The U.S. farm economy weakened further in the third quarter despite an upward revision to farm income projections. Following a brief rebound in crop prices in the second quarter, profit margins for crop producers deteriorated in August and September. Profit margins also remained poor in the cattle and dairy sectors. Agricultural credit conditions have weakened further as loan repayment problems have picked up steadily, and bankers throughout the Tenth Federal Reserve District have expressed increasing concerns about the softening farm economy spilling over to Main Street business activity in rural areas.

Farm Income

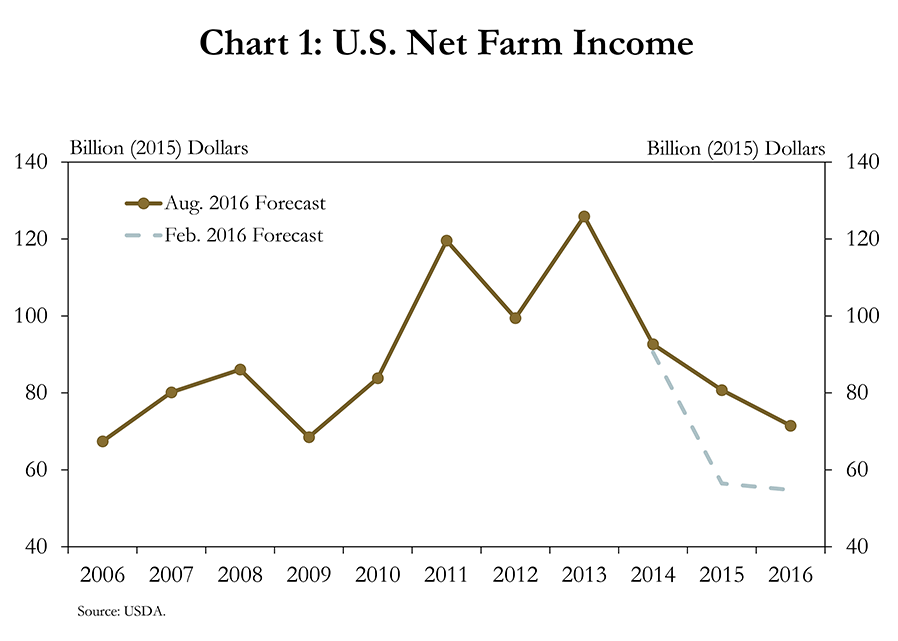

In August, expectations for 2016 farm income were revised up modestly from the February forecast, but income was still expected to decline notably from a year ago. The U.S. Department of Agriculture’s August revision can be interpreted as both positive and negative for the farm sector. On the positive side, farm income expectations for 2015 and 2016 were revised up by 43 percent and 31 percent, respectively (Chart 1). On the negative side, however, the expected decline in farm income from 2015 to 2016 widened from 3 percent earlier in the year to 11 percent in the most recent report. Essentially, farm income was higher than initially forecasted, but the deterioration from a year ago is now believed to be sharper than expected.

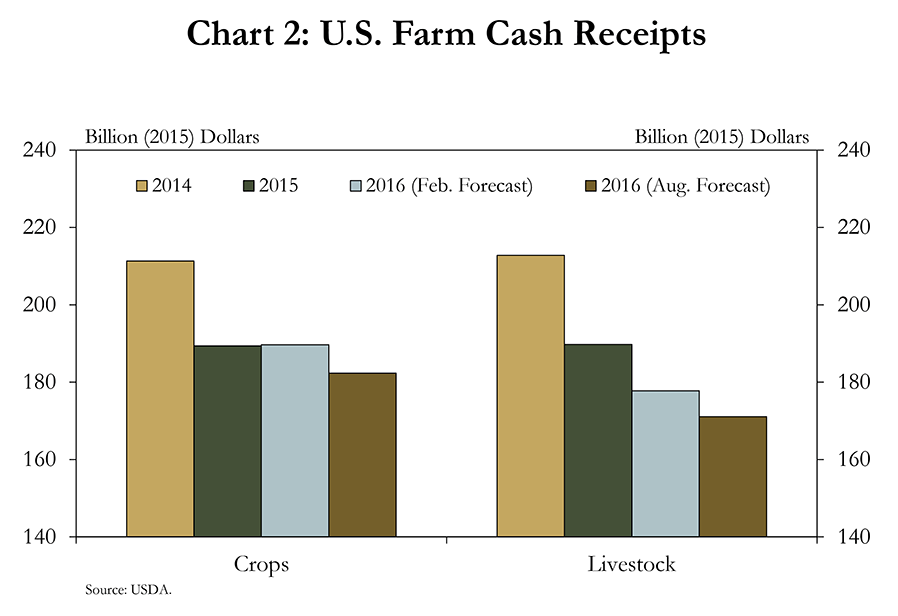

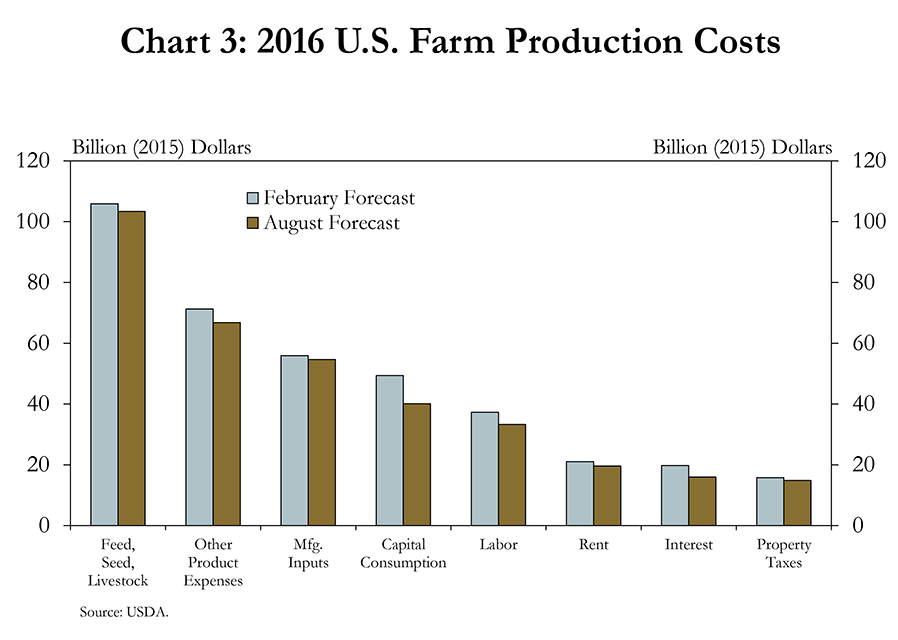

The improvement in farm income expectations was largely due to downward revisions in production costs for the farm sector as revenue expectations continued to weaken. Whereas cash receipts in the crop sector generally were expected to remain unchanged in February, the revision in August pointed to a decline of about 4 percent from a year ago (Chart 2). Similarly, in the livestock sector, the August report predicted a 10 percent drop in cash receipts from a year ago, slightly more than expected in February. Production costs for 2016, however, were also revised lower and more than offset the more pessimistic outlook for revenue. Total production expenses in the farm sector were anticipated to be more than 7 percent less than expected earlier in the year, with much of this adjustment coming from a reduction in capital outlays (Chart 3).

Profit Margins

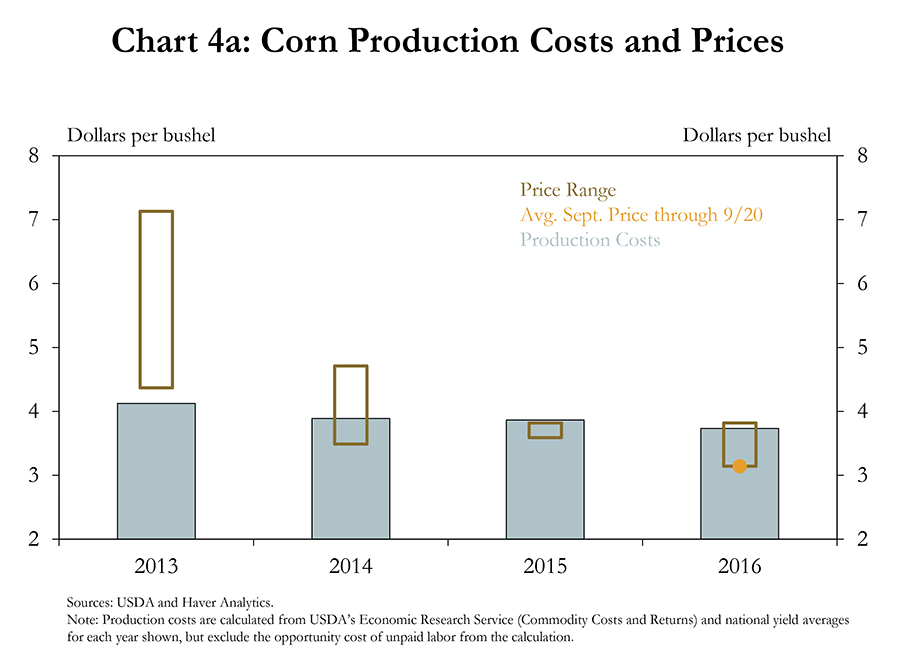

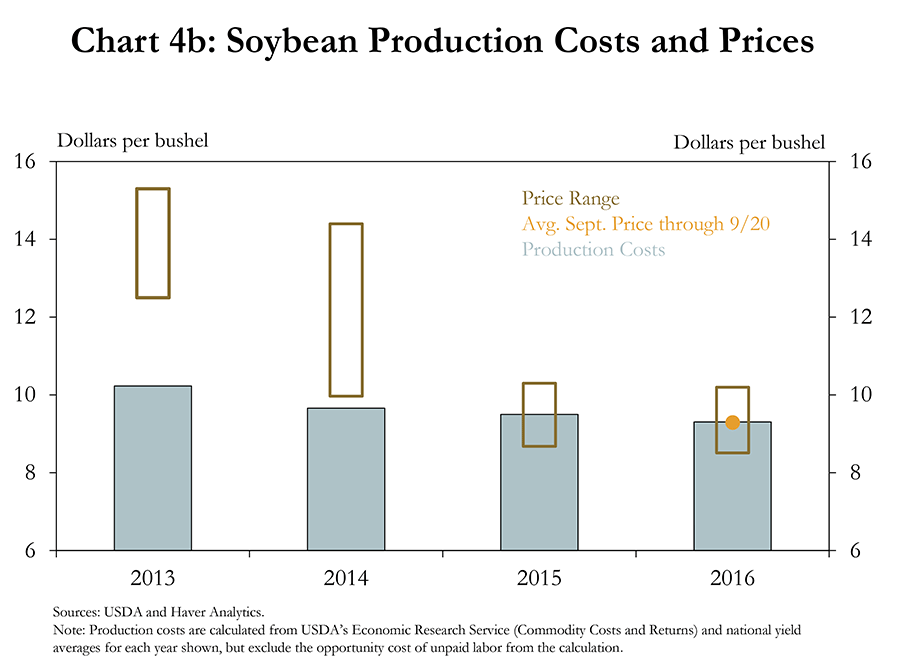

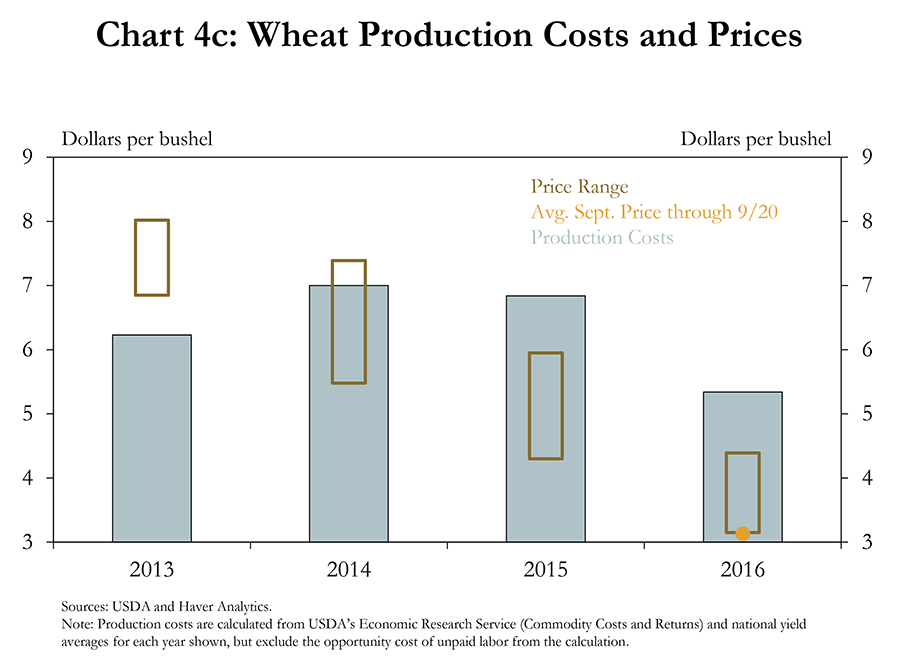

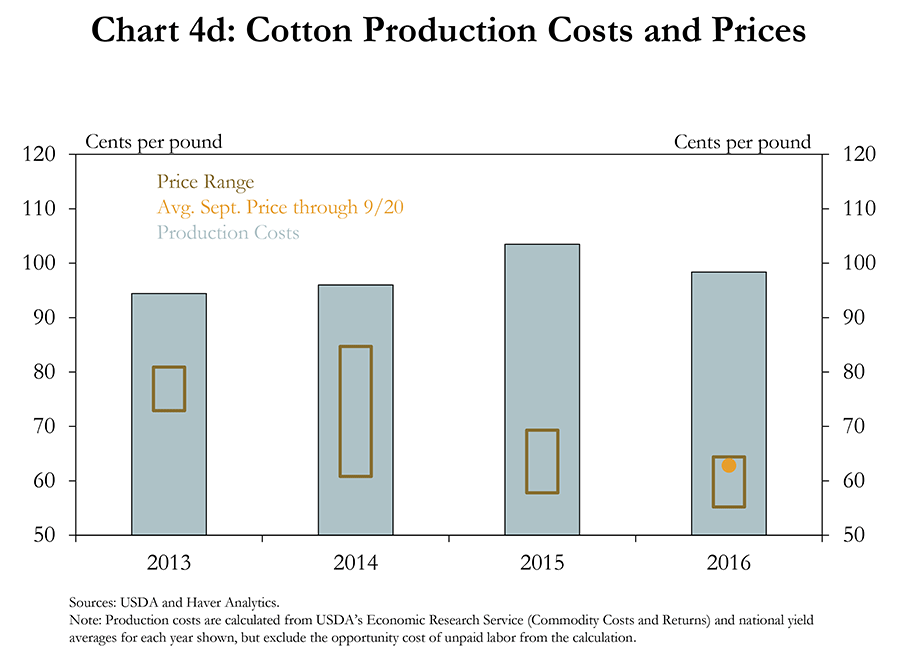

Although U.S. farm income expectations were revised up in August, profit margins for many producers of major U.S. agricultural commodities weakened significantly in the third quarter. In the crop sector, the range of average monthly prices throughout 2016 has left very few opportunities for producers to sell at a profit (Charts 4a – 4d). Since 2013, profit margins have dropped precipitously for corn, soybeans, wheat, and cotton, and both wheat and corn prices were hovering at or near 10-year lows in September.

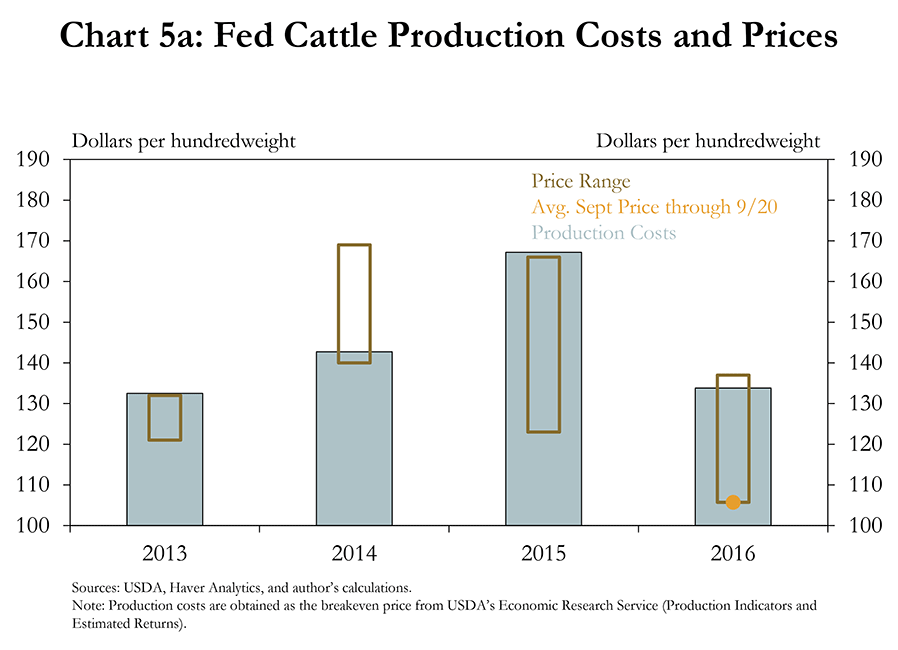

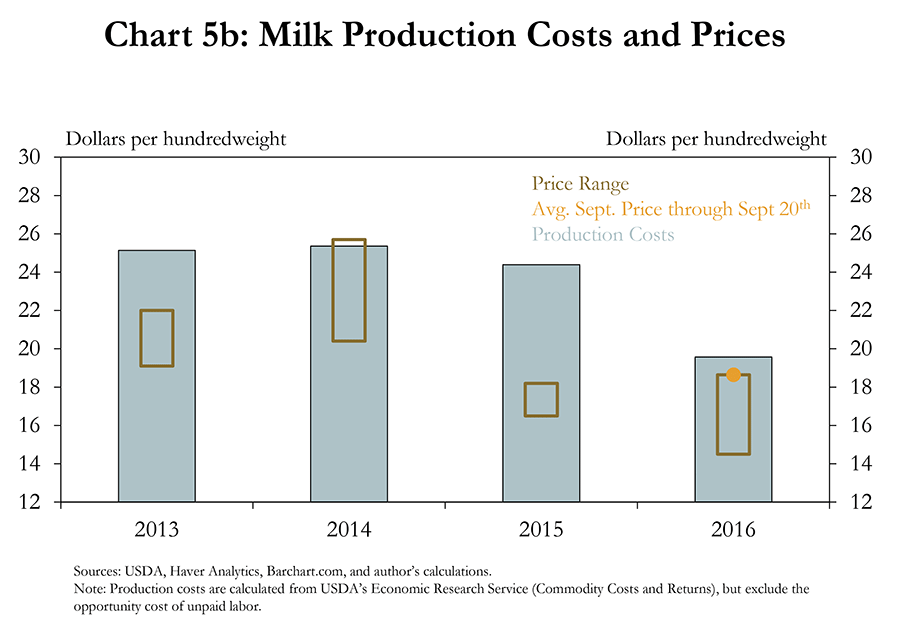

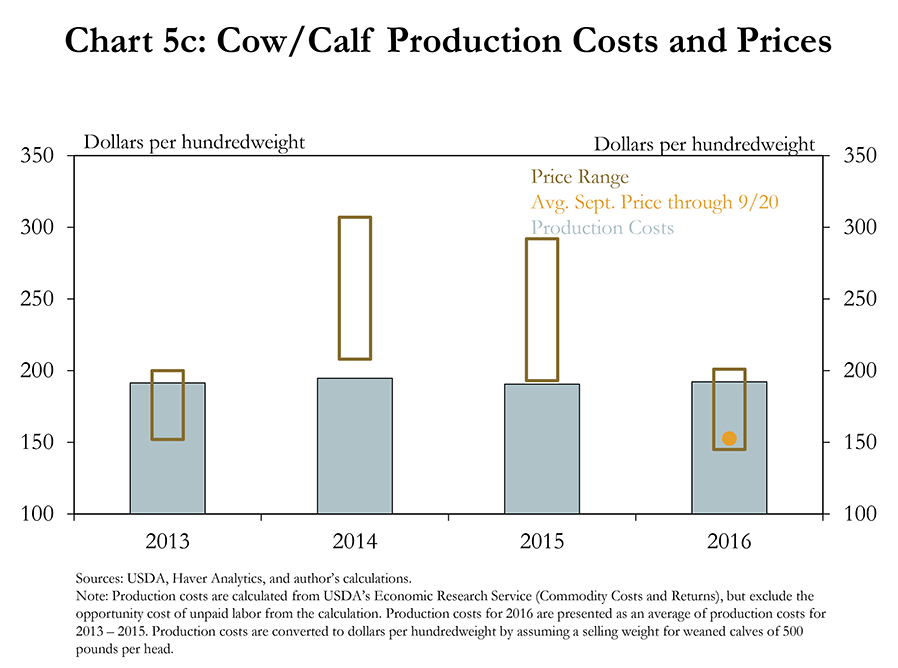

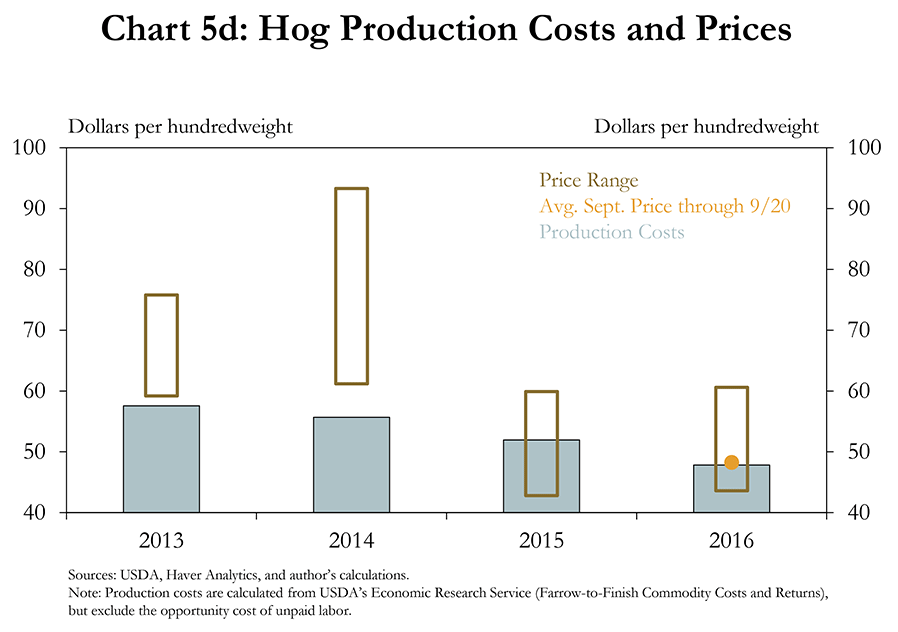

Profit margins in the livestock sector have also dropped sharply over the past few years (Charts 5a – 5d). In the cattle sector, losses at feedlots have persisted in 2016, following extreme losses toward the end of 2015. Profit margins have also remained weak in the dairy sector, and have narrowed considerably in the cow/calf sector following two consecutive years of strong profits. Among the major livestock markets, only profit margins in the hog sector generally have been positive in 2016, although prices were near breakeven toward the end of the third quarter.

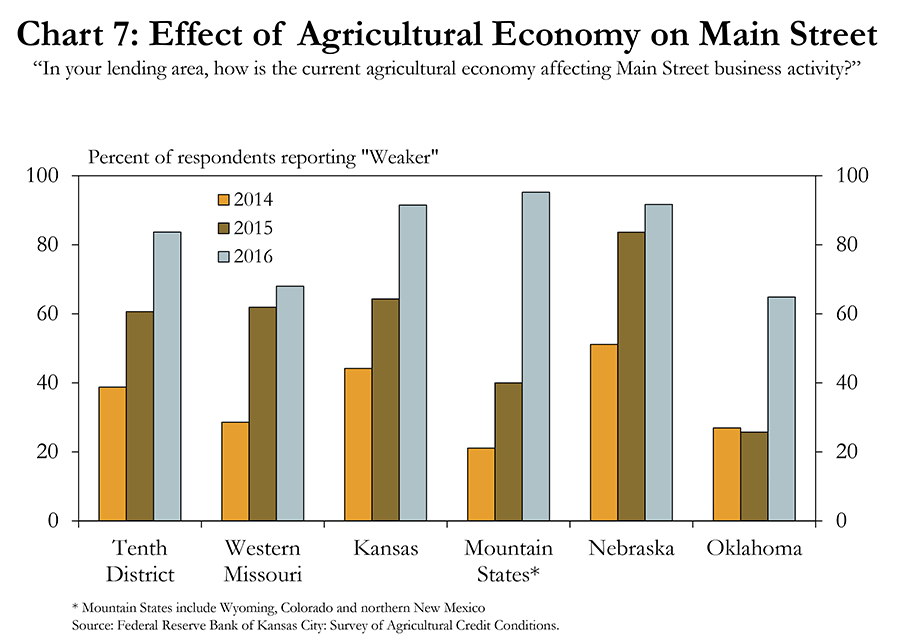

Credit Conditions and Spillovers

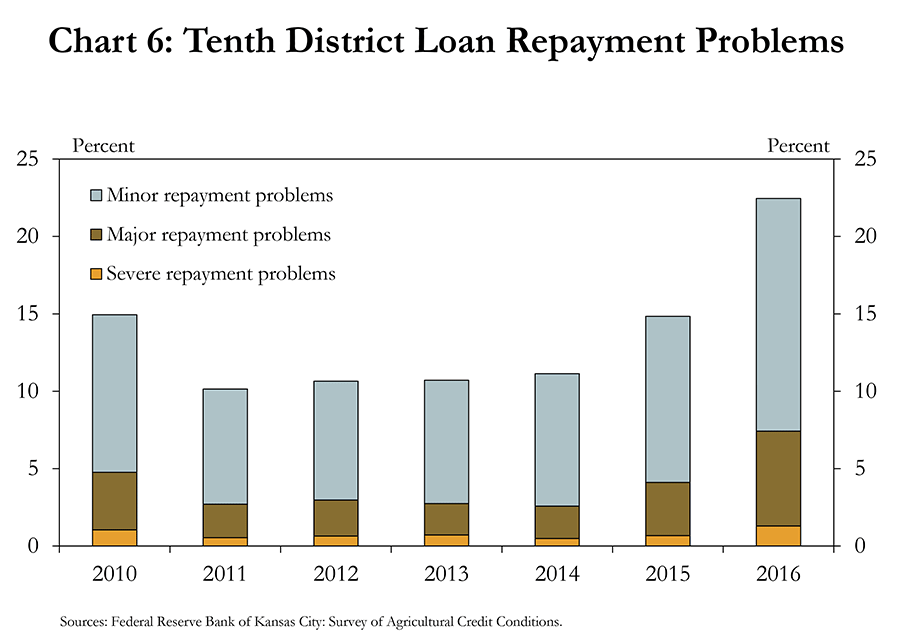

The downturn in the agricultural economy has continued to affect credit conditions in the sector. From 2010 to 2014, borrowers had few problems repaying loans. Since 2014, though, bankers in the Tenth Federal Reserve District have consistently reported an increase in the severity of loan repayment problems (Chart 6). As of the second quarter of this year, Tenth District bankers indicated that more than 7 percent of their agricultural loans were experiencing either “major” or “severe” repayment problems, an increase from just 4 percent in 2015.

Bankers in the Kansas City Fed District also continued to point to spillover effects from the softening farm economy to Main Street business activity. As the downturn in the farm economy began in earnest in 2014, only 40 percent of District bankers indicated that the downturn was having a negative effect on their broader business environment at that time (Chart 7). Halfway through 2016, however, more than 80 percent of District bankers had indicated the downturn was causing ripple effects on Main Street in their rural lending area.

Conclusion

The outlook for the farm economy has continued to worsen through 2016, despite some occasional rebounds in income and profit margins. As 2016 winds down, there will be increasing focus on the outlook for 2017 and likely more questions about the ability of some producers to continue to operate after experiencing losses for multiple consecutive years. Many producers have relied more heavily on short-term financing and restructured debt to get through 2016, but if the outlook for cash flow remains poor during the next loan renewal season, some producers may need to consider more aggressive alternatives to shore up depleted working capital.