Large operating loans made by large agricultural banks led to a significant increase in farm lending in the third quarter of 2018. A sharp increase in the volume of loans exceeding $1 million was a primary contributor to the increase in non-real estate farm lending. In particular, a majority of the increase was supported by loans used to fund current operating expenses. The increase in the size of loans also sharply increased the share of agricultural lending at large banks while interest rates on farm loans continued to trend upward.

Section A - Third Quarter National Farm Loan Data

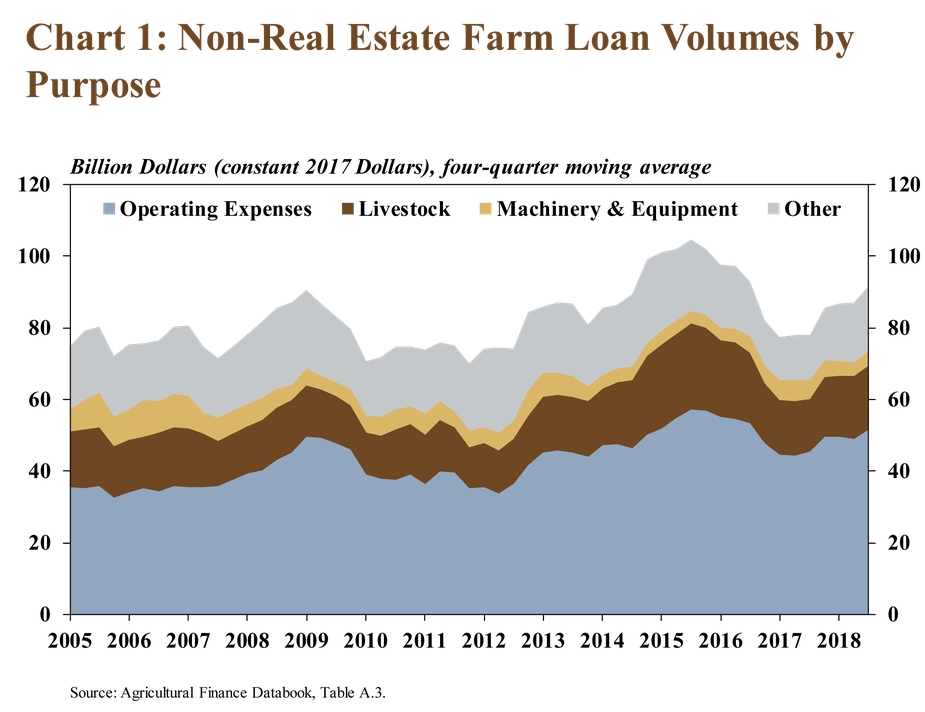

Non-real estate lending increased significantly in the third quarter, according to the National Survey of Terms of Lending to Farmers. The total volume of non-real estate farm loans was more than 30 percent higher than a year ago (Chart 1). This sharp growth in farm lending followed steady increases earlier in 2018 and represents the largest annual percentage increase in the third quarter since 2002. The typical seasonal pattern of reduced loan volumes from the second quarter to the third quarter also was much less pronounced. The volume of non-real estate loans decreased less than 3 percent from the previous quarter, compared with an average decline over the last 10 years of 14 percent.

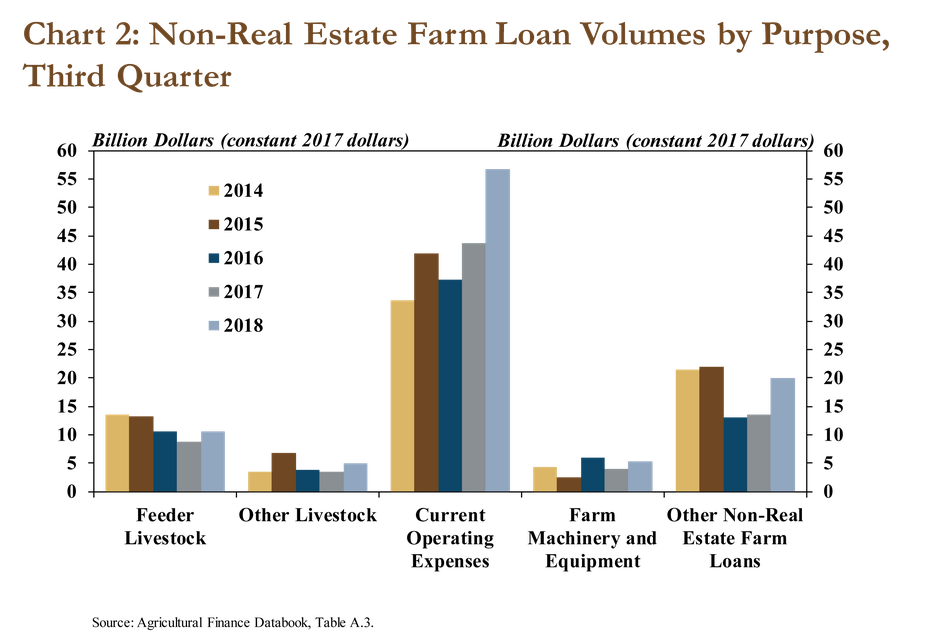

The increase in non-real estate farm lending again was driven primarily by operating loans. Similar to 2015, when there was a significant increase in farm lending, loans to fund current operating expenses accounted for the majority of the increase in the third quarter. In contrast to 2015, however, loan volumes increased in all non-real estate lending categories in the third quarter (Chart 2). Similar to the quarterly change in the total volume of non-real estate loans, operating loan volumes decreased less than 2 percent relative to the second quarter of 2018.

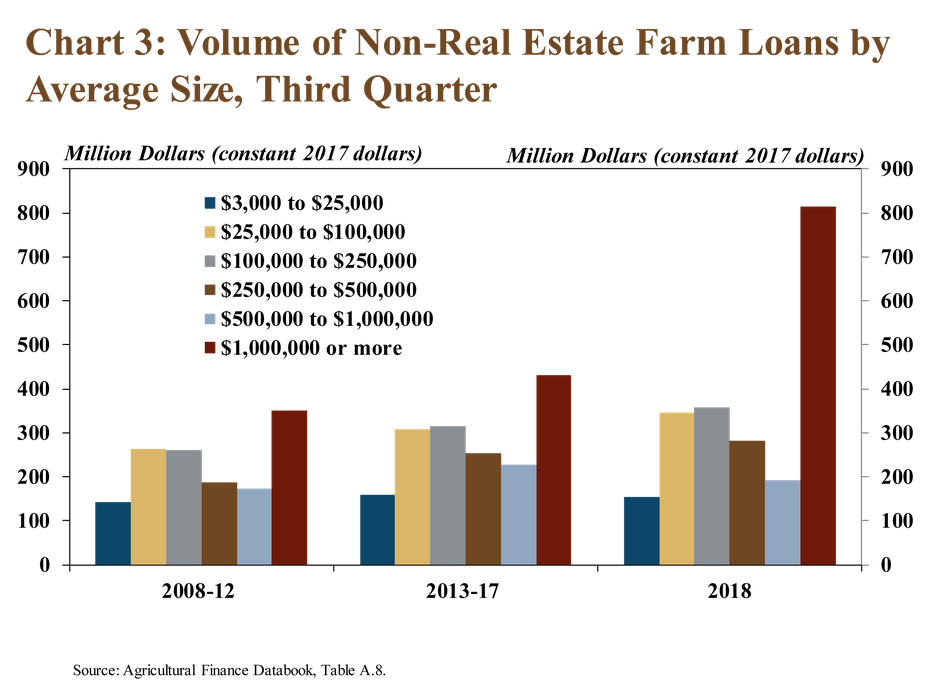

The large increase in the volume of operating loans was influenced heavily by larger-sized loans. Continuing a recent trend, the volume of very large loans rose sharply in the third quarter (Chart 3). From 2008 to 2012, the volume of individual loans larger than $1 million made by survey respondents totaled an average of about $350 million, or 25 percent of total non-real estate lending. Between 2013 and 2017, the average volume of loans larger than $1 million increased slightly, but remained unchanged as a share of total loan volumes. In the third quarter, the volume of loans larger than $1 million nearly doubled and accounted for almost 40 percent of total non-real estate lending during the reporting period.

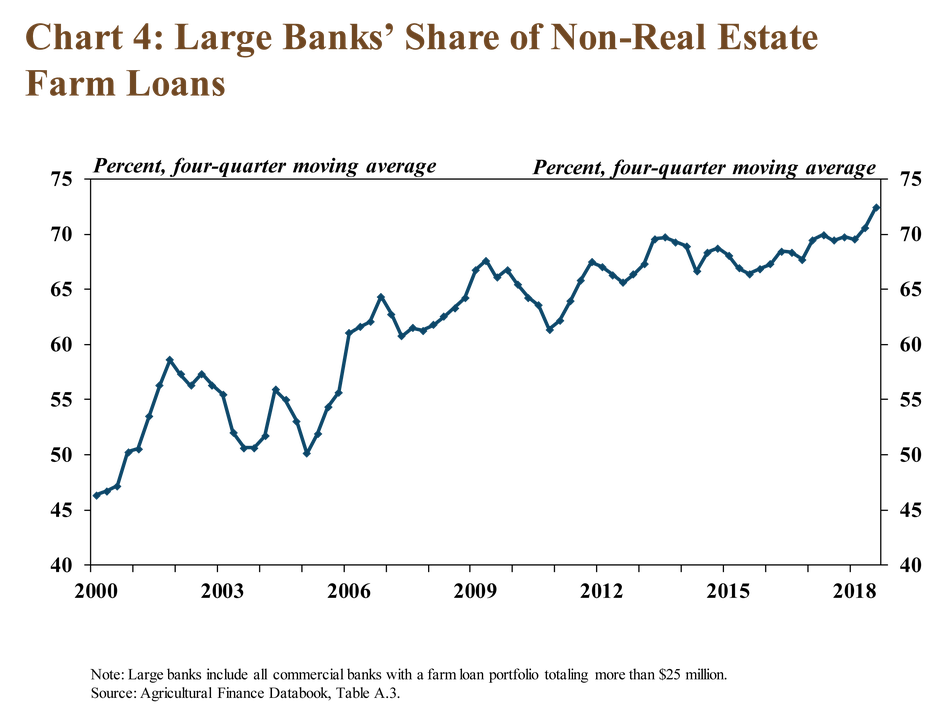

With the increase in the size of loans, there also was a large increase in the share of lending at large agricultural banks. Following a long-term trend, banks with the largest agricultural loan portfolios continued to gain a greater share of non-real estate agricultural loans (Chart 4). Bolstered by larger individual loans and growing loan portfolios, the share of all non-real estate farm loans held by large banks reached a historical high of nearly 80 percent in the third quarter, compared with 72 percent a year ago.

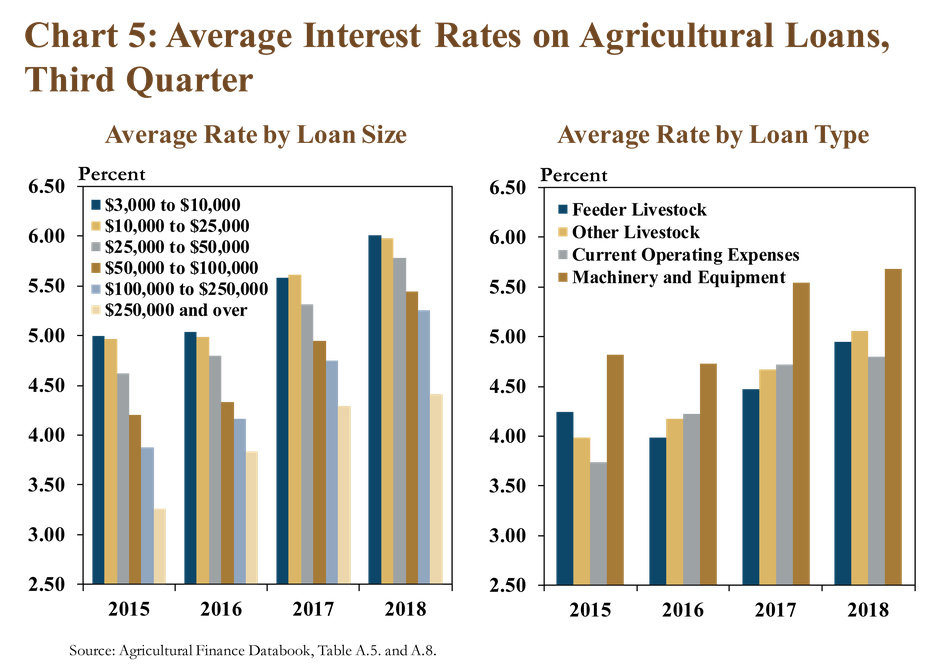

Alongside the increases in farm lending and larger-sized loans, interest rates on farm loans in the third quarter continued to rise. While rates increased across all loan sizes, the pace of increase was slower on the largest loans. In fact, the spread between rates on the smallest and largest loans increased to more than 150 basis points (Chart 5, left panel). Rates on operating loans also were slower to increase and were lower than rates on other types of non-real estate farm loans (Chart 5, right panel).

Section B - Second Quarter Call Report Data

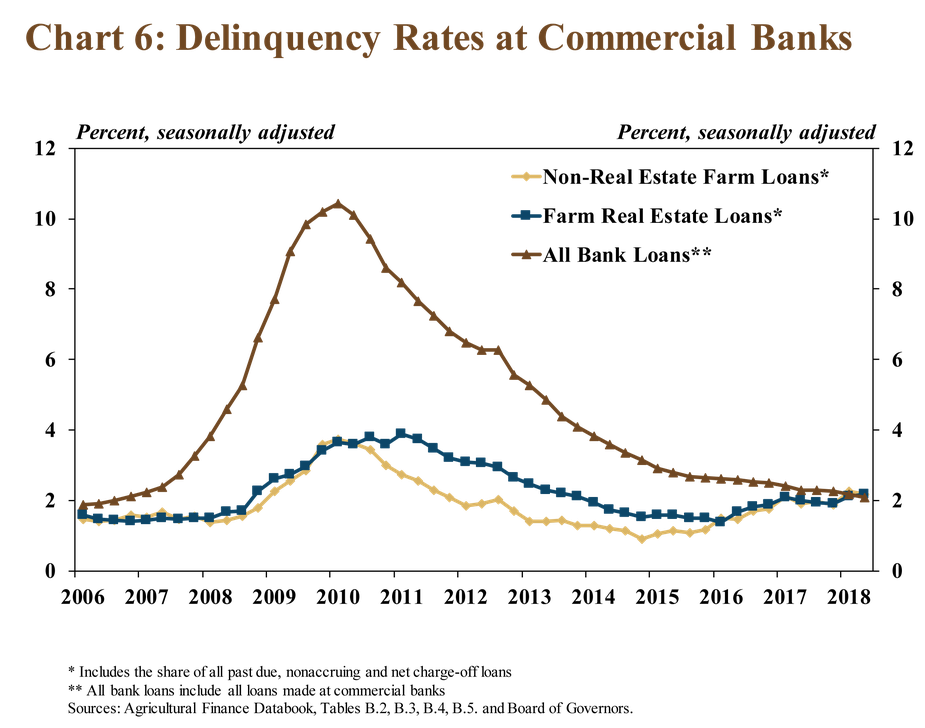

Despite additional increases in lending and increases in interest rates, delinquency rates on farm loans at commercial banks remained low through the second quarter, according to Call Report data. Delinquency rates on farm real estate loans, however, continued to trend higher at a modest pace and were higher than the rate of delinquencies on all bank loans for the first time in nearly 20 years (Chart 6). The growth in the volume of delinquent farm real estate loans was driven primarily by an increased volume of nonaccruing loans.

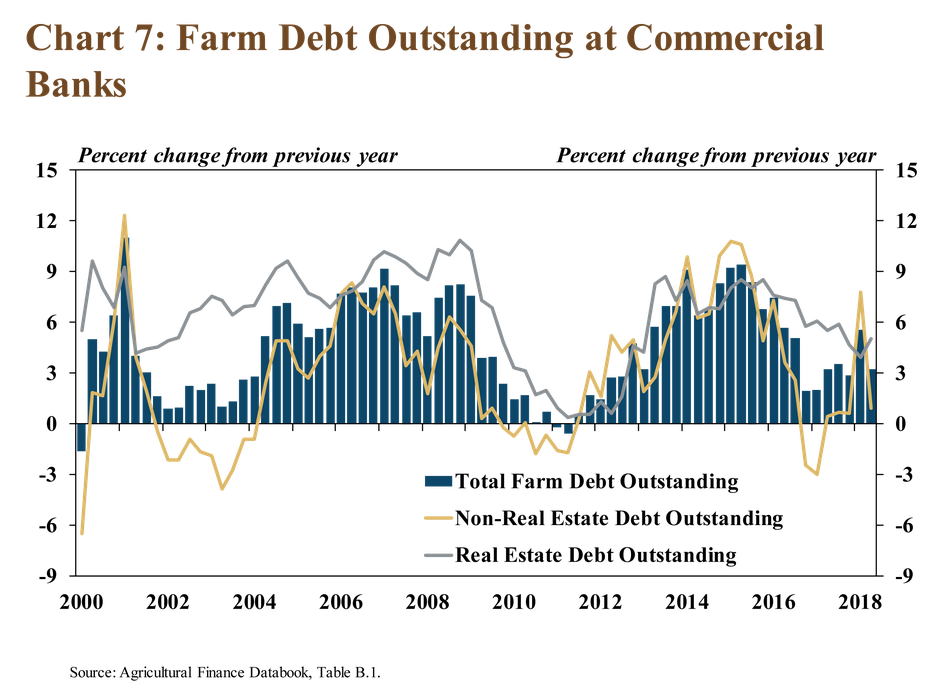

Increases in farm real estate lending remained the primary driver of additional increases in total farm debt. Loans secured by farm real estate increased 5 percent in the second quarter, slightly faster than in the previous quarter (Chart 7). Non-real estate debt increased about 1 percent from a year ago following a brief surge in the first quarter. The timing of grain sales and repayment of operating loans likely contributed to the changing rates of growth in non-real estate debt in each of the first two quarters of 2018.

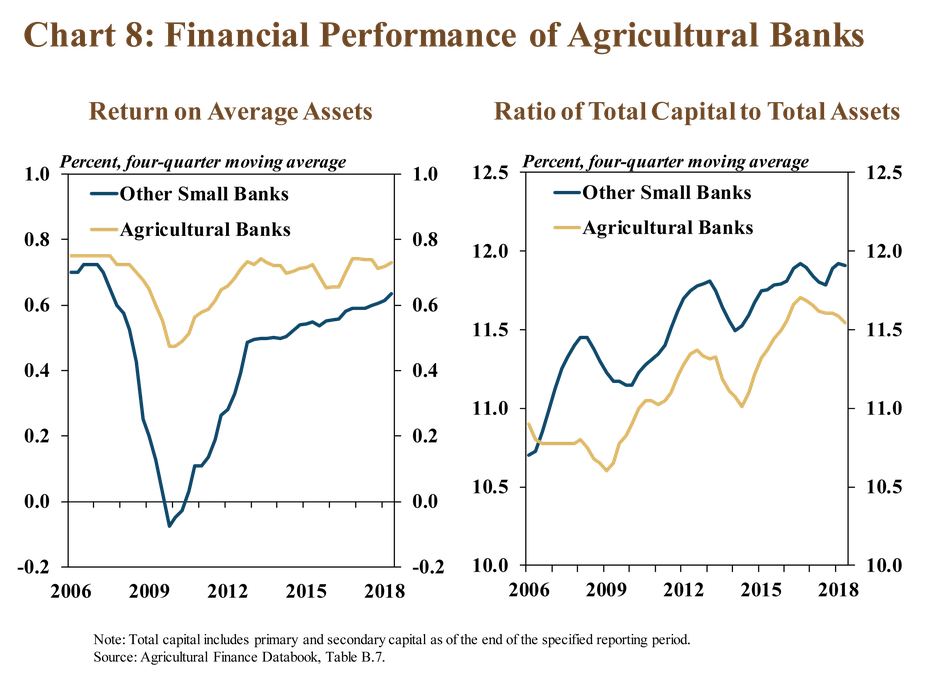

As farm debt continued to trend higher, the performance of agricultural banks across the country generally has remained solid. The historical trend of agricultural banks maintaining a higher return on average assets than other small banks continued in the second quarter (Chart 8, left panel). Despite the spread between the two narrowing slightly, the return on average assets at agricultural banks increased 5 basis points compared with the second quarter of 2017. As lending activity at agricultural banks continued to rise, the ratio of total capital to total assets continued to decline in the second quarter, but remained historically high (Chart 8, right panel).

Section C - Second Quarter Regional Agricultural Data

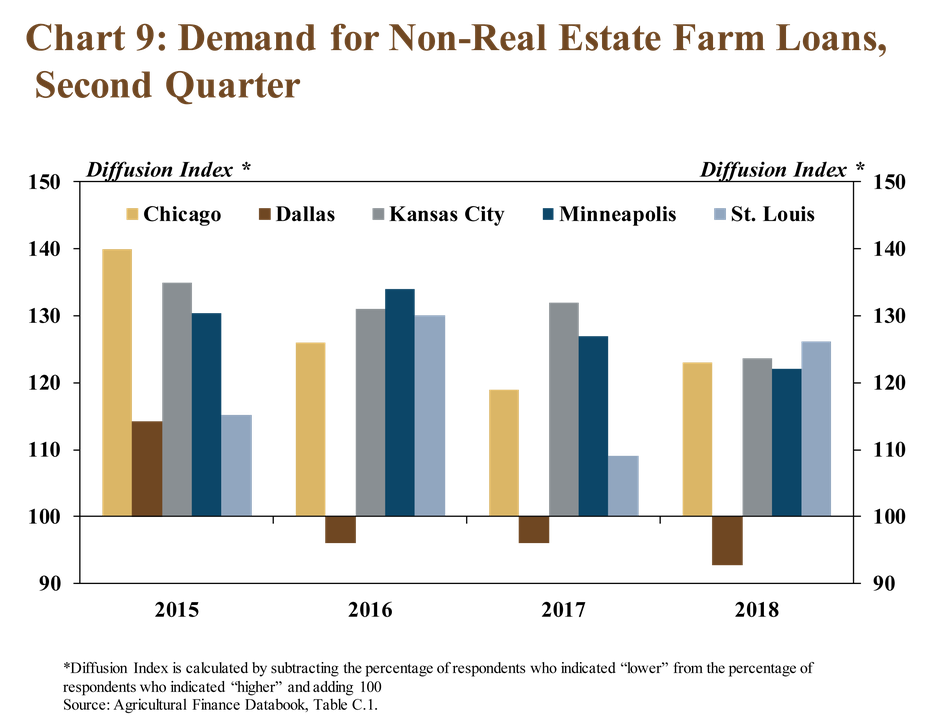

Similar to Call Report data, Regional Federal Reserve surveys also showed that demand for farm loans continued to trend higher in the second quarter. Respondents in all reporting Districts, with the exception of Dallas, indicated continued growth in demand for farm loans (Chart 9). The St. Louis District reported a large increase in loan demand compared with the second quarter of 2017 while all other Districts reported only slight changes. While indicators of loan demand in the Kansas City and Minneapolis Districts were slightly lower compared with the previous year, the demand for farm loans remained high overall.

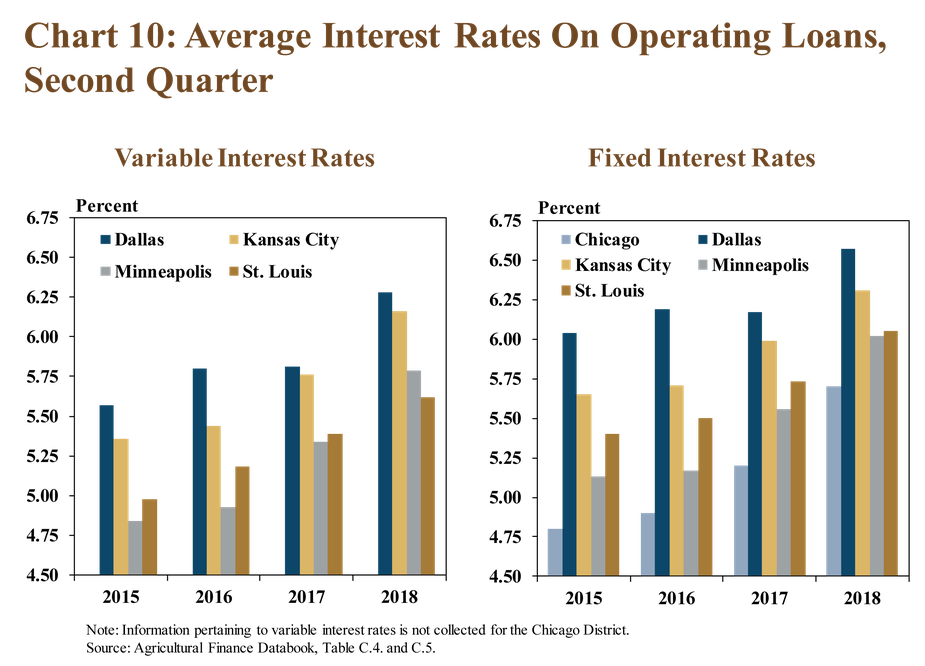

Alongside high loan demand, interest rates on farm loans also continued to rise across all Federal Reserve Districts. Variable rates increased at a slightly faster pace in the Dallas and Kansas City Districts, while fixed rates increased slightly more in the Minneapolis and St. Louis Districts (Chart 10, left panel). The Chicago District reported the largest increase for all types of interest rates on farm loans when compared with a year ago, with fixed rates increasing nearly 50 basis points (Chart 10, right panel). However, fixed interest rates still remained lowest in the Chicago District.

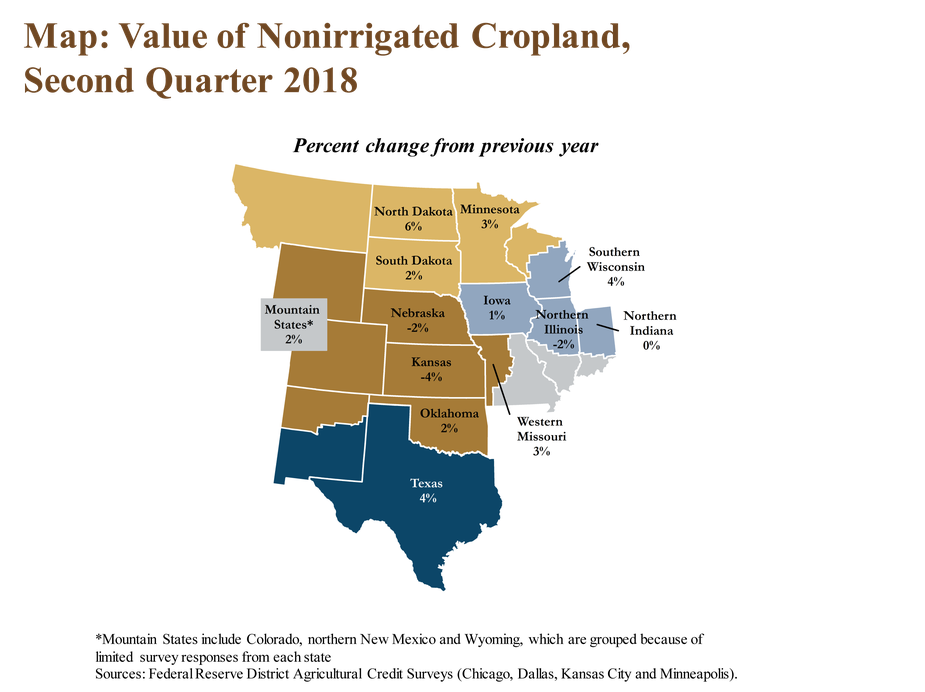

Despite additional increases in interest rates and emerging concerns about profitability in the farm sector, several Districts reported an increase in farmland values. In fact, nonirrigated farmland values increased in the majority of states in the Midwest and Plains regions, with the largest increase of 6 percent in North Dakota (Map). In comparison, values in Nebraska, Illinois and Kansas decreased slightly. In general, farmland values continued to remain relatively stable as demand for farm loans remained high and the volume of farm lending continued to increase.

In contrast to modest increases in farmland values, farm income continued to decline in all Districts that report on changes in income. Despite a slight improvement compared with 2017, farm income in the second quarter remained weak and respondents indicated they expect the trend to continue over the next three months (Chart 11). The continued weaknesses in farm income reported by agricultural banks was similar to recent farm income predictions released by the U.S. Department of Agriculture, which has forecasted U.S. farm income in 2018 to decline 13 percent from a year ago.

Conclusion

As the size of large agricultural operating loans at relatively large agricultural banks continued to increase, the volume of non-real estate farm loans rose sharply in the third quarter. The recent trend of large loans made by large banks also contributed to a modest increase in the share of farm loans held by large banks. Federal Reserve Districts continued to report high levels of demand for farm loans, even as interest rates rose further. Alongside persistently low agricultural commodity prices, bankers throughout the country expected farm income to decline in the coming months. Despite the ongoing weaknesses in farm income and agricultural credit conditions, however, delinquency rates on farm loans remained low and the performance of agricultural banks remained sound.

Data and Information

The views expressed are those of the authors and do not necessarily reflect the positions of the Federal Reserve Bank of Kansas City or the Federal Reserve System.

Authors

Nate Kauffman

Senior Vice President, Economist, and Omaha Branch Executive; Executive Director of the Center for Agriculture and the Economy