Farmland values in the Federal Reserve’s Tenth District held steady in the fourth quarter of 2018 despite risks to ongoing stability. While demand for farmland remained relatively strong across the District, weaknesses in the crop sector continued to dampen the overall agricultural economy. Risks to the outlook for farmland values in the quarter included slightly higher interest rates and an uptick in the pace of farmland sales in states with higher concentrations of crop production. In addition, continued deterioration in farm finances and credit conditions could put further pressure on values for farm real estate. Looking into 2019, bankers’ expectations for farmland values were slightly weaker than a year ago.

Data

Credit Conditions | Fixed Interest Rates | Variable Interest Rates | Land Values

Farmland Values

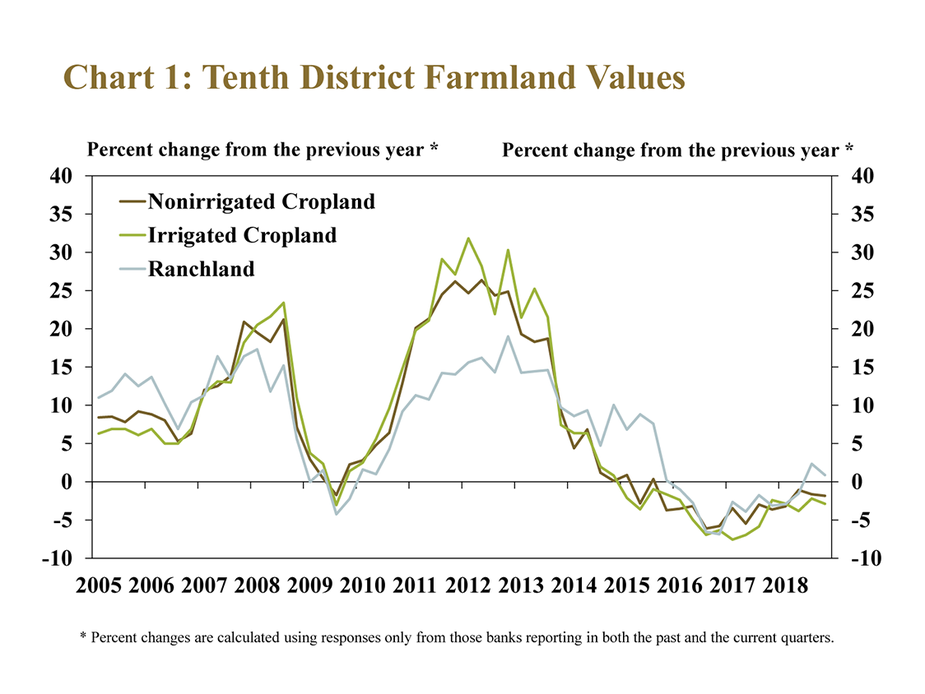

Farmland values remained stable in the fourth quarter, according to the Tenth District Survey of Agricultural Credit Conditions. Declines in the value of nonirrigated and irrigated cropland remained modest across the District, and declined only 3 percent from last year (Chart 1). On average, cropland values also declined at a slower pace in 2018 than in the previous two years. Ranchland values increased slightly for the second quarter in a row, the first consecutive increase in farmland values since 2015.

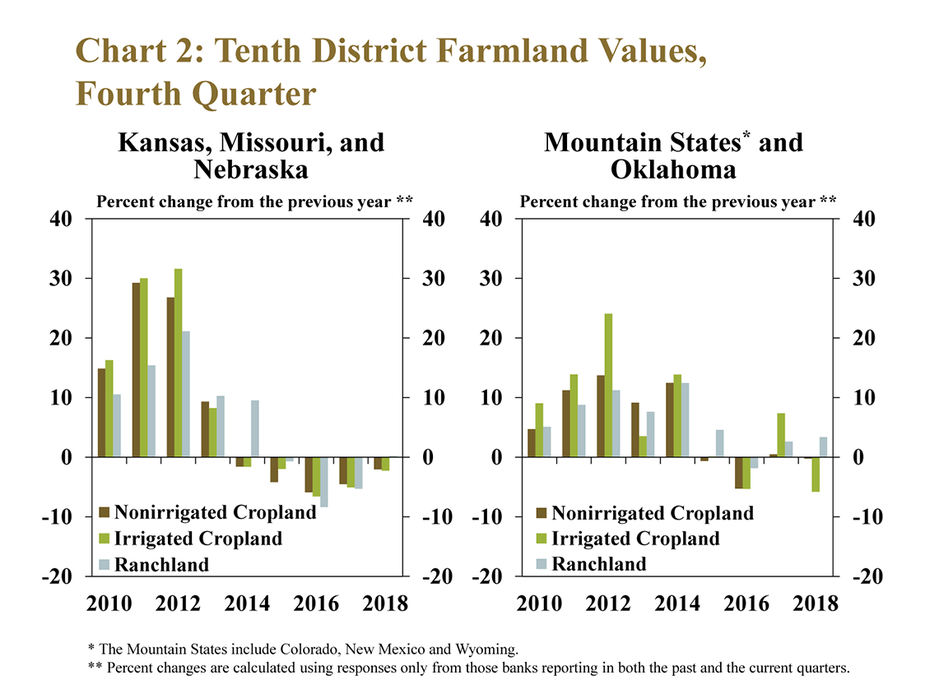

Farmland values were more stable in states more concentrated in livestock and energy production. Although irrigated cropland values declined at a faster pace in the Mountain States and Oklahoma, nonirrigated cropland was relatively unchanged while ranchland values increased more than 3 percent (Chart 2). Furthermore, most of the strength in ranchland values across the District was driven by developments in the Mountain States and Oklahoma, states with higher concentrations of cattle production. Bankers in these states also commented that farmland values have been supported by an uptick in activity in the energy sector.

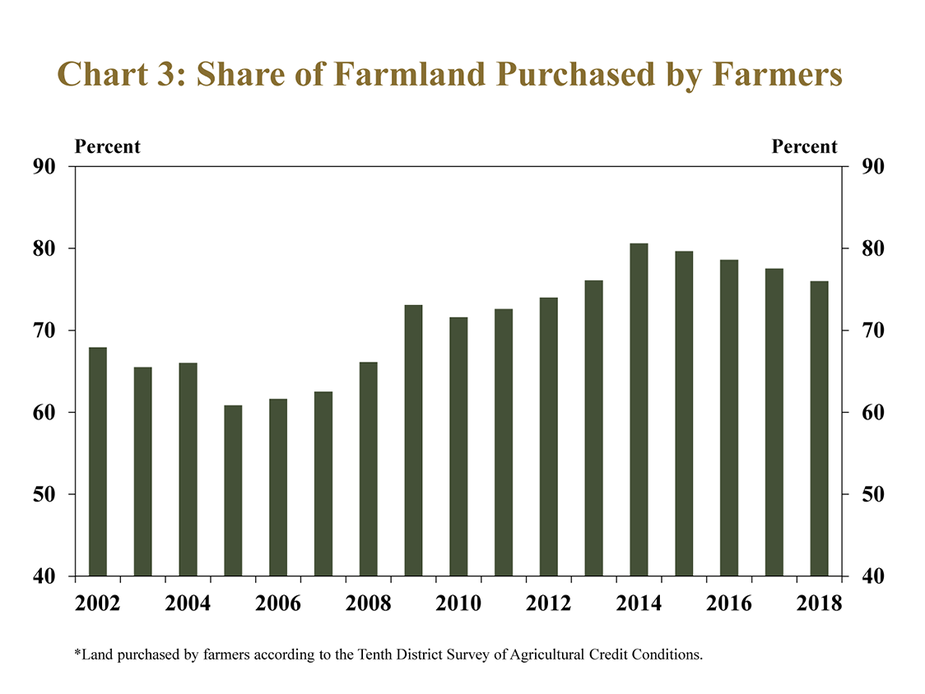

Demand for real estate remained strong in the farm sector, which could be supporting farmland values. Although the share of farmland purchased by farmers has trended lower since 2014, the decline has remained modest (Chart 3). In 2018, farmers remained the primary buyers of farmland and accounted for more than 75 percent of purchases.

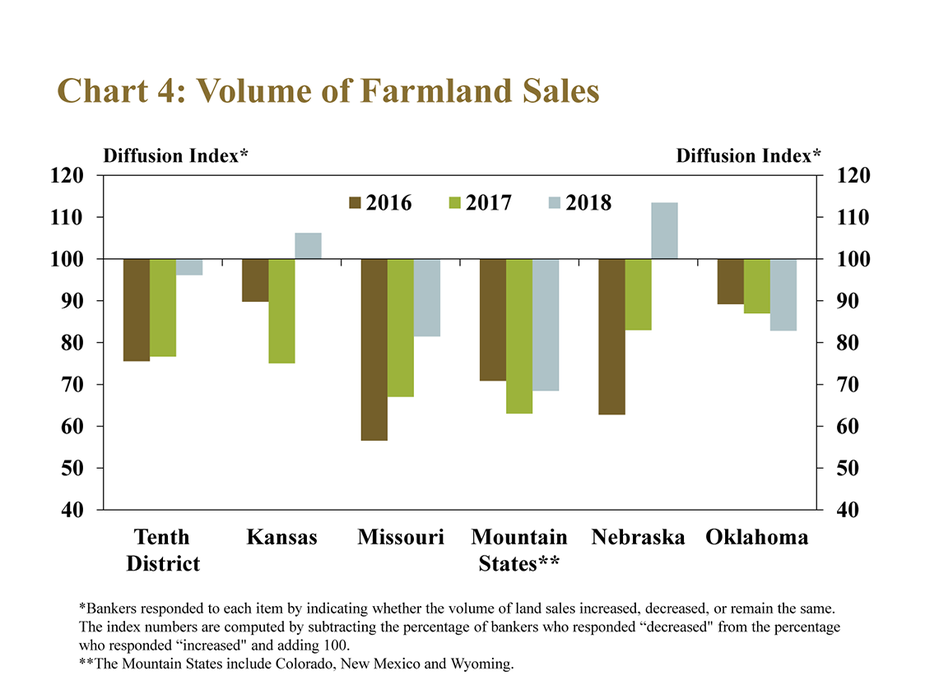

Despite strong demand, a higher volume of sales in parts of the District in the fourth quarter could be a key risk to the outlook for farmland values. Across the District, the pace of decline in farmland sales was slower in 2018 (Chart 4). The slower pace was driven by an increase in farmland sales in Kansas and Nebraska. During the current downturn in the agricultural economy over the past five years, the persistently low volume of land sales has contributed to the stability of farmland values. However, if the supply of farmland were to continue to increase in 2019, farmland values could be less stable.

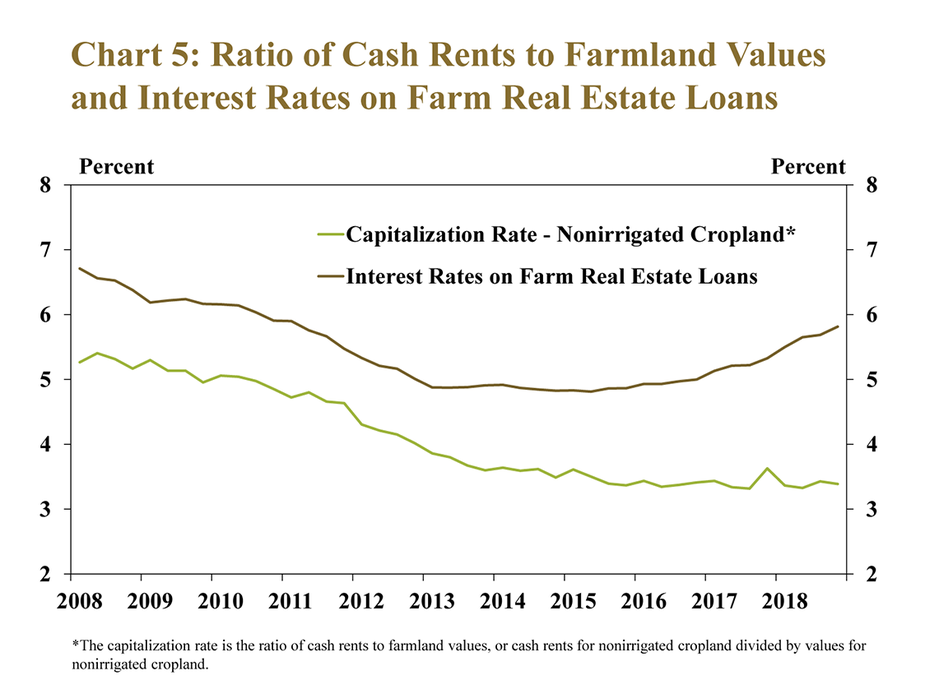

In addition, increases in interest rates in recent years also could weigh on farmland values. Higher interest rates have increased the financing costs of land purchases slightly and could signal higher returns on alternative investments. At the same time, stable farmland values and lower cash rents have led to lower capitalization rates (Chart 5). As interest rates have increased, they have diverged from capitalization rates on farm real estate, and this divergence intensified in 2018. As interest expenses on new land purchases have increased amid flat returns, demand for farmland, and hence farmland values, could decline.

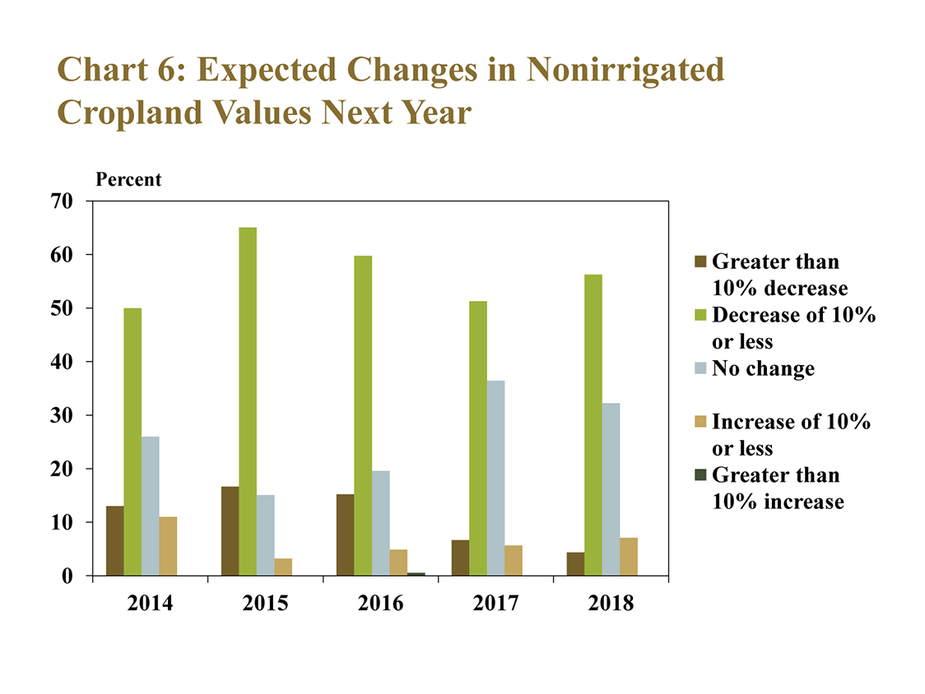

Alongside higher interest rates, expectations for farmland values continued to wane. Compared with last year, a larger share of bankers indicated in the fourth quarter that they expect modest declines in nonirrigated cropland values in 2019 (Chart 6). Although some bankers still expected farmland values to increase slightly in 2019, 61 percent of respondents expected farmland values to decline, while 32 percent expected values to remain unchanged.

Farm Income and Credit Conditions

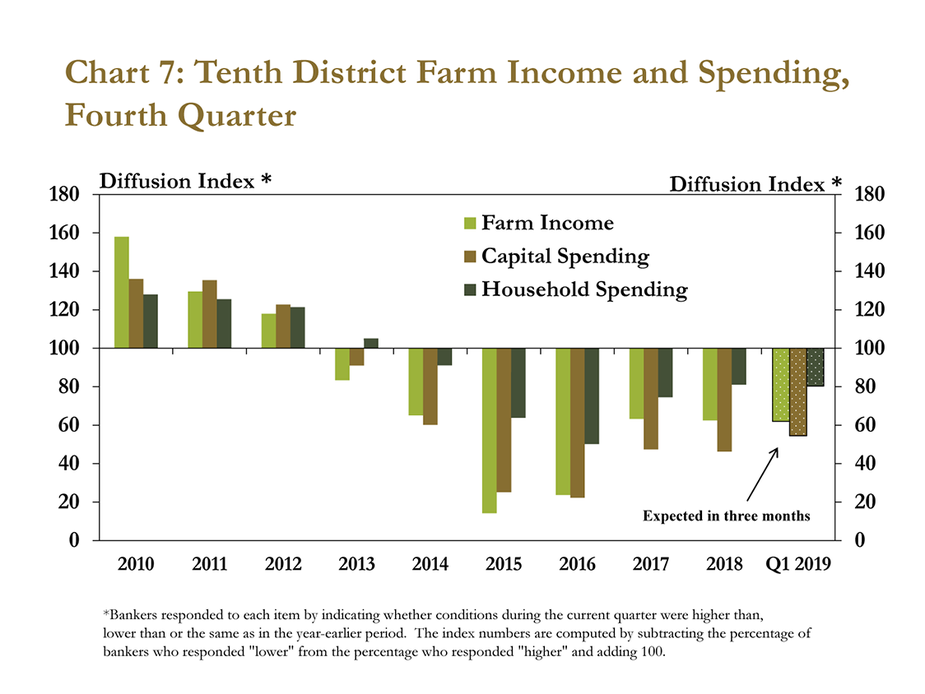

Amid persistent stress in the agricultural economy, farm income and borrower spending continued to decline. Farm income in the fourth quarter declined for the sixth consecutive year, according to respondents throughout the Tenth District (Chart 7). Bankers also indicated they expected farm income to remain weak in the first quarter of 2019. Similar to 2017, nearly 60 percent of respondents reported lower capital spending than a year ago. Although 30 percent of bankers indicated that household spending had decreased from a year ago, the majority continued to report no change.

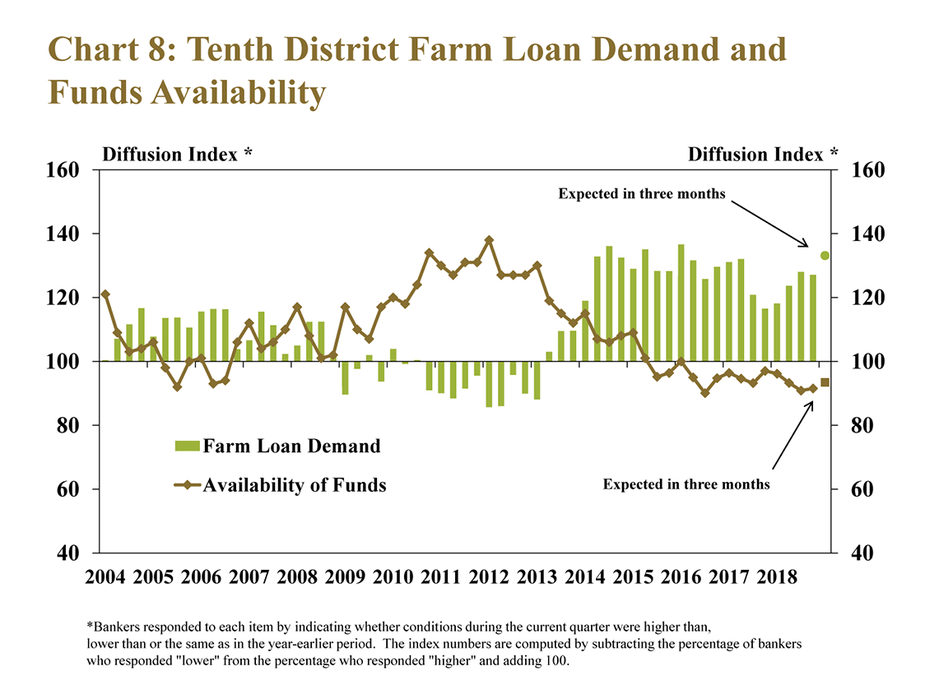

Alongside lower farm income, demand for farm loans also remained high. Nearly six years of strong farm loan demand has placed downward pressure on liquidity at agricultural banks (Chart 8). In fact, the percent of respondents reporting lower availability of funds than in the previous year increased to 15 percent from 9 percent in the fourth quarter of 2017. Bankers also expected high demand for farm loans and tight liquidity to continue.

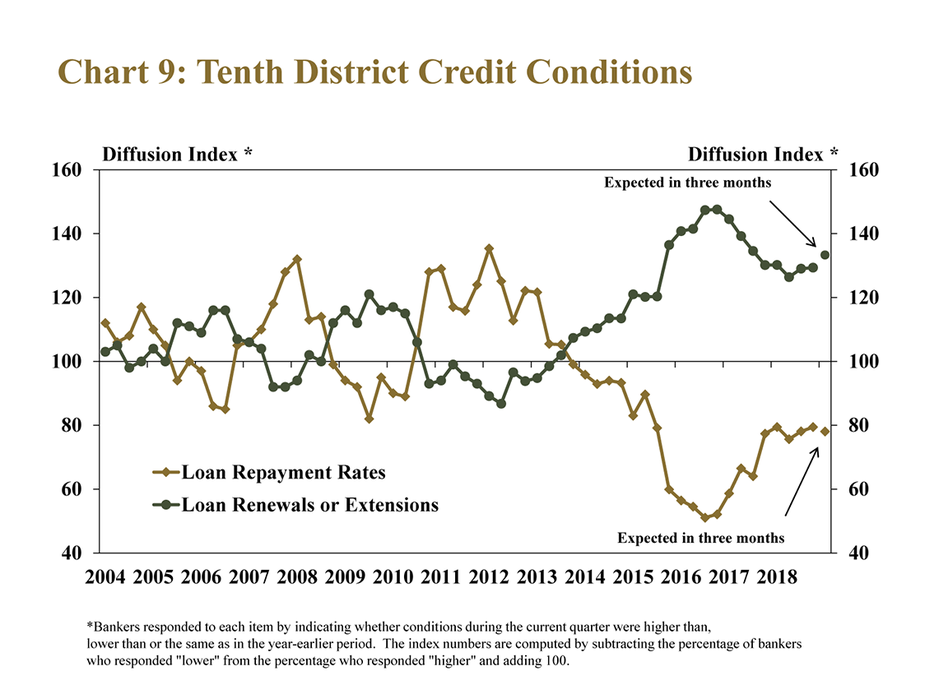

Demand for renewals and extensions also remained elevated, and the rate of repayment on agricultural loans was lower than a year ago. Respondents also expected both trends to continue (Chart 9). While still remaining weak, loan repayment rates appeared to stabilize somewhat through the end of 2018. Demand for renewals and extensions has followed a similar trend of stabilization but remained high and also continued to suggest signs of stress in farm lending.

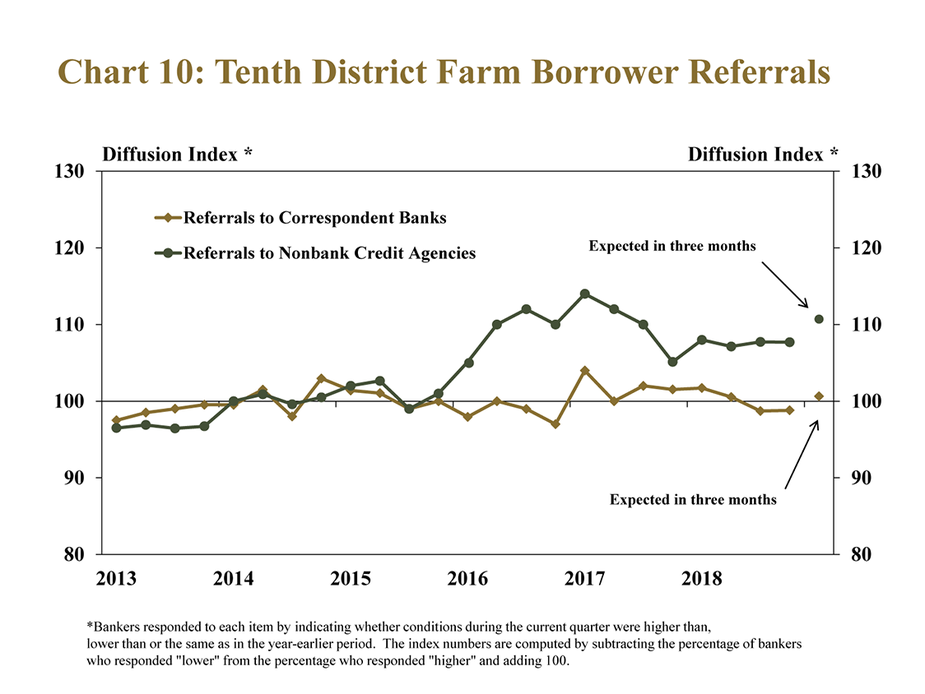

Pressure from deterioration in farm finances in recent years also has contributed to a slight increase in referrals of borrowers to other creditors. The pace of change in referrals to correspondent banks was relatively unchanged from a year ago while referrals to nonbank credit providers increased slightly (Chart 10). Although the change has been only modest, referrals to nonbank credit agencies increased at a faster pace in 2016, 2017 and 2018 compared with the prior three years.

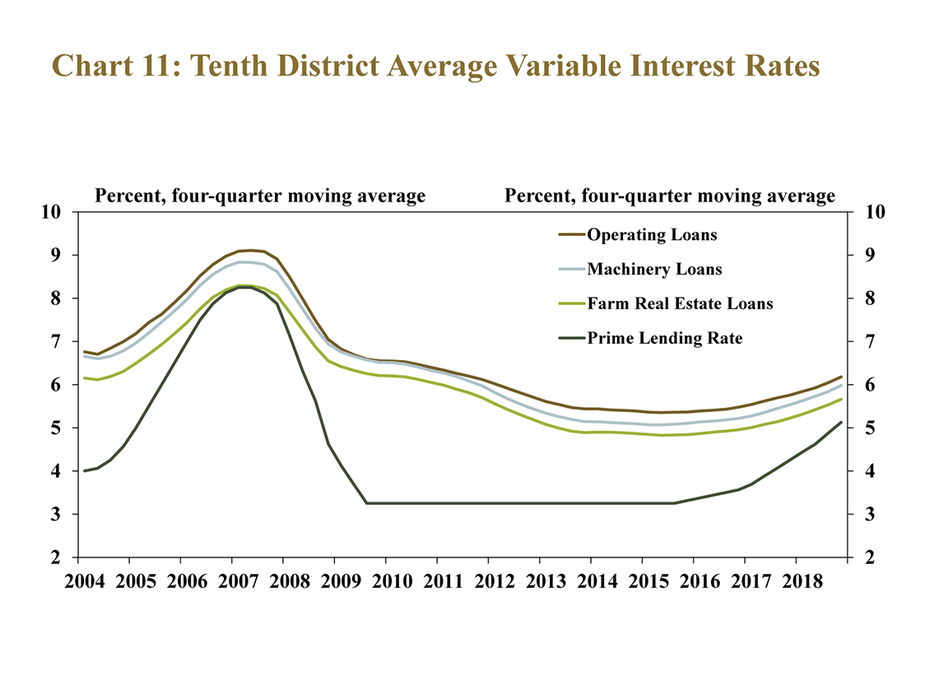

In addition to placing downward pressure on farmland values, higher interest rates also have increased financing costs for some farm borrowers, but only modestly. Interest rates on all types of agricultural loans rose further in the fourth quarter, but at a slower pace than other benchmark interest rates (Chart 11). In fact, the spread between variable rates charged on farm loans and the prime lending rate has narrowed recently and in the fourth quarter, reached the lowest margin since 2007 as farm loan interest rates have been slower to rise.

Conclusion

Farm real estate values in the Tenth District declined only modestly in the fourth quarter, despite downward pressure from a weak farm economy. The deterioration of farm finances, another year of low farm income, and higher interest rates may have contributed to a slight decline in the share of farmland purchased by farmers. Although farmers remained active in farm real estate markets, lower demand for farmland, combined with a slight uptick in volume of farmland sales in some states could weigh on farmland values moving forward. Even as risks to recent stability in farm real estate markets mounted through the end of 2018, the value of farmland continued to provide ongoing support to the farm sector and remained a key factor to monitor in 2019.

___________________________________________________________

Banker Comments from the Tenth District

Farm ground is beginning to back up in most areas. Pasture land is still selling high but trending a little lower as too much has hit the market recently and affected supply and demand. – Southeast Nebraska

Higher interest rates, low commodity prices and higher input costs are going to create more carryover and cause some farmers to go out of business. – Northeast Colorado

Low commodity prices are taking a toll. I anticipate several irrigated farmers to sell out this year as some are trying to salvage equity instead of seeing it continue to decrease year after year. – Southwest Kansas

Good farmland values are still stable in this area and a recent sale at auction brought considerably more than our present market value. – Central Missouri

A lot of land has been offered for sale and sold in our area. There has been a buyer for every farm with prices being paid that we have not seen before. – Southern Oklahoma

Recent trade talks between China and U.S. and a temporary truce on tariffs has given a slight boost to attitudes about commodity prices and market stability. – Central Kansas

Farmers that are not highly leveraged are maintaining, but those with significant leverage continue to proactively reduce assets to get out in front of struggles. – Central Kansas

Loan demand from farmer and non-farm customers continues to be very strong and deposits seem to be nearly impossible to attract. We have not declined any loans over funding issues, but that may change. – North Central Missouri

Cash flows look very tight and higher rates will apply further pressure. The trends of more stress on liquidity and earnings are very concerning, especially in the sugar industry. – Northern Wyoming

Many farmers in our portfolio seemed to out produce the low price environment again this year and USDA Market Facilitation Program payments helped those with more soybeans. – Southeast Nebraska

A total of 190 banks responded to the Fourth Quarter Survey of Agricultural Credit Conditions in the Tenth Federal Reserve District—an area that includes Colorado, Kansas, Nebraska, Oklahoma, Wyoming, the northern half of New Mexico and the western third of Missouri. Please refer questions to Cortney Cowley, economist or Ty Kreitman, assistant economist, at 1-800-333-1040.

The views expressed in this article are those of the authors and do not necessarily reflect the views of the Federal Reserve Bank of Kansas City or the Federal Reserve System.

Author