Stock prices retreated sharply in the fourth quarter of 2018, with the Standard and Poor’s (S&P) 500 stock price index falling 11.5 percent from September to December. Could the recent stock market decline dampen consumer and business confidence and thereby jeopardize the strong economy? To examine the relationship between consumer confidence and the stock market, I estimate a statistical model of the joint behavior of equity price growth and growth in consumer confidence. I measure equity prices using the S&P 500 index and consumer confidence using the University of Michigan’s consumer sentiment index, although I obtain similar results using the Conference Board’s consumer confidence index._

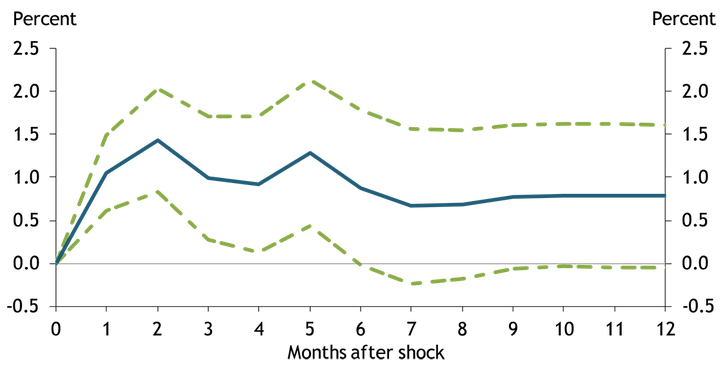

The model allows me to test whether changes in equity prices predict changes in confidence or the other way around. A Granger causality test shows that changes in equity prices predict changes in confidence, but changes in confidence do not predict changes in equity prices. Chart 1 shows the response of consumer sentiment to a 1 standard deviation shock to equity price growth (a negative shock would yield the opposite responses). Consumer sentiment increases for about a year and a half after the shock, which raises the equity price index persistently by about 4.5 percent. These results are qualitatively consistent with previous findings by Otoo (1999), who focuses on the 1980–99 period.

Chart 1: Response of Consumer Sentiment to a Stock Market Shock

Note: Dashed lines represent ±2 standard deviations obtained from 1,000 Monte Carlo repetitions.

Sources: Standard and Poor’s (Haver Analytics), University of Michigan (Haver Analytics), and author’s calculations.

Stock market valuations could affect consumer confidence through two channels. First, higher equity prices could boost consumer confidence by increasing household wealth. Second, higher equity prices could boost consumer confidence because they are viewed as a leading indicator of future economic activity and thus future incomes. However, the first channel is likely relatively small because stock ownership is highly concentrated among the wealthiest households—in fact, nearly half of households do not own any stocks. Indeed, reestimating the statistical model separately on the current-conditions and future-expectations components of the consumer sentiment index shows that the response of consumer expectations to a stock market shock is greater than the response of consumer perceptions of current economic conditions. This result indicates that stock market gains boost consumer sentiment more by signaling higher future incomes than by increasing households’ current wealth.

Previous research has established a link from consumer confidence to real consumption spending. For example, Carroll, Fuhrer, and Wilcox (1994) and Ludvigson (2004) find that confidence measures contain information about future consumption spending, although much of that information can also be found in other economic and financial indicators.

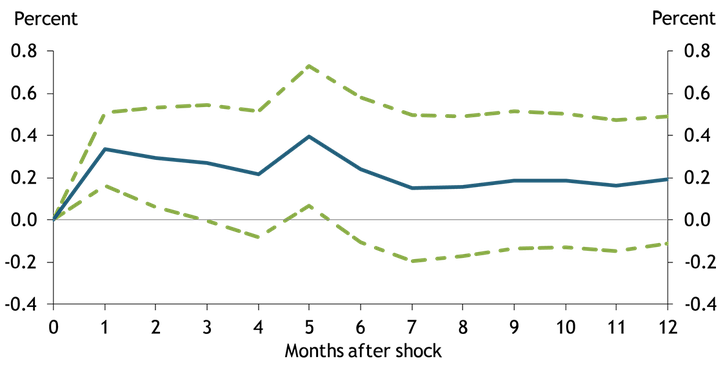

Like consumer confidence, business confidence responds positively to stock market surprises. I examine the relationship between business optimism and the stock market by reestimating the statistical model after replacing the consumer sentiment index with the National Federation of Independent Business (NFIB)’s small business optimism index. The Granger causality test shows that equity price growth predicts growth in small business optimism and vice versa. Chart 2 displays the response of NFIB small business optimism to a 1 standard deviation shock to equity price growth._ The response of small business confidence is significantly higher than zero for half a year, although the magnitude is smaller than the response of consumer sentiment in Chart 1. Because small businesses are not publicly listed, a stock market shock does not boost the value of small businesses directly. Small business sentiment likely rises after such a shock because the higher equity prices are a leading indicator of future economic activity and thus future profits.

Chart 2: Response of Small Business Optimism to a Stock Market Shock

Note: Dashed lines represent ±2 standard deviations obtained from 1,000 Monte Carlo repetitions.

Sources: Standard and Poor’s (Haver Analytics), NFIB (Haver Analytics), and author’s calculations.

These results indicate that a slumping stock market dampens consumer and business confidence by signaling bad times ahead. A risk for the current economic outlook is that the recent stock market decline could undermine confidence. Once consumers become more pessimistic about their future income and businesses become more pessimistic about their future profits, they may rein in spending, with adverse consequences for economic activity. However, taken at face value, the estimated responses of confidence and the estimated effects on consumption spending obtained by other studies suggest that even a large stock market decline would have limited effects on economic activity through this channel.

Endnotes

-

1 The model is a VAR(6) estimated on monthly data for both indexes from 1978:M1 to 2018:M9. Both variables enter the model after taking logs and first differences. The lag length is based on a likelihood ratio test. An equity price growth shock is identified by assuming that consumer confidence does not respond contemporaneously to such a shock.

-

2 The model is a VAR(6) estimated on monthly data for the NFIB’s small business optimism index and the S&P 500 equity price index from 1986:M1 to 2018:M9. Both variables enter the model after taking logs and first differences. The lag length criterion and the identification method are the same as before.

References

Carrol, Christopher D., Jeffrey C. Fuhrer, and David W. Wilcox. 2008. “Does Consumer Sentiment Forecast Household Spending? If So, Why?” American Economic Review, vol. 84, pp. 1397–1408.

Ludvigson, Sydney C. 2004. “Consumer Confidence and Consumer Spending.” Journal of Economic Perspectives, vol. 18, pp. 29−50.

Otoo, Maria W. 1999. “Consumer Sentiment and the Stock Market.” Board of Governors of the Federal Reserve System.

Willem Van Zandweghe is an assistant vice president and economist at the Federal Reserve Bank of Kansas City. The views expressed are those of the author and do not necessarily reflect the positions of the Federal Reserve Bank of Kansas City or the Federal Reserve System.