Six years ago, the Federal Open Market Committee (FOMC) adopted a longer-run 2 percent inflation target. Economic theory predicts that such a policy change should lead to better economic outcomes: specifically, by anchoring long-run inflation expectations, a central bank can respond aggressively to cyclical swings in employment without destabilizing prices.

Indeed, the FOMC had such benefits in mind when it adopted its long-run inflation target. In its January 2012 “Statement on Longer-Run Goals and Monetary Policy Strategy," the Committee wrote that communicating an inflation target to the public “helps keep longer-term inflation expectations firmly anchored, thereby fostering price stability and moderate long-term interest rates and enhancing the Committee's ability to promote maximum employment in the face of significant economic disturbances.”

Merely publishing a target for inflation, however, does not necessarily anchor inflation expectations at that target. Instead, the degree to which inflation expectations are anchored remains an empirical question. In this Macro Bulletin, we examine whether the FOMC’s adoption of an explicit longer-run inflation target better anchored inflation expectations in the United States._

If inflation expectations are anchored, then news about current, realized inflation should not affect forecasts about inflation far in the future. But if inflation expectations are unanchored or “drifting,” then recent inflation developments could sway investors’ longer-term inflation expectations. We use the following simple model to allow for both of these possibilities:

where Δπ LT,t denotes the change in longer-term inflation expectations, π news, t denotes news about current inflation, α is a constant, and ε t is a residual. The coefficient β reflects the degree to which long-term inflation expectations respond to realized inflation. If β is equal to 0, then long-term inflation expectations do not respond to realized inflation, which suggests inflation expectations are anchored. If β is positive, however, then inflation expectations drift in response to inflation news and are therefore unanchored.

To determine whether longer-term inflation expectations respond to realized inflation, we examine movements in market-based measures of inflation compensation—the extra remuneration investors receive for holding long-term securities not protected from inflation—following the release of the consumer price index (CPI). We measure news about current inflation using inflation “surprises” constructed as the difference between the reported value of core CPI inflation and the median forecast of core CPI inflation from a panel of professional forecasters compiled by Bloomberg. We measure long-term inflation expectations using five-year, five-year forward inflation compensation implied by the spread between Treasury yields and yields on Treasury inflation-protected securities. We estimate the previous model on CPI release days across two distinct periods: before the FOMC adopted its inflation target (1999–2011) and after (2012–17)._

Table 1: U.S. inflation compensation and inflation surprises on CPI release days

Note: Standard errors are Eicker-White robust.

Sources: Bloomberg, Federal Reserve Board (Haver Analytics), and authors’ calculations.

We find statistical evidence that inflation compensation became less responsive to inflation surprises after the FOMC adopted its inflation target. Table 1 shows the estimated values of β across the pre- and post-target sample periods. Prior to January 2012, core inflation surprises led to a statistically significant increase in inflation compensation. Specifically, a core CPI release 10 basis points higher than expected led five-year, five-year forward inflation compensation to rise by 1.5 basis points. After January 2012, however, the coefficient on core inflation surprises fell and was statistically indistinguishable from zero, suggesting that, on average, long-term inflation compensation no longer responded significantly to news about current inflation. Overall, these results suggest that communicating a numerical inflation target helped anchor inflation expectations.

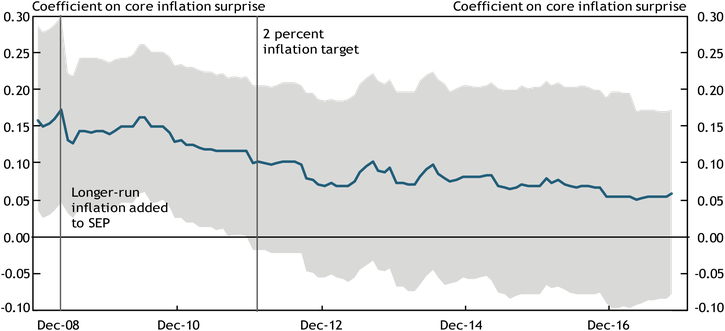

To gain more insight into when inflation expectations became better anchored, we next estimate our statistical model using a rolling 10-year sample of data. Chart 1 shows that β began declining in 2009 following the addition of “longer-run” inflation to the FOMC’s Summary of Economic Projections. One explanation for this decline is that investors interpreted these projections as an initial numerical range for the FOMC’s longer-run inflation target. By the time the FOMC adopted a numerical inflation target, the coefficient became statistically indistinguishable from zero.

Chart 1: Coefficient on core inflation surprises over time

Notes: Shaded areas denote 90 percent confidence intervals around the coefficient estimates. Dates represent the end point of the 10-year sample used in the estimation.

Sources: Bloomberg, Federal Reserve Board (Haver Analytics), and authors’ calculations.

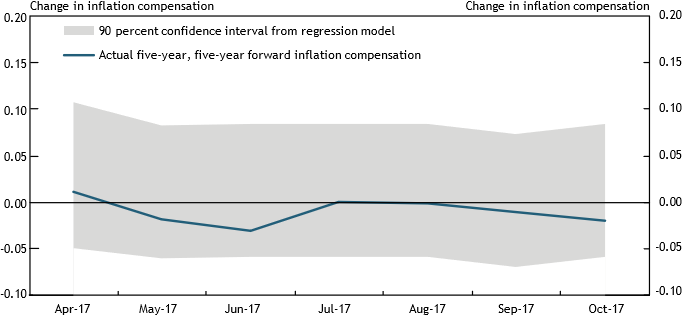

Although inflation expectations appear to have become better anchored over the past few years, a recent string of inflation surprises could have threatened this trend. Core inflation has persistently surprised forecasters over the last year: beginning with the March 2017 CPI report, five consecutive core CPI reports came in below the median expectation of Bloomberg forecasts. To examine whether this string of inflation shortfalls has frayed inflation expectations, we test whether the response of inflation compensation changed following these recent surprises.

We find that the recent CPI reports had little effect on the sensitivity of inflation expectations to inflation surprises._ Chart 2 shows the actual change in inflation compensation following the release of recent CPI reports and 90 percent confidence intervals for the predicted change in inflation compensation from our model estimated from January 2012 through March 2017. From April 2017 to October 2017, none of the actual changes in inflation compensation fell outside the range of likely outcomes predicted by the regression model. These findings suggest the degree to which inflation expectations are anchored, as measured by the sensitivity of inflation compensation to core CPI surprises, has remained unchanged in recent months.

Chart 2: Actual and predicted inflation compensation response to CPI reports

Note: The dates on the horizontal axis denote the dates of CPI releases. The U.S. bond market was closed on Friday, April 14, so we use the two-day change in inflation compensation for this observation. Our results are essentially unchanged if we omit this observation.

Sources: Bloomberg, Federal Reserve Board (Haver Analytics), and authors’ calculations.

The evidence in this Bulletin indicates that communicating a numerical inflation target better anchored U.S. inflation expectations. Moreover, the evidence indicates that expectations remained anchored throughout a series of recent inflation surprises. This does not, however, suggest a permanent change in the sensitivity of inflation expectations to unexpected news. After all, the past instability we have highlighted in this relationship suggests it could further evolve in response to changes in perceptions about monetary policy. Therefore, monitoring the sensitivity of inflation compensation to new data remains a valuable tool for central banks to better understand how bond markets perceive monetary policy.

Endnotes

-

1 For further analysis and discussion, see the related working paper by Bundick and Smith.

-

2 Our model also includes controls for the inflation surprises associated with the volatile food and energy components of the CPI, which are not included in the core measure. The coefficients on these controls and the estimates for the constant, α, are not statistically significant, so we omit them from this text. For more details, see Bundick and Smith.

-

3 Our model also includes controls for the inflation surprises associated with the volatile food and energy components of the CPI, which are not included in the core measure. The coefficients on these controls and the estimates for the constant, α, are not statistically significant, so we omit them from this text. For more details, see Bundick and Smith.

References

Board of Governors of the Federal Reserve System. 2012. “External LinkStatement on Longer-Run Goals and Monetary Policy Strategy,” January.

Bundick, Brent, and A. Lee Smith. 2018. “Does Communicating a Numerical Inflation Target Anchor Inflation Expectations? Evidence and Bond Market Implications.” Federal Reserve Bank of Kansas City, Research Working Paper 18-01, January.

Brent Bundick and A. Lee Smith are economists at the Federal Reserve Bank of Kansas City. The views expressed are those of the authors and do not necessarily reflect the positions of the Federal Reserve Bank of Kansas City or the Federal Reserve System.

Authors

Brent Bundick

Vice President