Levels of non-real estate farm lending at commercial banks remained high in the fourth quarter of 2015 despite a modest decline from a year earlier. Loans used to finance current operating expenses remained at record levels, while volumes for most other types of non-real estate loans declined slightly. As farm income declined again in 2015, persistently high short-term lending needs amplified concerns about farm sector liquidity moving into 2016, especially if farmers’ profit margins remain low. Despite these concerns, agricultural banks continued to report strong loan performance and solid returns on their assets.

Section A – Fourth Quarter National Farm Loan Data

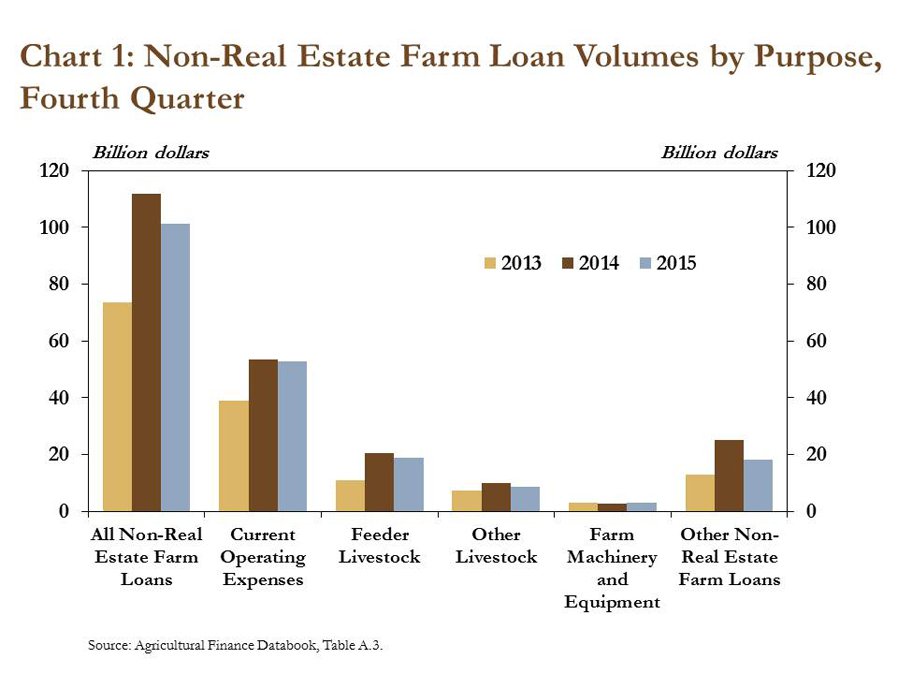

The volume of new farm loans originated at commercial banks declined, but only slightly, in the fourth quarter. Data from the Survey of Terms of Bank Lending to Farmers showed commercial banks originated $101.4 billion of non-real estate farm loans in the quarter, down 9 percent from a year earlier (Chart 1). Still, farm loans used to cover operating expenses were largely unchanged, underscoring the persistent demand for short-term cash flow support amid an ongoing environment of reduced profits. Farm loans used to finance the purchase of feeder and other livestock, however, declined slightly, coinciding with sharp losses on feedlot closeouts in late 2015.

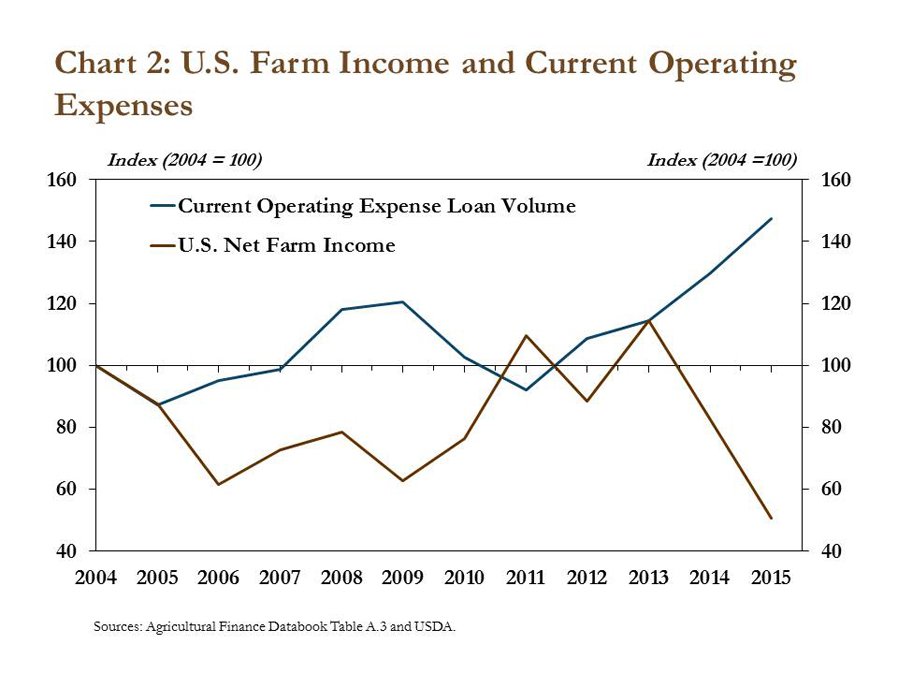

Recent acceleration in the demand for short-term loans, combined with renewed expectations of lower farm income highlight intensifying concerns surrounding liquidity. The volume of loans to cover current operating expenses remained historically high in the fourth quarter. In fact, the average volume of operating loans in 2015 was 6 percent higher than 2014 and more than double the low mark set in 2011. The increases in short-term lending, however, have occurred amid a significant decline in income (Chart 2).

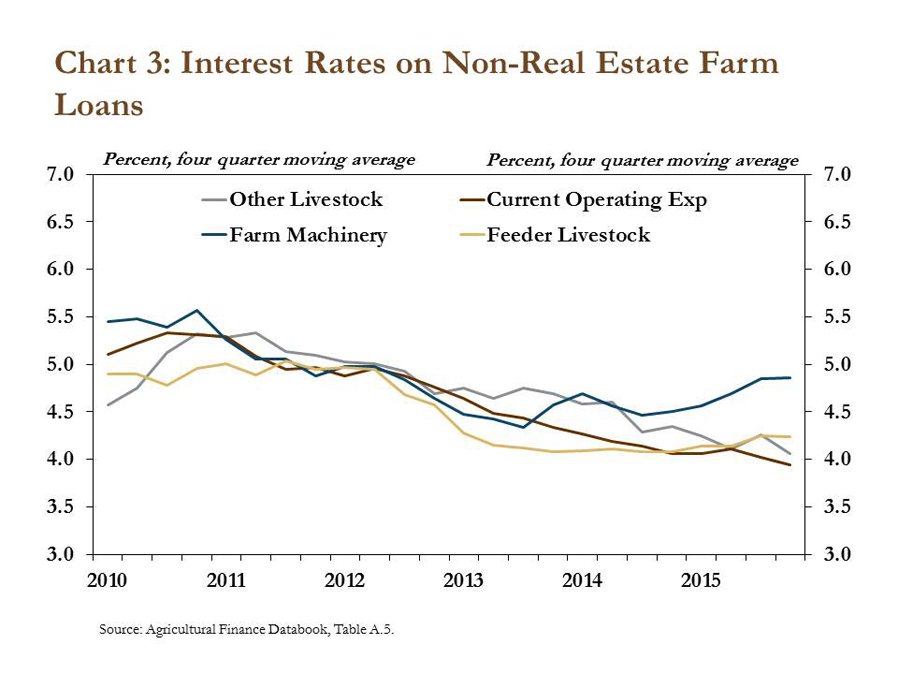

Though farm income has continued to weaken, interest rates generally have remained unchanged. For most loan types, average interest rates trended lower through 2015 (Chart 3). Loans for farm machinery, however, were a notable exception to this downward trend. These loans typically carry much longer maturities and may be priced higher due to forward-looking risks. Farm sector interest rates generally have remained historically low due, in part, to relatively strong loan performance, historically low delinquency rates, low debt-to-asset ratios in the farm sector and regional loan competition. Moreover, interest rates in each loan category declined in the fourth quarter.

Section B – Third Quarter Call Report Data

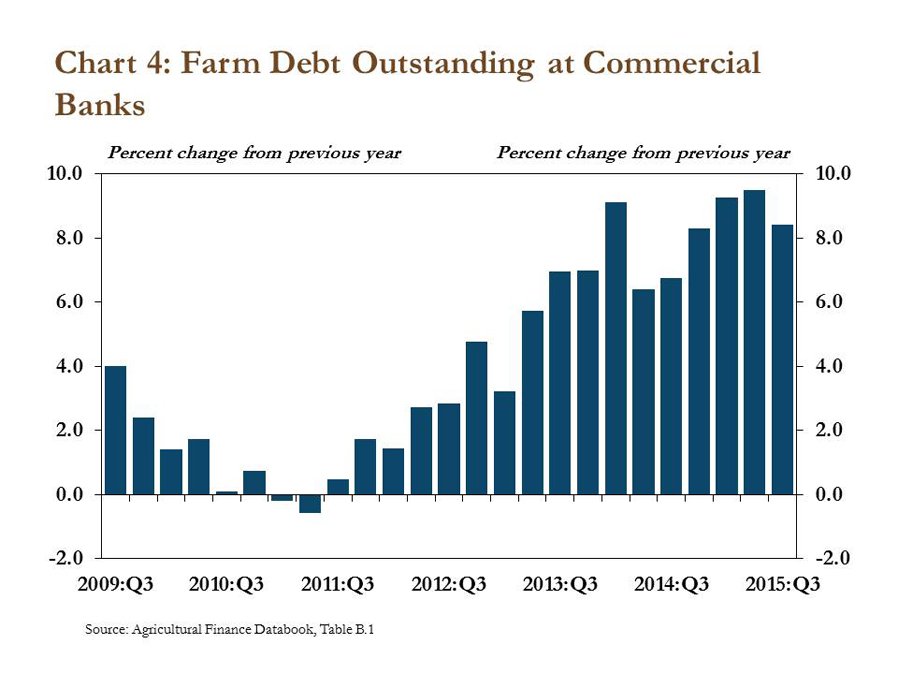

Through the third quarter, farm debt outstanding at commercial banks continued to increase, but at a slower rate than in previous quarters. Debt for both non-real estate and real estate farm loans increased more than 8 percent in the third quarter, more than a year earlier, but slightly less than in the first half of 2015. Although the pace of debt expansion slowed slightly from the previous quarter, the pace remained elevated when compared to recent years (Chart 4). Amid growing debt levels, average loan-to-deposit ratios at agricultural banks climbed for the third consecutive year and rose to almost 80 percent in the third quarter.

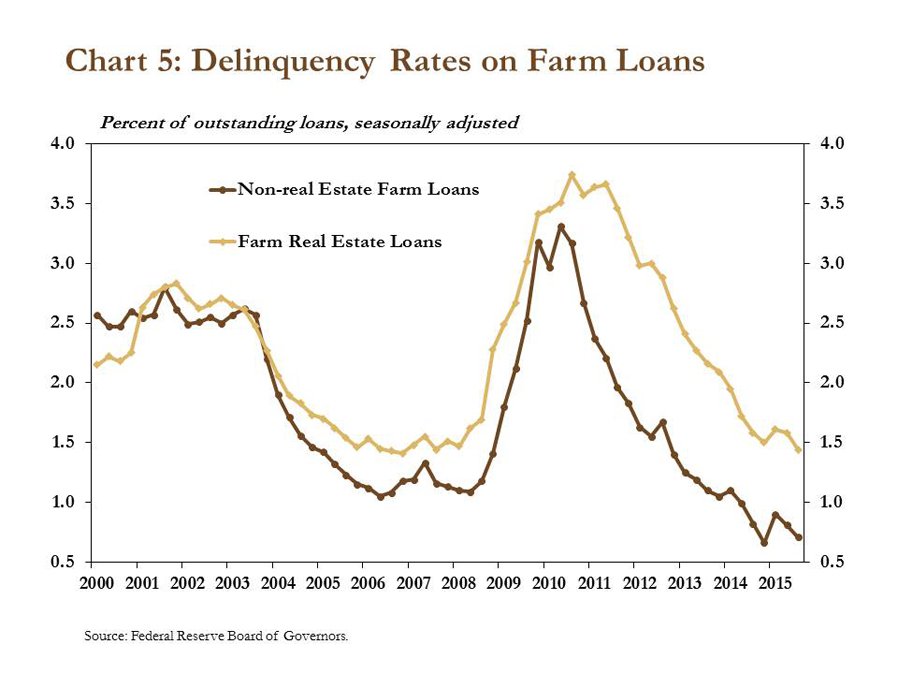

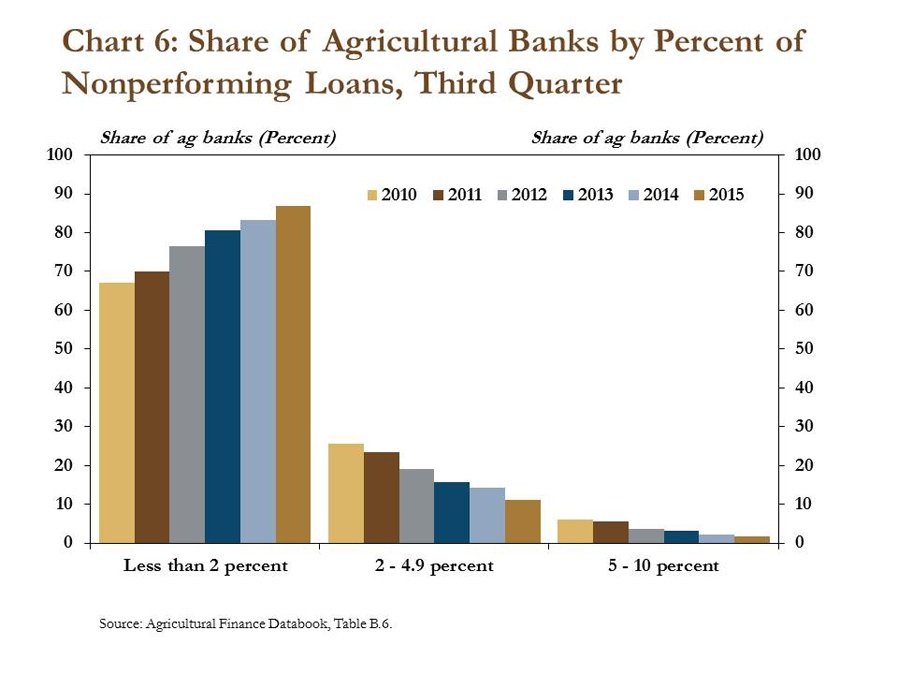

Despite increasing debt levels, loan quality at agricultural banks remained strong and shares of delinquent and nonperforming loans declined in the third quarter. Delinquency rates on loans for farm real estate and non-real estate dropped to 1.4 percent and 0.7 percent, respectively (Chart 5). According to commercial bank call report data, 98 percent of agricultural banks had less than 5 percent of their total loans listed as nonperforming (Chart 6). In fact, the average share of nonperforming farm production loans at agricultural banks was 0.5 percent, the lowest on record for non-real estate farm loans.

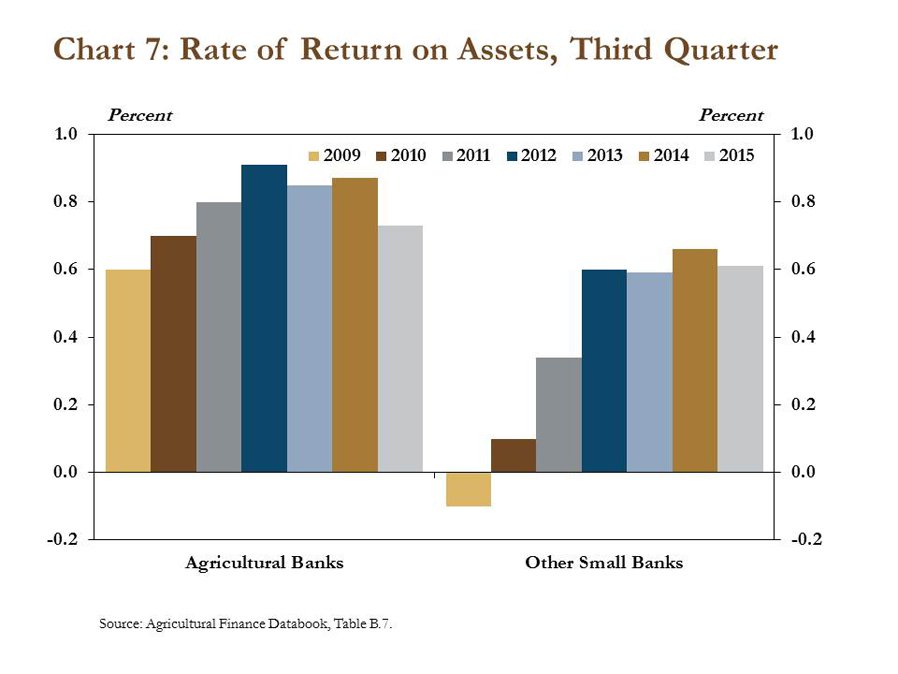

Although loan quality remained stable, the performance of agricultural banks slowed slightly. Amid increased lending activity and strong credit quality, returns at agricultural banks had grown steadily in recent years (Chart 7). In the third quarter, however, the average rate of return on assets at agricultural banks declined to 0.73 percent from 0.87 percent a year earlier. Despite the recent decline, though, returns at agricultural banks remained higher than at other banks of similar size.

Section C – Third Quarter Regional Agricultural Data

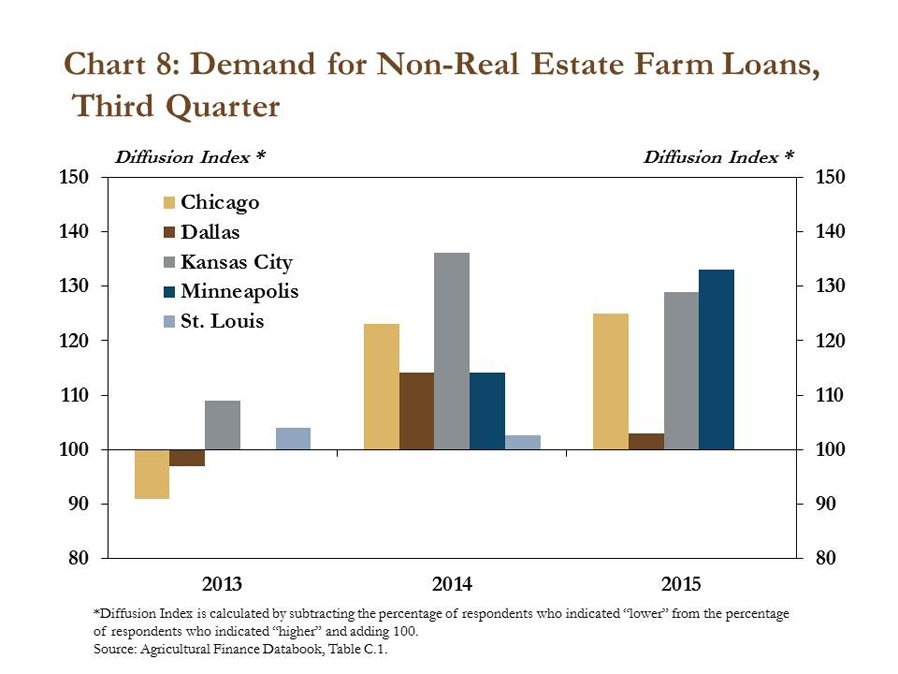

Regional Federal Reserve surveys of agricultural credit conditions also pointed to persistently strong demand for non-real estate farm loans. Districts with a relatively high concentration of agricultural production—Chicago, Dallas, Kansas City and Minneapolis—reported increased demand for non-real estate farm loans in the third quarter (Chart 8). The increase reported in third-quarter Federal Reserve surveys marked the fourth consecutive quarter of higher demand for farm loans and was consistent with recent national trends.

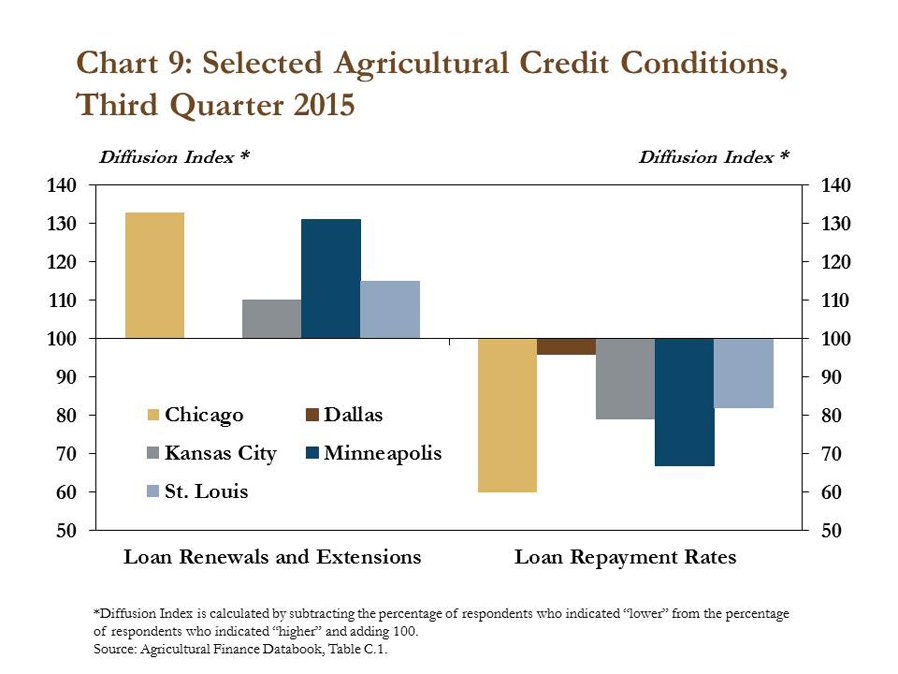

In addition to heightened demand for non-real estate farm loans, demand for renewals and extensions also rose in the third quarter. For the third consecutive quarter in 2015, the Federal Reserve Districts of Chicago, Kansas City, Minneapolis and St. Louis reported an increase in the demand for loan renewals and extensions while also reporting further decreases in loan repayment rates (Chart 9). The changes in the third quarter were especially pronounced in the Chicago and Minneapolis Districts.

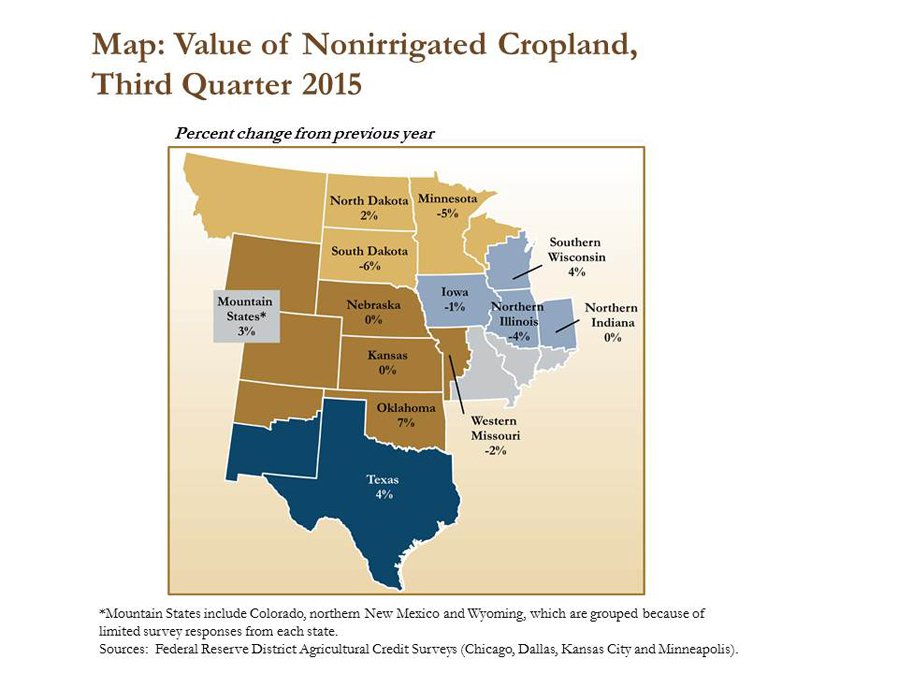

Despite increased demand for non-real estate farm loans and declining repayment rates, farmland values generally remained steady in the third quarter. According to Federal Reserve surveys, values of good quality, nonirrigated farmland continued to rise modestly in states on the periphery of the Corn Belt, with the largest gains in the southern plains (Map). Consistent with recent trends, farmland values declined modestly throughout the Corn Belt, with Minnesota and South Dakota experiencing the largest declines.

Conclusion

Farm lending activity at commercial banks remained elevated through the end of 2015. Agricultural credit conditions continued to tighten somewhat as repayment rates softened further and demand for renewals and extensions continued to rise. Overall loan performance, however, generally remained strong through 2015. Still, persistently high demand for farm loans coupled with further declines in farm income remains a concern heading into the 2016 production season.

The views expressed are those of the authors and do not necessarily reflect the positions of the Federal Reserve Bank of Kansas City or the Federal Reserve System.

Authors

Nate Kauffman

Senior Vice President, Economist, and Omaha Branch Executive; Executive Director of the Center for Agriculture and the Economy