Consumer debt has increased steadily since 2013, but sharp differences underlie this trend.

The plunge and rise of debt

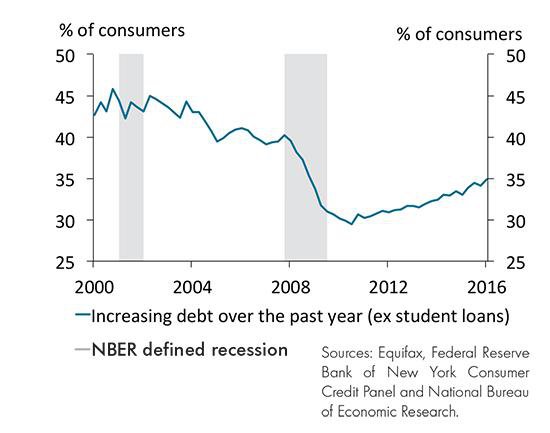

Consumer debt plunged when the Great Recession took hold in 2008, falling nearly $2 trillion by 2013. Borrowing began an upward trend, however, in mid-2013, with 35 percent of consumers adding debt from the first quarter of 2015 to the first quarter of 2016. Much of the increase, says Troy Davig, director of Economic Research at the Federal Reserve Bank of Kansas City, is among people with lower credit scores.

Who's borrowing

Since the recession, the scale of borrowing by people with lower credit scores has almost reached pre-recession levels, whereas the share of debt for consumers with higher credit scores has remained flat. The type of debt, however, has trended differently in the post-crisis economy.

Decline in mortgage debt

There was a large spike in consumer mortgage debt before the recession and then it tumbled during the recession. Since then, mortgage debt has slowly increased but remains 4 percentage points below pre-crisis levels.

Current debt increase

Most of the recent increase in debt is in credit card and auto loans, with the increase in the latter being the largest. While auto loan borrowing has more than recovered from its post-recession decline, the share of borrowers adding to credit card debt is still about 4 percentage points below its pre-recession level.

Who's behind the trend?

Consumers with lower credit scores have been the primary drivers of the increase in auto debt borrowing, with the number of borrowers increasing from 6 percent in 2010 to 15 percent in 2016. In that same period, the number of consumers with higher credit scores adding to auto loan debt has grown slightly from 8 to 9 percent.

Conclusion

Davig says adding debt to buy a long-lived asset, such as a car, can benefit consumers and the broader economy. There are, however, past examples of credit growth instability. Davig and William Xu, a research associate at the bank, looked at how consumers with lower credit scores are managing higher debt levels. The share that is current on all nonauto accounts has increased—meaning consumers are handling debt levels well—however, the share current on auto loans has declined in recent years. This could happen for many reasons, but the result is that the sale of new lightweight vehicles, which had doubled since the recession, is declining and auto demand from those with lower credit scores may face some headwinds, Davig says.

Further Resources

Read "External LinkTracking Consumer Credit Trends" by Troy Davig and William Xu.

The views expressed are those of the authors and do not necessarily reflect the positions of the Federal Reserve Bank of Kansas City or the Federal Reserve System.