During and after the global financial crisis, asset purchase programs substantially increased the size and share of longer-term assets on the Federal Reserve’s balance sheet. These purchases were largely used to provide additional accommodation when the federal funds rate was constrained by its effective lower bound. The funds rate has since increased, and the FOMC has discussed reducing the size of its balance sheet. One question, however, is whether decreasing the balance sheet has the same effect on the economy as increasing the target federal funds rate.

One approach to quantifying the so-called substitutability of balance sheet policy and changes in the funds rate is to use a framework that allows balance sheet policy to affect the natural real federal funds rate, frequently referred to as r*. The natural rate provides a baseline that monetary policy makers often use to assess the stance of monetary policy. If the real funds rate is below r*, for example, then monetary policy is providing accommodation that tends to ease financial conditions and support economic growth. To the extent the FOMC can shape financial market conditions through changes in its balance sheet—and, in turn, r*—it could trade reductions in the balance sheet for increases in the target federal funds rate.

To explore this, Hakkio and Smith specify a model that links the Fed’s balance sheet to r* through the term premium. The term premium is the additional compensation investors require to lend money at longer horizons. When the Fed buys longer-term Treasury or agency mortgage-backed securities, the balance sheet expands; evidence indicates these purchases lower longer-term interest rates by lowering the term premium. Reductions in longer-term interest rates, in turn, often result in lower interest rates on mortgages and auto loans. In the Hakkio and Smith model, these lower rates raise r*, as the additional accommodation from the balance sheet reduces the accommodation needed from the funds rate. In other words, the Hakkio and Smith model predicts some substitutability between the funds rate and the balance sheet.

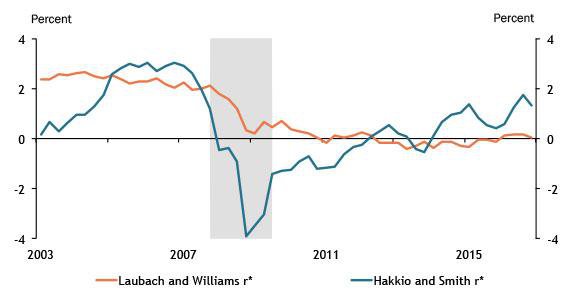

However, r* estimates are model dependent, as are measures of the term premium. To the extent economic models differ, so will measures of r*. As an example, Chart 1 shows estimates from Hakkio and Smith alongside a commonly cited measure of r* from Laubach and Williams._ This latter measure allows a broad array of factors to affect r* but does not explicitly incorporate the term premium. As a result, the Hakkio and Smith measure of r* rises by more than the Laubach and Williams measure in recent years, largely due to balance sheet policies that reduced the term premium.

Chart 1: Estimates of r* vary across different models

Note: Gray bar denotes National Bureau of Economic Research (NBER)defined recession.

Sources: Federal Reserve Bank of San Francisco (Haver Analytics), NBER (Haver Analytics), Hakkio and Smith, and authors’ calculations.

Presumably, reducing the balance sheet reverses some of the effects of expanding the balance sheet. Therefore, balance sheet reductions should raise the term premium and thereby raise long-term rates. Gagnon and others estimate that a decrease in the Fed’s balance sheet of 1 percent of gross domestic product, which would currently be about $190 billion, raises the term premium by about 4.4 basis points. Thus, by raising the term premium, reductions in the balance sheet would be expected to lower the Hakkio and Smith measure of r*. In terms of the magnitude, Hakkio and Smith estimate a 1 basis point increase in the term premium decreases r* by about 1 to 1.5 basis points. Intuitively, a lower r* reflects a higher term premium, as it captures that monetary policy is less accommodative even when the funds rate is unchanged.

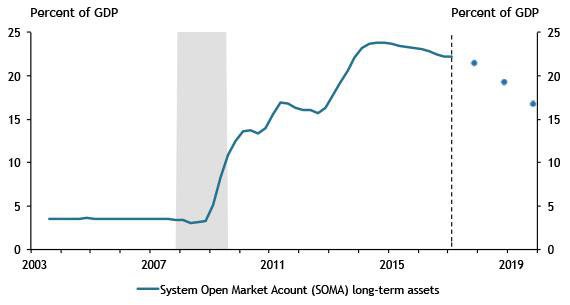

Chart 2: Hypothetical Fed balance sheet scenario

Note: Gray bar denotes NBER-defined recession.

Sources: Federal Reserve Bank of New York (Haver Analytics), Bureau of Economic Analysis (Haver Analytics), NBER (Haver Analytics) and authors’ calculations.

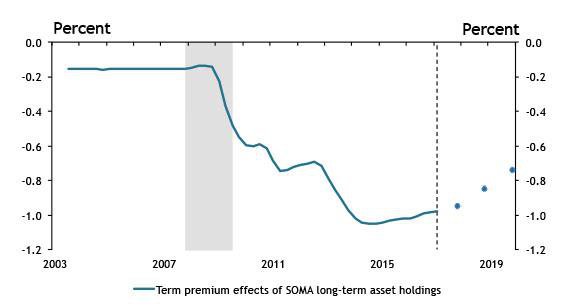

As the Fed contemplates possible reductions in its balance sheet, estimates of r* can quantify how much accommodation these reductions would remove. Though uncertain, Chart 2 illustrates one possible scenario for the balance sheet over the coming years._ In this scenario, the balance sheet declines by $675 billion through 2019. As it declines, the term premium is likely to rise. Chart 3 illustrates movements in the term premium due to the Fed’s longer-term asset holdings (based on the estimates of Gagnon and others), then shows projections of how the term premium will rise as holdings decline. This exercise suggests that due to balance sheet adjustments alone, the term premium could rise by about 25 basis points through the end of 2019_. According to the Hakkio and Smith model, this rise in the term premium would reduce r* by a similar magnitude—that is, by about 25 basis points. These changes are roughly equivalent to raising the funds rate by 25 basis points._

Chart 3: Balance sheet effects on the term premium

Sources: Federal Reserve Bank of New York (Haver Analytics), Bureau of Economic Analysis (Haver Analytics), NBER (Haver Analytics), and authors’ calculations.

However, estimates of the term premium’s effects on r* are highly uncertain. The 95 percent confidence bands around the estimate from Hakkio and Smith suggest the effect on r* could be as high as 75 basis points (assuming the term premium exerts a stronger influence on r*) or as low as 0 (assuming the term premium has little or no effect on r*)._

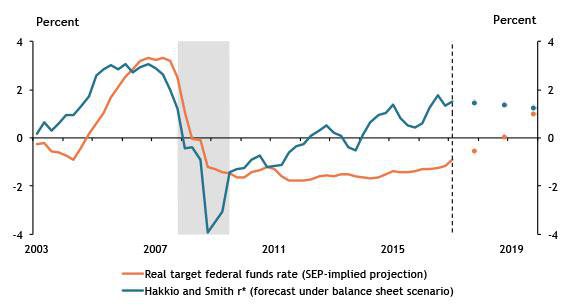

In addition to changes in the balance sheet, FOMC participants project changes to the funds rate in their Summary of Economic Projections (SEP). Chart 4 shows how SEP-implied adjustments to the real federal funds rate would evolve relative to r* under the balance sheet adjustment scenario in Chart 2. The chart shows r* declining modestly by about 25 basis points over the forecast horizon, as the real funds rate rises by almost 2 percentage points. Under this estimate of r*, monetary policy is currently accommodative and is likely to remain so for the next few years under a scenario of gradual balance sheet adjustment. Monetary policy isn’t expected to become neutral until 2019. However, the Hakkio and Smith estimate of r* is considerably higher than the Laubach and Williams estimate. When the actual federal funds rate reaches neutral depends not only on the size of the Fed’s balance sheet and the path of the funds rate but also on the underlying measure of the natural rate.

Chart 4: Projections of r* and the actual funds rate under balance sheet adjustment

Note: Gray bar denotes NBER-defined recession.

Sources: Board of Governors of the Federal Reserve System, NBER (Haver Analytics), Hakkio and Smith, and authors’ calculations.

Endnotes

-

1 The key difference between specifications are as follows: Laubach and Williams assume rt* = cgt + zt and Hakkio and Smith assume rt* = cgt + zt + ctptpt + crprpt' where gt is the growth rate of potential GDP, tpt is the 10-year term premium, rpt is a measure of the risk premium, and zt are unspecified factors. See Hakkio and Smith for additional details.

-

2 For alternatives, see Markets Group of the Federal Reserve Bank of New York or Bonis, Ihrig, and Wei.

-

3 Bonis, Ihrig, and Wei estimate the term premium will increase about 30 basis points from 2017 year-end until 2019 year-end in a scenario assuming slightly less of a decline in the balance sheet.

-

4 More precisely, assuming 4 percent annual nominal GDP growth from the 2017:Q1 level going forward, then -ctp x 4.4 x (B2019:Q4/Y2019:Q4 - B2017:Q4/Y2017:Q4) = —0.21 under the restricted model in Hakkio and Smith that sets ctp = —1 where B is the amount of longer-term assets held by the Fed, and Y is nominal GDP.

-

5 To get the upper bound of the 2 standard deviation confidence interval, this calculation assumes ctp = —1.55 ± 2 x 0.81 where 0.81 is the standard error around ctp estimated by Hakkio and Smith.

References

Bonis, Brian, Jane Ihrig, and Min Wei. 2017. “External LinkThe Effect of the Federal Reserve’s Securities Holdings on Longer-term Interest Rates.” Board of Governors of the Federal Reserve System, FEDS Notes, April 20.

Gagnon, Joseph, Matthew Raskin, Julie Remache, and Brian Sack. 2011. “External LinkThe Financial Market Effects of the Federal Reserve’s Large-Scale Asset Purchases.” International Journal of Central Banking, vol. 7, no. 1, pp. 3–43.

Hakkio, Craig S., and A. Lee Smith. 2016. “Bond Premiums and the Natural Rate of Interest.” Federal Reserve Bank of Kansas City, Economic Review, vol.102, no. 1, pp. 5–39.

Laubach, Thomas, and John C. Williams. 2003. “External LinkMeasuring the Natural Rate of Interest.” The Review of Economics and Statistics, vol. 85, no. 4, pp. 1063–1070.

Markets Group of the Federal Reserve Bank of New York. 2017. “External LinkDomestic Open Market Operations During 2016,” April.

Troy Davig is the senior vice president and director of research at the Federal Reserve Bank of Kansas City. A. Lee Smith is an economist at the bank. The views expressed are those of the authors and do not necessarily reflect the positions of the Federal Reserve Bank of Kansas City or the Federal Reserve System.

Author