Demand for livestock loans grew in the third quarter, boosting agricultural lending activity at commercial banks. Demand for operating loans was more subdued however, and total non-real estate lending remained near its average of the past decade. The average size of loans for some livestock categories reached an all-time high and contributed to the increased lending. While the average size of operating loans also remained elevated, a smaller number of loans limited the overall financing of operating expenses.

The U.S. agricultural economy generally remained strong as elevated commodity prices continued to support farm incomes. Prices of most major crops were at multi-year highs moving into fall harvest and supported farm revenue prospects. Weakness in the cattle industry persisted, however, as low cattle prices continued to limit profit margins for producers. In addition, concerns about drought and higher input costs continued to intensify and likely contributed to an increase in producers’ financing needs in the livestock sector.

Third Quarter National Survey of Terms of Lending to Farmers

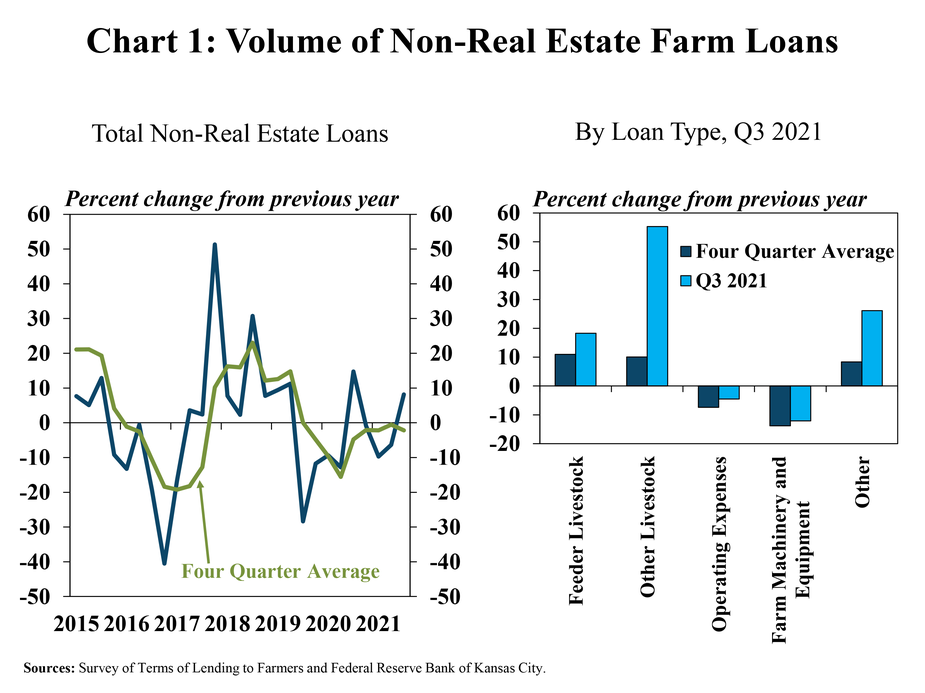

The volume of non-real estate farm loans increased in the third quarter, but some types of lending remained limited. Total non-real estate lending was about 8% higher than a year ago but has declined at an average pace of about 2% over the last four quarters (Chart 1). A large share of the increase during the quarter was due to an increase in loans used to finance feeder livestock and other livestock, which grew by about 20% and more than 50%, respectively. In contrast, operating loan volumes declined by about 5%.

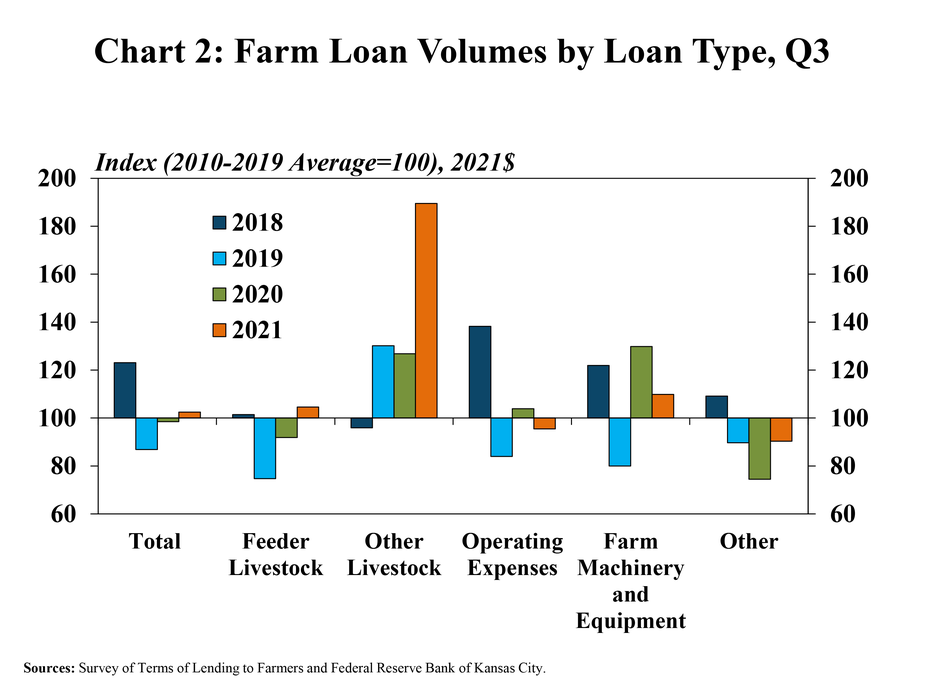

With sharp increases from a year ago, lending for livestock purchases continued to trend above the recent historical average for the third quarter. The volume of loans for poultry and livestock other than feeders (other livestock) was nearly double the inflation adjusted average during the same quarter from 2010-2019 (Chart 2). Feeder livestock loans were also slightly greater than the recent average while operating loans were slightly less.

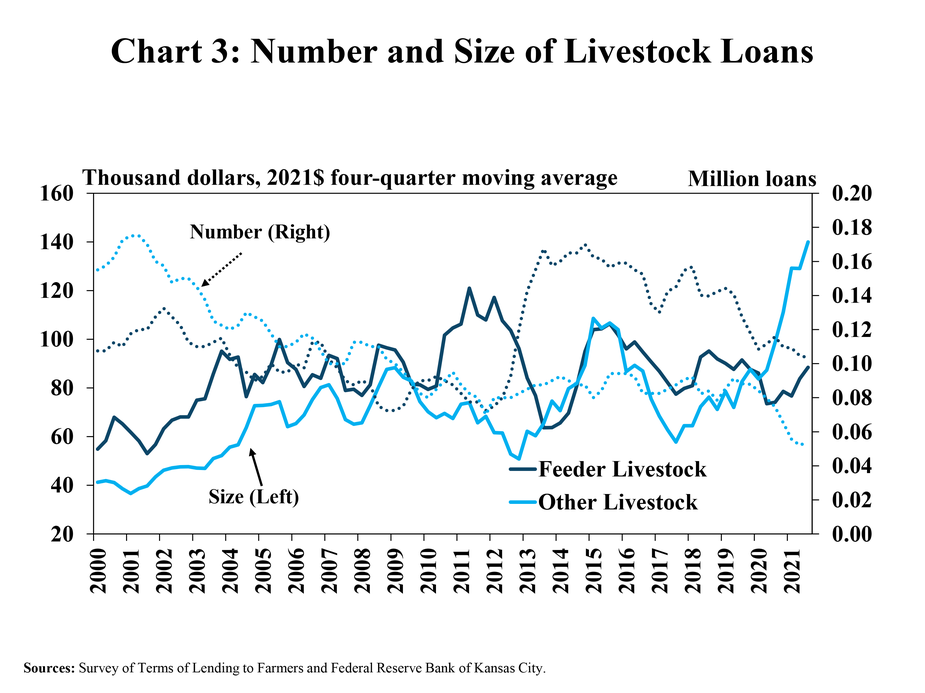

The increase in livestock loan volumes was driven by larger loan sizes. The average size of loans for other livestock continued a sharp upward trend, increasing about 30% in the third quarter and reaching an all-time high (Chart 3). The number of other livestock loans was also higher than a year ago but remained historically low. Similarly, the average size of feeder livestock loans has also increased steadily over the past year, but the number of loans declined for the fourth straight quarter.

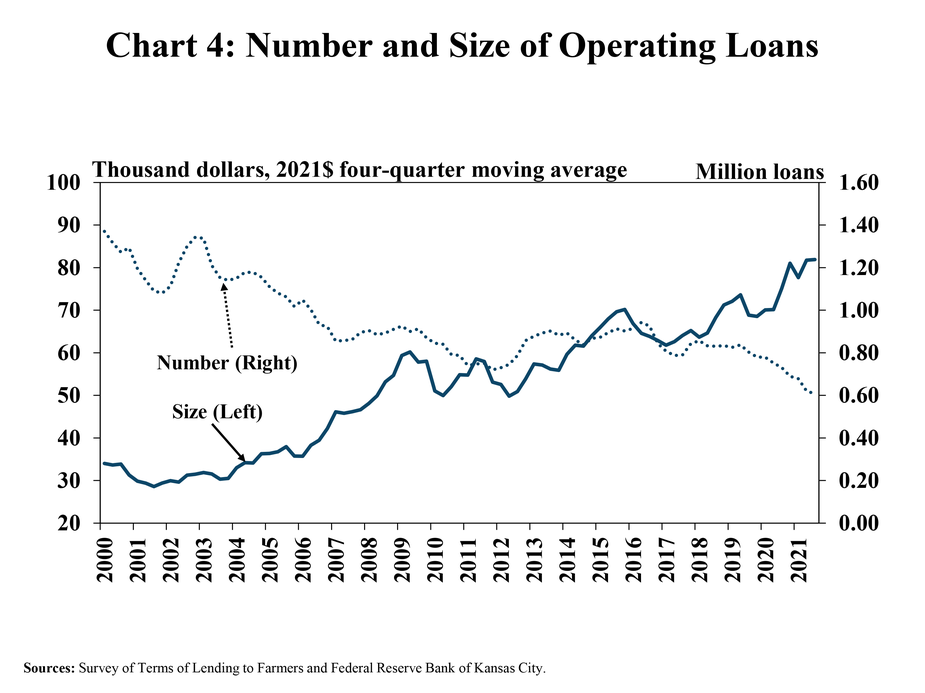

While the size of livestock loans increased sharply, the growth in the size of operating loans was less pronounced. The average size of operating loans remained elevated but was only about 5% larger than a year ago (Chart 4). The number of operating loans continued to trend downward and remained historically low, limiting any gains in loan volumes.

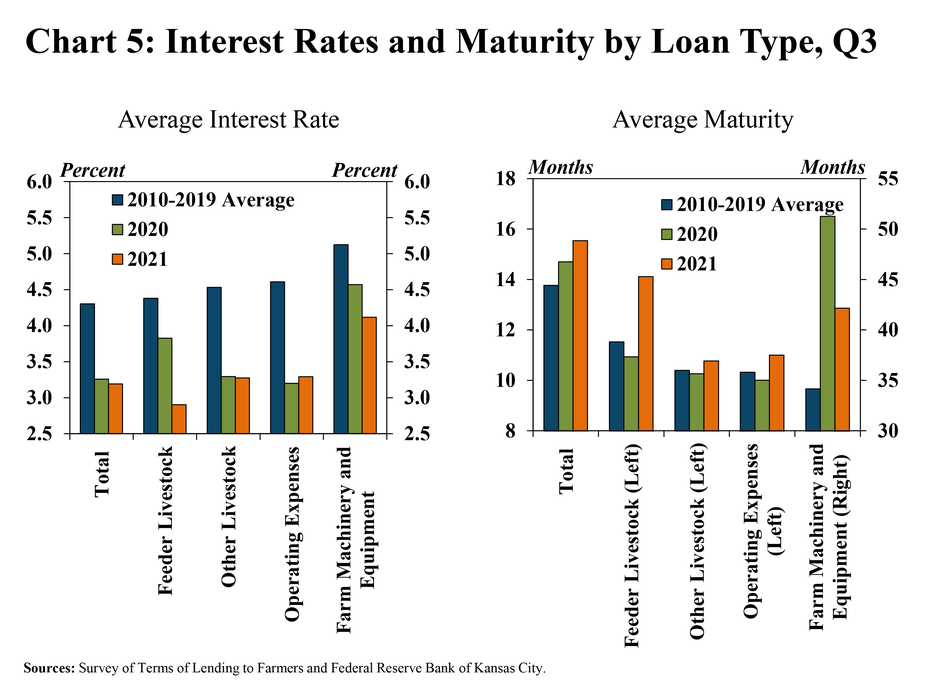

Alongside an increase in loan sizes, interest rates remained low, and loan durations were higher than recent averages. Rates charged on all types of loans except operating loans declined slightly from a year ago and reached an all-time low for the third quarter (Chart 5). The average maturity of all types of loans, except machinery and equipment loans, were higher than a year ago.

Data and Information

National Survey of Terms of Lending to Farmers Historical Data

National Survey of Terms of Lending to Farmers Tables

About the National Survey of Terms of Lending to Farmers

The views expressed are those of the authors and do not necessarily reflect the positions of the Federal Reserve Bank of Kansas City or the Federal Reserve System.

Authors

Nate Kauffman

Senior Vice President, Economist, and Omaha Branch Executive; Executive Director of the Center for Agriculture and the Economy