New small business commercial and industrial (C&I) lending_ increased by 9.3 percent when compared to the previous quarter but remained unchanged when compared to the same period in 2022. Interest rates for term loans at both urban and rural banks mostly increased, while interest rates on new lines of credit decreased for rural banks. The percentage of new variable-rate loans with interest rate floors increased to 6.4 percent, the highest reported quarter-over-quarter increase since second quarter 2020.

With over $65 billion in small business loans reported, the 150 respondents to the survey indicated that credit standards tightened while credit quality continued to decrease. Application approval rates among large and midsized banks declined, and for the seventh consecutive quarter, respondents indicated declining loan demand. Most respondents indicated their lending to small businesses was unconstrained by available liquidity, though the percent of respondents reporting a constraint has consistently increased since first quarter 2023.

Chart 1: Outstanding Small Business Loans Increase Year-over-Year

Skip to data visualization tableNote: Items are calculated using a subset of 106 respondents that completed the FR 2028D for the last five quarters surveyed.

Sources: Call Report, Schedule RC-C Part I, items 4. Commercial and Industrial Loans and 12. Total Loans and Leases Held for Investment and Held for Sale, and FR 2028D, items 5.b and 6.c.

| Quarter-Over-Quarter | Total Loans | C&I Loans | Small Business C&I Loans |

|---|---|---|---|

| 2023:Q1 | 0.33 | 1.47 | 1.72 |

| 2023:Q2 | 1.38 | -0.38 | 0.44 |

| 2023:Q3 | -0.72 | -2.02 | 1.21 |

| 2023:Q4 | -0.45 | -1.21 | -0.93 |

| Year-Over-Year 2023:Q4 | 0.53 | -2.16 | 2.44 |

When compared to fourth quarter 2022, small business C&I loan balances increased by 2.4 percent, while C&I loans decreased by 2.2 percent and total loans increased by 0.5 percent. Quarter-over-quarter, small business loans decreased by 0.9 percent, C&I loans decreased by 1.2 percent, and total loans decreased by 0.4 percent. This is the first quarter-over-quarter decline for all loan categories since third quarter 2021.

Chart 2: New Small Business Lending Increases Quarter-Over-Quarter

Skip to data visualization tableNote: Items are calculated using a subset of 106 respondents that completed the FR 2028D for the last five quarters surveyed. All loan types referenced in Chart 2 refer to small business lending.

Source: FR 2028D, items 7.b and 8.c.

| Quarter-Over-Quarter | Total New C&I Loans | New C&I Term Loans | New C&I Credit Lines |

|---|---|---|---|

| 2023:Q1 | 2.97 | -4.72 | 14.29 |

| 2023:Q2 | 0.16 | 2.44 | -2.64 |

| 2023:Q3 | -11.24 | -8.21 | -15.15 |

| 2023:Q4 | 9.25 | 5.68 | 14.24 |

| Year-Over-Year 2023:Q4 | 0.02 | -5.31 | 7.86 |

Quarter-over-quarter, new small business loan balances increased by 9.3 percent, with a 5.7 percent increase in new term loans and a 14.2 percent increase in new credit lines. The increase in new small business lending was driven by increases in new loans across both large and mid-sized banks, while small banks reported decreases. Compared to fourth quarter 2022, total new loan balances remained stable, with the 5.3 percent decrease in new term loans being offset by the 7.9 percent increase in new credit lines.

Chart 3: Credit Line Usage Remains Stable

Skip to data visualization tableSource: FR 2028D, items 6.b and 6.c.

| Quarter | Total | Fixed Rate | Variable Rate |

|---|---|---|---|

| 2017:Q4 | 38.28 | 36.33 | 38.44 |

| 2018:Q1 | 38.79 | 29.62 | 39.87 |

| 2018:Q2 | 38.84 | 35.07 | 39.20 |

| 2018:Q3 | 37.91 | 39.85 | 37.71 |

| 2018:Q4 | 40.76 | 43.25 | 40.49 |

| 2019:Q1 | 41.05 | 43.66 | 40.77 |

| 2019:Q2 | 39.71 | 41.38 | 39.53 |

| 2019:Q3 | 39.43 | 37.56 | 39.66 |

| 2019:Q4 | 39.73 | 37.15 | 40.04 |

| 2020:Q1 | 39.98 | 36.42 | 40.34 |

| 2020:Q2 | 35.26 | 37.69 | 34.99 |

| 2020:Q3 | 33.46 | 40.64 | 32.66 |

| 2020:Q4 | 32.20 | 40.72 | 31.33 |

| 2021:Q1 | 30.83 | 38.20 | 30.16 |

| 2021:Q2 | 30.77 | 39.17 | 29.97 |

| 2021:Q3 | 32.00 | 44.04 | 30.94 |

| 2021:Q4 | 31.56 | 41.86 | 30.71 |

| 2022:Q1 | 31.79 | 41.35 | 31.00 |

| 2022:Q2 | 32.08 | 36.64 | 31.63 |

| 2022:Q3 | 31.70 | 37.28 | 31.11 |

| 2022:Q4 | 32.49 | 39.80 | 31.63 |

| 2023:Q1 | 32.37 | 40.43 | 31.54 |

| 2023:Q2 | 32.86 | 47.29 | 31.64 |

| 2023:Q3 | 33.49 | 49.57 | 32.10 |

| 2023:Q4 | 34.04 | 54.40 | 32.47 |

Usage of small business credit lines continued an increasing trend for the third straight quarter. As of fourth quarter 2023, respondents indicated variable rate lines make up about 89 percent of total credit line usage.

Chart 4: Most Rates Increase on New Term Loans

Skip to data visualization tableNote: Items are calculated using a subset of 106 respondents that completed the FR 2028D for the last five quarters surveyed.

Source: FR 2028D, item 7.c.

| Quarter | Rural Fixed New Term Loans | Rural Variable New Term Loans | Urban Fixed New Term Loans | Urban Variable New Term Loans |

|---|---|---|---|---|

| 2022:Q4 | 6.58 | 7.15 | 6.41 | 7.64 |

| 2023:Q1 | 7.37 | 7.46 | 6.93 | 8.00 |

| 2023:Q2 | 7.97 | 7.38 | 7.41 | 8.53 |

| 2023:Q3 | 7.87 | 7.72 | 7.71 | 9.00 |

| 2023:Q4 | 7.98 | 8.44 | 7.98 | 8.86 |

Median interest rates increased for most new small business term loans in fourth quarter 2023. The highest reported rates were for variable rate loans offered at urban banks, which were reported as 8.9 percent. This was a 14-basis point decrease from third quarter 2023, which brought variable rates offered at urban banks closer to parity with their rural counterparts. The lowest reported rates were for fixed rates offered at urban and rural banks, which were both reported as 8.0 percent. _

Chart 5: Rates Offered at Rural Banks on New Lines of Credit Decrease

Skip to data visualization tableNote: Items are calculated using a subset of 106 respondents that completed the FR 2028D for the last five quarters surveyed.

Source: FR 2028D, item 8.d.

| Quarter | Rural Fixed New LOC | Rural Variable New LOC | Urban Fixed New LOC | Urban Variable New LOC |

|---|---|---|---|---|

| 2022:Q4 | 7.20 | 8.09 | 6.40 | 8.27 |

| 2023:Q1 | 7.47 | 8.80 | 6.75 | 8.62 |

| 2023:Q2 | 7.84 | 9.05 | 7.11 | 8.93 |

| 2023:Q3 | 8.84 | 9.23 | 7.43 | 9.06 |

| 2023:Q4 | 8.38 | 8.93 | 7.67 | 9.13 |

Median interest rates on new rural small business lines of credit decreased in fourth quarter 2023, while rates at urban banks increased. Variable and fixed rates offered at rural banks reported a 29-basis point and 46-basis point decrease, respectively, from third quarter 2023, which is directionally consistent with the 15-basis point decrease for the three-month Treasury rate. The highest rates were for variable lines of credit offered at urban banks, which were reported as 9.1 percent, while the lowest were fixed rates offered at urban banks, which were reported as 7.7 percent.

Chart 6: New Loans with Interest Rate (IR) Floors Increase

Skip to data visualization tableSources: FR 2028D, items 7.a, 7.f, 8.a, 8.e and Federal Reserve Bank of St. Louis, 3-Month Treasury Constant Maturity Rate.

| Quarter | Percent of Loan Balances with IR Floor | Three-Month Treasury Rate |

|---|---|---|

| 2017:Q4 | 8.07 | 1.21 |

| 2018:Q1 | 6.22 | 1.56 |

| 2018:Q2 | 8.86 | 1.84 |

| 2018:Q3 | 9.43 | 2.04 |

| 2018:Q4 | 8.64 | 2.32 |

| 2019:Q1 | 7.98 | 2.39 |

| 2019:Q2 | 8.15 | 2.30 |

| 2019:Q3 | 8.58 | 1.98 |

| 2019:Q4 | 8.80 | 1.58 |

| 2020:Q1 | 8.00 | 1.11 |

| 2020:Q2 | 9.82 | 0.14 |

| 2020:Q3 | 8.60 | 0.11 |

| 2020:Q4 | 8.39 | 0.09 |

| 2021:Q1 | 5.47 | 0.05 |

| 2021:Q2 | 5.85 | 0.03 |

| 2021:Q3 | 5.67 | 0.04 |

| 2021:Q4 | 5.85 | 0.06 |

| 2022:Q1 | 5.01 | 0.52 |

| 2022:Q2 | 4.87 | 1.72 |

| 2022:Q3 | 5.04 | 3.33 |

| 2022:Q4 | 5.14 | 4.42 |

| 2023:Q1 | 5.02 | 4.85 |

| 2023:Q2 | 5.77 | 5.43 |

| 2023:Q3 | 5.56 | 5.55 |

| 2023:Q4 | 6.45 | 5.40 |

While the three-month Treasury rate decreased slightly, the percentage of new variable-rate loans with interest rate floors increased from 5.6 to 6.4 percent, representing the highest quarterly increase since second quarter 2020.

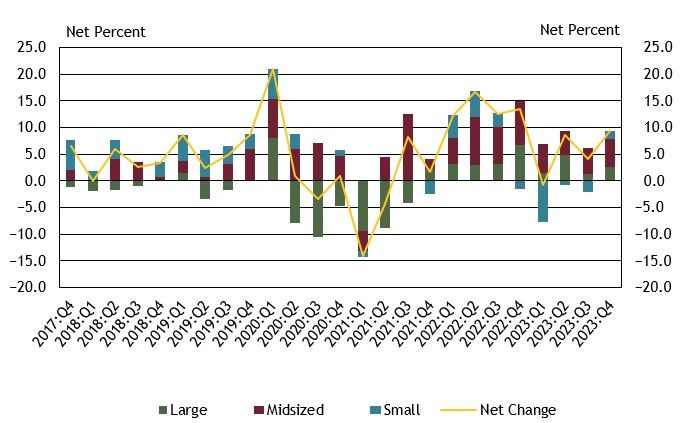

Chart 7: All Bank Sizes Report Increase in Credit Line Usage

Note: Chart 7 shows diffusion indexes for credit line usage. The diffusion indexes show the difference between the percent of banks reporting decreased credit line usage and those reporting increased credit line usage. Net percent refers to the percent of banks that reported having decreased (“decreased somewhat” or “decreased substantially”) minus the percent of banks that reported having increased (“increased somewhat” or “increased substantially”)._

Source: FR 2028D, items 9 and 10.

In the fourth quarter, 25 percent of respondents reported a change in credit line usage. Nine percent of respondents, on net, indicated that credit line usage increased, up from 4 percent last quarter.

On net, all bank sizes reported an increase in credit line usage. Of the banks reporting an increase, about 31 percent cited changes in local or national economic conditions and changes in borrowers’ business revenue or other business-specific conditions as very important reasons.

The reported increase in credit line usage is consistent with a shift to increased debt financing observed in other key indicators such as elevated consumer credit card debt. _ Total household credit card debt continues to increase each quarter._

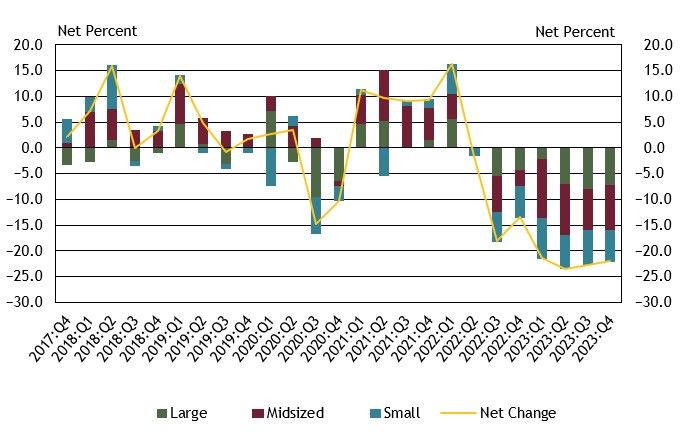

Chart 8: Respondents Report Declines in Loan Demand for Seventh Consecutive Quarter

Note: Chart 8 shows diffusion indexes for loan demand. The diffusion indexes show the difference between the percent of banks reporting weakened loan demand and those reporting stronger loan demand. Net percent refers to the percent of banks that reported having weakened (“moderately weaker” or “substantially weaker”) minus the percent of banks that reported having stronger loan demand (“moderately stronger” or “substantially stronger”).

Source: FR 2028D, item 11.

About 43 percent of respondents reported a change in small business loan demand in fourth quarter 2023. On net, about 22 percent of respondents indicated weaker loan demand across all bank sizes. This marks the seventh consecutive quarter of respondents reporting a net decline in loan demand.

The timing of softer loan demand aligns with the Federal Reserve’s tightened monetary policy since mid-2022. It is also consistent with the External LinkJanuary 2024 Federal Reserve Senior Loan Officer Opinion Survey (SLOOS), where about 31 percent of respondents reported weaker C&I loan demand from small firms (annual sales of less than $50 million) over the prior three months.

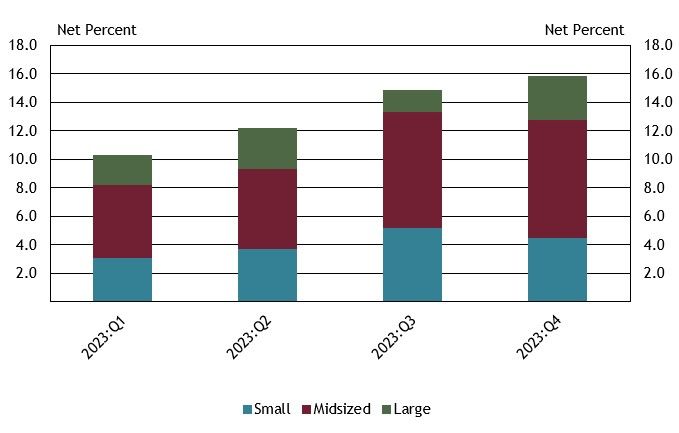

Chart 9: Banks Indicating More Constrained Lending Increases Slightly

Source: FR 2028D, Special Question.

About 16 percent of all respondents indicated their lending to small businesses was constrained by the availability of liquidity in the market in fourth quarter 2023. This is an increase of 5.5 percent from first quarter 2023 and a 1 percent increase from the previous quarter. For the respondents who indicated lending was constrained, the most cited reason was greater competitive pressures for deposits (100 percent). This increase is consistent with more respondents citing deterioration in their bank's current or expected liquidity position as a reason for tightening credit standards or terms.

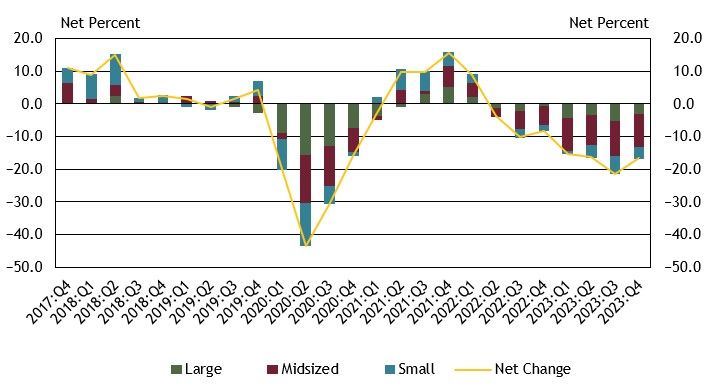

Chart 10: Overall Credit Quality Continues to Decline

Note: Chart 10 shows diffusion indexes for credit quality of applicants. The diffusion indexes show the difference between the percent of banks reporting a decline in credit quality and those reporting improvement in credit quality. Net percent refers to the percent of banks that reported declining credit quality (“declined somewhat” or “declined substantially”) minus the percent of banks that reported improving credit quality (“improved somewhat” or “improved substantially”).

Source: FR 2028D, items 18 and 19.

About 17 percent of survey respondents, on net, reported a decrease in applicant credit quality, a slight improvement from 21 percent in third quarter 2023. This is the seventh consecutive period in which respondents of all bank sizes, on net, reported a decrease. Of the respondents reporting a change in credit quality, whether an increase or decrease, 44 percent cited the debt-to-income level of business owners and liquidity position of business owners as very important reasons for a change. Other commonly cited reasons for a change include recent business income growth, credit scores, quality of business collateral, and personal wealth of business owners.

The decrease in applicant credit quality reported by firms is consistent with the negative outlook of loan availability reported by small businesses in the External LinkJanuary 2024 NFIB Survey of Loan Availability.

Chart 11: Loan Approval Rates Decrease for Midsized and Large Banks

Skip to data visualization tableSource: FR 2028D, items 12.a and 13.

| Quarter | Small | Midsized | Large |

|---|---|---|---|

| 2017:Q4 | 88.14 | 75.33 | 51.07 |

| 2018:Q1 | 87.00 | 86.15 | 56.78 |

| 2018:Q2 | 86.32 | 80.90 | 48.71 |

| 2018:Q3 | 85.07 | 85.50 | 52.83 |

| 2018:Q4 | 82.91 | 85.18 | 55.04 |

| 2019:Q1 | 89.81 | 86.15 | 55.12 |

| 2019:Q2 | 89.68 | 81.50 | 55.45 |

| 2019:Q3 | 79.00 | 80.93 | 54.01 |

| 2019:Q4 | 86.87 | 76.18 | 53.58 |

| 2020:Q1 | 87.44 | 75.45 | 51.93 |

| 2020:Q2 | 87.98 | 95.12 | 74.54 |

| 2020:Q3 | 86.52 | 89.81 | 38.33 |

| 2020:Q4 | 89.52 | 79.64 | 45.56 |

| 2021:Q1 | 89.73 | 88.23 | 51.24 |

| 2021:Q2 | 93.50 | 89.83 | 46.85 |

| 2021:Q3 | 71.20 | 85.20 | 49.78 |

| 2021:Q4 | 81.00 | 87.23 | 50.50 |

| 2022:Q1 | 83.15 | 77.35 | 51.31 |

| 2022:Q2 | 83.25 | 80.43 | 51.83 |

| 2022:Q3 | 86.77 | 86.50 | 48.34 |

| 2022:Q4 | 86.38 | 68.93 | 47.82 |

| 2023:Q1 | 86.96 | 67.96 | 49.66 |

| 2023:Q2 | 84.46 | 67.44 | 48.42 |

| 2023:Q3 | 88.43 | 68.27 | 51.67 |

| 2023:Q4 | 89.48 | 66.00 | 48.87 |

Large bank approval rates decreased from 52 percent to 49 percent and midsized bank approval rates decreased from 68 percent to 66 percent in the fourth quarter. Small banks increased slightly from 88 percent to 89 percent over the quarter. About 67 percent of respondents indicated borrower financials were the most common reason for denying a loan. Other commonly cited reasons were borrower collateral and credit history.

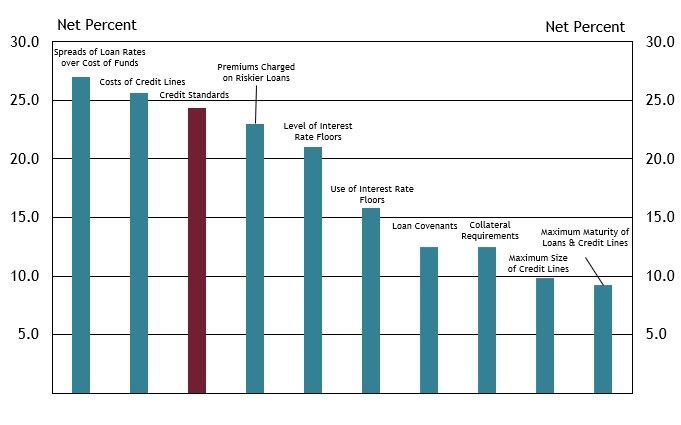

Chart 12: Respondents Report Tightening Credit Standards for the Ninth Consecutive Quarter

Note: Chart 12 shows diffusion indexes for credit standards (red bar) and various loan terms. The diffusion indexes show the difference between the percent of banks reporting tightening terms and those reporting easing terms. Net percent refers to the percent of banks that reported having tightened (“tightened somewhat” or “tightened considerably”) minus the percent of banks that reported having eased (“eased somewhat” or “eased considerably”). Source: FR 2028D, items 14, 15, 16 and 17.

About 24 percent of respondents reported tightening credit standards (red bar) in the fourth quarter. This is the ninth consecutive quarter that respondents have reported tightening credit standards and is consistent with the tightening credit standards reported in the External LinkJanuary 2024 Senior Loan Officer Opinion Survey on Bank Lending Practices.

On net, respondents indicated that all loan terms tightened. About 85 percent of respondents cited less favorable or more uncertain economic outlook as a somewhat important or very important reason for the tightening. Other commonly cited reasons were worsening of industry-specific problems and reduced tolerance for risk.

Other contributors to the release include Lauren Bennett, Nicholas Bloom, Nicholas Courtney, Stefan Jacewitz, Stewart Pozzuto, and Emily Robinson.

Endnotes

-

1 Small business lending refers to commercial and industrial lending to organizations generally defined as having less than five million in gross annual revenue, unless otherwise noted.

-

2 Urban and rural classification is determined exclusively by the bank’s head office location and External LinkUS Census Population data.

-

3 Small banks have total assets of $1 billion or less, midsized banks have total assets between $1 billion and $10 billion and large banks have total assets greater than $10 billion.

-

4 Source: FRED, Consumer Loans: Credit Cards and Other Revolving Plans.

-

5 Source: FRBNY Consumer Credit Panel/Equifax

The views expressed are those of the authors and do not necessarily reflect the positions of the Federal Reserve Bank of Kansas City or the Federal Reserve System.

Authors

Dustyn DeSpain, Assistant Vice President

Assistant Vice President