The dollar volume of new small business commercial and industrial (C&I) loans declined 9.9 percent in the first quarter of 2019 compared with the first quarter of 2018. The decline was driven by a 19.9 percent decrease in new small business C&I credit lines. Total small business C&I loan balances increased, but grew at the lowest rate in five quarters. Most of the 133 respondents to the Federal Reserve’s Small Business Lending Survey (FR 2028D) reported that credit standards remained stable, but indicated tightening of most loan terms. Interest rates on variable rate term loans and lines of credit rose in the first quarter, while loan demand increased and credit line usage remained unchanged.

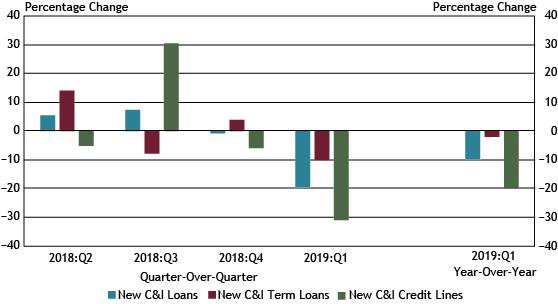

Chart 1: New Small Business C&I Loans Decline

Note: Items are calculated using a subset of respondents that completed the FR 2028D for the last five quarters surveyed. All loan types referenced in Chart 1 refer to small business lending.

Source: FR 2028D, items 7.b and 10.c.

The value of new small business C&I loans decreased 19.8 percent in the first quarter compared with the previous quarter, reflecting decreases in both new C&I term loans and new C&I credit lines of 10.1 percent and 31.1 percent, respectively. Compared with the same quarter in 2018, total new small business C&I loans decreased 9.9 percent, with new C&I term loans decreasing 1.9 percent and new C&I credit lines decreasing 19.9 percent.

Chart 2: Small Business C&I Loan Balances Increase at Lowest Rate in Five Quarters

Note: Items are calculated using a subset of respondents that completed the FR 2028D for the last five quarters surveyed.

Sources: Call Report, schedule RC-C, items 4 and 12; and FR 2028D, items 4.b and 5.c.

Balances on C&I and small business C&I loans increased for the fifth consecutive quarter, while total loans increased for the fourth consecutive quarter. Small business C&I loan balances were up only 0.1 percent in the first quarter, the smallest increase in five quarters. Compared with the first quarter of 2018, small business C&I loans grew 1.8 percent, lagging total loans and C&I loans, which grew 3.7 percent and 10.1 percent, respectively.

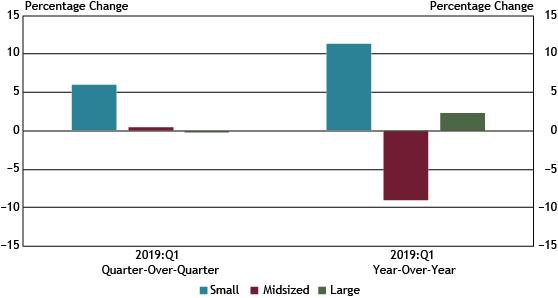

Chart 3: Small Banks Report Largest Increase in Outstanding Small Business C&I Loan Balances

Note: Items are calculated using a subset of respondents that completed the FR 2028D for the last five quarters surveyed. Small banks have total assets of $1 billion or less, midsized banks have assets between $1 billion and $10 billion and large banks have assets greater than $10 billion.

Source: FR 2028D, items 4.b and 5.c.

Small banks reported the largest increase in outstanding small business C&I loan balances compared with the previous quarter and year-over-year, growing 5.9 percent and 11.4 percent, respectively. Midsized banks reported a decline of 9.0 percent in outstanding small business C&I loan balances compared with the first quarter of 2018.

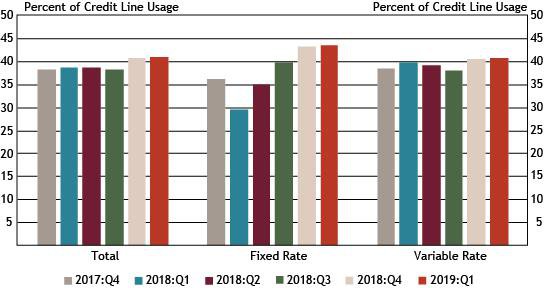

Chart 4: Total Small Business C&I Credit Line Usage Remains Largely Unchanged

Source: FR 2028D, items 5.b and 5.c.

Total small business C&I credit line usage remained largely unchanged from the previous quarter at 41.0 percent. Similarly, both fixed and variable rate credit line usage remained unchanged from the fourth quarter of 2018.

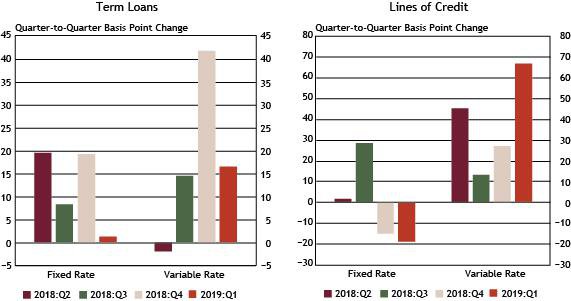

Chart 5: Interest Rates on Variable Rate Term Loans and Lines of Credit Increase

Note: Items are calculated using a subset of respondents that completed the FR 2028D for the last five quarters surveyed.

Source: FR 2028D, items 7.c and 10.d.

Weighted average rates on variable rate credit grew at the fastest pace in the first quarter, with variable rate lines of credit increasing 67 basis points and variable rate term loans increasing 17 basis points. Weighted average fixed rates on lines of credit declined for the second consecutive quarter, decreasing 19 basis points, while weighted average rates on fixed rate term loans remained largely unchanged.

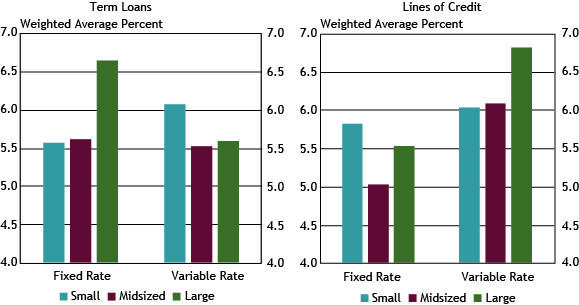

Chart 6: Large Banks Charge Highest Rates on New Fixed Rate Term Loans and Variable Rate Lines of Credit

Note: Average interest rates are weighted by the dollar volume of new small business C&I loans. Small banks have total assets of $1 billion or less, midsized banks have total assets between $1 billion and $10 billion and large banks have total assets greater than $10 billion.

Source: FR 2028D, items 7.c and 10.d.

First quarter weighted average interest rates varied on new small business C&I term loans and lines of credit across bank sizes, ranging from 5.04 percent to 6.82 percent. Large banks charged the highest rates on fixed rate term loans and variable rate lines of credit, while small banks charged the highest rates on variable rate term loans and fixed rate lines of credit.

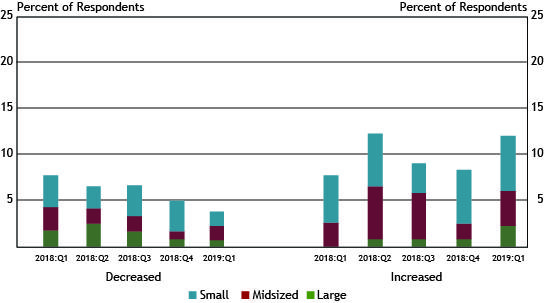

Chart 7: Credit Line Usage Remains Stable

Note: Small banks have total assets of $1 billion or less, midsized banks have total assets between $1 billion and $10 billion and large banks have total assets greater than $10 billion.

Source: FR 2028D, item 11.

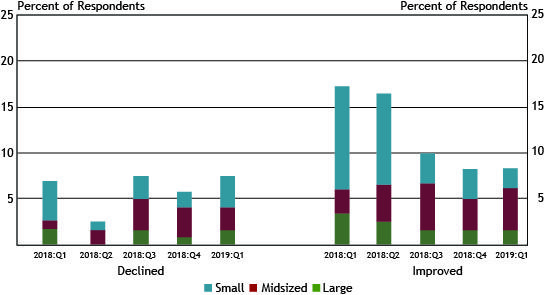

The percentage of respondents indicating no change in credit line usage declined slightly from 87 percent in the fourth quarter of 2018 to 84 percent in the first quarter of 2019. About 12 percent of respondents indicated that credit line usage increased. Small banks represented the largest group reporting an increase. Respondents reporting a decrease in credit line usage declined for the third consecutive quarter to 4 percent. The most commonly cited reasons for a change, whether an increase or decrease, were related to borrowers’ business revenue or other business-specific conditions and differences in local or national economic conditions.

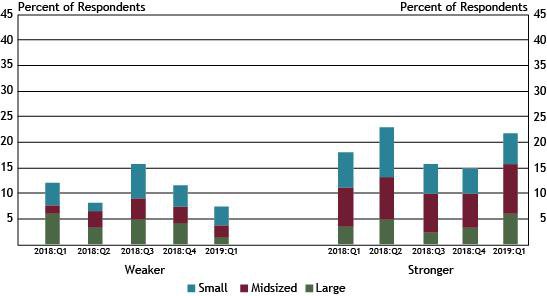

Chart 8: Respondents Report Stronger Loan Demand

Note: Small banks have total assets of $1 billion or less, midsized banks have total assets between $1 billion and $10 billion and large banks have total assets greater than $10 billion.

Source: FR 2028D, item 13.

The number of respondents reporting stronger loan demand increased in the first quarter, while those reporting weaker demand decreased. Respondents reporting stronger loan demand rose to 22 percent, higher than the 18 percent of banks reporting stronger loan demand in the same period of 2018. The number of respondents reporting stronger loan demand increased across all bank sizes. About 7 percent of respondents indicated weaker loan demand in the first quarter.

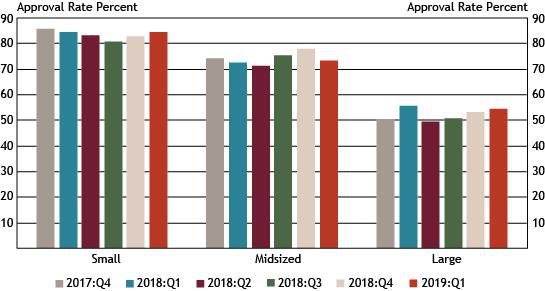

Chart 9: Small Business C&I Application Approval Rates Increase for Small and Large Banks

Note: Small banks have total assets of $1 billion or less, midsized banks have total assets between $1 billion and $10 billion and large banks have total assets greater than $10 billion.

Source: FR 2028D, items 14.a and 17.

Application approval rates varied from 85 percent at small institutions to 54 percent at large institutions during the first quarter. Application approval rates trended higher for small and large banks but decreased for midsized institutions. The three most commonly cited reasons for denying a loan were borrower financials, collateral quality and credit history.

Chart 10: Small Business Credit Quality Remains Stable

Note: Small banks have total assets of $1 billion or less, midsized banks have assets between $1 billion and $10 billion and large banks have assets greater than $10 billion.

Source: FR 2028D, items 24 and 25.

About 85 percent of respondents indicated credit quality remained unchanged in the first quarter with 8 percent reporting improved credit quality and 7 percent indicating a decline in credit quality. The percentage of respondents reporting improved credit quality decreased from the first quarter of 2018 when 17 percent reported improved credit quality. Respondents reporting a decline in credit quality cited recent business growth, credit scores, the debt-to-income level of business owners and the liquidity position of business owners as important reasons for the decline.

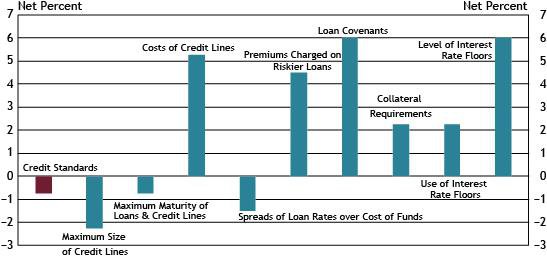

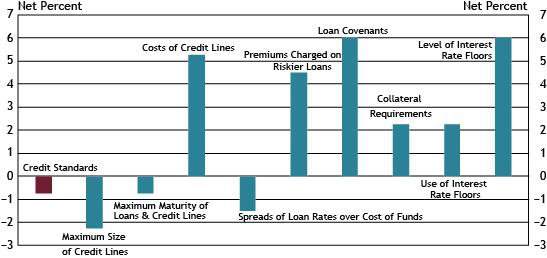

Chart 11: Banks Tighten Most Loan Terms

Note: The net percent refers to the percent of banks that reported having tightened (“tightened considerably” or “tightened somewhat”) minus the percent of banks that reported having eased (“eased considerably” or “eased somewhat”).

Source: FR 2028D, items 18, 19, 20 and 22.

Chart 11 shows diffusion indexes for credit standards (red bar) and various loan terms. The diffusion indexes show the difference between the percent of banks reporting tightening terms and those reporting easing terms. About 87 percent of respondents reported no change in credit standards in the first quarter, down from 92 percent in the fourth quarter of 2018. Of banks indicating a change in credit standards, slightly more reported easing.

On net, respondents indicated that most loan terms tightened with loan covenants and level of interest rate floors showing the most tightening. Respondents indicated that maximum size of credit lines and spreads of loan rates over cost of funds were the loan terms that showed the most easing, on net.

Of respondents reporting tightening, 71 percent cited a less favorable or more uncertain economic outlook as a somewhat or very important reason, with 63 percent citing worsening of industry-specific problems and 55 percent indicating a reduced tolerance for risk. More aggressive competition from other bank lenders was cited as a somewhat or very important reason by 77 percent of respondents reporting easing, with 63 percent indicating more aggressive competition from nonbank lenders.

*Other contributors to this report included Dan Harbour, Thomas Hobson, Alli Jakubek, Brody Smith, Tony Walker and Jim Wilkinson.

Contact Us

For questions or comments about this survey, contact us at KC SRM FR2028D Survey.

The views expressed are those of the authors and do not necessarily reflect the positions of the Federal Reserve Bank of Kansas City or the Federal Reserve System.