Monitoring uncertainty around the future path of interest rates can help ensure that monetary policy is transmitting to the economy as intended. Because uncertainty is not directly observable, measuring uncertainty about the future policy rate can be difficult. Previous measures often face two key limitations. First, they may be released with a lag, making them less useful as a timely measure of policy rate uncertainty. Second, they may not be available over a long sample, making it difficult to compare measures of current uncertainty with historical context.

In this article, Brent Bundick, A. Lee Smith, and Luca Van der Meer introduce the Kansas City Fed’s Measure of Policy Rate Uncertainty (KC PRU), a timely, market-based measure that can help overcome these limitations. The KC PRU measures one-year-ahead uncertainty using the prices of financial options, which settle based on future short-term interest rates that tend to be highly correlated with the federal funds rate. By combining both historical and newly issued options, they calculate the measure at a daily frequency starting in the late 1980s. Overall, their analysis suggests the KC PRU provides a timely measure of policy rate uncertainty that appears to be consistent with both historical movements and recent macroeconomic developments.

Introduction

The outlook for interest rates has important implications for the economic decisions of households and businesses. For example, if households expect the Federal Reserve to lower its policy rate in the future, they may choose to finance a home with a variable-rate mortgage today, hoping for a lower interest rate in the future. Likewise, if businesses expect the Federal Reserve to increase interest rates in the future, they may pay down their variable-rate loans in advance to avoid rising interest expenses. However, uncertainty about the future path of interest rates can complicate this decision-making process. As a result, monitoring interest rate uncertainty can help ensure monetary policy is transmitting to the economy as intended.

Because uncertainty is not directly observable, measuring uncertainty about the future policy rate can be difficult. Previous studies examine several data sources to gauge uncertainty about future policy rates. However, these measures often face two key limitations. First, they may be released with a lag, making them less useful as a timely measure of policy rate uncertainty. Second, they may not be available over a long sample, making it difficult to compare measures of current uncertainty with historical context.

In this article, we introduce the Kansas City Fed’s Measure of Policy Rate Uncertainty (KC PRU), a timely, market-based measure that can help overcome these limitations. The KC PRU measures one-year-ahead uncertainty using the prices of financial options, which settle based on future short-term interest rates that tend to be highly correlated with the federal funds rate. We calculate our measure at a daily frequency, which allows us to examine how policy rate uncertainty responds to a policy announcement or macroeconomic development in real time. In addition, we combine information from both historical and newly issued options, which allows us to calculate our daily measure starting in the late 1980s and update it as more data become available.

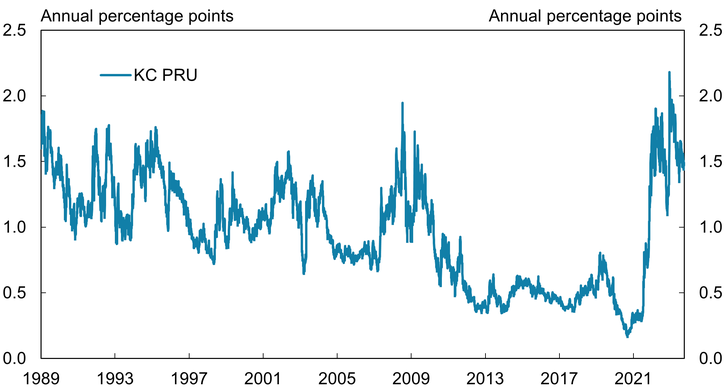

We evaluate this measure over time and show that changes in the KC PRU are correlated with changes in policymakers’ communication strategies as well as other macroeconomic and financial events. From 1989 until early 2020, our measure displays a downward trend in policy rate uncertainty, consistent with previous research arguing that increased communication and transparency from the FOMC over this period generally reduced uncertainty about its future policy rate. However, the KC PRU increases significantly as the economy emerges from the pandemic. According to our measure, the 2022–23 period marks the highest measure of policy rate uncertainty over the last three decades. Although several factors likely contributed to this recent rise in uncertainty, casual analysis suggests that uncertainty over the outlook for inflation, historically large increases in the funds rate, and regional banking stresses in March 2023, including the failure of Silicon Valley Bank, were important drivers of policy rate uncertainty during this period. Overall, our analysis suggests the KC PRU provides a timely measure of policy rate uncertainty that appears to be consistent with both historical movements and recent macroeconomic developments.

Section I describes the construction of the KC PRU and shows that the measure responds to changes in Federal Reserve communications about future policy rates as well as long-term trends, illustrating its potential usefulness as a measure of policy rate uncertainty. Section II highlights the significant increase in policy rate uncertainty during the post-pandemic economic recovery and highlights the KC PRU’s potential usefulness in monitoring policy uncertainty in real time.

I. Measuring Policy Rate Uncertainty

Researchers have previously attempted to gauge monetary policy uncertainty using several different methods, including textual analysis of newspaper articles or prices from financial markets. For example, Husted, Rogers, and Sun (2022) construct their Monetary Policy Uncertainty (MPU) index by counting the relative frequency of newspaper articles related to monetary policy uncertainty. Although this index is continually updated, it is only available at a monthly frequency. Bauer, Lakdawala, and Mueller (2022) also create a market-based measure of monetary policy rate uncertainty. However, their measure is only publicly available through the end of 2020 and thus unable to gauge uncertainty during and after the pandemic period.

The KC PRU has two key advantages over these existing measures. First, the KC PRU is available at a daily frequency, whereas the MPU index is only available monthly. As a result, the KC PRU can be used for event studies of financial market reactions to FOMC announcements, which are commonly used in empirical studies of macroeconomics._ Second, the KC PRU is available over a long horizon and is continually updated, whereas the measure by Bauer, Lakdawala, and Mueller (2022) is only available through the end of 2020. More specifically, the KC PRU is available for each business day beginning in 1989 and is updated regularly on the Kansas City Fed’s website.

Measuring policy rate uncertainty with options prices

To measure policy rate uncertainty on a daily basis, we construct the KC PRU from end-of-day options prices on futures contracts whose payoff depends on three-month interest rates one year in the future. These three-month interest rates tend to closely follow the federal funds rate—the rate at which banks make overnight loans to each other—which the Federal Open Market Committee (FOMC) targets as its primary policy tool. Thus, changes in the prices of these contracts are a good proxy for investors’ expectations of how the policy rate will evolve one year in the future.

To capture uncertainty, we examine the prices of both “put” options and “call” options on these contracts, which capture investors’ expectations of both higher and lower interest rates, respectively. Specifically, we use the same methodology as the Chicago Board of Exchange (Cboe) Volatility Index (VIX), which measures uncertainty about future returns on the S&P 500 equity price index. Using this method, we can combine the prices of put and call options on future interest rates into a single measure of uncertainty that captures the range of possible future rates rather than the likelihood that rates will move in one specific direction or the other. By using the VIX methodology, our measure technically captures uncertainty over future returns of holding interest rate futures contracts. However, Bundick, Herriford, and Smith (2024) show that applying the VIX method to interest rate options yields a measure that closely approximates interest rate uncertainty in percentage points. Thus, we report the KC PRU in annualized percentage points (see the appendix for additional details on the construction of the KC PRU)._

Options prices respond to key monetary policy announcements

Chart 1 plots the KC PRU for each business day from 1989 (which corresponds with the introduction of the options market for interest rate futures) through the end of 2023. This long horizon allows us to capture both daily changes in our measure of policy uncertainty in response to monetary policy announcements as well as longer-term trends.

Chart 1. The Kansas City Fed’s Measure of Policy Rate Uncertainty

Note: Chart spans April 1989 through December 2023.

Sources: Federal Reserve Bank of Kansas City and Chicago Mercantile Exchange.

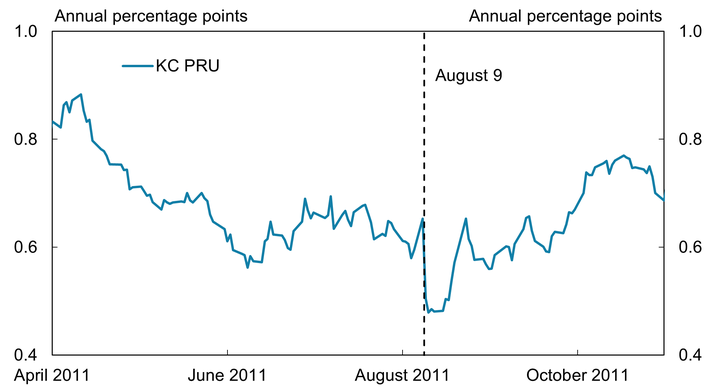

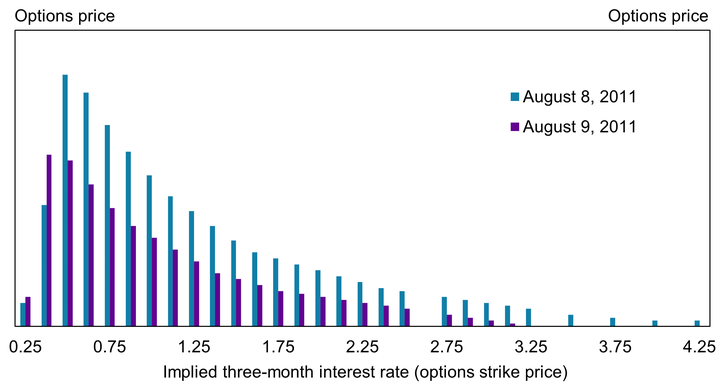

As one example of a daily change captured by the KC PRU, Panel A of Chart 2 shows that our measure of interest rate uncertainty changes significantly around August 9, 2011, when the FOMC released a statement with new forward guidance that conditions would likely warrant a low funds rate “through mid-2013.” This specific date-based language provided financial markets additional clarity about the path of possible interest rates; accordingly, the KC PRU fell dramatically. To more clearly illustrate this response, Panel B of Chart 2 shows changes in the options prices used to calculate the KC PRU from August 8, 2011—the day before the FOMC statement—to August 9, 2011. On August 8, the current federal funds rate remained near zero. However, options prices (blue bars) suggested that market participants were somewhat uncertain about the outcomes for short-term interest rates in one year. The policy announcement on August 9 provided additional clarity about future interest rates by communicating that the federal funds rate was highly likely to remain low throughout the year. As a result, options prices after the announcement (purple bars) on almost all strike prices fell significantly, reflecting a decline in uncertainty. These lower options prices feed through to the KC PRU, which fell from 0.65 to 0.50 on the day of the policy announcement—a significant one-day change (Panel A).

Chart 2. Policy Rate Uncertainty and Options Prices before and after August 9, 2011 Forward Guidance

Panel A: KC PRU, April through October 2011

Panel B: Options Prices, August 8 and 9, 2011

Notes: The bars in Panel B are the settlement prices of options as denoted by their strike price on the x-axis. Because these data are proprietary, y-axis labels are not included.

Sources: Federal Reserve Bank of Kansas City and Chicago Mercantile Exchange.

Options prices illustrate longer-run trends

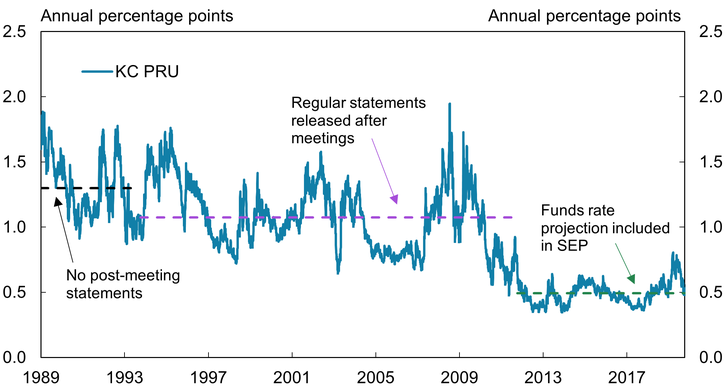

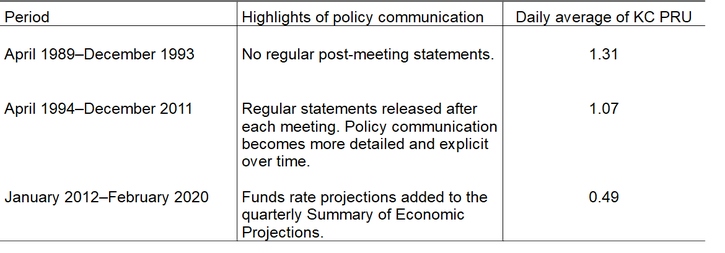

In addition to analyzing daily changes in response to macroeconomic events, the KC PRU can be used to assess longer-run trends in policy rate uncertainty over time. Previous research by Swanson (2006) as well as Bundick and Herriford (2017) argues that longer-term changes in policy rate uncertainty correlate with changes in longer-term communication strategies by monetary policymakers. Swanson shows that option-implied measures of policy rate uncertainty (similar to the KC PRU) fell when the FOMC chose to start issuing regular statements after each change in the federal funds rate in 1994. Before then, market participants had to infer changes in the policy rate from market interest rates, which likely increased uncertainty around the current and future stance of policy.

Building on this idea, Bundick and Herriford (2017) argue that the 2012 introduction of interest rate projections to the quarterly Summary of Economic Projections (SEP) provided additional guidance about future interest rates, which led to a further reduction in uncertainty about future policy rates. This research suggests that longer-term changes in communication strategies by policymakers during the 1989–2019 period were likely one factor that led policy uncertainty to trend lower.

To help illustrate these longer-term trends, Chart 3 plots the KC PRU and its average value over the periods 1989–93, 1994–2011, and 2012–19. After averaging around 1.3 percentage points from 1989–93, average policy rate uncertainty dropped from 1994–2011 (coinciding with the introduction of post-meeting FOMC statements) and dropped further from 2012–19 (coinciding with the addition of interest rate forecasts to the SEP).

Chart 3: Policy Rate Uncertainty and Changes in FOMC Communication Strategies

Note: Chart spans April 1989 through December 2019.

Sources: Federal Reserve Bank of Kansas City and Chicago Mercantile Exchange.

Basic statistical analysis highlights that these changes in policy rate uncertainty are statistically and economically important. Table 1 highlights that the average value of the KC PRU declined over these three sample periods. This finding reinforces the results in Swanson (2006) as well as Bundick and Herriford (2017), which generally highlight a declining trend in policy rate uncertainty over the 1989–2019 period. These longer-term trends suggest that increased monetary policy transparency and enhancements to central bank communications reduced uncertainty about the future path of policy before the pandemic.

Table 1: Average Policy Rate Uncertainty over Time

Sources: Board of Governors of the Federal Reserve System and Federal Reserve Bank of Kansas City.

II. Evolution of Policy Rate Uncertainty during and after the Pandemic

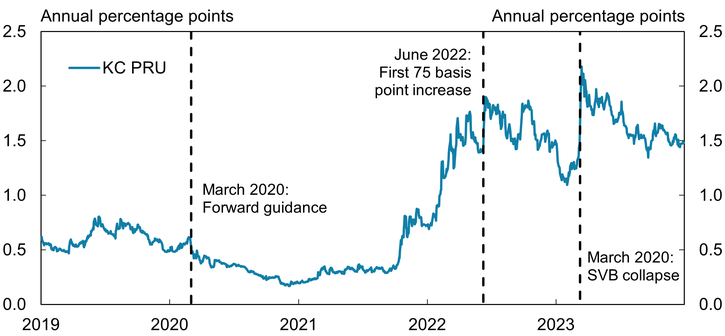

While prior research has examined historical movements in policy rate uncertainty, these analyses end prior to the onset of the pandemic. Because the KC PRU will be updated as new data become available each day, it can analyze more recent outcomes in policy rate uncertainty. Indeed, the KC PRU shows that the relatively steady longer-run decline in policy rate uncertainty changed rapidly both during and immediately after the pandemic. Policy rate uncertainty hit both its all-time low and high during the 2020–23 period (see Chart 1). To further analyze these developments, Chart 4 zooms in on the evolution of the KC PRU from 2019 through 2023. On March 3, 2020, the FOMC significantly lowered the federal funds target rate to offset the risks to economic activity posed by COVID-19. On March 15, the Committee lowered the funds target to its effective lower bound, stating that it expected “to maintain this target range until it is confident that the economy has weathered recent events and is on track to achieve its maximum employment and price stability goals.” In its September 2020 statement, the Committee refined its guidance, projecting that “it will be appropriate to maintain this target range until labor market conditions have reached levels consistent with the Committee’s assessments of maximum employment and inflation has risen to 2 percent and is on track to moderately exceed 2 percent for some time.”

Chart 4: Policy Rate Uncertainty during and after the Pandemic

Notes: Chart spans January 2019 through December 2023. Vertical lines denote March 3, 2020; June 6, 2022; and March 13, 2023.

Sources: Federal Reserve Bank of Kansas City and Chicago Mercantile Exchange.

This guidance about future rates, coupled with an economic backdrop of high unemployment and low inflation, led to expectations that the federal funds rate would remain near zero for several years. For example, the median projection in the December 2020 SEP signaled that the funds rate would remain near zero through the end of 2023. With rates pinned near zero and communications from the FOMC indicating they would likely remain there for several years, the range of potential interest rate outcomes over the next year was perceived to be historically narrow._ Indeed, Chart 4 shows that at the end of 2020, the KC PRU hit an all-time low of less than 0.2 percentage points.

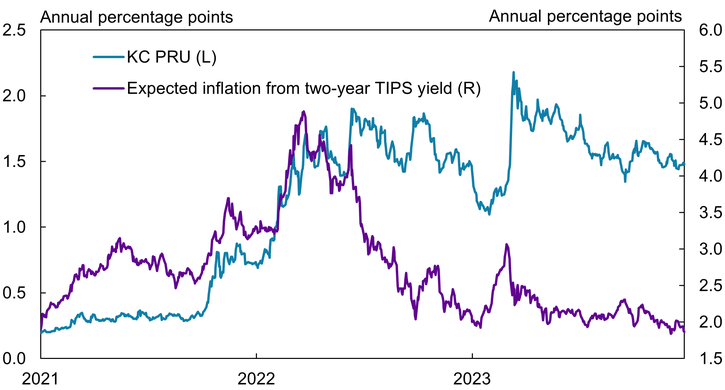

In 2021, however, inflation unexpectedly picked up as demand quickly recovered and the economy’s capacity to produce was hampered by supply bottlenecks and a reduced labor supply. The rapid rise in inflation and uncertainty over its underlying dynamics likely contributed to an increase in uncertainty around future inflation. Consistent with this interpretation, the KC PRU began to rise steadily in November 2021 and continued to climb during the first half of 2022. Given the FOMC’s mandate to achieve stable prices, an increase in uncertainty about future inflation likely transmitted to uncertainty about the appropriate stance of future policy. Although we cannot calculate an exact inflation-based counterpart to the KC PRU, as no liquid market exists for options on future inflation, we can compare our measure to yields on two-year Treasury Inflation Protected Securities (TIPS), which provide a market-based measure of expected inflation over the next two years. Chart 5 shows that increases in yields on two-year TIPS (purple line) corresponded to an increase in the KC PRU (blue line)._ Given that expected inflation and policy rate uncertainty rose together in late 2021 and early 2022, uncertainty about the inflation outlook could be an important factor in explaining the KC PRU’s historically high level in early 2022. However, Chart 5 shows that the KC PRU moved significantly higher in June 2022 even as inflation expectations started to decline from their peak.

Chart 5. Policy Rate Uncertainty and Market-Based Expected Inflation

Sources: Federal Reserve Bank of Kansas City, Chicago Mercantile Exchange, and Board of Governors of the Federal Reserve System.

A second factor that may help explain the early 2022 increase in policy uncertainty is the historically large increases in the federal funds rate in 2022. During the previous two tightening cycles, which began in 2004 and 2015, the FOMC increased the funds rate in increments of 25 basis points, typically at a measured pace. In response to elevated levels of inflation in 2022, however, the FOMC increased the funds rate by 50 and then 75 basis point increments throughout the year. These large changes in the federal funds rate likely imply a mechanical increase in one-year-ahead policy rate uncertainty. Intuitively, if market participants believe that larger changes in the policy rate are possible at each meeting, then uncertainty over the path of rates would accumulate over the following year, leading to more uncertainty about the future rate path.

The movements in the KC PRU around the June 2022 FOMC meeting provide some support for this idea. The June 2022 Survey of Primary Dealers (conducted around June 6) shows that market participants expected a 50 basis point increase in the federal funds rate at the conclusion of the June FOMC meeting (Federal Reserve Bank of New York 2022). Moreover, movements in futures markets suggest that markets expected interest rate increases to continue throughout the year, with short-term rates ending modestly above 3 percent by June 2023.

However, the FOMC chose to increase the federal funds target by 75 basis points on June 15, 2022, the largest single-meeting increase in the last three decades. While markets raised expectations for the future path of policy following the meeting, one-year-ahead policy rate uncertainty also increased dramatically. More specifically, the KC PRU rose from 1.60 on June 10 to 1.78 on June 15 after the FOMC announcement._

Policy rate uncertainty began to slowly trend down over the second half of 2022. In March 2023, however, several regional banks began to experience financial stress and runs on their unsecured deposits. These strains ultimately caused the failure of Silicon Valley Bank (SVB) on March 10, 2023. The KC PRU climbed significantly on the day of the SVB collapse (see Chart 4), suggesting that this banking stress and its implications for the policy outlook may be another factor leading to the elevated policy rate uncertainty during that time. A few weeks after the SVB collapse, the FOMC’s meeting statement also acknowledged uncertainty about how the stresses in the banking industry would affect the flow of credit to households and firms and broader economic activity, which highlights the KC PRU’s ability to measure uncertainty in real time.

The increased uncertainty about the inflation outlook, the rapid increases in the funds rate, and the failure of Silicon Valley Bank were likely some, but not all, of the factors that led to higher policy rate uncertainty during the 2022–23 period. Although policy rate uncertainty as measured by the KC PRU began to fall somewhat during the end of 2023, it remained elevated relative to its historical values, suggesting market participants remained uncertain about the exact path of policy required to restore price stability.

Conclusion

Quantifying uncertainty about the future path of policy rates is important in understanding how policy changes transmit to the economy. In this article, we introduce the Kansas City Fed’s Measure of Policy Rate Uncertainty (KC PRU). Our goal is to provide both the historical data and regular updates to this series to help policymakers and researchers measure and study policy rate uncertainty. For policymakers, our measure could provide a useful gauge for the efficacy of their communications about the likely future path of policy as well as how investors perceive the risk and uncertainty around that path. For researchers, our daily measure of interest rate uncertainty could be used to construct high-frequency monetary policy surprises by conducting event studies around monetary policy announcements. As recent work by Bundick, Herriford, and Smith (2024) shows, measures of interest rate uncertainty like the KC PRU can better illustrate the macroeconomic effects of monetary policy announcements.

Technical Appendix: Calculation of the KC PRU

To calculate the Kansas City Fed’s Measure of Policy Rate Uncertainty (KC PRU), we follow the VIX methodology from the Chicago Board Options Exchange. This method was originally developed to measure expected volatility on the S&P 500 equity price index._ The VIX formula below allows us to aggregate the prices of various put and call options on future short-term interest rates to derive our measure of policy uncertainty. Specifically, the formula uses out-of-the-money options, which means that if an option were to expire today, it would have no value. Thus, these out-of-the-money options are informative about the future implied volatility of interest rates since their prices depend on expected future volatility.

We calculate the KC PRU using the generalized formula below:

where T is the time to expiration, R is the risk-free interest rate, F is the option-implied forward price, K0 is the first strike equal or otherwise immediately below the option-implied forward price, Ki is the strike price of the call or put option, Q(Ki) is its current trading price, and ΔKi = (1/2) × (Ki+1 – Ki−1) is the distance between the strike prices above and below i. For simplicity, we set R = 0 in our calculations.

Our goal is for the KC PRU to measure one-year-ahead uncertainty about future short-term interest rates. However, options in our sample most often trade for settlement in March, June, September, and December of a given year. Therefore, we linearly interpolate the computed variances for horizons slightly less than and slightly longer than a one-year horizon to arrive at a one-year constant maturity index. After interpolating, we take the square root and scale by 100 to arrive at our final KC PRU.

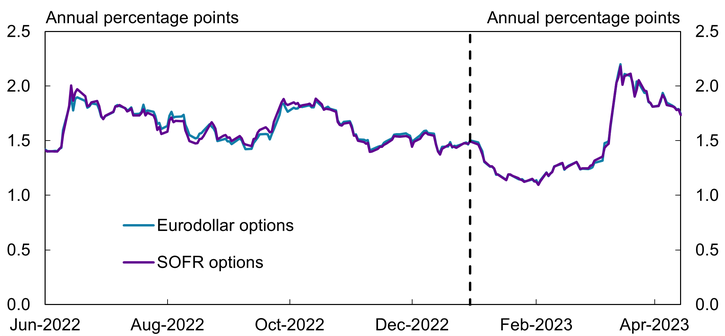

Prior to January 1, 2023, we use options on Eurodollar futures in our KC PRU calculation, which settle based on unsecured and survey-based London Interbank Offer Rate (LIBOR). However, the LIBOR market officially closed in June 2023 following issues with survey manipulation. After that date, we use options on the market-based Secured Overnight Financing Rate (SOFR)._ Chart A-1 shows the resulting implied volatility calculations using both the Eurodollar options and options on the SOFR over a sample in 2022 and the middle of 2023 (a period in which both options are available). The chart shows that the calculations are almost identical over the overlapping sample, suggesting that we can use a simple splicing method to generate a longer-consistent time series. Therefore, for simplicity, we choose to change data sources for the KC PRU at the beginning of 2023._

Chart A-1. Calculating the KC PRU with Eurodollar and SOFR Options

Source: Federal Reserve Bank of Kansas City.

Endnotes

-

1 The daily frequency similarly advantages the KC PRU over measures of interest rate uncertainty constructed from survey data measuring disagreement across forecasters (cross-sectional dispersion).

-

2 At a high level, the magnitude of the KC PRU can be thought of as the uncertainty around one-year-ahead interest rates. A higher value for policy rate uncertainty implies that market participants see a wider range of future outcomes.

-

3 The range of projections from the December 2020 SEP shows no disagreement across participants for the appropriate federal funds rate at the end of 2021.

-

4 Survey-based measures of inflation uncertainty from households and firms also rose generally around the same time.

-

5 This outcome contrasts starkly with most FOMC announcements in which uncertainty tends to fall on average (see Bauer, Lakdawala, and Mueller 2022).

-

6 For more information, see Cboe (2023).

-

7 One mechanical difference in calculating the KC PRU using SOFR rather than Eurodollar options is that SOFR contracts expire the Friday before the third Wednesday of the expiry month, whereas Eurodollar options expire two business days before the third Wednesday of the expiry month. This difference is trivial but important to incorporate when calculating the expiry horizons on each trade day.

-

8 Recent work by Acosta, Brennan, and Jacobson (2024) illustrates how to combine Eurodollar and SOFR futures to measure changes in the path of policy rate expectations around FOMC announcements. However, because SOFR options settle into a future that still has three months to expiration, we do not make any timing adjustments when we change from Eurodollar to SOFR options.

Publication information: Vol. 109, no. 7

DOI: 10.18651/ER/v109n7BundickSmithVanderMeer

References

Acosta, Miguel, Connor M. Brennan, and Margaret M. Jacobson. 2024. “Constructing High-Frequency Monetary Policy Surprises from SOFR Futures.” Economics Letters, vol. 242, no. 111873. Available at External Linkhttps://doi.org/10.1016/j.econlet.2024.111873

Bauer, Michael D., Aeimit Lakdawala, and Philippe Mueller. 2022. “Market-Based Monetary Policy Uncertainty.” Economic Journal, vol. 132, no. 644, pp. 1290–1308. Available at External Linkhttps://doi.org/10.1093/ej/ueab086

Board of Governors of the Federal Reserve System. 2021. “FOMC Statement.” Press release, March 17.

———. 2020a. “FOMC Projection Materials.” Press release, December 16.

———. 2020b. “FOMC Statement.” Press release, September 16.

———. 2020c. “FOMC Statement.” Press release, March 15.

———. 2011. “FOMC Statement.” Press release, August 9.

Bundick, Brent, and Trenton Herriford. 2017. “How Do FOMC Projections Affect Policy Uncertainty?” Federal Reserve Bank of Kansas City, Economic Review, vol. 102, no. 2, pp. 5–22. Available at External Linkhttps://doi.org/10.18651/ER/2q17BundickHerriford

Bundick, Brent, Trenton Herriford, and A. Lee Smith. 2024. “The Term Structure of Monetary Policy Uncertainty.” Journal of Economic Dynamics and Control, vol. 160, no. 104803. Available at External Linkhttps://doi.org/10.1016/j.jedc.2023.104803

Cboe (Chicago Board Options Exchange). 2023. “Volatility Index Methodology: Cboe Volatility Index.” November.

Federal Reserve Bank of New York. 2022. “Survey of Primary Dealers.” June.

Husted, Lucas, John Rogers, and Bo Sun. 2022. “Monetary Policy Uncertainty.” Journal of Monetary Economics, vol. 115, pp. 20–36. Available at External Linkhttps://doi.org/10.1016/j.jmoneco.2019.07.009

Swanson, Eric T. 2006. “Have Increases in Federal Reserve Transparency Improved Private Sector Interest Rate Forecasts?” Journal of Money, Credit and Banking, vol. 38, no. 3, pp. 791–819. Available at External Linkhttps://doi.org/10.1353/mcb.2006.0046

The authors thank the Center for Advancement of Data and Research in Economics (CADRE) at the Federal Reserve Bank of Kansas City for providing essential computational resources that contributed to developing the KC PRU. The authors also thank CADRE software engineers Jacob Dice, Frank Tsay, and Greg Woodward for valuable technical expertise.

Authors

Brent Bundick

Vice President