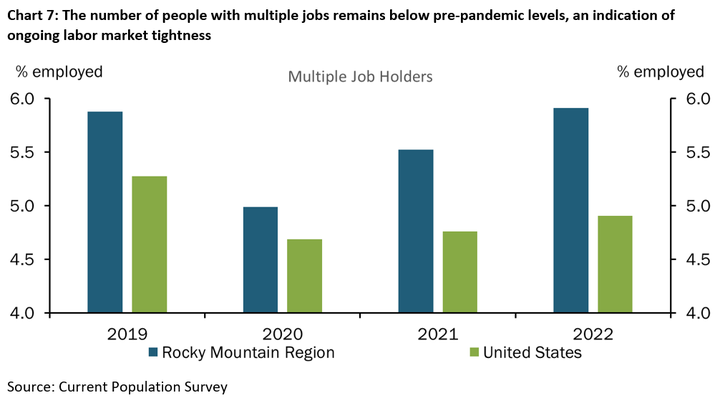

Subdued Multiple Job Holders Signals Ongoing Labor Market Tightness

Another important indicator of changing labor market dynamics is the share of works who hold multiple jobs. A decline in multiple job holders may reflect greater availability of full-time work, a feature of tightening labor market conditions. Additionally, changes in multiple job holders may also provide insight into the state of household finances and worker sentiment, as an individual’s willingness to take an additional job may be partially influenced by their outlook on their own financial conditions. Employees with multiple jobs represented roughly 7% of the workforce in 2019, a number that plummeted to 4% in the beginning of 2020, due to pandemic-induced layoffs. However, even as labor demand returned, and workers re-entered the labor force, many businesses still experienced labor shortages, especially in service-oriented industries, partially due to the decline in the number of employees with more than one job. The number of people reporting that they have more than one job increased, but still has not recovered to pre-pandemic levels nationally. The lack of recovery in this source of labor supply indicates workers increased engagement with full-time positions as well as their improved ability in meeting their financial obligations without the need for additional sources of income. However, the share of multiple jobholders has increased somewhat over the past few months. The increase perhaps provides some insight into the impacts of inflation – households may be seeking out additional work at a higher rate to supplement their income in the face of higher expenses.

With tight labor conditions, and persistently high inflation, policy makers are looking to the strength of the labor market for substantial evidence of effective monetary policy transmission. While labor demand remains strong in most sectors, and job gains exceed expectations, signs of waning worker confidence may point to a more bleak path moving forward. The University of Michigan’s measure of consumer unemployment expectations highlights growing uncertainty regarding economic conditions. The share of respondents that expect an increase in unemployment in the next year is currently above its pre-trend after increasing over the past few months. Additionally, announcements of layoffs in the tech sector have the potential to weigh on consumer sentiment, even for workers in unaffected industries. However, this negative economic sentiment is offset by monthly reports of higher than expected job growth. The conflicting narratives make it difficult to fully grasp what is going on in the labor market. Although tighter financial conditions have not yet translated to a notable reduction in labor market tightness, a labor market once characterized by burgeoning worker confidence appears to have run its course. While there are few signs of further labor market tightening, the labor market remains strong by historical standards. Inflation is still well-above the Fed’s 2 percent target. But the path toward restoring price stability may be clearing slightly.

The views expressed are those of the authors and do not necessarily reflect the positions of the Federal Reserve Bank of Kansas City or the Federal Reserve System.

Author