Strong growth in farm lending activity at commercial banks continued into the first quarter of 2025. The volume of farm operating loans increased sharply from a year ago alongside an increase in the number of large loans. Demand for non-real estate agricultural loans has grown over the past year alongside elevated production expenses and a contraction in farm sector liquidity. The growth was recorded during the survey period in early February, ahead of recent distribution of assistance payments from the American Relief Act which could potentially improve liquidity for some producers. Looking ahead, however, weak crop prices are likely to continue weighing on financial conditions in the sector and could keep demand for financing elevated.

Fourth Quarter National Survey of Terms of Lending to Farmers

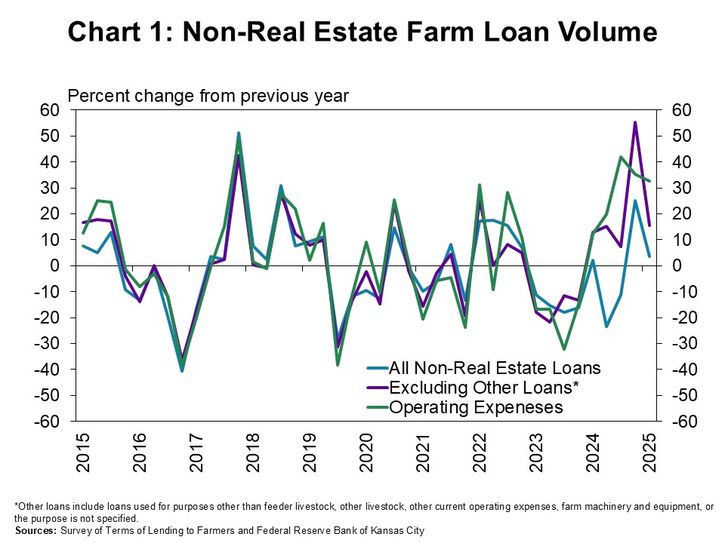

According to the Survey of Terms of Lending to Farmers, the pace of growth in farm lending eased slightly in the early months of 2025. The volume of new non-real estate farm loan activity at commercial banks increased about 4% from a year ago (Chart 1, blue line). However, similar to recent quarters loans for miscellaneous purposes remained subdued while the volume of loans for key types of farm debt increased considerably more (purple line). The increase continued to be largely attributed to loans for operating expenses, which grew by more than 30% for the third consecutive quarter (green line).

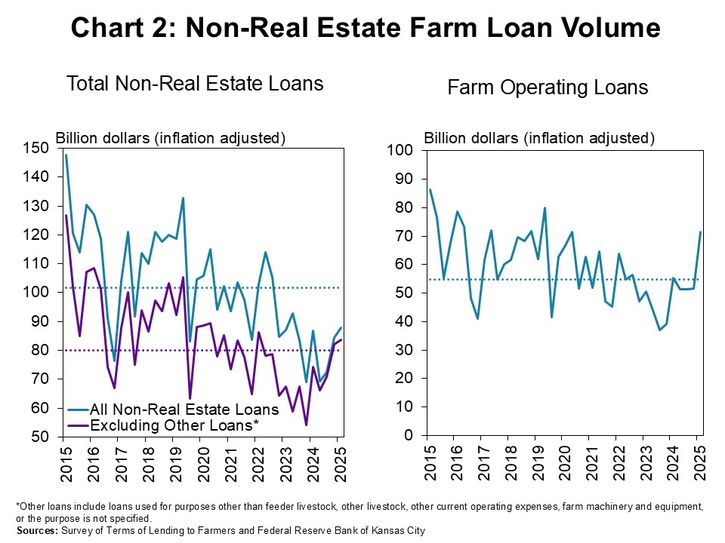

Sharp growth over the past year pushed loan volumes above recent historic averages. Excluding loans for miscellaneous purposes, the volume of all non-real estate lending was slightly above the average over the past year (Chart 2, dark purple line). Growth in operating loans was more pronounced, volumes were well above average, and at the highest level since 2019 (Chart 2, right panel).

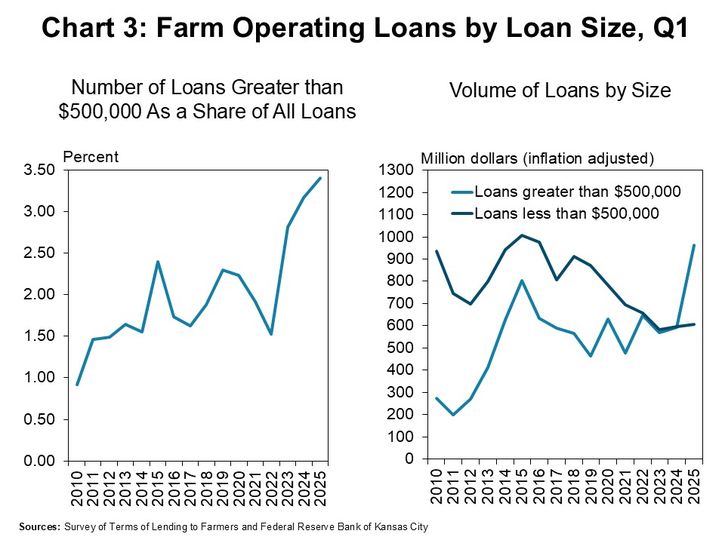

Operating loan volumes grew alongside an increase in large loans. The share of new loans larger than $500,000 increased sharply for the second consecutive year, rising to about 3.5% in the first quarter (Chart 3, left panel). With a greater number of large loans, the share of lending volumes attributed to loans more than $500,000 increased substantially (Chart 3, right panel).

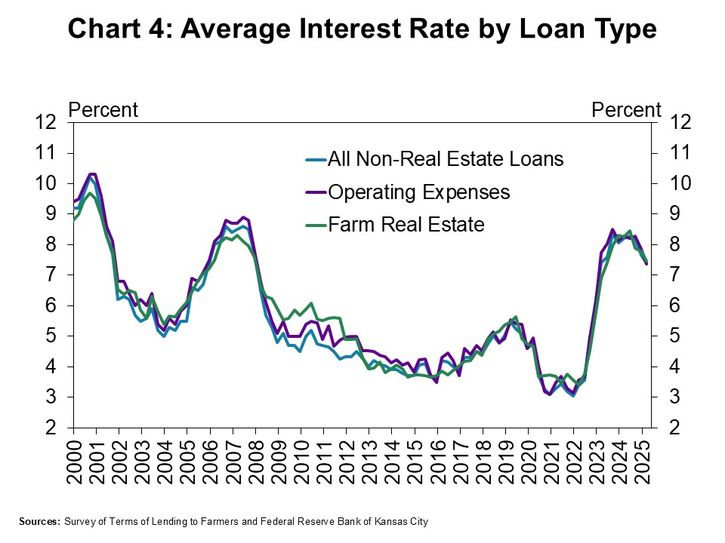

Interest rates on most types of agricultural loans declined slightly. The average rate charged on non-real estate farm loans dropped on average, by about 30 basis points from the previous quarter (Chart 4). Average rates were around 80 basis points lower than this time last year, but remained above the average of recent decades.

National Survey of Terms of Lending to Farmers Historical Data

National Survey of Terms of Lending to Farmers Data Tables

About National Survey of Terms of Lending to Farmers Data

The views expressed are those of the authors and do not necessarily reflect the positions of the Federal Reserve Bank of Kansas City or the Federal Reserve System.

Author