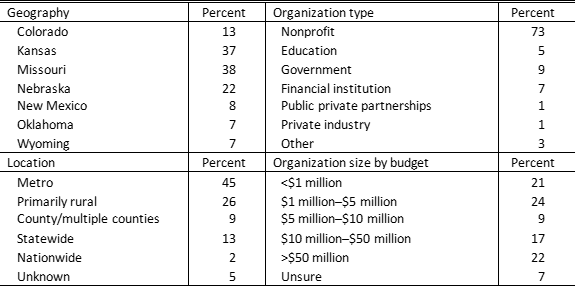

This Community Conditions Survey report is based on responses within the Tenth Federal Reserve District—a region covering Colorado, Kansas, Nebraska, Oklahoma, Wyoming, and parts of Missouri and New Mexico—to the Community Perspectives Survey, a national expansion of the Community Conditions Survey. The report covers reported community economic conditions in Part 1 and the financial and operational health of low- and moderate-income (LMI)-serving organizations in Part 2.

Part 1: Community Conditions

Regional responses to the national Community Perspectives Survey suggest that community conditions in the Tenth Federal Reserve District have generally worsened. In nearly every sector, a plurality of respondents reported poorer conditions in spring 2025 relative to fall 2024, when the District-focused Community Conditions Survey was conducted. The one exception is the human services sector, which reported modest improvements relative to fall 2024. However, the sector had the largest share of respondents reporting “very poor” conditions, and no respondents expected conditions to improve over the next year. Conditions for finding work deteriorated modestly over the last six months, and respondents were mixed on their expectations of conditions in the sector through the next year.

Economic Mobility Outlook

Conditions for economic mobility worsened considerably between fall 2024 and spring 2025. The share of organizations in the region reporting that conditions for economic mobility were “poor” or “very poor” increased by 22 percentage points, with most of that share shifting from responses of “neither good nor poor” in the last survey. The share of respondents expecting conditions for economic mobility to worsen over the next year also increased. While respondents’ expectations for economic mobility were mixed in fall 2024, Chart 1 shows that as of spring 2025, a substantial majority of respondents expect conditions to worsen over the next year.

Chart 1: Few sectors report good current conditions, and most expect worsening conditions over the next year

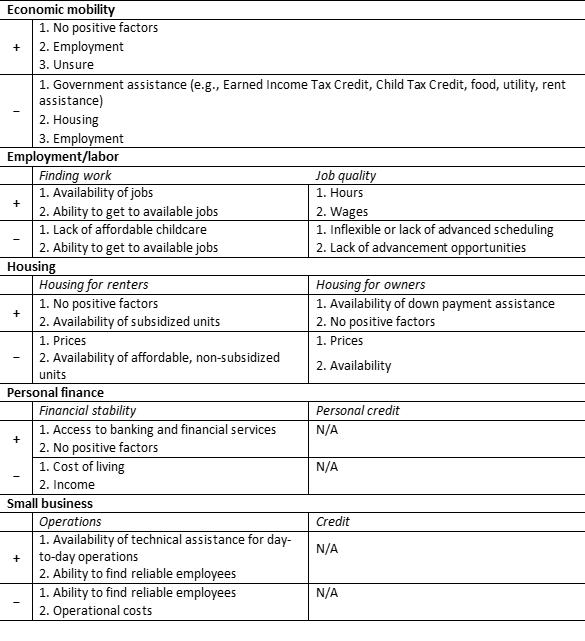

Expectations have similarly fallen for employment, housing, and personal finance. While respondents to the fall 2024 survey expected improvements in all three sectors, respondents in spring 2025 expected worsening conditions in housing and personal finance. Table 1 emphasizes this deterioration. When asked to rank the top positive and negative factors affecting their expectations for the next year, respondents ranked “no positive factors” first for both housing and financial stability.

Table 1 also shows that respondents’ top areas of concern have changed somewhat. Although housing and wages were the biggest concerns in the fall, by spring, respondents’ top concern shifted to the availability of government assistance. Most comments focused on the expected negative effects of changes to federal programs for low- and moderate-income (LMI) populations.

Table 1: Top positive and negative factors affecting expectations over the next year

Notes: Respondents were asked to choose the top three positive and top three negative factors affecting their expectations of conditions over the next year for each program area. Respondents could select "No positive factors" in lieu of ranking if they were unable to identify any positive factors affecting their expectations for the sector. To generate an overall ranking, individual rankings were weighted, with items ranked "1" scored higher than items ranked "2" or "3." "N/A" indicates not enough responses to reliably report. The third ranked item in each sector is not reported for brevity.

Sector Highlights

Employment. Organizations working in the employment sector reported mixed employment conditions overall with a slight skew toward poor conditions. The share of organizations reporting “good” conditions was higher for employment than for other areas. Comments were mixed on whether there were jobs available or not, and respondents mentioned inadequate wages where jobs were available. Job-readiness training, transportation, and childcare remained commonly cited barriers to work.

Housing. After some improvement in the fall 2024 survey, respondents in the housing sector shifted back to reporting “poor” conditions for both renter and owner housing. In addition, respondents shifted back to reporting that they expect housing conditions to worsen. The ranking of factors did not change between surveys, and comments centered around the declining affordable housing stock and prices rising faster than wages.

Personal finance. Respondents working in the finance sector reported the poorest conditions of any other sector in both the fall 2024 and spring 2024 surveys. However, expectations have worsened. In the fall, respondents expected conditions to improve over the next year. In the spring survey, respondents largely expected conditions to worsen. Comments centered on an increasing cost of living outpacing wage gains but also mentioned job losses and concerns about nonprofits being able to meet the needs of LMI populations.

Small business. Conditions for small business credit were “poor,” and nearly all respondents in the sector expect worsening conditions over the coming year. Comments mentioned tightening standards due to concerns about the overall economy and the deteriorating credit quality of small business applicants.

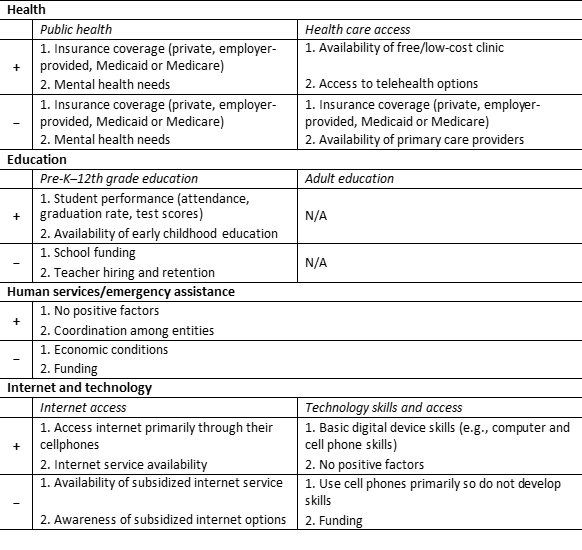

Health. Although respondents reported “poor” conditions in public health, their views of current health care access were mixed. However, respondents expect conditions in both sectors to worsen over the coming year, with a significant share expecting conditions to worsen substantially. Insurance and the availability of providers were ranked as top concerns (Table 1), reinforced by comments about rising uninsured rates stemming from changes to Medicaid. Many respondents also mentioned seeing rising numbers of people putting off care or being unable to find providers.

Education. Conditions for pre-K through 12th-grade education were mixed, and most respondents in the education sector expect conditions to worsen over the coming year. Comments mentioned heightened concerns around funding for Head Start and public schools in general.

Human services. Although human services respondents in the region were mixed on their ratings of current conditions, nearly all respondents expect conditions to worsen over the coming year. This differed from the national results, where only 20 percent of respondents nationwide reported “good” conditions compared with 40 percent of respondents in the region. Moreover, 24 percent of Tenth District respondents reported that conditions were “very poor.” Comments mentioned increasing precarity among LMI populations due to rising prices and stagnating wages. Many comments stated concern around human services providers’ ability to meet the growing need while simultaneously facing declining funding from donations and government funds.

Internet and technology. Internet and technology respondents reported “poor” conditions, and most expected no change in conditions over the coming year. While Tenth District respondents’ expectations were similar to national respondents, a much larger share of respondents in the region reported “poor” or “very poor” conditions for internet and technology than in the nation overall. Respondents ranked the availability of subsidized internet and access to funding for technology as key negative factors in the sector (Table 1). Comments reinforced the rankings, with respondents stating they did not see conditions changing, as there was no longer significant funding and effort to improve internet and technology access. Comments also highlighted that while the cost of internet and technology has led many to solely rely on their cell phones for internet; respondents see continued challenges in people both meeting their needs through only a cell phone and in transitioning to jobs that require mouse and keyboard work.

Part 2: Health of LMI-Serving Organizations

Organizations reported good ability to serve their clients currently, even in the face of significantly increasing demand for services. However, they also reported significant funding challenges that are likely to impact their ability to serve into the future.

Ability to Serve

Nearly all organizations reported they were able to serve their communities well, but they were nearly evenly split on whether they would be able to serve their communities well into the next year (Chart 2). On a weighted basis, their top challenges to serving their communities were:

- Funding (43 percent ranked as the number one challenge)

- Rising expenses (11 percent)

- Adapting to uncertainty (17 percent)

Chart 2: Organizations’ current ability to serve was good but expected to moderate over the next year

Consistent with these top challenges, Chart 3 shows that most organizations have experienced declining funding, and nearly all have experienced rising expenses. Over 80 percent experienced increasing demand for their services, while 34 percent have experienced declining staffing levels. In sum, most organizations appear to be trying to do more with less.

Chart 3: Organizations reported having to do more with fewer resources

Funding and expenses also appear to be top challenges in these organizations’ ability to meet demand for services, staffing, and expenses. When asked about their biggest challenge in meeting demand for services, just over half of respondents cited funding, while 12 percent cited the increase in demand. Top challenges in staffing were not as skewed, with 23 percent reporting a lack of resources to open new positions, and 18 percent reporting difficulty maintaining staff. Finally, top challenges in wages and compensation included expenses (38 percent of respondents) and higher input costs (21 percent).

Funding

Organizations were about evenly split on whether they were experiencing financial stress, with 52 percent experiencing at least some stress (Chart 4). Organizations also reported mixed experiences with funding changes over the last year, with the exception of funds from the government (Chart 5). More organizations reported declining individual donations than increasing individual donations (47 percent versus 33 percent, respectively). Meanwhile, 73 percent reported decreased government funds. A nearly equal share of organizations relying on corporate donations, fees for services, and foundation funds either saw increased or decreased funding from those sources.

Chart 4: Just over half of organizations reported at least some financial stress

Chart 5: Government funding decreased for nearly every organization that relies on it

Note: Organizations were only asked to report changes to funding levels if it was one of their top three sources of funds.

About the Survey

The Community Conditions Survey surveys nonprofits, government agencies, and other organizations who assist low- and moderate-income (LMI) populations. Organizations are surveyed twice a year (spring and fall): the spring survey is sent out nationwide as the Community Perspectives Survey, and the fall survey is sent only to organizations within the Tenth Federal Reserve District, covering Colorado, Kansas, western Missouri, Nebraska, northern New Mexico, Oklahoma, and Wyoming. Tenth District respondents to the spring survey include but are not limited to those who respond to the fall survey due to the surveys’ different enrollment processes.

The spring 2025 Community Perspectives Survey was conducted from April 14 to May 23, 2025. The Kansas City Fed received 86 responses.

All survey respondents are asked to answer questions on conditions for economic mobility for the LMI populations they serve. Each respondent then has the opportunity to answer community conditions questions related to various topic areas depending on their organization’s involvement in those issues. The Community Perspectives Survey also includes a section of questions on the health of the organizations responding to the survey.

The national reports of the Community Perspectives Survey are available at FedCommunities.org:

External LinkCommunity report

External LinkHealth of Organizations report

About the Respondents

Steven Howland is a senior researcher in community development at the Federal Reserve Bank of Kansas City. The views expressed are those of the author and do not necessarily reflect the positions of the Federal Reserve Bank of Kansas City or the Federal Reserve System.

Author