The emergence of COVID-19 in the United States has created substantial challenges for all segments of the meat supply chain, but especially for producers and consumers. Beginning in April 2020, outbreaks of COVID-19 at meatpacking plants led to significant disruptions and created issues of oversupply and low prices for livestock producers. These disruptions temporarily reduced meat production, which led to higher prices for consumers, making it more difficult for some households to purchase meat. Consumers also shifted purchases of meat from foodservice to retail outlets, creating logistical challenges in the supply chain and putting additional upward pressure on wholesale and retail prices. Meat production continued to lag 2019 levels even after plants reopened, and changing consumer patterns could have persistent effects on supply chains.

Production Disruptions and Consumer Shifts in the Supply Chain

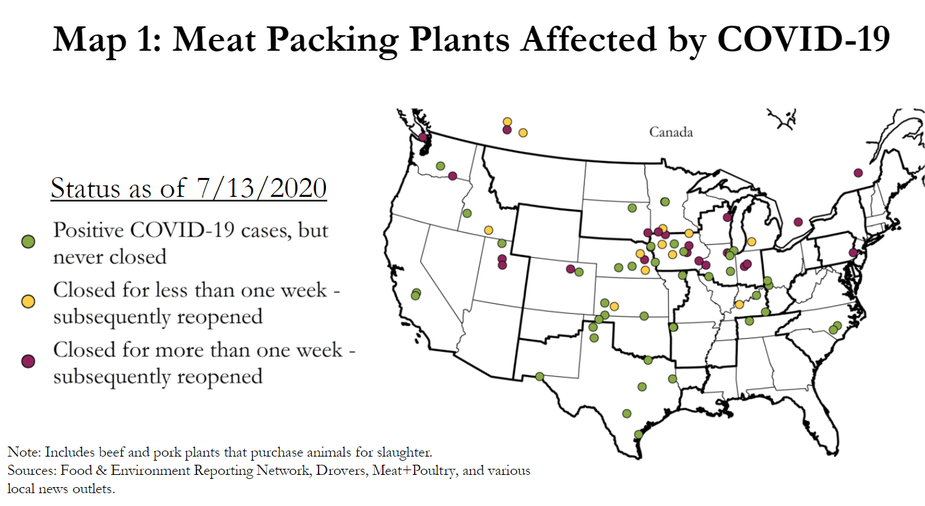

The spread of COVID-19 among employees led to closures and slowdowns at many meatpacking plants across the United States. Closures were especially prominent in beef and pork industries. From April to June, more than 80 beef and pork packing plants reported confirmed cases of COVID-19. On average, about 10% of employees at beef and pork plants tested positive for COVID-19. At some plants, COVID-19 affected as many as 30% to 70% of the workforce. Almost half of the plants with outbreaks closed for some time (Map 1). Most facilities that did were closed for more than one week. Plants that did not close or that reopened after a temporary closure typically slowed operations due to the need for social distancing and other precautionary measures.

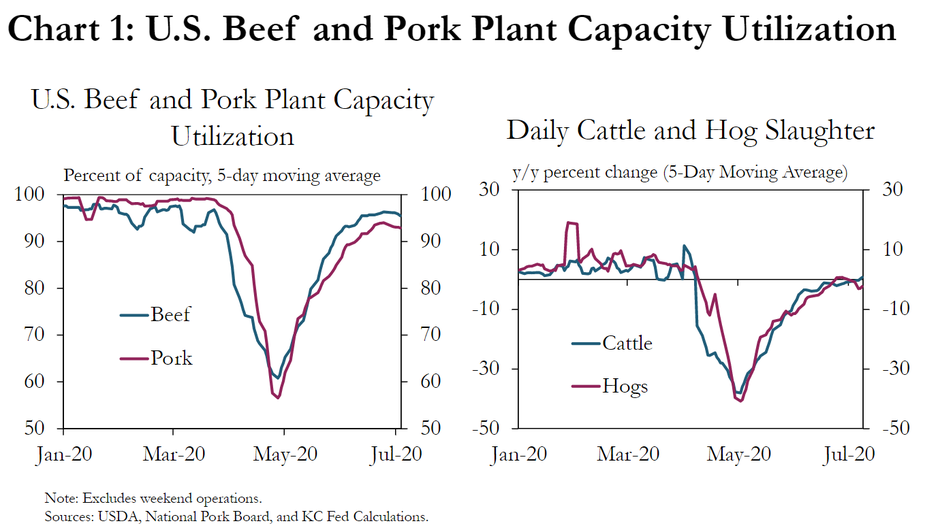

Closures and slowdowns led to sharp reductions in operating capacity at beef and pork plants and a significant decline in meat production. As plants were idled or limited operations, daily capacity at U.S. cattle and hog facilities declined as much as 45% (Chart 1, left panel). Reduced capacity at meatpacking plants led to notable reductions in cattle and hog slaughter compared with previous years. Meat production began to decline in early April, and by mid-May, was 40% below 2019 levels (Chart 1, right panel). Even as plants reopened, modified operations and revised processes related to COVID-19 put some constraints on production.

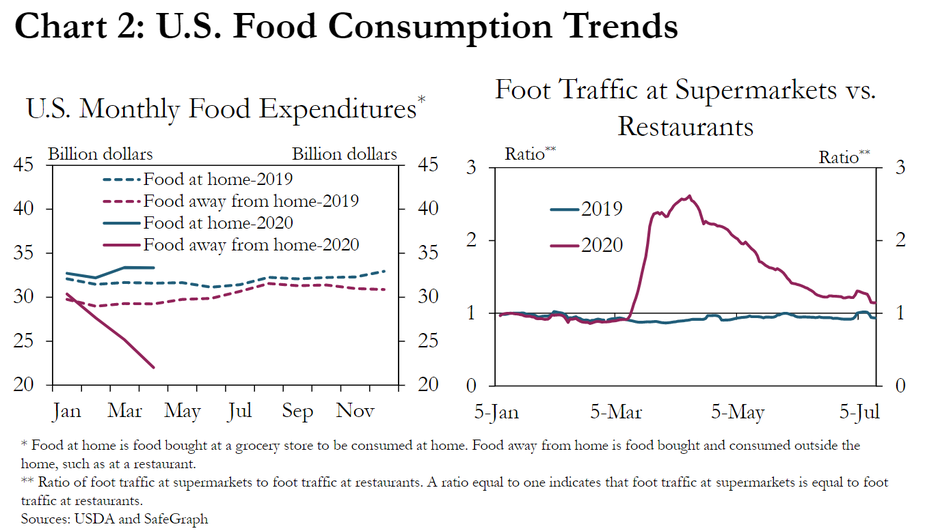

Alongside disruptions in meat production, rapid shifts in consumer demand shocked supply chains following the emergence of COVID-19. Household expenditures on food at grocery stores to be consumed at home typically are almost equal with expenditures on food consumed outside the home (for example, at restaurants). Following the emergence of COVID-19 in the United States, however, expenditures on food away from home declined sharply, and expenditures on food at home increased (Chart 2, left panel). In addition, starting in March, foot traffic at supermarkets increased, while activity at restaurants declined sharply (Chart 2, right panel). In fact, foot traffic at supermarkets was roughly double that of restaurants through the first week of May.

Implications for U.S. Livestock and Meat Sectors

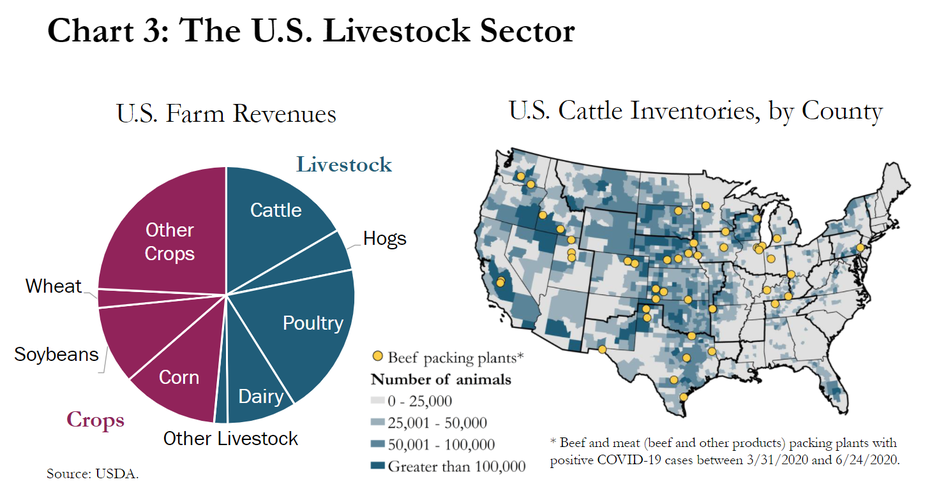

Developments in the supply chain are important to the agricultural sector, in part, because the livestock sector accounts for a large portion of the U.S. farm economy. The livestock industry accounts for more than 50% of total farm revenues in the Unites States, and cattle and hogs make up almost half of all livestock revenues (Chart 3, left panel). Moreover, some regions of the United States are particularly concentrated in livestock and meat production. For example, the Midwest and Great Plains account for 65% of U.S. cattle production (Chart 3, right panel). Meatpacking plants generally are in areas where livestock production is more prevalent. Therefore, although developments in the meat supply chain are a national concern, the effects may be greater in areas that produce higher quantities of livestock and meat.

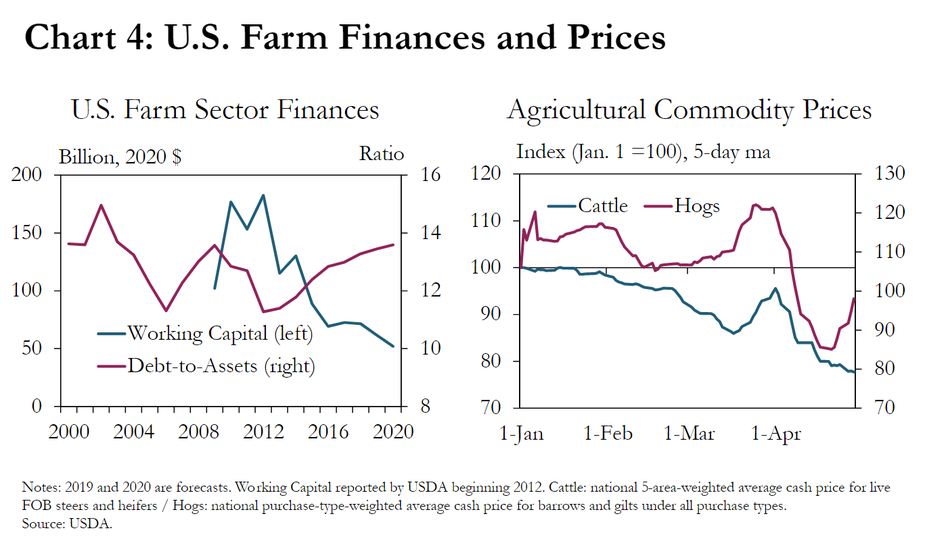

The agricultural economy had been in a prolonged downturn prior to the pandemic, intensifying concerns of how COVID-19 and disruptions in the meat production could affect farm finances. In 2020, working capital on U.S. farms was forecasted to decline 16% from the previous year, and if realized, would be 72% less than in 2012 (Chart 4, left panel). Although farm solvency ratios have increased only modestly, liquidity has declined more considerably since 2012, highlighting weakening financial conditions among agricultural producers. Amid disruptions related to COVID-19, prices for cattle began to decline in February and, by the end of April, had declined more than 20% (Chart 4, right panel). Prices for hogs were slightly stronger in February and March but also declined sharply in April.

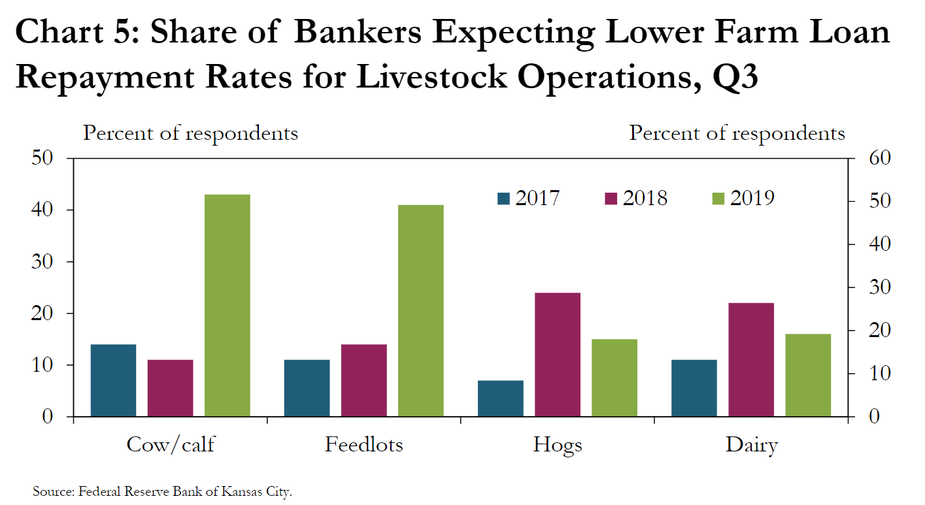

Greater financial difficulties for livestock producers could add to stress in agricultural lending portfolios that already had increased before the pandemic. In the third quarter of each year, the Federal Reserve Bank of Kansas City collects information on expected changes in loan repayment rates for specific types of farms, including livestock operations. Prior to the outbreak of COVID-19, agricultural lenders in the Tenth District already were more pessimistic about credit conditions in the livestock sector. For example, in the third quarter of 2019, about 40% of bankers expected lower repayment rates for cow/calf and feedlot operations (Chart 5). Almost 20% of agricultural lenders also expected lower loan repayment rates on hog and dairy operations. Moreover, according to information gathered at the onset of developments related to COVID-19, farm income and loan repayment rates declined at a faster pace than in recent quarters. As of the end of 2019 and the first quarter of 2020, results from the Kansas City Ag Credit Survey, which typically aligns with national developments, were more pessimistic about farm finances than in previous quarters. Conditions in the livestock sector continued to deteriorate in the second quarter alongside developments related to COVID-19, and the disruptions could put more pressure on farm finances and farm lending portfolios moving forward.

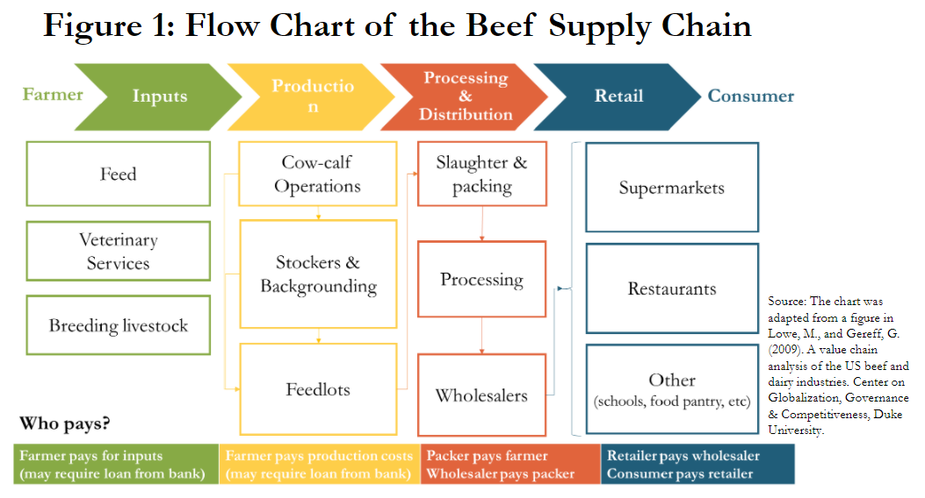

The U.S. meat supply chain spans from the livestock producer to the meat consumer, and disruptions in any one segment can have direct and indirect implications for other segments. In the beef supply chain, the production of meat begins on the farm, where the farmer breeds, raises and feeds cattle (Figure 1). Cow-calf operations raise and sell calves to backgrounding or feedlot operations, which feed cattle to maturity. Once finished, farmers sell cattle to packing plants. Packing plants slaughter live animals and package primal cuts of meat. Processing plants purchase primal cuts from packing plants, create value-added products, such as hamburger patties, sausage, and frozen meals, and distribute meat products to retail outlets directly or via a wholesaler. Consumers can purchase meat from a wide variety of retailers, but about 70% of food expenditures occur at grocery stores and restaurants, according to the USDA (2020).

Alongside closures at meatpacking plants, developments surrounding COVID-19 have contributed to substantial disruptions in other downstream segments of the food supply chain. Meat processing plants experienced disruptions directly if workers tested positive for the coronavirus or indirectly if the facility received product from a meatpacking plant that was closed. About 65% of processing plants reported outbreaks, and 20% closed temporarily. Further downstream, public health concerns and shelter-in-place guidelines also led to closures and reduced operations at schools, restaurants and farmers markets.

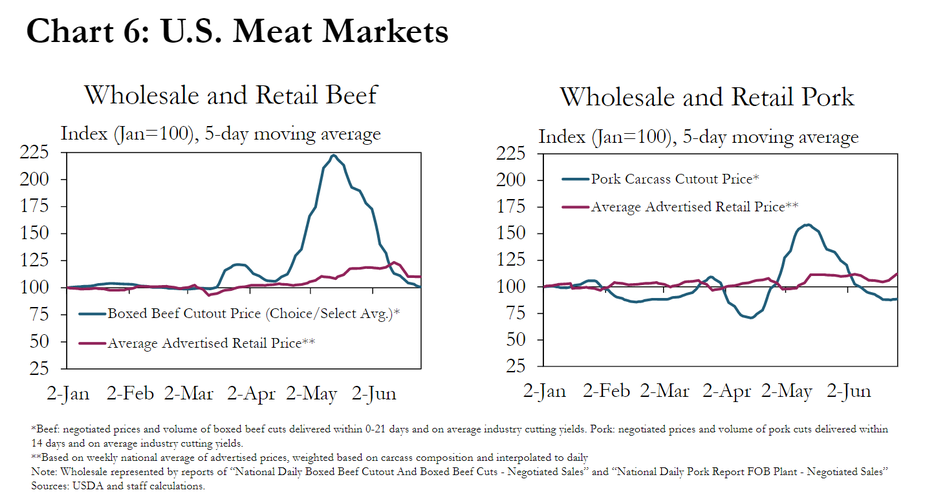

Meanwhile, wholesale prices increased dramatically, which led to higher retail prices for consumers. COVID-related shutdowns and slowdowns at meatpacking plants reduced supplies of meat in the supply chain. At the same time, supermarkets saw a significant spike in demand alongside concerns about food shortages and growing economic challenges associated with the pandemic. The combination of higher demand and lower supply of meat led to a dramatic increase in wholesale meat prices. In fact, wholesale beef prices rose 100% in May, while pork prices increased 50% (Chart 6). Retail meat prices were slower to react to disruptions but began to increase in May.

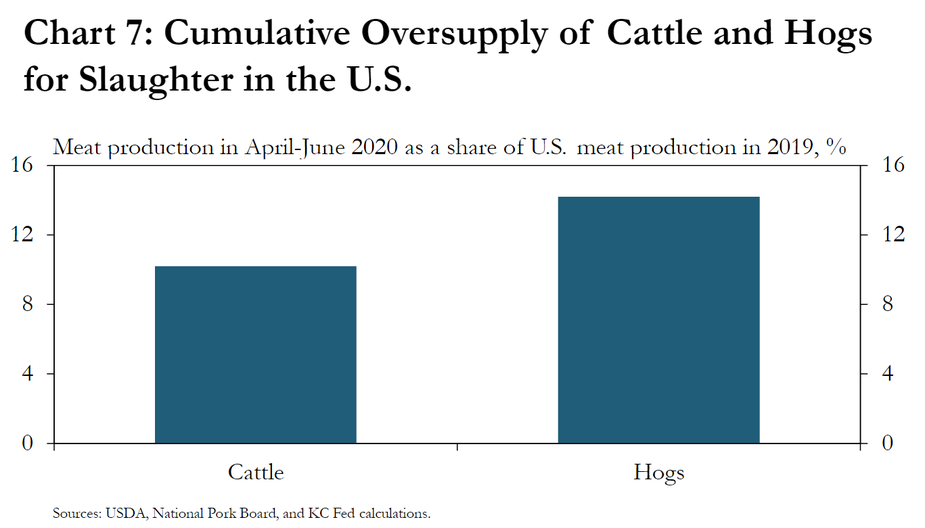

Disruptions at meatpacking plants created an oversupply of animals on farms, a situation that could take time to unwind. Normally, when an animal has reached maturity, a farmer sells it to a meatpacking plant. As packing plants closed or slowed their production, the demand for live animals was greatly reduced, leaving producers with limited options. Each day an animal remains on the farm or feedlot incurs additional costs to the producer. A farmer who cannot sell an animal to a packing plant typically finds an alternative market for the animal, bears the costs of retaining the animal on the farm or, as a possible last resort, may euthanize the animal. Based on reduced capacity at meatpacking plants, the cumulative oversupply associated with disruptions in the supply chain may have been about 500,000 head of cattle and about 3 million hogs through the end of June (Chart 7). Some of the backlogs created by lower capacity during normal operations were offset by increased slaughter activity on Saturdays, helping to reduce oversupplies of livestock on farms.

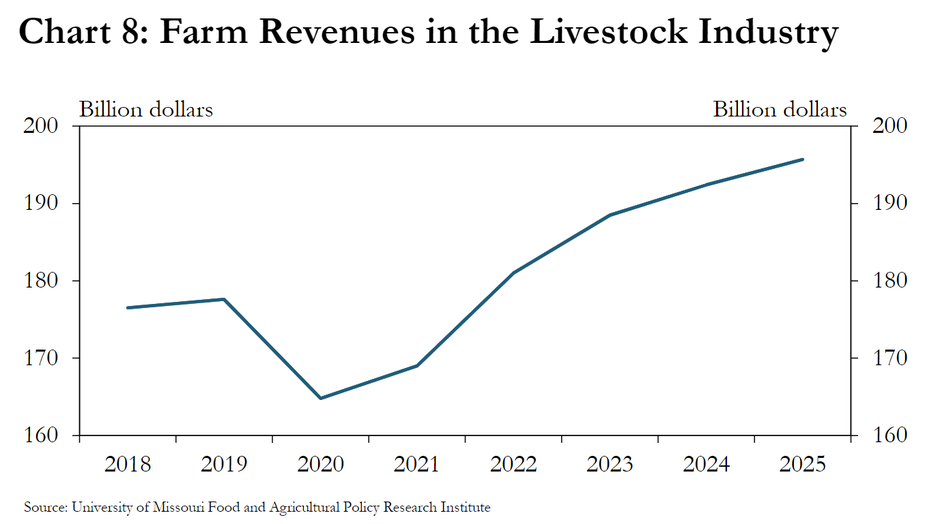

Reduced demand for livestock has weighed on the outlook for farm finances in 2020. For example, reduced capacity at meatpacking plants caused a surplus of animals on farms and forced some farms to euthanize animals. A euthanized animal is a loss to the producer, both in unearned revenues and direct costs associated with the euthanasia. Government payments appear likely to offset revenue losses somewhat, but depopulation is still a financial strain for livestock producers. For cattle, prices began falling in February and have yet to recover to pre-COVID levels. Prices for hogs increased somewhat in May but again declined sharply in June. In addition, quantities of cattle and hogs sold were likely lower than a year ago due to reduced capacity at packing plants, resulting in lower revenues in the livestock industry. University of Missouri Food and Agricultural Policy and Research Institute forecasts in June indicated livestock revenues could decline 8% in 2020, due, in large part, to slowdowns in foodservice and disruptions at meatpacking plants during COVID-19 (Chart 8).

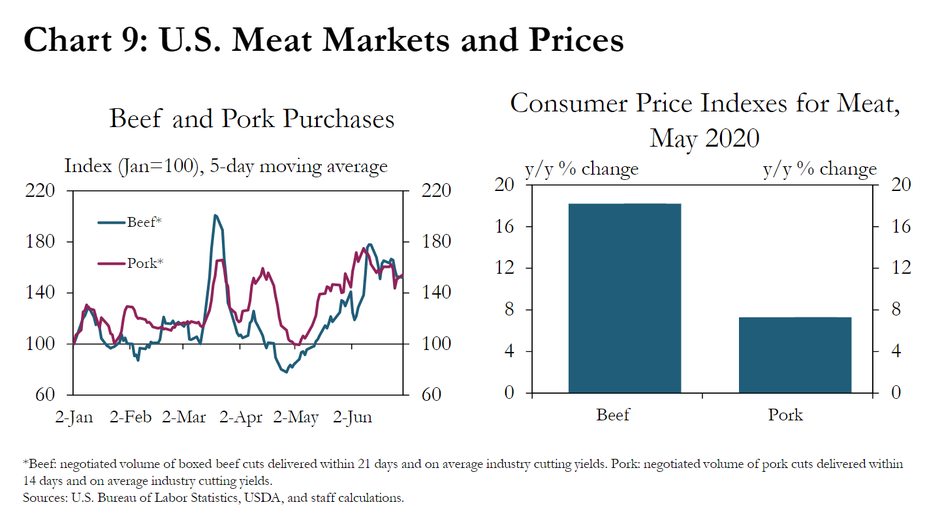

In the meantime, higher demand for meat at grocery stores in the midst of reduced supplies placed additional inflationary pressure on retail prices. In late April and early May, purchases of wholesale meat products declined alongside reduced meat production (Chart 9, left panel). However, purchases of meat began to rebound in mid-May. The uptick in purchases while packing plants were operating at reduced capacity drove historically large increases in prices for meat products (Chart 9, right panel). In May, beef prices were 18% higher than a year ago, and pork prices were 7% higher than in 2019. Also, beef prices increased 11% from April to May, the largest monthly increase on record, according to the Bureau of Labor Statistics.

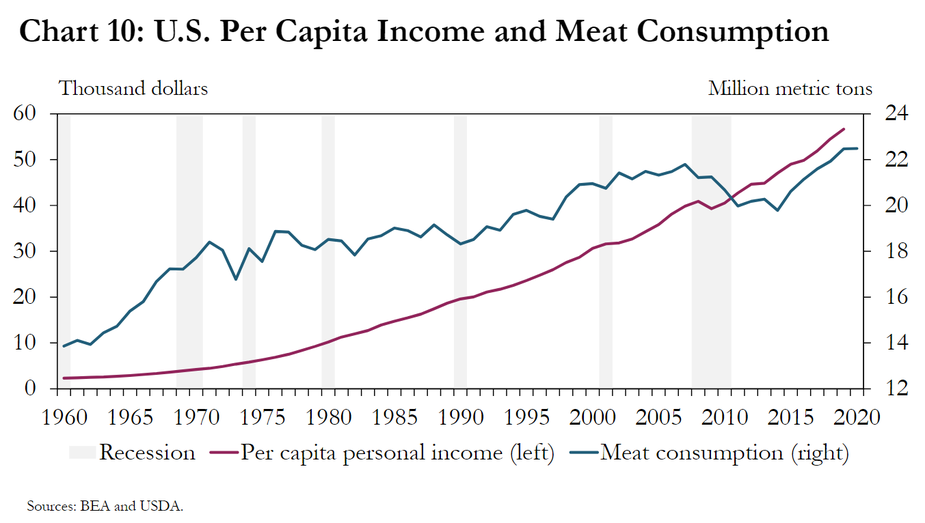

As retail prices increase during an economic downturn, some consumers may buy less meat, which could create more persistent challenges for the livestock industry. First, the U.S. meat industry is highly dependent on domestic consumption. Domestic meat consumption tends to decline during economic downturns (Chart 10). For example, since 1960, U.S. meat consumption has increased alongside increases in household incomes. However, meat consumption steadily declined during the last recession that began in late 2007 and ended in mid-2009. In fact, annual meat consumption did not surpass pre-recession levels until 2018. Second, a temporary increase in prices for meat could encourage consumers to try alternative protein sources. If some consumers decide that they either prefer non-meat alternatives or wish to reduce meat consumption by regularly consuming more plant-based proteins, demand for meat could decline. Reduced meat consumption may result in lower prices for upstream segments of the supply chain. However, the effects of lower demand on livestock prices could be offset somewhat if challenges in April and May lead to fewer animals in the supply chain.

Higher prices may also limit the ability of some households to purchase meat. Food expenditures make up a larger share of income for low-income households even though these households spend less on food each year. For example, in 2018, households with the lowest levels of income spent about $4,000 on food, representing 35% of their income, on average (Chart 11). Conversely, households in the highest income group spent about 8% of their income on food, totaling about $13,000 a year. Because the share of income spent on food is high for lower-income households, these households may be less able to increase spending on food when prices rise. Furthermore, lower-income households have less money to spend on food, and therefore, tend to choose lower-priced options. For example, lower-income consumers are more likely to choose lower-priced products such as ground beef, chicken wings and rice and beans than are higher-income consumers (Lusk and Tonsor 2015). In addition, a larger share of lower-income consumers may choose not to purchase meat compared with middle- and higher-income consumers. In fact, Lusk and Tonsor (2015) found that, in the midst of rising meat prices and the previous recession, lower-income segments likely were representing a declining share of total consumption for meat products. In the current crisis, higher retail prices for meat again could put more persistent pressure on finances for some families and compel lower-income households to seek alternative or cheaper protein sources.

Conclusion

Outbreaks of COVID-19 in the U.S. meat industry caused a temporary slowdown in meat production and widespread uncertainty about markets for food and livestock in the United States. Kinks in the supply chain resulted in higher meat prices for consumers, even as producers faced lower livestock prices. Although hog prices rebounded and were higher than at the beginning of the year in May, farm revenues could still decline in 2020 due to disruptions at meat packing plants, which forced some producers to depopulate herds. Moving forward, modified operations and revised processes related to COVID-19 at packing plants may continue to put constraints on meat production. In addition, higher retail prices, particularly in the midst of an economic downturn, could temporarily reduce aggregate meat consumption, further weighing on the outlook for producers and consumers of meat.

References:

Lusk, Jayson L., and Glynn T. Tonsor. 2016. “How meat demand elasticities vary with price, income, and product category.” Applied Economic Perspectives and Policy. 38(4): 673-711. Available at: External Linkhttps://doi.org/10.1093/aepp/ppv050.

United States Department of Agriculture (USDA). 2020. “Food Expenditure Series.” Economic Research Service. Available at External Linkhttps://www.ers.usda.gov/data-products/food-expenditure-series/.

The views expressed are those of the authors and do not necessarily reflect the positions of the Federal Reserve Bank of Kansas City or the Federal Reserve System.

Author