Agricultural credit conditions continued to tighten in the second quarter and growth in farmland values slowed. The pace of decline in farm loan repayment rates picked up gradually through mid-year alongside considerable softening in farm income. Elevated production costs and lower prices for key commodities, particularly major row crops, have reduced liquidity in the sector and spurred a rise in non-real estate loan demand. Interest rates on farm loans also remained at multi-decade highs, keeping financing costs high. Growth in farm real estate values tempered further during recent months, but valuations held firm in most regions.

Second Quarter Federal Reserve District Ag Credit Surveys

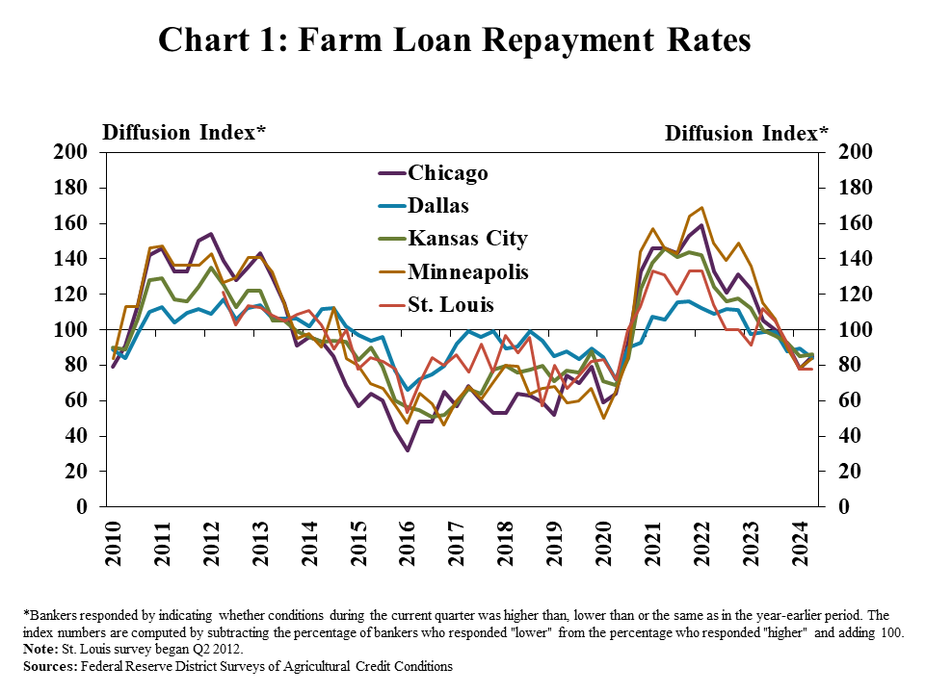

Credit conditions deteriorated gradually as the farm economy remained subdued. According to Federal Reserve Surveys, farm loan repayment rates slowed across all participating Districts in the second quarter (Chart 1). On average, about 20% of respondents reported that repayment rates were lower than a year ago while roughly 75% indicated repayment had not changed.

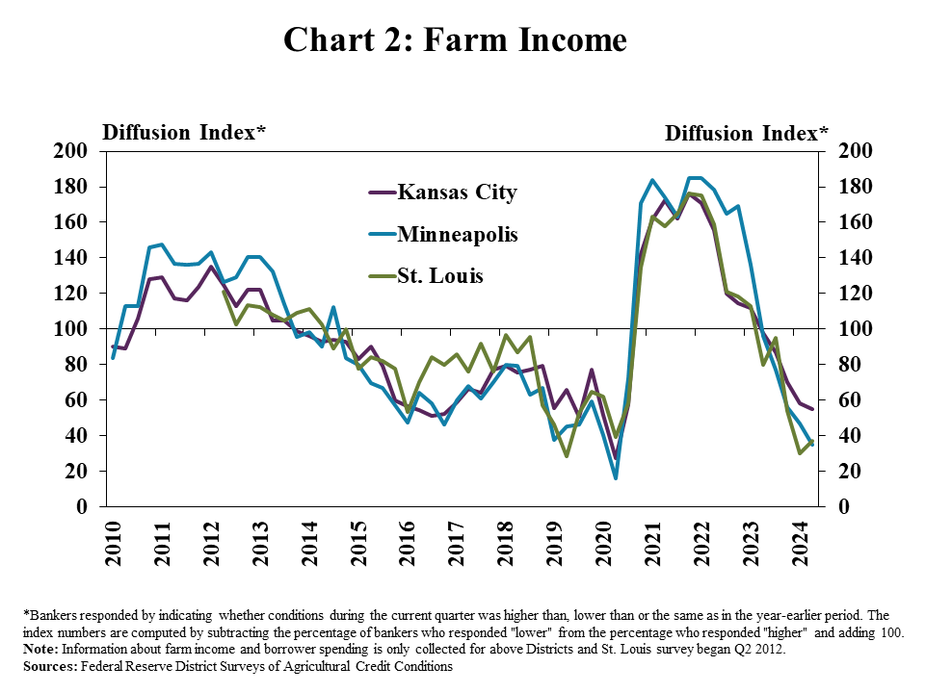

Credit conditions moderated as farm income weakened at a rapid pace. Farm income continued to decrease from exceptional levels in all participating regions (Chart 2). The pace of decline was slightly less pronounced in the Kansas City District, where greater reliance on cattle revenues has limited the drop in farm incomes.

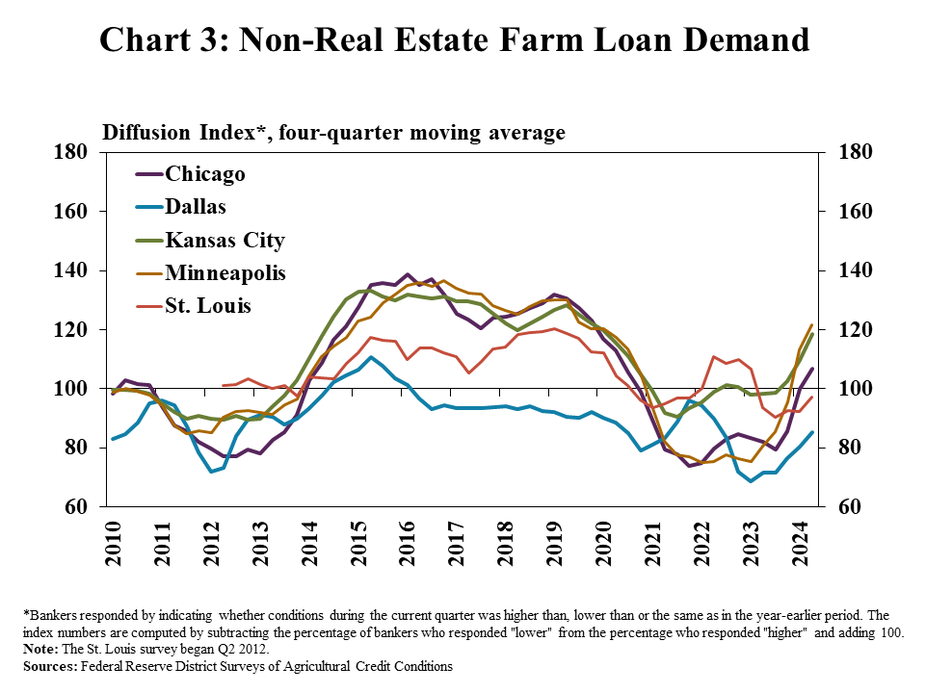

Demand for non-real estate farm loans in most areas continued to grow as income and liquidity tightened. The pace of increase in loan demand continued to rise in most regions (Chart 3). Demand stayed subdued in the Dallas and St. Louis Districts, but the share of lenders reporting lower demand decreased from previous quarters.

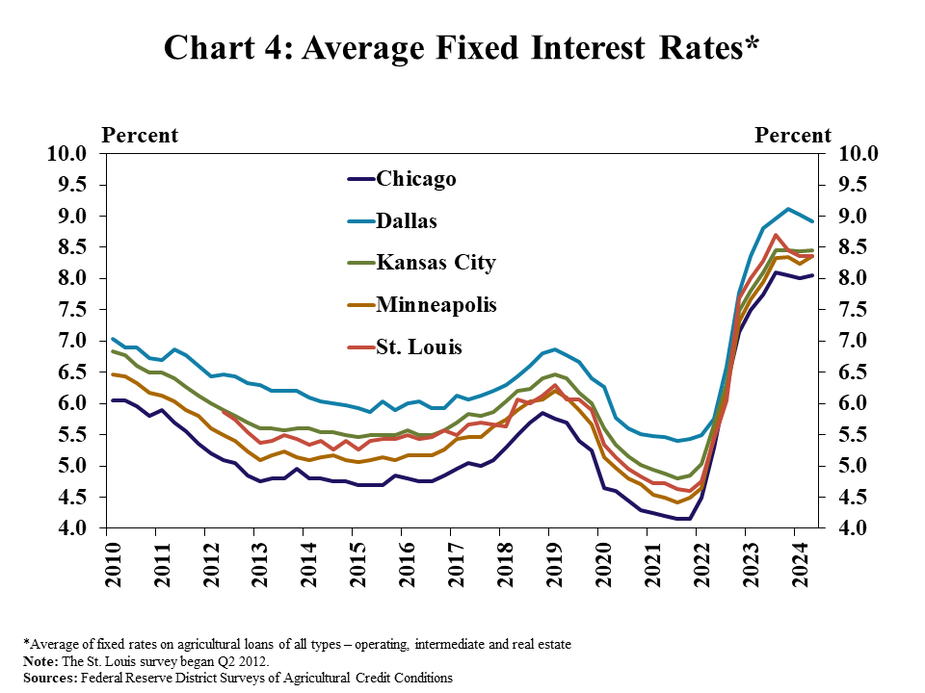

Lending has also increased as interest rates have remained at multi-decade highs. The average rate charged on farm loans was generally steady in most Districts as benchmark rates were unchanged (Chart 4). Farm loan interest rates have been well above the average of the past decade for almost two years and interest expense for producers has risen considerably.

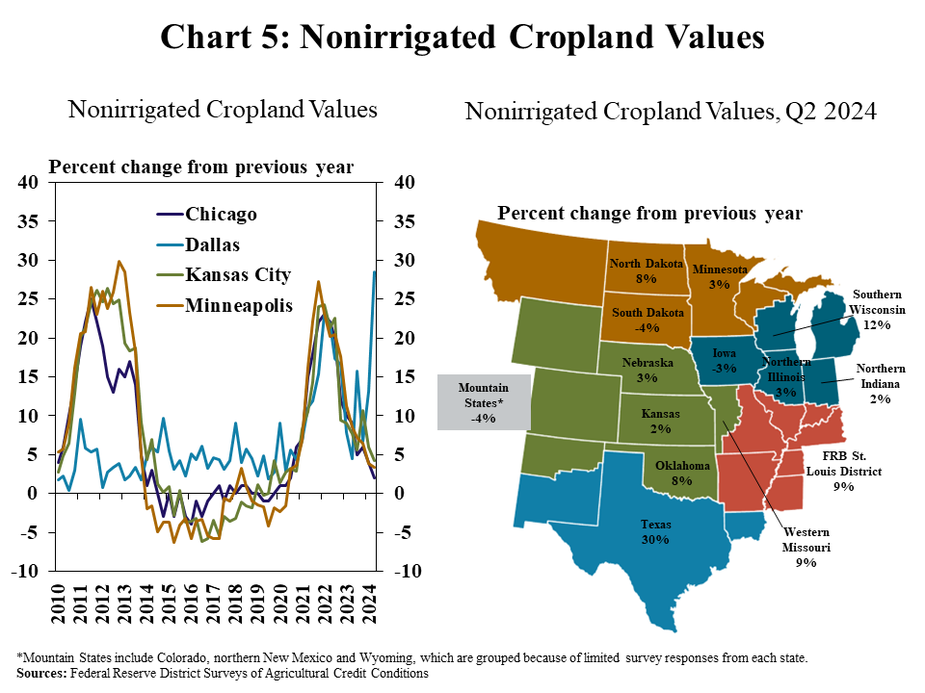

Farmland values remained firm, but growth slowed in most regions. The value of nonirrigated cropland increased by less than 5% in nearly all participating Districts (Chart 5). In contrast to other areas, land values in Texas increased considerably with contacts in some areas of the state citing strong recreational and investor demand.

Federal Reserve Ag Credit Surveys Historical Data

Federal Reserve Ag Credit Surveys Tables

About the Federal Reserve Ag Credit Surveys

The views expressed are those of the authors and do not necessarily reflect the positions of the Federal Reserve Bank of Kansas City or the Federal Reserve System.

Authors

Nate Kauffman

Senior Vice President, Economist, and Omaha Branch Executive; Executive Director of the Center for Agriculture and the Economy