Buy now, pay later (BNPL) services have become increasingly popular in the United States over the past decade, especially among both younger and financially vulnerable consumers. Although BNPL services may help some consumers manage financial constraints by breaking down purchases into smaller installments and providing access to interest-free credit, the smaller, interest-free installments may also lead some consumers to perceive purchases as more affordable than they really are, increasing the risk of overspending, debt accumulation, and even default.

Fumiko Hayashi and Aditi Routh examine the financial constraints and repayment behavior of BNPL users, using the 2023 Survey of Household Economics and Decisionmaking (SHED) to create financial constraint indicators. They find that BNPL users tend to be more financially vulnerable relative to BNPL nonusers, consistent with previous studies. Their results also suggest a high correlation between consumers who make late payments on BNPL loans and those experiencing financial vulnerability or distress, implying that some BNPL users with late payments may have overspent or overextended their debt through BNPL.

Article Citation

Hayashi, Fumiko, and Aditi Routh. 2025. "Financial Constraints Among Buy Now, Pay Later Users." Federal Reserve Bank of Kansas City, Economic Review, vol. 110, no. 4. Available at External Linkhttps://doi.org/10.18651/ER/v110n4HayashiRouth

Introduction

Over the past decade, U.S. consumers have increasingly adopted buy now, pay later (BNPL) services, which are generally defined as short-term, interest-free loans repaid in a fixed number of installments over a fixed period. Indeed, consumer surveys suggest that 14 percent to 25 percent of U.S. consumers used BNPL services in 2023. These services have become particularly popular among both younger and financially vulnerable consumers, as BNPL loans have become increasingly available at merchants and require only a soft credit check that does not factor into a consumer’s credit score.

Whether BNPL services improve or harm a consumer’s financial situation is an open question. BNPL services may help assist consumers in managing financial constraints by breaking down purchases into smaller installments and providing access to interest-free credit, especially to consumers who may not qualify for traditional credit products. However, the smaller, interest-free installments may also lead some consumers to perceive purchases as more affordable than they really are, increasing the risk of overspending, debt accumulation, and even default.

In this article, we examine the financial constraints and repayment behavior of BNPL users. Specifically, we create financial constraint indicators using the 2023 Survey of Household Economics and Decisionmaking (SHED) and assess (1) whether BNPL users are more likely to face financial constraints than BNPL nonusers and (2) whether BNPL users with late payments are more likely to have indicators of financial constraints than BNPL users without late payments. Our results suggest BNPL users tend to be more financially vulnerable relative to BNPL nonusers, consistent with previous studies. Our results also suggest a high correlation between consumers who make late payments on BNPL loans and those experiencing financial vulnerability or distress, implying that some BNPL users with late payments may have overspent or overextended their debt through BNPL.

Section I provides an overview of the BNPL market. Section II discusses the benefits and risks of BNPL services for consumers. Section III examines to what extent BNPL users face financial constraints relative to BNPL nonusers and whether the extent varies by BNPL users’ repayment behavior of BNPL loans.

I. Overview of the BNPL Market

BNPL services are short-term loans that allow consumers to purchase goods and services and pay off the balance in a fixed number of installments over a fixed period. The most common BNPL structure is called “4-in-6” or “pay-in-four,” in which consumers pay for a purchase in four equal, interest-free installments: The first installment is paid at the time of purchase, and the remaining installments are paid in three two-week cycles._ Although BNPL services are typically interest-free, consumers may be charged late fees or penalties if they fail to comply with the terms of repayment.

BNPL services are increasingly available at merchants both online and in-person. Consumers are generally presented with BNPL services as a payment option at checkout, though the availability of BNPL options may be advertised prior to checkout. After a consumer chooses BNPL, the next steps vary depending on whether the consumer is a first-time or returning user of the BNPL provider. If the consumer is a first-time user, they set up an account at the BNPL provider and select a payment method for repayment, such as a credit card, debit card, or direct debit to a bank account via automated clearinghouse (ACH)._ The BNPL provider runs a soft credit check that verifies information such as the consumer’s credit history, age, and salary and then uses alternative data such as the consumer’s shopping profile to determine their loan eligibility and credit limit. If, on the other hand, the consumer already has an account with the BNPL provider, the provider verifies whether the consumer has sufficient unused credit to complete the purchase. After this verification, the consumer proceeds with their purchase. The BNPL provider typically sets three repayment dates and will automatically debit the consumer’s account on those dates._ However, consumers can cancel auto-repayments by contacting their banks or negotiate with their BNPL providers for other repayment options (National Consumer Law Center 2024).

The BNPL market has evolved since BNPL services were first introduced in the United States in the 2010s. Initially, most BNPL providers were fintechs—such as Affirm, AfterPay, Klarna, PayPal, Sezzle, and Zip. Today, these fintechs remain prominent BNPL providers, but more recently, different types of BNPL providers have entered the market. Card networks such as Mastercard and Visa have developed BNPL products and enabled card-issuing banks to offer these products to their cardholders. Similarly, some credit card-issuing banks such as Citi and J.P. Morgan Chase have created their own BNPL products, which let their cardholders pay off purchases through fixed-amount payments over time (Alcazar and Bradford 2021a)._

Initially, BNPL services were offered primarily as payment options through online merchants; however, more recently, in-person stores as well as merchants in the travel and healthcare services sectors have started offering BNPL options (Alcazar and Bradford 2021b)._ BNPL services are most common for purchases of clothing, consumer electronics, home appliances, and luxury items such as jewelry (Sharma 2024). Although BNPL loans for groceries are less common, their use has increased since inflation surged in 2021 (PYMNTS 2024b). The transaction value of purchases made using BNPL services has trended up since 2021 as well. Worldpay, a large payment processing company, finds that BNPL accounted for 4 percent of e-commerce purchase value and 1 percent of in-person purchase value in North America in 2021; these percentages are projected to reach 9 percent and 2 percent, respectively, in 2025 (Worldpay 2022). The number and variety of merchants who offer BNPL services as payment options are increasing more rapidly as BNPL providers partner with large wallet providers (such as Cash App) and merchant payment processors (such as Stripe) (Business Wire 2025; PYMNTS 2025a).

As BNPL services have become increasingly available at a wider range of merchants, the number of consumers who use BNPL services has also increased. The share of U.S. consumers who used BNPL services in 2023 varies by consumer survey, ranging from 14 percent in SHED to almost 20 percent in two surveys conducted by the Federal Reserve Banks of New York and Philadelphia, respectively, to 25 percent in an online survey conducted by the Harris Poll on behalf of NerdWallet. Despite these variances, the surveys commonly find that the share has been trending up in the past few years (Aidala, Mangrum, and van der Klaauw 2023; Akana and Zeballos Doubinko 2024; Federal Reserve Board 2024; Renter 2024)._ In addition, several studies suggest that adoption or use rates of BNPL services are higher for millennial and Gen Z consumers as well as for financially vulnerable or distressed consumers—for example, those with low credit scores, those who were recently rejected on a credit application, and those who are racial or ethnic minorities (Aidala, Mangrum, and van der Klaauw 2023; Akana and Zeballos Doubinko 2024; CFPB 2023; Gdalman, Greene, and Celik 2022; Larrimore and others 2024). These groups of consumers may benefit by having access to BNPL loans, provided the services do not increase their vulnerability to financial risks.

II. Benefits and Risks of BNPL Services for Consumers

BNPL services offer three main benefits to consumers: accessible credit, predetermined repayment schedules, and convenience comparable to credit cards. First, BNPL loans are more accessible than credit cards in both their payment terms and their application criteria. BNPL loans are typically interest-free if the repayment period is three months or shorter, while credit card loans may be interest-free for only one month, provided cardholders pay the previously billed amount in full. BNPL loans also require only a soft credit check, which has no effect on a consumer’s credit score and allows for loans to be approved even if the consumer has no credit history. In contrast, credit card loans use a hard credit check, which requires the consumer to have a credit score and can also negatively affect it. In these ways, BNPL’s less stringent application criteria and more generous payment terms may help ease financial constraints among consumers, especially those who have had difficulty accessing credit in the past.

Second, the predetermined repayment schedules of BNPL loans may help consumers to budget. Unlike credit card debt, for which consumers make their own repayment plans, BNPL services have structured repayment schedules that consumers can follow. In addition, BNPL’s biweekly repayments may better allow consumers to match their cash inflows with outflows, especially if the payment schedule is aligned with the consumer’s paydays (PYMNTS 2023).

Third, BNPL services are seen as convenient by their users (Aidala, Mangrum, and van der Klaauw 2024; Akana and Zeballos Doubinko 2024; Federal Reserve Board 2024). BNPL services are readily available at many merchants, and the application process is typically fast, adding little friction to the checkout process. Although BNPL services are currently not as widely accepted by merchants as credit cards, this gap is likely to narrow, as the number and variety of merchants that offer BNPL options has been increasing rapidly.

While these benefits have made BNPL services attractive to many consumers, BNPL services may also expose consumers to three key risks: overspending and overextending debt, high costs from missed or late BNPL repayments, and complications regarding refunds and disputes comparable to credit cards._ First, consumers using BNPL services may risk overspending and overextending their debt, as the smaller, interest-free installments may make some purchases seem more affordable than they really are. Adding to this risk is that consumers can make multiple purchases with a BNPL provider up to a predetermined credit limit and can also use BNPL services from multiple providers._ Because BNPL providers typically do not share their customers’ credit limits with credit bureaus or other BNPL providers, each BNPL user’s summed credit limit across multiple providers could be more than their ability to repay. In contrast, credit limits for credit cards are reported to credit bureaus, and credit card issuers determine their potential customers’ credit limits based on the customers’ income, credit score, repayment history, and total amount of debt._ As a result, credit card issuers may deny consumers access to additional credit if a consumer already has substantial debt relative to their income.

Second, consumers who miss BNPL payments or who make them late may incur substantial costs from penalties and fees across multiple channels. For example, if BNPL users do not have auto-repayments set up and miss their repayment schedules, they may incur costs through late fees or penalties assessed by the BNPL providers (CFPB 2024a)._ Even if BNPL users have auto-repayments set up, they could incur overdraft or non-sufficient funds (NSF) fees from their banks if they do not have sufficient funds to cover these auto-repayments. In addition, if a BNPL user makes auto-repayments through a credit card and the BNPL repayments add to the card’s unpaid balance, the user may incur interest charges on the credit card. Together, late fees, penalties, and overdraft or NSF fees could be as high as interest charges on credit cards (National Consumer Law Center 2024). Unlike credit cards, a single missed or late BNPL repayment may not lower the consumer’s credit score._ However, if BNPL users fall substantially behind their repayment schedules, their unrepaid loans may be turned over to debt collectors who do report the debt to credit bureaus, thereby hurting their credit scores.

Third, BNPL services have complicated return and dispute processes, making some BNPL users less able to return items or dispute transactions. To address this complexity, the Consumer Financial Protection Bureau (CFPB) adopted a new interpretive rule in May 2024 requiring BNPL providers to provide the same dispute rights and protections to consumers that credit card issuers provide, including protection against errors, limited liability for unauthorized use, and a right to withhold payment for problematic purchases (CFPB 2024b; National Consumer Law Center 2024). More recently, however, the CFPB has signaled its plan to revoke this interpretive rule (PYMNTS 2025b).

The benefits and risks of BNPL services may be especially salient for consumers who face financial constraints. These consumers are less likely to be able to access credit through traditional means, making BNPL services potentially attractive; however, some of these consumers may be more likely to miss repayments or seek returns, making them more exposed to BNPL services’ risks. Whether the benefits offset the risks depends on how these consumers use BNPL services.

III. The Extent to Which BNPL Users Face Financial Constraints

BNPL services have several features that may make them more attractive to consumers with financial constraints—though they could also worsen constraints for these customers. To help quantify the benefits and risks, we first confirm whether BNPL users in general are indeed more likely to be financially constrained. We then examine whether BNPL users who make late payments for BNPL loans are more likely to be financially constrained. Late payments for BNPL loans could be a sign of overspending, overextension of debt, or a heightened default risk, especially among BNPL users who also face severe financial constraints.

To assess the degree to which BNPL users are financially constrained, we use data from the SHED, an annual consumer survey conducted by the Board of Governors of the Federal Reserve System with a weighted sample that is nationally representative (Federal Reserve Board 2024). About 14 percent of U.S. adult consumers surveyed in the 2023 SHED had used BNPL services in the past 12 months. Because the Federal Reserve Board conducts the SHED to monitor the financial circumstances of U.S. households, with a particular emphasis on understanding how low- and middle-income individuals are faring, the SHED contains many variables that indicate financial constraints.

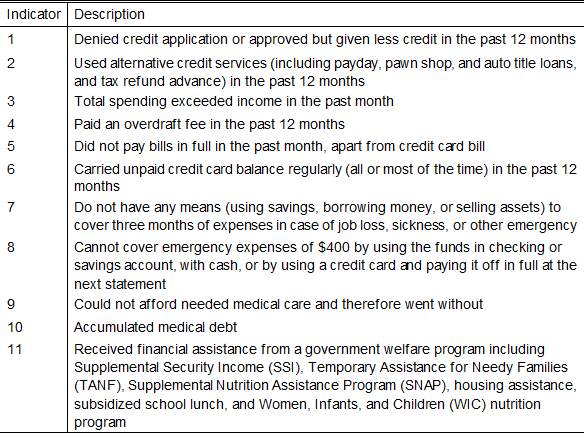

We create 11 financial constraint indicators from variables that indicate credit or liquidity constraints, listed in Table 1. Although a few indicators are related to either credit or liquidity constraints, most indicators are related to both constraints. For example, the first indicator, “denied credit application or approved but given less credit in the past 12 months” is related to credit constraints, while the third indicator, “the total spending exceeded income in the past month” is likely related to liquidity constraints. The fourth indicator, “paid an overdraft fee in the past 12 months” may be related to both constraints: Consumers who paid an overdraft fee may have experienced an income or expenditure shock or may not have been able to access credit to meet their credit needs.

Table 1: Financial Constraint Indicators

Some of the 11 indicators may be related to each other but differ in severity. For example, both the seventh and eighth indicators are related to covering emergency expenses, but the eighth indicator, which refers to the consumer’s inability to cover an emergency expense of $400 with cash or cash-equivalent means, is likely a more severe constraint than the seventh indicator, which refers to the consumer’s inability to cover three months of expenses. Similarly, while the ninth and tenth indicators are both related to medical expenses, the tenth indicator, which indicates medical debt, likely reflects a more severe constraint than the ninth indicator, which indicates the consumer has skipped needed medical care due to lack of money.

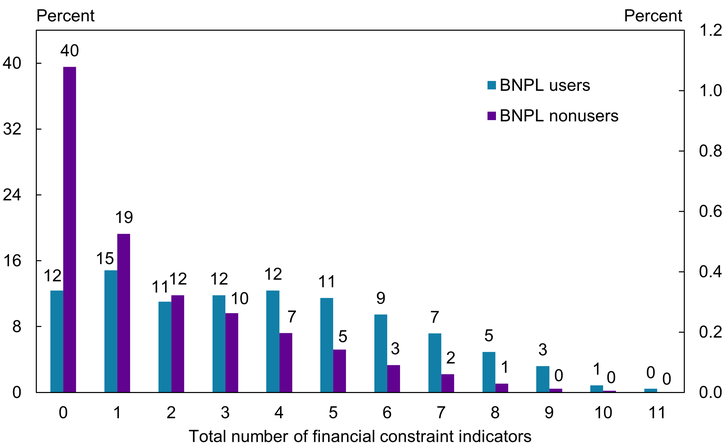

We use these indicators to examine whether BNPL users are more likely to face financial constraints than BNPL nonusers in large part to verify that the 2023 SHED data provide the same results as several previous studies. Specifically, we calculate the total number of financial constraint indicators each consumer has and then assess how consumers are distributed across the total numbers of indicators from zero (those who have no indicators) to 11 (those who have all indicators) for BNPL users and nonusers, respectively._

BNPL users are significantly more likely to face financial constraints than BNPL nonusers. Chart 1 shows that only 12 percent of BNPL users have no indicator of financial constraint (blue bar) compared with 40 percent of nonusers (purple bar). Moreover, nearly half of BNPL users have four or more indicators of financial constraints, while 80 percent of nonusers have three indicators or fewer.

Chart 1: BNPL Users Are More Likely to Face Financial Constraints Than Nonusers

Sources: Board of Governors of the Federal Reserve System and authors’ calculations.

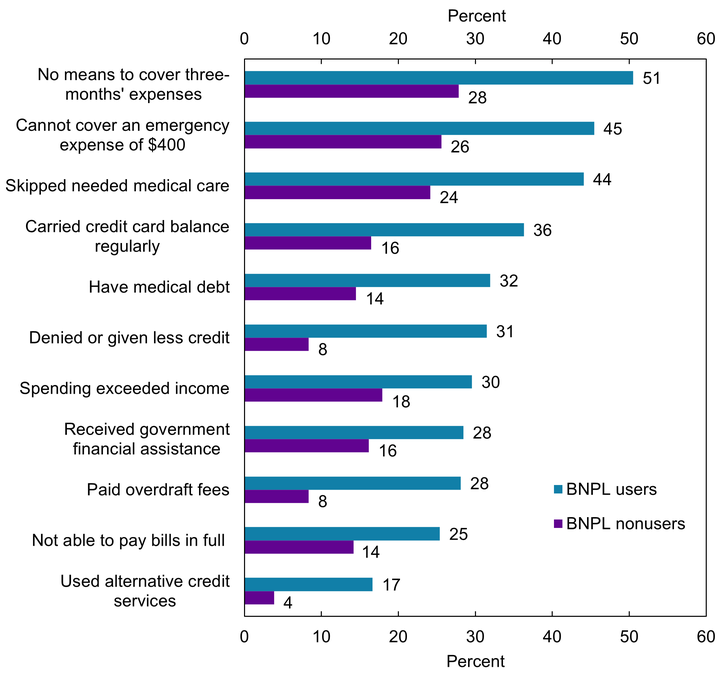

BNPL users are also more likely to have any given financial constraint indicator than BNPL nonusers. Chart 2 shows the (weighted) shares of BNPL users and BNPL nonusers who have a given indicator, with the 11 indicators listed from most to least common among BNPL users. For all 11 indicators, the share of consumers with a given indicator is higher for BNPL users (blue bars) than for BNPL nonusers (purple bars). For example, while the most common indicator for both BNPL users and nonusers is “no means to cover three-months’ expenses,” the share of BNPL users with that indicator is nearly twice as high as that of nonusers (51 percent versus 28 percent). Similarly, the least common indicator for both BNPL users and nonusers is “used alternative credit services,” but the share of BNPL users with that indicator is more than four times the share of BNPL nonusers (17 percent versus 4 percent). Together, both Charts 1 and 2 suggest BNPL users are more likely to face financial constraints than BNPL nonusers, confirming results from previous studies using different data sources.

Chart 2: BNPL Users Are More Likely to Have a Given Financial Constraint Indicator Than BNPL Nonusers

Sources: Board of Governors of the Federal Reserve System and authors’ calculations.

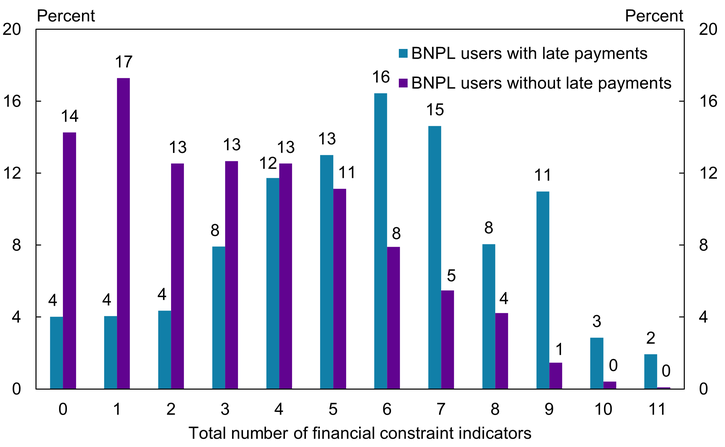

We next assess whether BNPL users who made late payments on their loans are more likely to face financial constraints. In particular, we assess the total number of financial constraint indicators that BNPL users with and without late payments face. About 18 percent of all BNPL users made at least one late payment in 2023. These late payments may be especially concerning if they are concentrated among users with greater financial constraints, as these users may be less able to recover from the financial penalties.

We find a high correlation between consumers who make late payments on BNPL loans and those who have a higher number of financial constraint indicators. Chart 3 shows that only 4 percent of BNPL users with late payments have no indicator of financial constraints (blue bar), compared with 14 percent of BNPL users without late payments (purple bar). In other words, 96 percent of BNPL users with late payments have at least one financial constraint indicator, and we consider them at least mildly financially constrained. Moreover, while only 32 percent of BNPL users with late payments have four or fewer financial constraint indicators, nearly 70 percent of BNPL users without late payments have four or fewer indicators.

Chart 3: BNPL Users with Late Payments Are More Likely to Have a Higher Number of Financial Constraint Indicators

Sources: Board of Governors of the Federal Reserve System and authors’ calculations.

The total number of indicators BNPL users face can proxy for the severity of a consumer’s financial constraints. Particularly, we consider BNPL users who have nine or more indicators to be facing severe financial constraints. More than 15 percent of BNPL users with late payments fall into this category, compared with less than 2 percent of BNPL users without late payments.

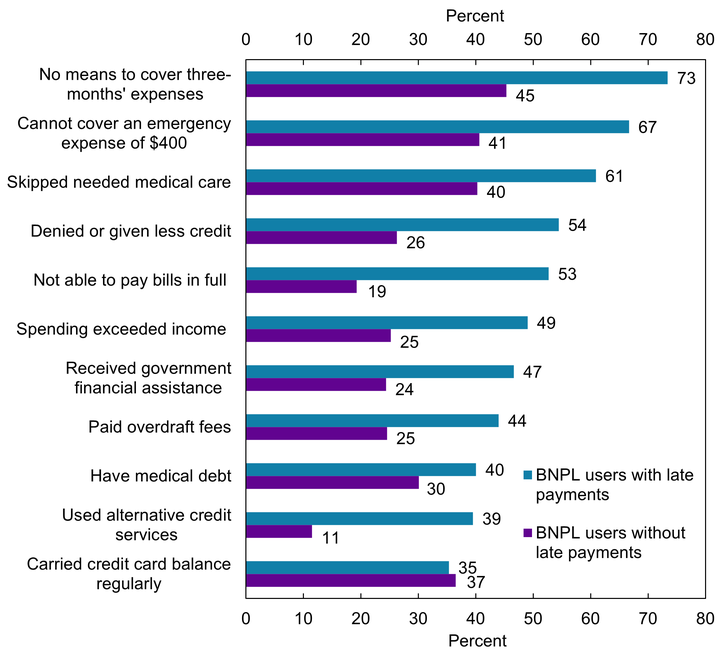

As suggested by their greater total number of indicators, BNPL users with late payments are more likely to have almost any given financial constraint indicator than BNPL users without late payments. Chart 4 shows that for all but one indicator (“carried credit card balance regularly”), the share of BNPL users with late payments (blue bars) is higher than the corresponding share of BNPL users without late payments (purple bars). The lower share of the credit card balance indicator among BNPL users with late payments is partly explained by the group’s lower credit card ownership rate relative to the group of BNPL users without late payments. If we account for credit cardholders only, the share of those who regularly carried credit card balances actually becomes slightly higher for BNPL users with late payments than for BNPL users without late payments (49 percent versus 43 percent)._

Chart 4: BNPL Users with Late Payments Are More Likely to Have Almost Any Financial Constraint Indicator Than BNPL Users Without Late Payments

Sources: Board of Governors of the Federal Reserve System and authors’ calculations.

Conclusion

U.S. consumers have increasingly adopted BNPL services over the past decade. These services have been particularly popular among millennial and Gen Z consumers as well as financially vulnerable consumers. As more consumers use BNPL services more frequently, researchers and policymakers have tried to understand the benefits and risks these services may pose for consumers. Although several studies report that financially vulnerable or distressed consumers are more likely to use BNPL services than financially healthy consumers, little research has examined how financial vulnerability and distress varies among BNPL users.

We find that the vast majority of BNPL users who made late payments for BNPL loans (96 percent) are at least mildly financially constrained compared with BNPL users who did not make late payments (86 percent). Moreover, we find that 15 percent of BNPL users with late payments are severely financially constrained compared with only 2 percent of BNPL users without late payments. Our results suggest a high correlation between BNPL users’ late payments and their financial vulnerability or distress, potentially implying that BNPL users with late payments may have overspent or overextended their debt through BNPL. Some of these users may even have a heightened default risk. However, many BNPL users, especially those without late payments, may use BNPL to help ease their financial constraints; if consumers use BNPL service as a substitute for alternative credit services or credit cards, they can reduce or avoid high costs or interest charges.

Endnotes

-

1 Many BNPL providers also offer longer-term loans (three months or longer), which may charge interest ranging from zero to nearly 30 percent of the annual percentage rate (Gill 2023).

-

2 Some BNPL providers and some credit card issuers do not allow their customers or cardholders to use a credit card as a repayment payment method for BNPL loans. Some BNPL providers allow their customers to use a credit card but charge a convenience fee for the credit card use. The level of convenience fee could be as high as 3 percent of the purchase value.

-

3 Some BNPL providers allow their customers to choose repayment dates in two-week intervals, for example, to align with the customer’s pay days (O’Shea 2023).

-

4 Consumers use general-purpose credit card-linked installment plans to cover the larger average purchase amount at $2,095, compared with the average purchase amount of $926 for BNPL (PYMNTS 2024a).

-

5 Alcazar and Bradford (2021b) discuss how merchants benefit from offering BNPL services as payment options. Berg and others (2024) find the benefits of offering BNPL outweigh the costs for a German e-commerce company.

-

6 CFPB (2025) finds that during 2022, 21 percent of consumers with a credit record used the BNPL services of at least one of six examined fintech BNPL providers at least once.

-

7 In addition to these three risks, the CFPB (2022) identifies risks of data harvesting and monetization. Many BNPL providers build a valuable digital profile of each user’s shopping preferences and behavior, which may threaten consumers’ privacy, security, and autonomy. Identity fraud is another risk. Because BNPL loans are not reported to credit bureaus, an individual may be unaware that their name is fraudulently used to establish and use BNPL loans (Alcazar and Bradford 2021a).

-

8 The CFPB (2025) finds that at some point during 2022, 63 percent of BNPL users had simultaneous loans at any firm and 33 percent of BNPL users had simultaneous loans at different firms.

-

9 Consumer debt from BNPL loans is unlikely to be reflected in the total amount of debt calculated on consumers’ credit report because BNPL providers may not share their customers’ debt with credit bureaus.

-

10 Several BNPL providers (including Afterpay and Klarna) charge a late fee up to 25 percent of the total purchase amount or a fixed amount.

-

11 A good repayment record on credit cards improves consumers’ credit scores, while such a record on BNPL may not, as BNPL providers often do not report their users’ repayment behavior to credit bureaus. Some BNPL providers partner with credit bureaus to submit eligible users’ repayment behavior to the credit bureau to help build their credit files and improve their credit scores (Sezzle 2021)

-

12 We calculate the weighted share of BNPL users (or nonusers) who have a given number of indicators.

-

13 About 72 percent of BNPL users with late payments owned a credit card compared with 85 percent of BNPL users without late payments.

Article Citation

Hayashi, Fumiko, and Aditi Routh. 2025. "Financial Constraints Among Buy Now, Pay Later Users." Federal Reserve Bank of Kansas City, Economic Review, vol. 110, no. 4. Available at External Linkhttps://doi.org/10.18651/ER/v110n4HayashiRouth

Publication information: Vol. 110, no. 4

DOI: 10.18651/ER/v110n4HayashiRouth

References

Aidala, Felix, Daniel Mangrum, and Wilbert van der Klaauw. 2024. “How and Why Do Consumers Use ‘Buy Now, Pay Later’?” Federal Reserve Bank of New York, Liberty Street Economics, February 14.

———. 2023. “Who Uses ‘Buy Now, Pay Later’?” Federal Reserve Bank of New York, Liberty Street Economics, September 26.

Akana, Tom, and Valeria Zeballos Doubinko. 2024. “4-in-6 Payment Products—Buy Now, Pay Later: Insights from New Survey Data.” Federal Reserve Bank of Philadelphia, Consumer Finance Institute, February 22.

Alcazar, Julian, and Terri Bradford. 2021a. “The Rise of Buy Now, Pay Later: Bank and Payment Network Perspectives and Regulatory Considerations.” Federal Reserve Bank of Kansas City, Payments System Research Briefing, December 1.

———. 2021b. “The Appeal and Proliferation of Buy Now, Pay Later: Consumer and Merchant Perspectives.” Federal Reserve Bank of Kansas City, Payments System Research Briefing, November 10.

Berg, Tobias, Valentin Burg, Jan Keil, and Manju Puri. 2024. “The Economics of ‘Buy Now, Pay Later’: A Merchant’s Perspective.” National Bureau of Economic Research, working paper no. 33152, November. Available at External Linkhttps://doi.org/10.3386/w33152

Business Wire. 2025. “Cash App Begins Roll Out of Afterpay’s Pay Over Time Offering at Hundreds of Thousands of Merchants.” March 17.

CFPB (Consumer Financial Protection Bureau). 2025. “Consumer Use of Buy Now, Pay Later and Other Unsecured Debt.” January.

———. 2024a. “Do Buy Now, Pay Later (BNPL) Loans Have Fees?” Last modified September 4.

———. 2024b. “CFPB Takes Action to Ensure Consumers Can Dispute Charges and Obtain Refunds on Buy Now, Pay Later Loans.” May 22.

———. 2023. “Consumer Use of Buy Now, Pay Later: Insights from the CFPB Making Ends Meet Survey.” CFPB Office of Research Publication no. 2023-1, March.

———. 2022. “CFPB Study Details the Rapid Growth of ‘Buy Now, Pay Later’ Lending.” September 15.

Federal Reserve Board (Board of Governors of the Federal Reserve System). 2024. “Economic Well-Being of U.S. Households in 2023.” May.

Gdalman, Hannah, Meghan Greene, and Necati Celik. 2022. “Buy Now, Pay Later: Implications for Financial Health.” Financial Health Network, March.

Gill, Lisa L. 2023. “New Buy Now, Pay Later Loans Come with More Risks.” Consumer Reports, July 20.

Larrimore, Jeff, Alicia Lloro, Zofsha Merchant, and Anna Tranfaglia. 2024. “‘The Only Way I Could Afford It’: Who Uses BNPL and Why.” Board of Governors of the Federal Reserve System, FEDS Notes, December 20. Available at External Linkhttps://doi.org/10.17016/2380-7172.3675

National Consumer Law Center. 2024. “New Rights for Buy Now, Pay Later Purchases.” December 2.

O’Shea, Bev. 2023. “How to Pay Off Your Buy Now, Pay Later Purchases.” Experian, September 7.

PYMNTS. 2025a. “Stripe Enables Merchants to Instantly Offer Klarna Payment Options.” January 14.

———. 2025b. “CFPB Signals It Will Drop Rule to Treat BNPL Providers Like Credit Card Companies.” March 27.

———. 2024a. “Buy Now, Pay Later Special Report: New Data: Defining the New Buy Now, Pay Later Consumer.” June.

———. 2024b. “Consumer Embrace BNPL for Groceries Amid Rising Food Costs.” June 12.

———. 2023. “BNPL Used as Budgeting Tool, Especially by Millennials, Says Sezzle CEO.” August 3.

Renter, Elizabeth. 2024. “2024 State of Consumer Credit Report.” NerdWallet, May 28.

Sezzle. 2021. “Sezzle Expands Partnership with TransUnion.” PR Newswire, October 14.

Sharma, Niketan. 2024. “Comprehensive BNPL Statistics Across the Globe.” Nimble AppGenie, June 14.

Worldpay. 2022. “The Global Payments Report for Financial Institutions and Merchants.” FIS, Worldpay.

Fumiko Hayashi is a vice president at the Federal Reserve Bank of Kansas City. Aditi Routh is an economist at the bank. The views expressed are those of the authors and do not necessarily reflect the positions of the Federal Reserve Bank of Kansas City or the Federal Reserve System.

Authors

Fumiko Hayashi

Vice President