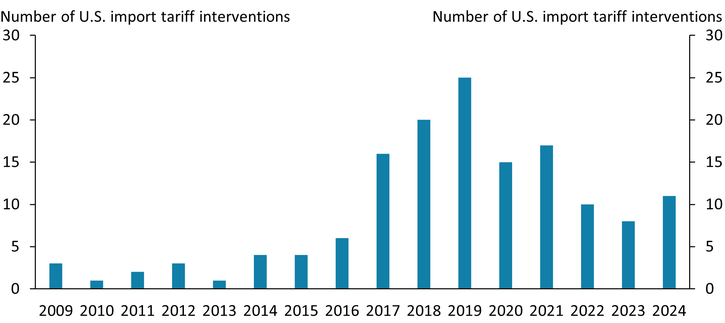

Over the last decade, the United States has implemented several new tariffs on goods from other countries. Chart 1 shows the number of import tariffs that the United States has implemented each year since the global financial crisis in 2007–08._ Since 2016, tariff interventions have risen substantially. On May 14, 2024, the White House announced new and expanded tariffs on roughly 7 percent of all U.S. imports from China, which are expected to roll out over the next two years.

Chart 1: The U.S. has implemented several new import tariffs over the last decade

Sources: Global Trade Alert and authors’ calculations.

Because tariffs make imported goods more expensive, they are generally thought to reduce the volume of imports. However, the actual effects on import volume can vary depending on how firms react to the tariff announcements. Some firms, for example, may attempt to “front-run” a tariff by increasing their inventories of an affected good before the tariff is implemented. This front-running produces a counterintuitive effect, as the affected good’s imports rise immediately after the tariff is announced. Determining whether firms are attempting to front-run tariffs requires us to look at individual goods rather than imports overall. Thus, we examine import dynamics for two goods categories for which tariffs were announced in May 2024 and implemented in September 2024: electric vehicle (EV) batteries and steel and aluminum.

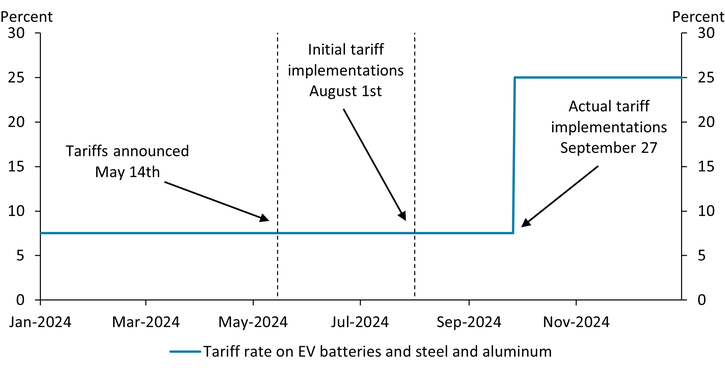

Front-running is a viable strategy for firms because tariffs take time to implement. Chart 2 depicts a timeline of tariffs on EV batteries and steel and aluminum from China in 2024. In May 2024, the White House announced that the tariff rate on both import goods categories would increase from 7.5 percent to 25 percent as of August 1, 2024. However, these tariffs were not actually implemented until September 27, 2024, giving importers four months to react to the announcement.

Chart 2: Tariffs on EV batteries and steel and aluminum from China increased noticeably in 2024

Source: Authors’ calculations.

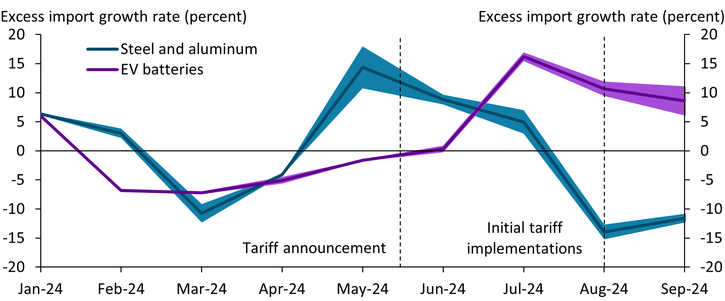

We estimate an event study model to assess whether imports of EV batteries and of steel and aluminum changed in response to the tariff announcement. Chart 3 shows price-adjusted import growth for EV batteries and for steel and aluminum from China around the announcement of the tariff relative to a trend based on imports from other U.S. trading partners (“excess import growth”)._ For example, if excess import growth is above zero, imports from China are growing more than predicted. The chart shows that growth rates for steel and aluminum imports from China (blue line) declined relative to imports from other trading partners following the announcement of the tariff. Thus, U.S. firms do not appear to have attempted to front-run tariffs on Chinese steel and aluminum. Imports for EV batteries from China, on the other hand, increased sharply after the tariff announcement (purple line). The increase is most pronounced in July, when excess imports from China increased by more than 15 percentage points. The response peaks two months after the tariff announcement, which reflects the time it takes to ship and produce additional orders.

Chart 3: Imports of EV batteries from China surged prior to tariff implementation, but imports of steel and aluminum did not

Note: Shaded areas represent 95 percent confidence intervals.

Sources: U.S. Census Bureau and authors’ calculations.

Why did importers front-run EV batteries from China but not steel and aluminum? Importers are likely to try to front-run tariffs if their imported products are 1) concentrated in the country subject to upcoming tariffs and 2) difficult to substitute or source from somewhere else. Both factors explain the different import patterns of EV batteries and of steel and aluminum following the 2024 tariffs.

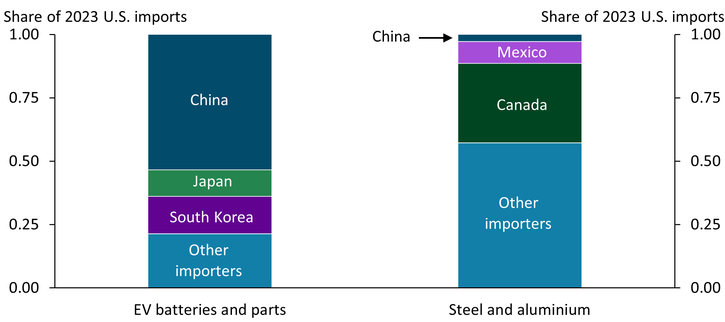

The United States imports most of its EV batteries from China but does not rely on China for steel and aluminum. Chart 4 shows that while more than half of all EV battery imports are sourced from China, a much smaller share of steel and aluminum imports come from China (dark blue bars). Indeed, the majority of U.S. imports come from other countries such as Canada, even though China is the single largest producer of steel and aluminum globally.

Chart 4: Most EV battery imports, but only a small share of steel and aluminum imports, are sourced from China

Sources: U.S. Census Bureau and authors’ calculations.

Although domestic production accounts for most U.S. consumption of both product categories, the United States does not have as much additional capacity to produce EV batteries to substitute for Chinese imports as it does for aluminum and steel (Department of Commerce 2024; International Energy Agency 2024). An EV battery costs at least 20 percent more to produce in the United States or another major U.S. trading partner than it does in China, making it cost inefficient to substitute away from Chinese batteries despite a roughly 20 percentage point increase in tariffs (International Energy Agency 2024). Moreover, China has only been operating at 40 percent of its production capacity, suggesting China can accommodate increased demand from U.S. importers. Lastly, because increasing the production capacity for EV batteries is both time- and cost-intensive, it is difficult to build production capacity elsewhere in a reasonable amount of time. These factors likely encouraged importers to front-run tariffs for batteries.

In contrast, steel and aluminum products are widely available domestically and from other countries (Congressional Research Service 2022). Thus, instead of front-running, it seems more likely that steel and aluminum importers would respond to the newly announced tariffs by substituting imports from China with imports from another country or, alternatively, domestically produced steel and aluminum.

Our analysis highlights that the extent to which importers front-run tariffs depends crucially on the product category. Importers are less likely to front-run tariffs if a tariffed good can be substituted with domestically produced goods or goods from a non-tariffed country. More generally, we document that tariff announcements can have unintended consequences: at least prior to implementation, tariff announcements can increase imports and add to volatility in trade data.

Endnotes

-

1 An import tariff intervention is the announcement and implementation of a set of trade measures that impose new tariffs or raise existing tariffs on a set of products.

-

2 We examine excess imports during a window around the announcement of tariffs on May 14, 2024. Excess imports are calculated as the residuals from a regression of real Chinese import growth on total U.S. import growth for each category.

Article Citation

Cook, Thomas R., Mariia Dzholos, and Johannes Matschke. 2025. "Did Importers Try to Front-Run Recent Tariffs on China?" Federal Reserve Bank of Kansas City, Economic Bulletin, January 17.

References

Congressional Research Service. 2022. “External LinkDomestic Steel Manufacturing: Overview and Prospects.” Retrieved on November 23, 2024.

Department of Commerce. 2024. “External LinkU.S. Steel Executive Summary.” Retrieved on November 22, 2024.

International Energy Agency. 2024. “External LinkGlobal EV Outlook 2024: Trends in Electric Vehicle Batteries.” Retrieved on November 22, 2024.

Thomas Cook is a data scientist and Johannes Matschke is an economist at the Federal Reserve Bank of Kansas City. Mariia Dzholos is a research associate at the bank. The views expressed are those of the authors and do not necessarily reflect the positions of the Federal Reserve Bank of Kansas City or the Federal Reserve System.

Authors

Thomas R. Cook

Data Scientist

Mariia Dzholos

Research Associate