Summary of Quarterly Indicators

Growth in Tenth District energy activity slowed in the third quarter of 2017, as indicated by firms contacted between September 15 and 29 (Tables 1 & 2). Most indexes fell but remained positive. The drilling and business activity index declined from 43 to 7 (Chart 1). The indexes for employment, employee hours and wages and benefits were moderately lower, and the supplier delivery time index fell into negative territory. However, access to credit climbed back into positive territory, and the revenues index inched higher. The total profits index increased from 3 to 21.

Chart 1.

Drilling/Business Activity Index vs. a Quarter Ago

Skip to data visualization table| Date | Drilling/Business Activity |

|---|---|

| 2014Q1 | 39 |

| 2014Q2 | 38 |

| 2014Q3 | 50 |

| 2014Q4 | -24 |

| 2015Q1 | -68 |

| 2015Q2 | -37 |

| 2015Q3 | -37 |

| 2015Q4 | -56 |

| 2016Q1 | -72 |

| 2016Q2 | 0 |

| 2016Q3 | 26 |

| 2016Q4 | 64 |

| 2017Q1 | 55 |

| 2017Q2 | 43 |

| 2017Q3 | 7 |

Most year-over-year indexes declined but remained above zero. The drilling and business activity, revenues, and profits indexes fell considerably. Capital expenditures and employment eased somewhat. Furthermore, the supplier delivery time index dropped from 11 to -14. On the other hand, access to credit increased to its highest level since the third quarter of 2014, and wages and benefits increased for the third consecutive quarter.

Expectations were mixed but overall solid. The future wages and benefits, revenues, profits, and capital expenditures indexes increased moderately. The future drilling and business activity and access to credit indexes edged higher. The future employment index was largely unchanged, while employee hours eased slightly. The supplier delivery time index turned negative for the first time since the fourth quarter of 2016.

Most price expectations for oil and gas improved. The expected oil and gas prices indexes increased considerably, indicating that a larger number of respondents expected prices to increase over the next six months. The NGL price index continued to increase modestly.

Summary of Special Questions

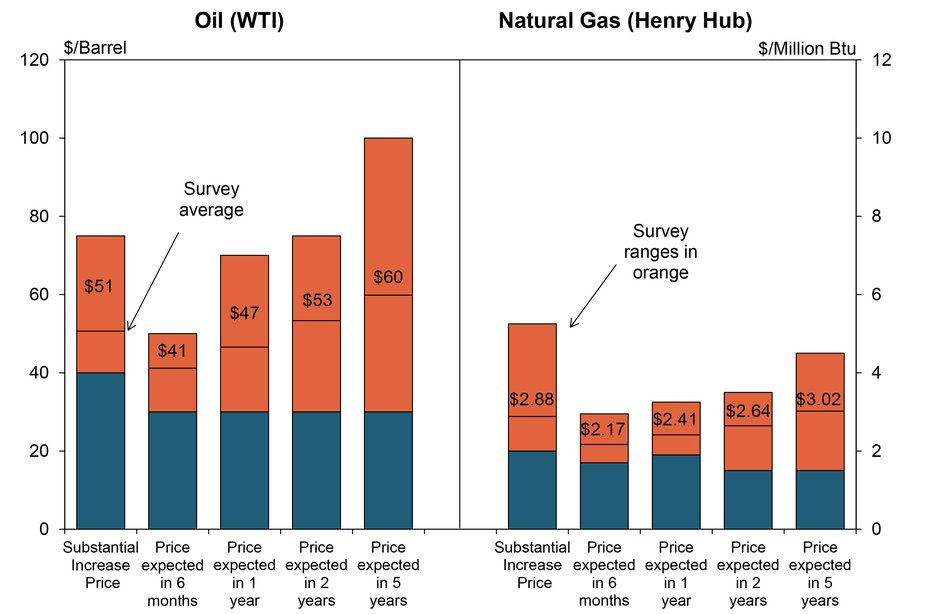

Firms were asked what oil and natural gas prices were needed for drilling to be profitable in the areas in which they were active. The average oil price needed was $51 per barrel, with a range of $40 to $75 (Chart 2). This was flat from the first quarter survey. The average natural gas price needed was $3.05 per million Btu, with responses ranging from $2 to $4. This was down from $3.38 per million Btu in the first quarter.

Chart 2. Special Question - What price is currently needed for drilling to be profitable for oil and natural gas, and what do you expect the WTI and Henry Hub prices to be in six months, one year, two years, and five years?

Firms were asked what they expected oil and natural gas prices to be in six months, one year, two years, and five years. Oil and gas price expectations increased modestly since the second quarter. The average expected WTI prices were $52, $55, $58, and $65 per barrel, respectively. The average expected Henry Hub natural gas prices for these periods were $3.01, $3.11, $3.30, and $3.73 per million Btu.

Firms were asked to estimate the impact of Hurricane Harvey on each segment of the oil and gas industry. Refineries were expected to be the most affected. Almost half of respondents estimated a medium impact and a fifth estimated high impact (Chart 3). The impact to trade was estimated at low to medium. Responses were mixed for offshore production, but over a third expected a medium impact. The impact to onshore production and pipelines and transportation was largely expected to be low.

Chart 3.

Special Question - What is your estimated severity of impact from Hurricane Harvey on each segment of the oil and gas industry?

Skip to data visualization table| Segment | None | Low | Medium | High | Severe |

|---|---|---|---|---|---|

| Upstream Offshore | 33 | 30 | 37 | 0 | 0 |

| Upstream OnShore | 22 | 63 | 15 | 0 | 0 |

| Pipelines | 26 | 63 | 11 | 0 | 0 |

| Refineries | 11 | 22 | 48 | 19 | 0 |

| Trade | 15 | 50 | 35 | 0 | 0 |

Additionally, firms were asked to give their estimates on the duration of impact from Hurricane Harvey on each segment. The impact was expected to last an average of nine weeks for refineries and almost six weeks for trade (Chart 4). Production and pipelines and transportation were estimated to be affected for four to five weeks.

Chart 4.

Special Question - What is your estimated duration of impact (in weeks) from the start of Hurricane Harvey (8/25/17) for the following segments of the oil and gas industry?

Skip to data visualization table| Segments | Average |

|---|---|

| Upstream Offshore | 5 |

| Upstream OnShore | 4 |

| Pipelines or Transportation | 5 |

| Refineries | 9 |

| Trade (Imports and Exports) | 6 |

Firms were asked how they expected the oil rig count to change over the next six months compared to current levels. Three-fourths of respondents expected rig counts to remain close to current levels. Slightly more than a fifth expected an increase, while only a few expected a decrease.

Finally, firms were asked for their year-end 2018 U.S. production forecast. A majority of respondents expected production to increase from current levels, to an average of 9.9 million barrels per day by the end of 2018.

Table 1 - Summary of Tenth District Energy Conditions, Quarter 3, 2017

Table 2 - Historical Energy Survey Indexes

Selected Comments

“We are moving ahead with the expectation that commodity prices may not materially improve for years. We can grow and be profitable at these levels as long as we watch our cost structure carefully.”

“Global market tightening due to continued OPEC production cuts and growing global demand are driving price expectations. Demand growth and reduced investment in long lead offshore developments may also give way to higher long-term prices.”

“We continue to balance expenditures and income to maximize growth and avoid additional debt.”

“Low worldwide demand growth and resiliency in supply are driving our oil price expectations.”

“Due to the large quantities of natural gas that can be produced from the Marcellus and other shale areas, I don’t see natural gas prices going up that much in the next couple of years. However, long-term I see natural gas prices going up as these excess quantities can be exported.”

“There is ample supply in the U.S. and abroad to keep natural gas prices in the $3.00 to $4.00 per million btu range for years ahead.”

“Saudi Arabia will continue to prop up price until after the Saudi Aramco IPO, which appears may still be 18 months out. By that time expectations are that demand will have caught up to supply, and then I expect more natural price inflation.”

Additional Resources

The views expressed are those of the authors and do not necessarily reflect the positions of the Federal Reserve Bank of Kansas City or the Federal Reserve System.

Author