Farm operating debt at commercial banks continued to increase at a rapid pace through mid-year. According to quarterly call reports, outstanding non-real estate farm debt at commercial banks grew about 10% from a year ago during the second quarter. The rise was even more substantial at agricultural banks where debt balances have rebounded to longer-term trends. A moderation in the agricultural economy and lower farm sector liquidity has spurred higher financing needs and credit conditions have also shown signs of tightening. However, despite inching slightly higher, delinquency rates on farm loans remained limited through mid-year.

Second Quarter Commercial Bank Call Report Data

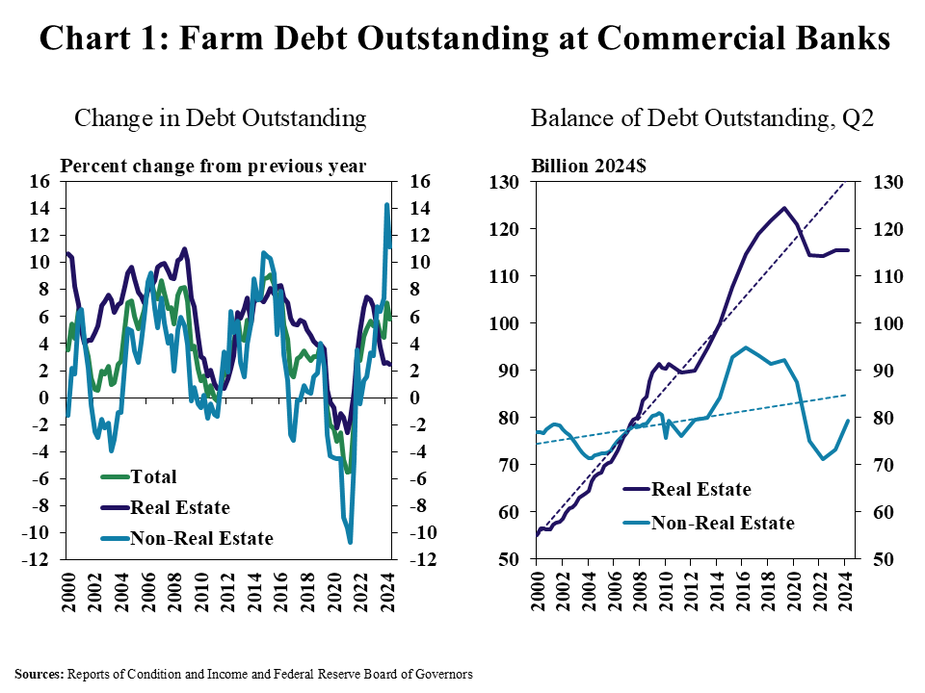

Growth in farm production loans stayed strong through mid-year as the agricultural economy continued to soften. The outstanding balance of real estate and non-real estate (operating) loans at commercial banks increased about 2% and 10% from a year ago, respectively (Chart 1). The rapid increase in non-real estate debt pushed balances nearer to, but still below the historical trend after adjusting for inflation. Growth in real estate debt, however, has remained subdued following a substantial retraction in 2021.

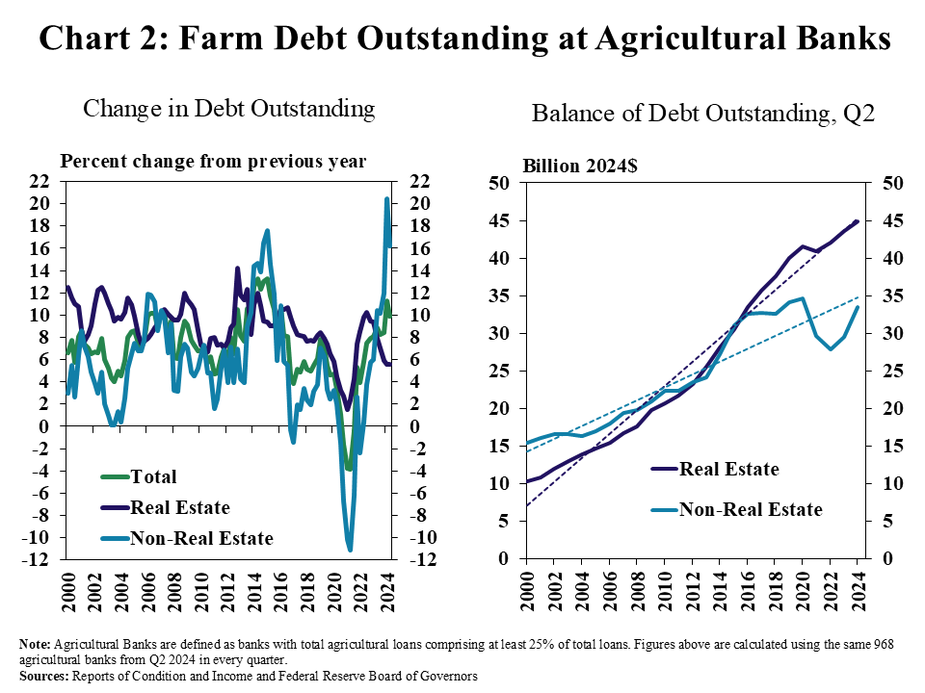

The increase in farm debt was notably more pronounced among agricultural banks. The outstanding balance of real estate and non-real estate (operating) loans at commercial agricultural banks increased roughly 6% and 15% from a year ago, respectively (Chart 2). For those lenders, real estate and non-real estate debt balances were near the long-term trend.

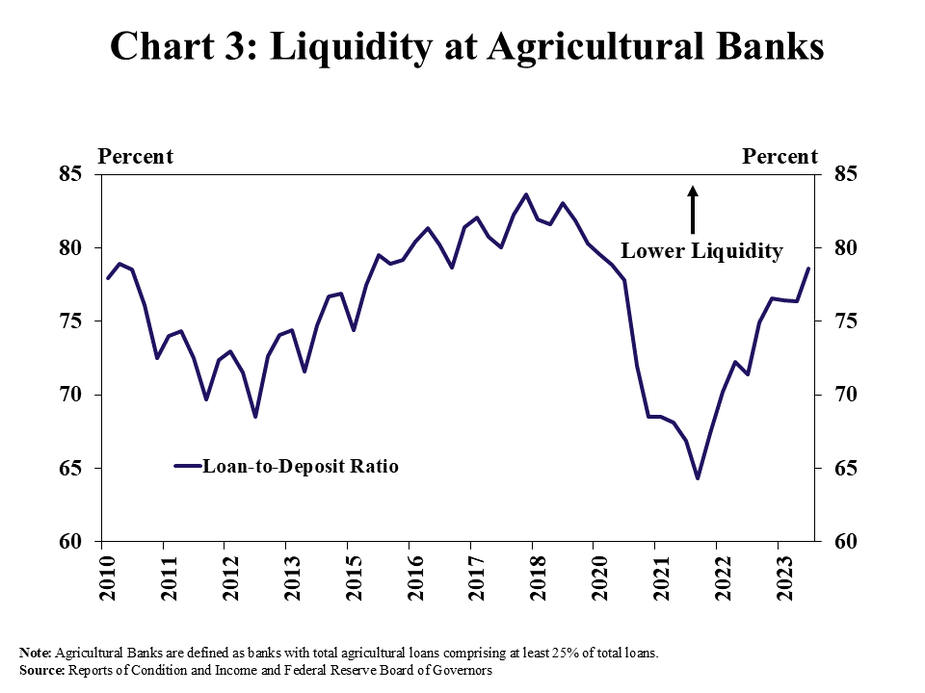

Liquidity for agricultural lenders has tightened alongside recent loan growth. The loan-to-deposit ratio among farm lenders increased to the highest level since 2020 (Chart 3). Agricultural bank liquidity has declined from record levels alongside strong loan growth and elevated competition for deposits that has led to increased use of alternative sources of funding at community banks.

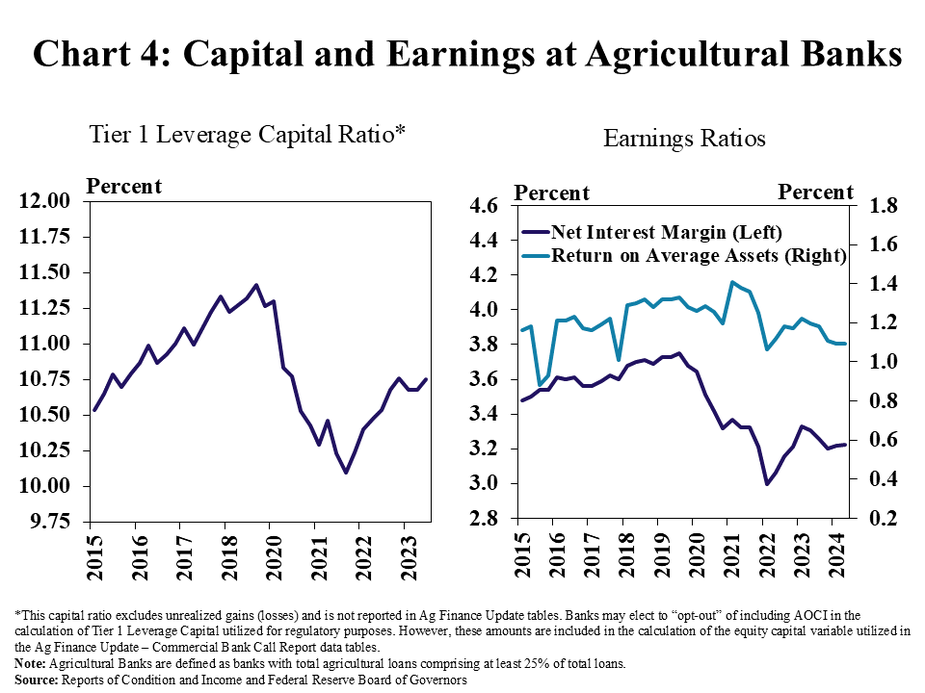

Capital levels at agricultural banks improved slightly alongside steady earnings. The tier 1 leverage capital ratios increased modestly from the previous quarter, remaining solid but below the 10-year average (Chart 4, left panel). The net interest margin and return on assets at agricultural banks was mostly unchanged over the quarter as elevated funding costs kept margins tight (Chart 4, right panel).

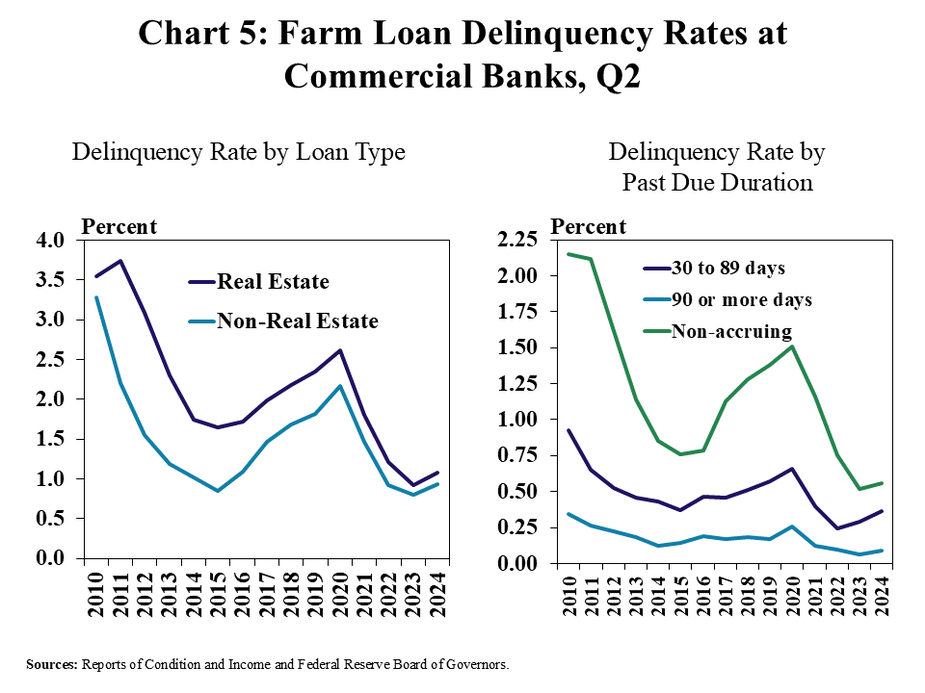

Credit conditions have tightened along with farm finances in recent months, but loan delinquency rates remained low. About 1% of real estate and non-real estate farm loans were past due at least 30 days in the second quarter, a slight increase from record low levels a year ago (Chart 5, left panel). Roughly half of the increase was attributed to newly delinquent loans past due 30 to 89 days (Chart 5, right panel).

Data and Information

Commercial Bank Call Report Historical Data

Commercial Bank Call Report Data Tables

About the Commercial Bank Call Report Data

The views expressed are those of the authors and do not necessarily reflect the positions of the Federal Reserve Bank of Kansas City or the Federal Reserve System.

Authors

Nate Kauffman

Senior Vice President, Economist, and Omaha Branch Executive; Executive Director of the Center for Agriculture and the Economy