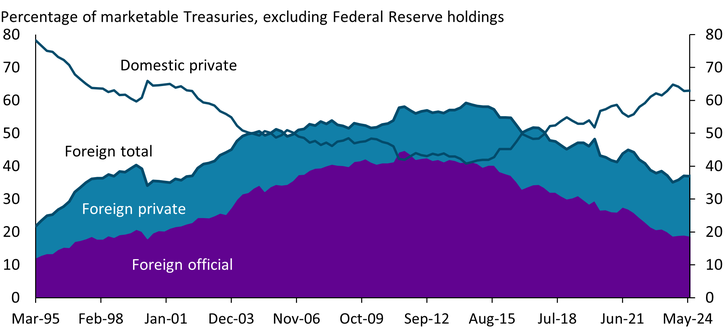

Between 1995 and 2010, the foreign ownership share of the Treasury market grew from about 20 percent to nearly 60 percent of publicly available securities. Chart 1 shows that this accumulation was driven by a substantial increase in foreign official holdings (purple area). This buildup occurred on the back of increased bond supply from U.S. fiscal and private sector net borrowing, which was met with increased foreign official (government) demand for foreign exchange reserves.

Chart 1: Marketable U.S. Treasury holdings since 1995

Sources: U.S. Department of the Treasury (Haver Analytics) and Treasury International Capital (TIC) System (Board of Governors of the Federal Reserve System).

Since the end of the global financial crisis (GFC), however, the footprint of foreign governments in the Treasury market has waned significantly, and with it the overall market share of foreign investors. This gradual decline in foreign market share, combined with recent increases in Treasury yields and emerging commentary about the attractiveness of dollar assets, has brought the role of foreign investors in the Treasury market into sharp focus. Despite the declining market share of foreign investors, their footprint is still large enough that even a passive decrease in foreign demand could be influential for yields.

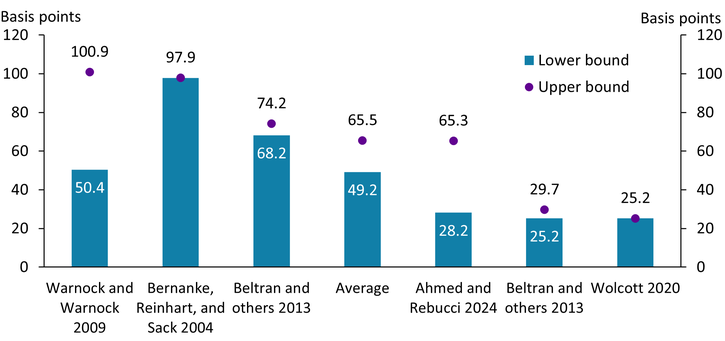

Chart 2 summarizes results from available studies that use Treasury International Capital (TIC) data to estimate the effect of foreign Treasury purchases on yields. Available evidence suggests that a month-to-month Treasury liquidation of one standard deviation (about $141 billion or 1.87 percent of foreign holdings as of March 2025) would raise yields by an average of 57 basis points. The estimates across all studies, which consider a variety of maturities and flow concepts, range from a low of 25 basis points to a high of 101 basis points (Wolcott 2020; Warnock and Warnock 2009). For a sense of scale, a 50 basis point rise in yields would lie in the top 5 percent of historical monthly changes in 10-year Treasury yields, and an 80 basis point increase would lie in the top 1 percent of all observed changes.

Chart 2: Estimated effect of a one standard deviation Treasury sale on Treasury yields

Notes: Estimates reflect a range of sample dates, maturities, and aggregation methods. Two sets of estimates are included from Beltran and others (2013)—the larger value (a) reflects the estimated effect of flows, while the smaller value (b) reflects the estimated effect of holdings.

Sources: Warnock and Warnock (2009), Bernanke, Reinhart, and Sack (2004), Beltran and others (2013), Ahmed and Rebucci (2024), and Wolcott (2020).

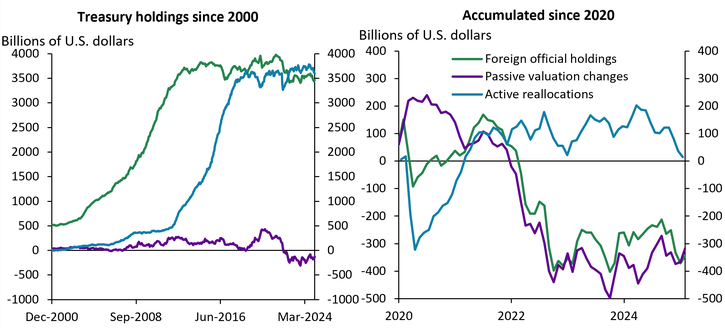

Measuring how foreign investors’ sales and purchases influence the price (and therefore yields) of U.S. Treasuries requires the quantity of transactions to be separated from the price of the securities. This separation produces changes in overall Treasury security holdings due to active reallocations (buying and selling), which are distinct from growth in holdings due to changes in the value of the asset._

This decomposition uncovers an important point—while active sales clearly carry consequences for the equilibrium yield on Treasuries, inaction from foreign investors also affects yields. The left and right panels of Chart 3 show how foreign official holdings (green line) have evolved since 2000 and since 2020, respectively, separating out the contributions to this change from active reallocations (cumulative flows, blue line) and passive valuation changes (purple line). The left panel shows that Treasuries began to accumulate rapidly on foreign official balance sheets starting in the 1990s. Since the spring of 2013, however, foreign official investors have held their allocation toward Treasuries (blue line) roughly stable, neither accumulating Treasuries nor offloading them. Thus, the dip in foreign holdings observed since 2020 is attributable almost entirely to valuation changes. Indeed, the right panel shows that the jump in Treasury issuance associated with pandemic-era fiscal stimulus was not met with a commensurate increase in Treasury demand from foreign official holders, contributing to the contemporaneous fall in accumulated value. This exercise underscores the notion that both sales and the absence of purchases carry implications for Treasury yields.

Chart 3: Changes in the value, not quantity, of Treasuries is responsible for the change in accumulated foreign official Treasury holdings since 2020

Source: TIC System (Board of Governors of the Federal Reserve System).

Since 2010, the composition of Treasury ownership has changed in meaningful ways, as foreign official holdings have given way to private (domestic and foreign) purchases. This change in the composition of Treasury demand is likely to have a profound effect on yields going forward, because official demand for Treasuries is less sensitive to changes in price (which translate into interest rates). Foreign official investors hold Treasuries because they value the securities’ settlement value for trade and other dollar denominated transactions. In contrast, private Treasury net purchases are motivated by yields and hedging value. Thus, waning foreign official demand for Treasuries shifts the burden of Treasury absorption onto economically motivated investors, who are more sensitive to rates. With a more rate-sensitive investor base, the same supply of Treasuries requires higher yields for markets to clear. In Part 2 of this Bulletin—Who’s Buying U.S. Treasuries?—Rajdeep Sengupta and Joshua A. Jacobs further explore how the composition of Treasury investors has shifted since the financial crisis.

In summary, foreign sales of U.S. Treasury securities have the potential to generate considerable volatility in Treasury markets. Empirical evidence suggests that a sufficiently large selloff has the potential to raise Treasury yields substantially. Part 2 of this Economic Bulletin will explore the consequences: Without stable, structural demand for Treasuries from foreign official participants, lower yields in the face of increased Treasury issuance will be difficult to sustain.

Endnotes

-

1 The best publicly available data for achieving this separation is the Treasury International Capital (TIC) system, which collects cross-border securities positions and transactions data on foreign official and private demand for U.S. Treasuries and other U.S. securities. Although the TIC system currently collects data separately on holdings of securities and on transactions, the Federal Reserve Board helpfully maintains a database that reconciles these two data sources using estimates of the valuation change (see Bertaut and Judson 2022).

Article Citation

Dilts Stedman, Karlye. 2025. "The Changing Investor Composition of U.S. Treasuries, Part 1: Foreign Treasury Sales Could Raise U.S. Yields." Federal Reserve Bank of Kansas City, Economic Bulletin, July 9.

References

Ahmed, Rashad, and Alessandro Rebucci. 2024. “External LinkDollar Reserves and U.S. Yields: Identifying the Price Impact of Official Flows.” Journal of International Economics, vol. 152, November.

Beltran, Daniel O., Maxwell Kretchmer, Jaime Marquez, and Charles P. Thomas. 2013. “External LinkForeign Holdings of U.S. Treasuries and U.S. Treasury Yields.” Journal of International Money and Finance, vol. 32, pp. 1120–1143.

Bernanke, Ben, Vincent Reinhart, and Brian Sack. 2004. “External LinkMonetary Policy Alternatives at the Zero Bound: An Empirical Assessment.” Brookings Papers on Economic Activity, vol. 2004, no. 2, pp. 1–100.

Bertaut, Carol, and Ruth Judson. 2022. “External LinkEstimating U.S. Cross-Border Securities Flows: Ten Years of the TIC SLT.” Board of Governors of the Federal Reserve System, FEDS Notes, February 18.

Krishnamurthy, Arvind, and Annette Vissing-Jorgensen. 2007. “External LinkThe Demand for Treasury Debt.” National Bureau of Economic Research, working paper no. 12881, January.

Warnock, Francis E., and Veronica Cacdac Warnock. 2009. “External LinkInternational Capital Flows and U.S. Interest Rates.” Journal of International Money and Finance, vol. 28, no. 6, pp. 903–919.

Wolcott, Erin L. 2020. “External LinkImpact of Foreign Official Purchases of U.S. Treasuries on the Yield Curve.” AEA Papers and Proceedings, vol. 110, May, pp. 535–540.

Karlye Dilts Stedman is a senior economist at the Federal Reserve Bank of Kansas City. The views expressed are those of the author and do not reflect the positions of the Federal Reserve Bank of Kansas City or the Federal Reserve System.

Author