During periods of financial stress, investors tend to shift toward safer assets. An asset is considered a safe haven if it is uncorrelated or negatively correlated with riskier assets during times of stress (Baur and Lucey 2010). Although U.S. government securities are often considered the quintessential safe haven against the stock market, previous studies have suggested that gold, too, has acted as a safe haven in the past._

In recent years, investors have questioned whether Bitcoin might function as a safe haven as well._ In theory, Bitcoin’s fixed supply and algorithm-based issuance allow it to be independent from traditional markets, which could make it a desirable asset in times of economic stress. Indeed, in a survey, many holders of Bitcoin stated they believed it to be similar to gold as opposed to stocks, U.S. dollars, or a “new technology” (Hundtofte, Lee, Martin, and Orchinik 2019). Consequently, the returns of other safe-haven assets may have changed after Bitcoin’s introduction.

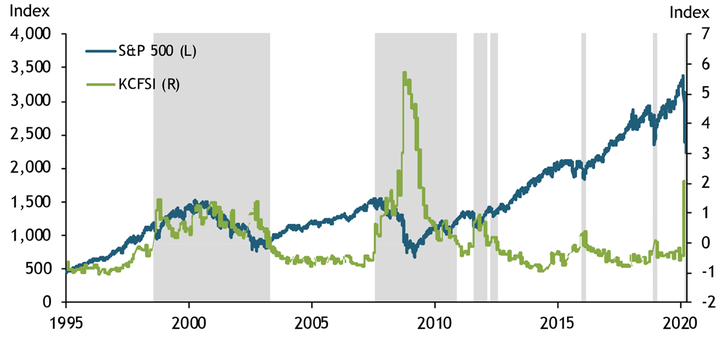

To assess how the 10-year Treasury note and gold behaved in periods of stress before and after the introduction of Bitcoin, we examine the correlations of their daily returns with the daily returns of the S&P 500, a diversified portfolio of large U.S. publicly traded companies that is commonly used as a proxy for risk asset performance. We examine these correlations from January 1995 through February 2020 to allow for a near-equivalent number of periods before and after the introduction of Bitcoin. In light of recent events, we also separately analyze correlations in March 2020, when the bull market ended amid concerns about the coronavirus pandemic. We separate the sample into periods in which financial stress was either above or below its long-term average using the Kansas City Financial Stress Index (KCFSI)._ Although assets are only considered safe havens in times of stress, we include periods without stress to capture any changes in asset behavior between the periods. Chart 1 shows that the KCFSI and S&P 500 index generally have an inverse relationship: over most of our sample, the KCFSI rises as the S&P 500 falls. The gray bars identify our periods of financial stress, which begin when the KCFSI (green line) rises above zero.

Chart 1: Periods of Financial Stress

Note: Gray bars indicate periods of stress.

Sources: Federal Reserve Bank of Kansas City and Bloomberg.

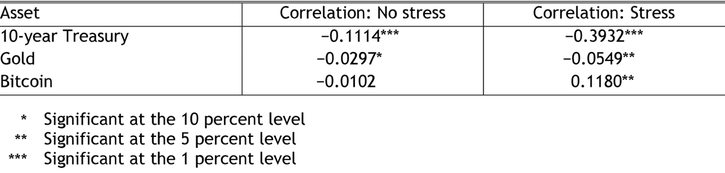

Table 1 shows the historic correlations of the 10-year Treasury, gold, and Bitcoin across the entire sample. Both the 10-year Treasury and gold have negative, statistically significant correlations with the S&P 500, suggesting both assets have the properties of safe havens. In contrast, Bitcoin has a weak positive correlation with the S&P 500 during periods of financial stress, suggesting Bitcoin behaves more like a risk asset than a safe haven.

Table 1: Historic Correlations with the S&P 500, 1995–2020

Source: Bloomberg.

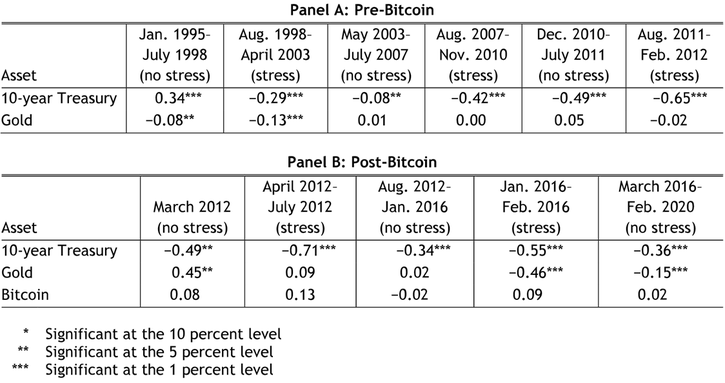

Table 2 breaks the full sample down into individual periods with or without financial stress and shows that the safe-haven properties of assets have varied over time. Panel A shows the correlations for gold and the 10-year Treasury before the introduction of Bitcoin, while Panel B shows the correlations after Bitcoin was introduced. As in Table 1, the 10-year Treasury consistently behaves like a safe haven: the correlations for the 10-year Treasury are negative and statistically significant across all stress periods._ In contrast, gold has only behaved like a safe haven in certain periods of financial stress. Finally, Panel B shows that Bitcoin has failed to exhibit the behaviors of a safe-haven asset—its correlations with the S&P 500 are not statistically significant in any period and positive in all but one._

Table 2: Historic Correlations with the S&P 500 in Varying Periods of Stress over Time

Sources: Federal Reserve Bank of Kansas City and Bloomberg.

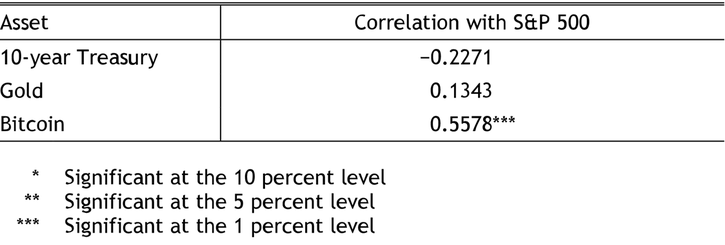

A natural question is whether the recent period of financial stress related to the coronavirus pandemic has altered these correlations. Table 3 shows that during March 2020, none of the assets exhibited statistically significant safe-haven behavior. The result for the 10-year Treasury is somewhat surprising, as it was a safe haven for every stress period from 1995 through February 2020, regardless of duration. Although its correlation with the S&P 500 in March 2020 is still negative, it is not statistically significant._ Gold has a positive but insignificant correlation, which is unsurprising given that it has not consistently demonstrated safe-haven properties across stress periods._ As in the full sample, Bitcoin has a positive, statistically significant correlation, suggesting it performed like a risk asset in March rather than a safe haven.

Table 3: Correlations with the S&P 500 in March 2020

Source: Bloomberg.

Overall, our results suggest that the 10-year Treasury has generally exhibited safe-haven behavior, gold has occasionally exhibited safe-haven behavior, and Bitcoin has never exhibited safe-haven behavior since its introduction. Moreover, the introduction of Bitcoin does not appear to have materially changed the safe-haven properties of government bonds or gold. Instead, Bitcoin at times appears to have behaved more like a risk asset than a safe haven.

Endnotes

-

1 He, Krishnamurthy, and Milbradt (2016) build a model to explain why U.S. government bonds exhibit this property. Coudert and Raymond (2011) find that gold qualifies as a safe haven.

-

2 Academics such as Baur, Dimpfl, and Kuck (2018) and Smales (2019) have asked this question, too.

-

3 To include Bitcoin in the sample, we do not use periods of extreme stress. As a robustness check, we also run the analysis using periods where stock markets fell more than 15 percent, 17.5 percent, and 20 percent and find nearly identical results to the main analysis using the KCFSI stress periods.

-

4 Using a t-test, we find the difference between the higher and lower stress periods to be statistically significant.

-

5 Although uncorrelated assets may be classified as safe-haven assets, none of the near-zero correlations are statistically significant.

-

6 The correlation is still negative even though it is not statistically significant. The lack of significance could be due to the volatility within this short sample period.

-

7 This result could also be due to the volatility within this short sample period.

References

Baur, Dirk G., Thomas Dimpfl, and Konstantin Kuck. 2018. “External LinkBitcoin, Gold and the US Dollar–A Replication and Extension.” Finance Research Letters, vol. 25, pp. 103–110.

Baur, Dirk G., and Brian M. Lucey. 2010. “External LinkIs Gold a Hedge or a Safe Haven? An Analysis of Stocks, Bonds External Linkand Gold.” Financial Review, vol. 45, no. 2, pp. 217–229.

Coudert, Virginie, and Hélène Raymond. 2011. “Gold and Financial Assets: Are There Any Safe Havens in Bear Markets?” Economics Bulletin, vol. 31, no. 2, pp. 1613–1622.

He, Zhiguo, Arvind Krishnamurthy, and Konstantin Milbradt. 2016. “External LinkWhat Makes US Government Bonds Safe Assets?” American Economic Review, vol. 106, no. 5, pp. 519–523.

Hundtofte, Sean, Michael Junho Lee, Antoine Martin, and Reed Orchinik. 2019. “External LinkDeciphering Americans’ Views on Cryptocurrencies.” Federal Reserve Bank of New York, Liberty Street Economics (blog), March 25.

Smales, Lee A. 2019. “External LinkBitcoin as a Safe Haven: Is It Even Worth Considering?” Finance Research Letters, vol. 30, pp. 385–393.

Jesse Leigh Maniff is a payments specialist at the Federal Reserve Bank of Kansas City. Sabrina Minhas is a former assistant economist at the bank. David Rodziewicz is a senior commodity specialist at the bank. Becca Ruiz is a research associate at the bank. The views expressed are those of the authors and do not necessarily reflect the positions of the Federal Reserve Bank of Kansas City or the Federal Reserve System.

Author