A slow but steady rise in financial stress in the farm sector continued in the third quarter of 2016 as income in the sector remained low. Persistent weakness in both the crop and livestock sectors has caused producers to expend more working capital to meet short-term financial obligations. An ongoing decline in farmland values and cash rental rates has accelerated slightly under prolonged pressure from falling farm income. Alongside increased risk in the Tenth District’s agricultural economy, bankers reported an increase in collateral requirements for agricultural loans and declines in available funds and farm loan repayment rates.

Farm Income

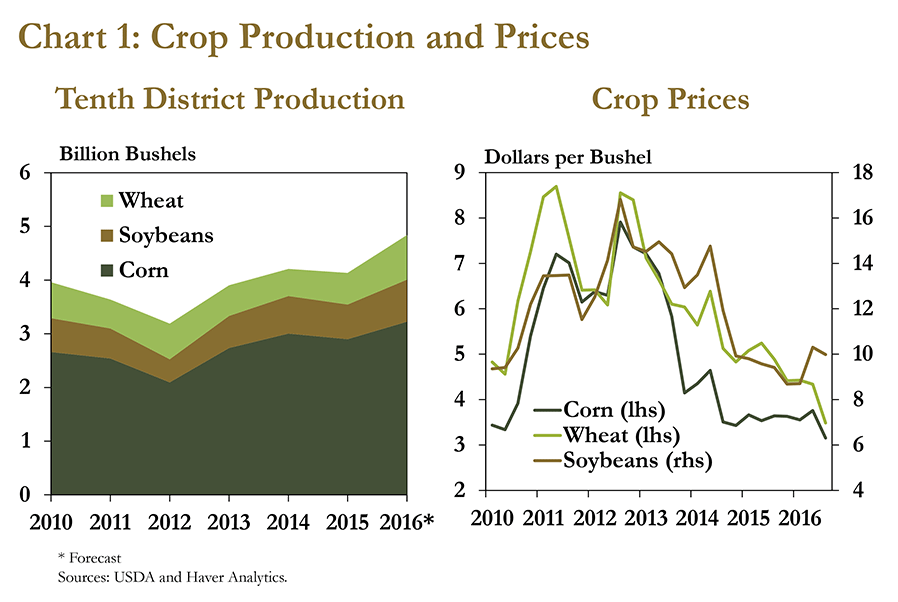

Low commodity prices continued to weigh on farm sector profits in the third quarter. As of the end of September, cattle and hog prices were 21 percent and 14 percent less, respectively, than a year ago, and profit margins remained poor. Corn and wheat prices also were less than a year ago alongside expectations for 2016 of strong production throughout the District (Chart 1). Soybean prices advanced due to strong export demand during the late summer months, and some producers may profit from extremely strong yields this fall. However, profit margins in the quarter generally remained weak throughout the agricultural sector.

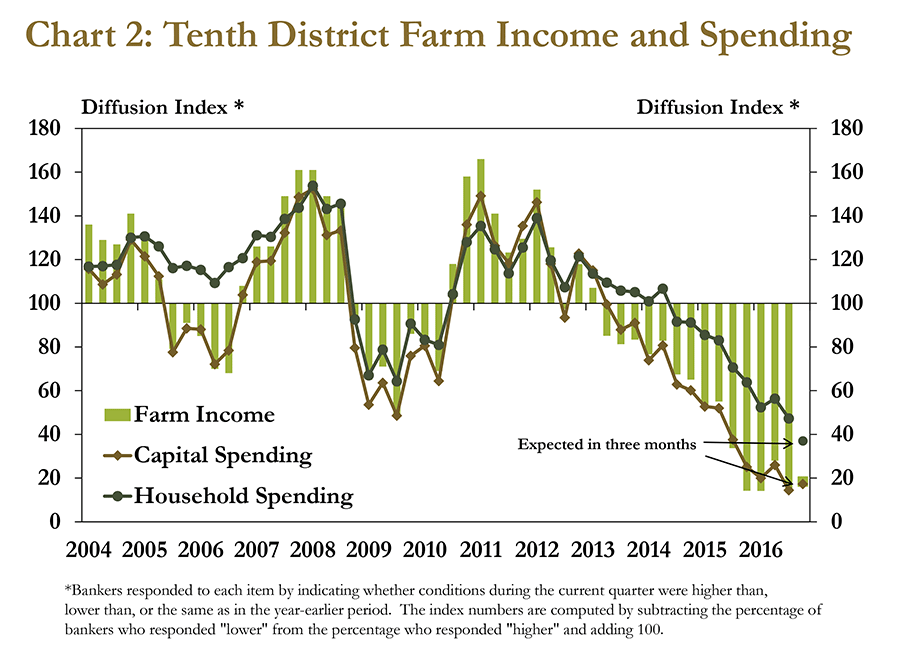

Amid tightening profit margins, respondents to the Tenth District Survey of Agricultural Credit Conditions reported additional declines in farm income. In fact, more than 87 percent of bankers reported a decline in farm income in the third quarter from the same quarter a year ago (Chart 2). Respondents also noted that capital and household spending continued to decrease alongside falling farm income.

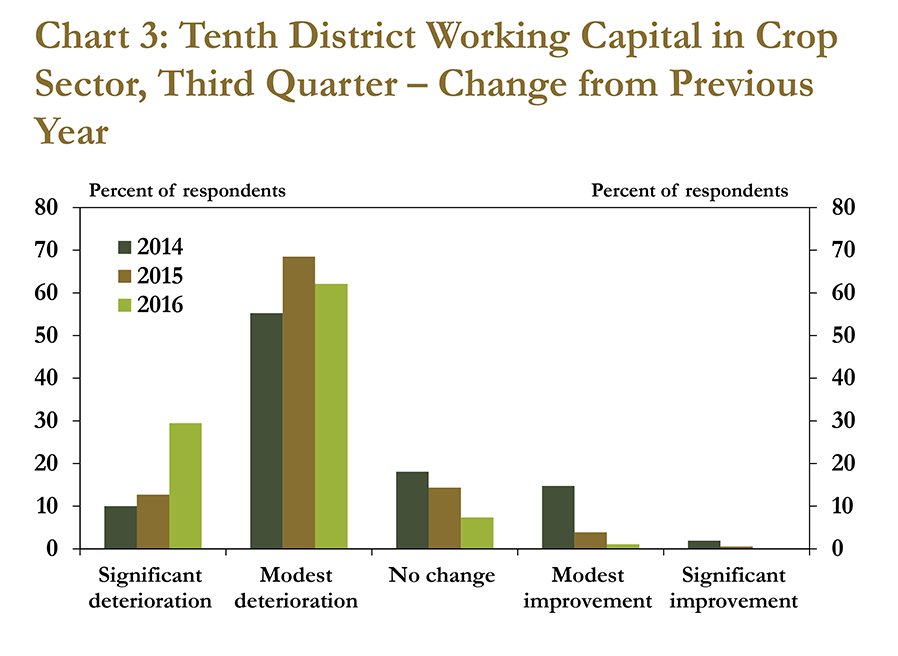

The decline in farm income in the District has taken a bigger bite out of farm borrowers’ working capital. More than 90 percent of bankers reported some deterioration in the level of working capital among borrowers in the crop sector, versus just 1 percent of bankers that reported an improvement from a year ago (Chart 3). Moreover, nearly 30 percent of bankers reported a significant deterioration in working capital from a year ago, about twice the number at the same time in 2015. Because working capital is an important buffer against potential financial difficulties, additional deterioration could result in some borrowers becoming more highly leveraged as they continue to try to support operations through short-term financing.

Farmland Values and Cash Rents

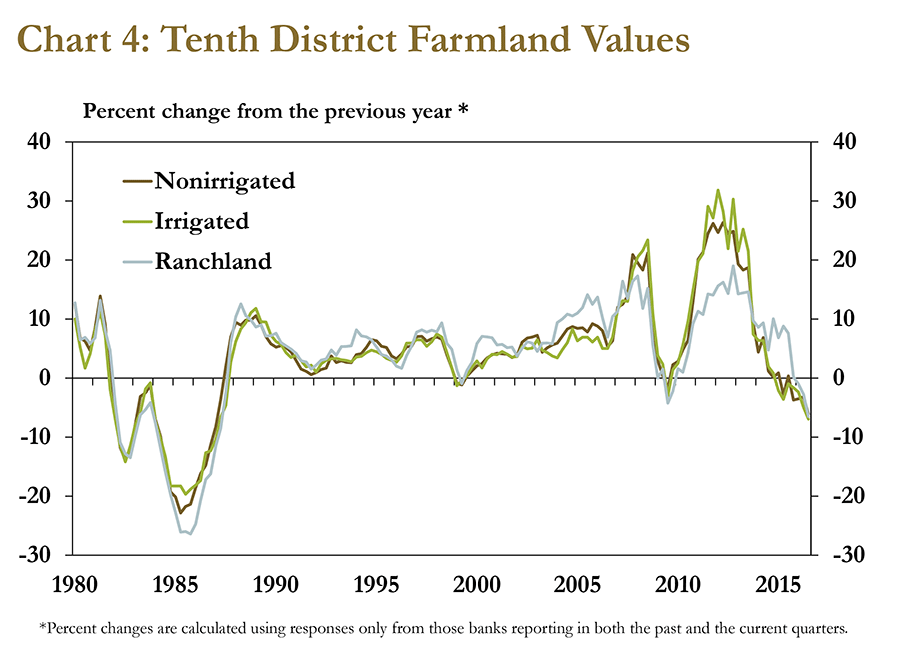

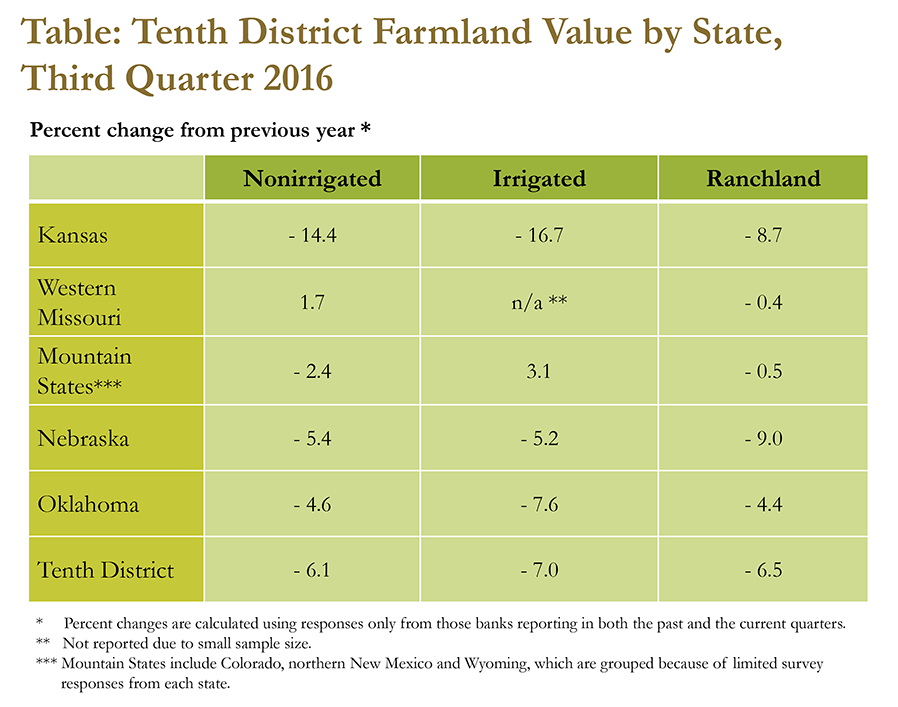

Ongoing weakness in the District’s farm economy in the quarter caused a more significant decline in farmland values. The value of each type of farmland—nonirrigated cropland, irrigated cropland and ranchland—fell more than 6 percent from a year ago (Chart 4). The decrease in the third quarter was the sharpest year-over-year reduction in the value of each type of farmland throughout the District since the mid-1980s. However, the declines have remained relatively modest. For example, the survey indicated irrigated cropland that might have been valued at $7,000 per acre in 2014, on average, would have been about $6,450 in the third quarter of 2016.

Evidence of steepening declines in farmland values was seen throughout the District. Except for western Missouri, the value of nonirrigated cropland decreased in all District states (Table). Similarly, the value of irrigated cropland fell in all but the Mountain States, and cropland values declined at a significantly sharper pace in Kansas. In addition, ranchland values decreased in all states in the District for only the second time since 2002.

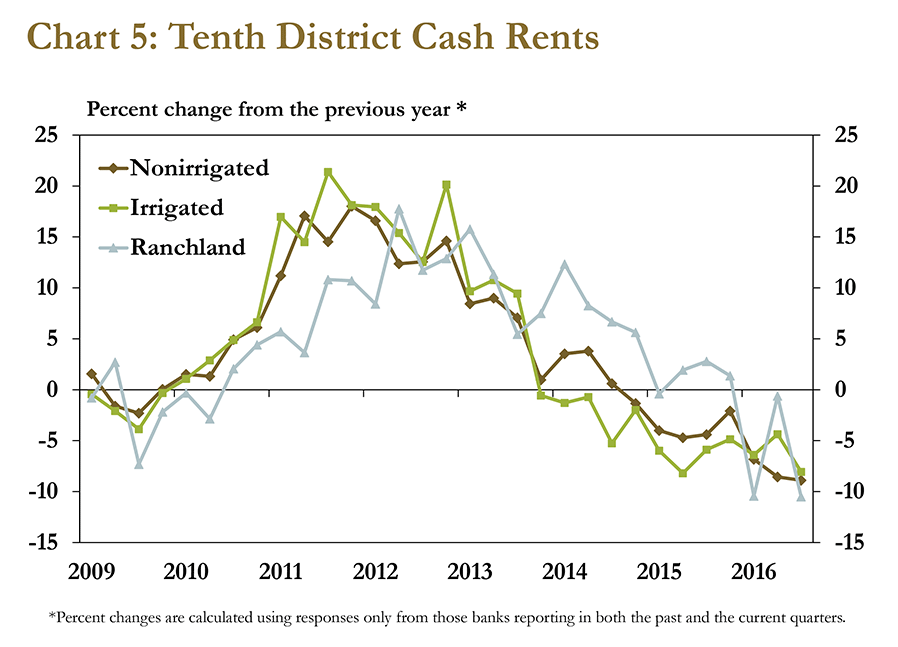

Similar to farmland values, cash rental rates for both cropland and ranchland decreased in the third quarter, following a recent trend of sharper declines (Chart 5). In the third quarter, cash rent for both irrigated and nonirrigated cropland was down nearly 10 percent from a year ago. The reduction in cash rents, the result of persistently weak profit margins for farm operations throughout the District, may represent a significant reduction in costs in the coming months at a time when revenue has remained relatively weak.

Credit Conditions

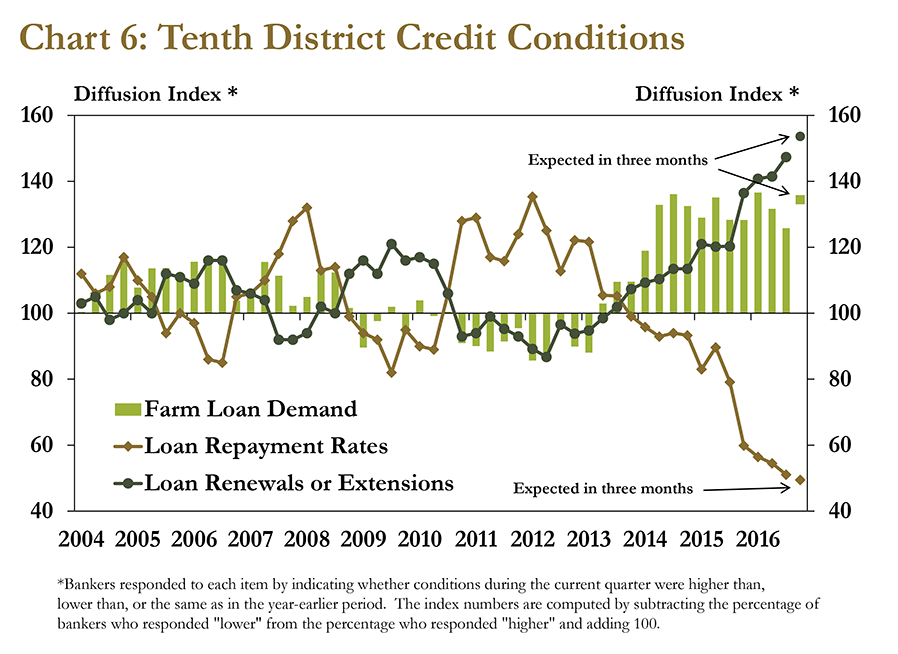

Reduced farm income has continued to weaken credit conditions in the agricultural sector in the District. Demand for farm loans, as well as renewals and extensions, increased in the third quarter alongside additional declines in repayment rates for farm loans (Chart 6). The third quarter started a fourth year of increasing demand for farm loans and renewals and extensions, following a period of relatively subdued demand for farm loans and strong repayment rates. Loans used to pay operating expenses have remained a primary driver of increased demand for financing. In 2016, operating loans have comprised nearly 60 percent of the volume of all non-real estate loans at commercial banks nationally, and have supported a steady increase in total outstanding farm debt.

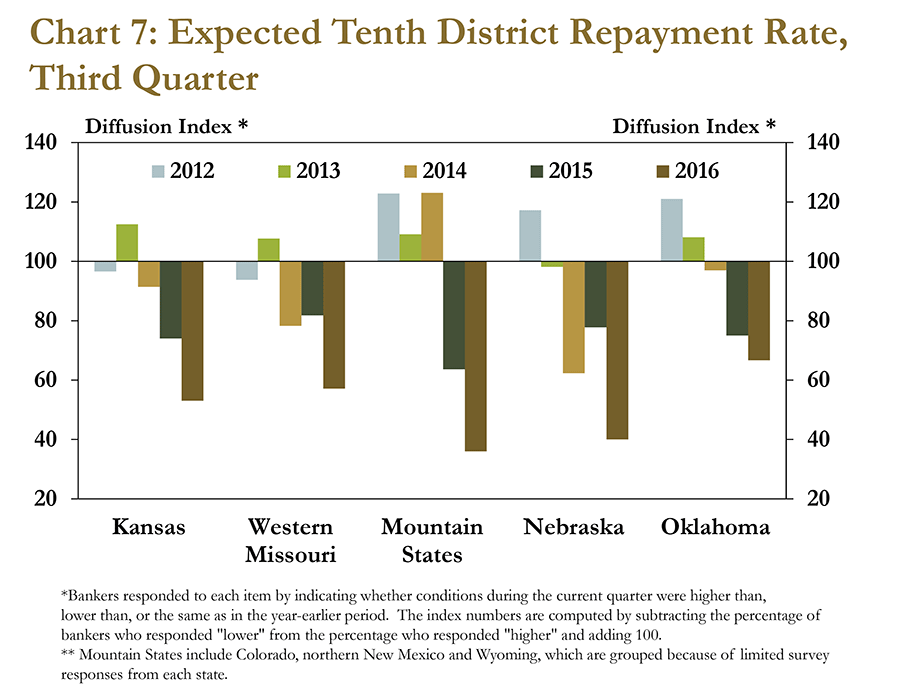

Decreasing repayment rates for farm loans pointed to rising financial stress for farm borrowers. More than half of bankers surveyed in the third quarter reported loan repayments had decreased, while less than 2 percent reported an improvement. As evidence of relatively widespread deterioration in agricultural credit conditions, no state in the District had more than 4 percent of bankers report stronger repayment rates, and none of the respondents from Kansas or Missouri reported an improvement. Moreover, bankers in each District state indicated they expect repayment rates to decline again in the fourth quarter (Chart 7).

The widespread decline in the rate at which farm loans are being repaid likely has been due to intensifying weakness across all segments of the Tenth District farm economy. For instance, when asked about near-term repayment rates by industry, bankers indicated they expect additional declines in loan repayment rates for each major industry in the Tenth District agricultural economy (Chart 8). Some segments of the livestock sector that had been relatively strong as recently as 2014 have weakened significantly over the past year.

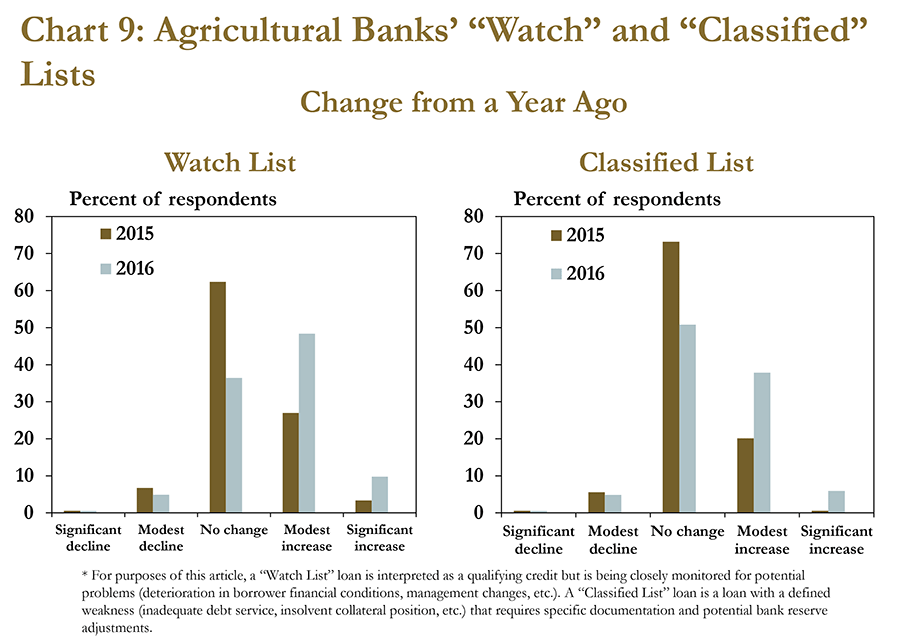

Weakening credit conditions have caused bankers to add more farm borrowers to their watch and classified lists. In the third quarter, bankers reporting an increase from the previous year in the number of farm borrowers on their watch list grew to 58 percent from 30 percent in 2015 (Chart 9). Likewise, 44 percent recorded some increase of farm borrowers on the classified list, up from 21 percent in 2015. Bankers also indicated they expect additional increases to the watch and classified lists. In fact, nearly 60 percent of bankers indicated they anticipate the volume of loans on their watch list will increase in the next three months.

Agricultural Lending

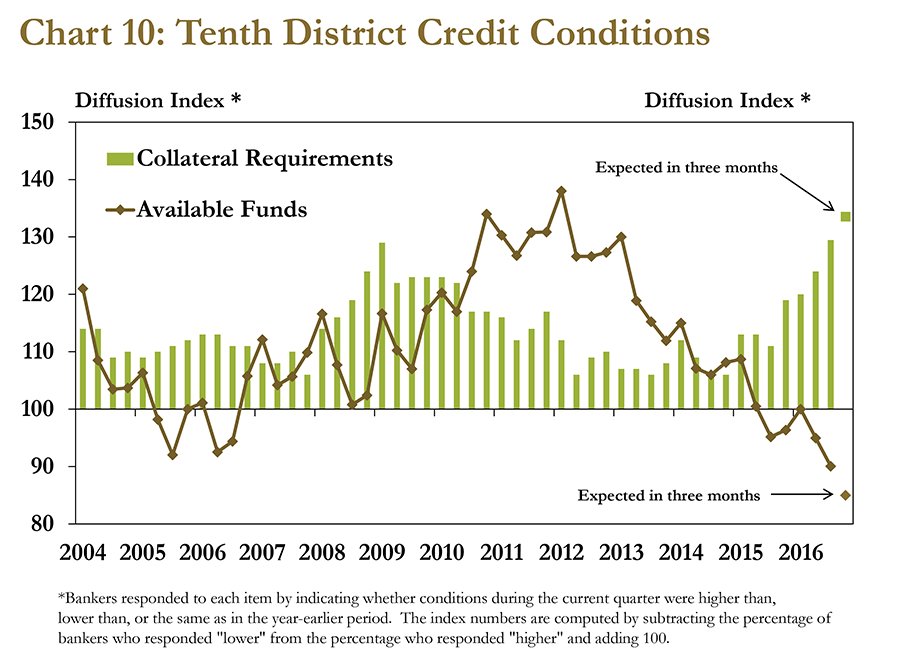

As the risks in the farm sector have grown, some banks have made adjustments to lending terms for their agricultural portfolio. For example, bankers reported a notable increase in the amount of collateral required to obtain farm loans (Chart 10). While collateral requirements have increased steadily over the past few years, the rate of increase has been steeper in recent quarters. In fact, the share of bankers that indicated collateral requirements had increased in the third quarter was the highest in 25 years, according to the survey. In many cases, agricultural lenders increasingly have relied on farm borrowers’ real estate as a source of collateral for other agricultural loans.

In addition to increased collateral requirements, bankers also reported fewer funds available for financing than a year ago. The decline in available funds, which has persisted for nearly two years, was preceded by nearly nine consecutive years in which bankers reported consistent increases in financing availability, a time when the District’s agricultural economy was extremely strong. The recent period of reduced farm income and increased demand for farm loans, however, likely has cut into funds available for financing.

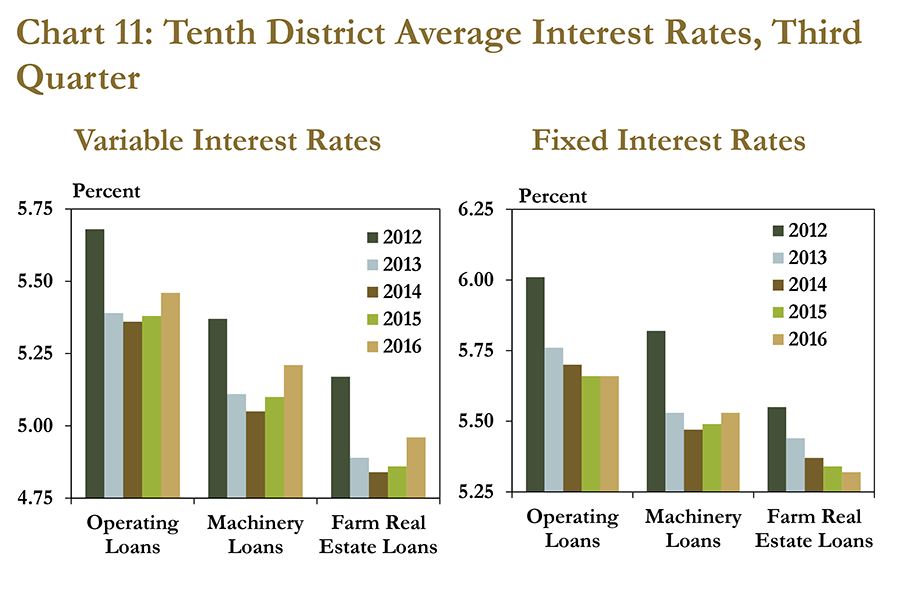

Bankers also raised interest rates on farm loans, particularly for variable rate loans. Although variable interest rates for operating, machinery and farm real estate loans generally remained low, each of these rates increased in the third quarter (Chart 11). Variable interest rates on farm operating loans, which typically comprise the largest share of farm lending at agricultural banks in the District, increased to an average of 5.4 percent. Fixed interest rates for machinery loans also increased in the third quarter, whereas fixed interest rates for operating loans remained steady; interest rates for farm real estate loans continued to edge lower.

Conclusion

The pressure that has been building in the Tenth District’s farm economy continued at a modest pace in third quarter. Agricultural credit conditions and farmland values deteriorated more rapidly under prolonged pressure from low commodity prices and tight profits margins. Although defaults on farm loans remain low, bankers indicated they expect farm income, farmland values and repayment rates to dip further in the coming months. If these expectations hold, the slow but steady increase in farm financial stress appears likely to continue.

Disclaimer

The views expressed in this article are those of the authors and do not necessarily reflect the views of the Federal Reserve Bank of Kansas City or the Federal Reserve System.

The views expressed are those of the authors and do not necessarily reflect the positions of the Federal Reserve Bank of Kansas City or the Federal Reserve System.

Author