In the past, U.S. consumers who traditionally have been underserved in banking tended to live in rural communities. In recent years, however, the demographics have changed, with a majority of consumers living in metropolitan communities.

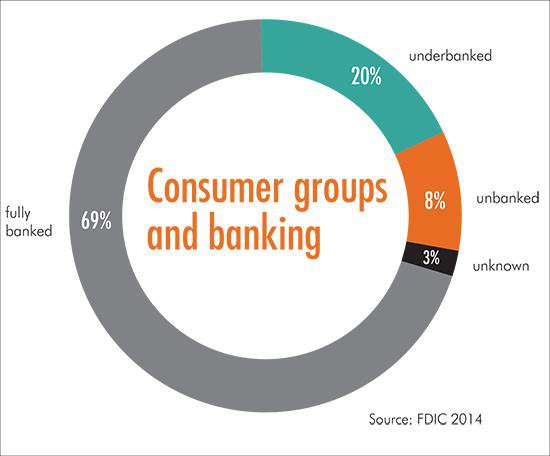

The term “underserved” in the banking system comprises two consumer groups: the “underbanked,” who have bank accounts, but have used alternative financial service providers outside the banking system such as check cashers and payday lenders within the last year, and the “unbanked,” who have no bank account, and may or may not use alternative financial services.

Kansas City Fed Senior Economist Fumiko Hayashi says a 2014 Federal Deposit Insurance Corporation (FDIC) report estimated nearly 8 percent of U.S. households, or 17 million adults, did not have a savings or checking account.

“Many of these consumers—who are considered ‘unbanked’—rely heavily on cash to meet their transaction needs,” she said.

Although a small fraction uses cash for privacy reasons, Hayashi said a majority of the unbanked do not have bank accounts for other reasons such as limited credit or banking history, low and unstable income, high fees, negative perceptions of banks and account attributes like complexity and slow speed of funds availability.

Consumers without bank accounts

Researchers estimate a good portion of the unbanked are low- to moderate-income individuals, including a high percentage of minority populations. Another segment is the unemployed—currently about 5 percent.

The average annual income of unbanked U.S. consumers varies. Surveys and reports on the unbanked show average annual household incomes between $20,000 and $50,000.

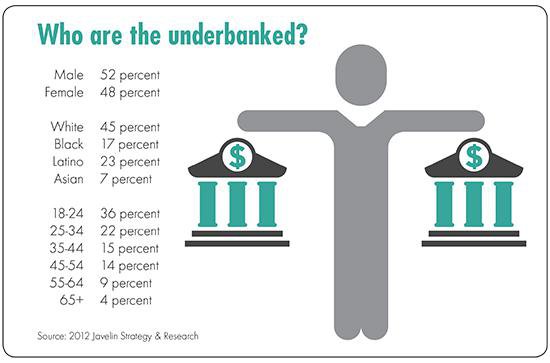

A 2012 Javelin Strategy and Research report found that a portion of the unbanked were mostly young—between 18 and 24. The report estimates many will change their financial habits as they grow older.

Because the unbanked mainly use cash, it’s not uncommon for this consumer group to pay exorbitant transactional fees. According to the St. Louis Fed, when considering the cost of cashing a bi-weekly paycheck and paying for services, such as rent and utilities using money orders each month, a household with a net income of $20,000 may pay as much as $1,200 annually for alternative service fees—substantially more than the expense of a monthly checking account fee.

In her recent research, “Access to Electronic Payments Systems by Unbanked Consumers,” Hayashi describes six main reasons consumers don’t have bank accounts.

The main reasons are ordered by importance to consumers and based on the FDIC report:

• High cost of maintaining an account due to low, unstable income and banks’ high fees

• Negative perceptions or past experiences with banks

• They do not meet banks’ qualification requirements

• Privacy—not using a bank provides more privacy

• The physical accessibility of banks, such as locations and hours

• Attributes of bank accounts and associated payment services do not meet the needs of certain groups of unbanked consumers

Understanding why consumers don’t have bank accounts is important, Hayashi says, because it will help financial institutions, payment service providers and policymakers remove barriers that prevent unbanked consumers from using financial services. This is especially important because new developments in electronic payment products could attract unbanked consumers.

Electronic payment products and the unbanked

Banks and nonbanks offer several electronic payment products that could attract unbanked consumers, including general purpose reloadable (GPR) prepaid cards, alternative checking accounts, or transaction accounts.

Hayashi evaluated payment products to see which are best equipped to address the reasons some consumers do not use the banking system.

GPR prepaid card accounts are one of the most prevalent electronic payment products for unbanked consumers. These cards can be used to make ATM cash withdrawals and retail transactions, ACH transactions and person-to-person transfers. Through participating retailers, consumers can reload the card by putting money into their account.

The FDIC report showed the share of unbanked households that had used a GPR prepaid card increased from 18 percent in 2011 to 27 percent in 2013. More than 22 percent of unbanked households used these cards in the 12 months prior to the survey, and nearly 58 percent of these households reloaded funds on their cards at least once.

For the unbanked, GPR cards have several advantages:

• The provider mitigates some qualification requirements, such as credit and banking histories, to open an account

• The cards are available at nonbanks as well as banks

• Consumers consider retailers more convenient than banks for their transaction needs

• Addresses the high costs due to unbanked consumers’ low, unstable income and bank accounts’ high fees

• Many GPR card providers offer tools such as online access, mobile applications and text alerts so cardholders can easily monitor and manage the balance of their card anytime, anywhere. Although most large banks offer similar tools, many smaller banks do not

GPR cards, however, have no advantage over traditional bank accounts in addressing consumer privacy concerns, Hayashi said. GPR card providers require prospective cardholders to present identification, and the cards’ traceable nature means payments are not anonymous, just like a debit card and ACH payments.

Alternative checking accounts offer another option for unbanked consumers to access electronic payment products such as debit cards and ACH. Banks and credit unions offer alternative checking accounts to consumers who are not qualified for, or cannot afford, traditional checking accounts.

The advantages of these accounts include:

• An alternative for consumers with credit and banking history problems

• Some alternative checking accounts offer lower fees than some traditional checking accounts

• Some depository institutions, especially credit unions, offer short-term, low interest rate, small-dollar loans to consumers with little or no credit history, which can mitigate overdraft incidents

• May be easier for consumers with limited financial literacy to manage. Some depository institutions are certified by the U.S. Treasury as Community Development Financial Institutions, which provides education to account holders and funding for account providers.

The downside, Hayashi says, is the accounts offer no advantage over traditional bank accounts in addressing consumer privacy concerns and physical accessibility. Also, some institutions charge the same fees for alterative accounts as traditional accounts.

Another type of account, a transaction account, also could address unbanked consumers’ needs.

“Outside the United States, especially in emerging and developing countries, mobile accounts—generally referred to as ‘mobile money’—have been playing a key role in promoting financial inclusion,” Hayashi said.

In the United States, mobile wallets linked with mobile carrier billing are emerging—payments made with the mobile wallet are added to the consumer’s mobile phone bill.

PayPal is the major U.S. provider of online accounts. Consumers can use PayPal to make purchases online, transfer money to and from individuals and make purchases at a brick-and-mortar store through a mobile app. Although account holders typically load funds onto the account by linking it to their bank accounts or payment card accounts, they can also load the account with cash.

The advantages of a transaction account include:

• Mitigates qualification requirements and negative perceptions of banks

• Relatively low cost to use

• Accessibility—consumers can use the account online or through a mobile app to make transactions and transfers

• For pre-funded accounts, users can visit an authorized location, such as a mobile provider, to put money into their accounts—more locations and longer operating hours than banks

• Monitor and manage accounts through mobile devices

Where there are no advantages over traditional bank accounts is with privacy—both mobile and online accounts are traceable. Also, there is limited functionality of mobile wallets because of the link with mobile payments—not all merchants accept the payment type. And there are some safety concerns, such as some payment forms are not FDIC insured and providers voluntarily limit consumer liability.

Reaching the unbanked

These accounts and associated electronic payment products can address issues unbanked consumers have with traditional bank accounts such as credit and banking history problems; high costs due to consumers’ low, unstable income and banks’ high fees; negative perceptions of or experiences with banks; and the complexity and security of certain account features.

All account types, however, need improvements to help promote adoption among consumers, Hayashi said.

“In particular, by offering faster payments as soon as is feasible, providers of electronic payment products associated with the three account types can meet unbanked consumers’ demand for immediate access to their funds and payments that immediately reach the recipients,” she said.

These options also have implications for policymakers, who will need to review the regulatory framework and encourage accessibility of faster payments through bank and alternative accounts.

“Access to affordable electronic payment products could enhance many unbanked consumers’ welfare,” Hayashi said.

Further Resources

Read "Access to Electronic Payments Systems by Unbanked Consumers" by Fumiko Hayashi.

Read "Could Restrictions on Payday Lending Hurt Consumers?" by Kelly Edmiston.

The views expressed are those of the authors and do not necessarily reflect the positions of the Federal Reserve Bank of Kansas City or the Federal Reserve System.