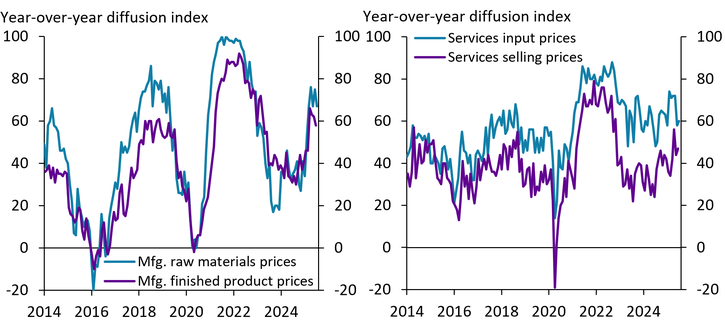

A growing share of businesses in the Tenth Federal Reserve District have reported rising input costs and selling prices in 2025, according to the manufacturing and services surveys from the Federal Reserve Bank of Kansas City._ The blue lines in Chart 1 show that the price indexes for raw materials and inputs rose sharply beginning in February 2025. By July 2025, a net 67 percent of manufacturing firms (left panel, blue line) and a net 60 percent of services firms (right panel, blue line) reported higher raw materials costs than a year prior. Price indexes for finished products and services (purple lines) tend to closely follow changes in input cost indexes. However, the spread between the two indexes has grown (as shown by the gap between the purple and blue lines), indicating fewer firms are passing on cost increases to their final consumers.

Chart 1: More manufacturing firms than services firms are raising their output prices in reaction to input price increases in 2025

Notes: Mfg. abbreviates manufacturing. The diffusion indexes measure the net percentage of firms reporting an increase in prices.

Sources: Federal Reserve Bank of Kansas City and U.S. Bureau of Labor Statistics (Haver Analytics).

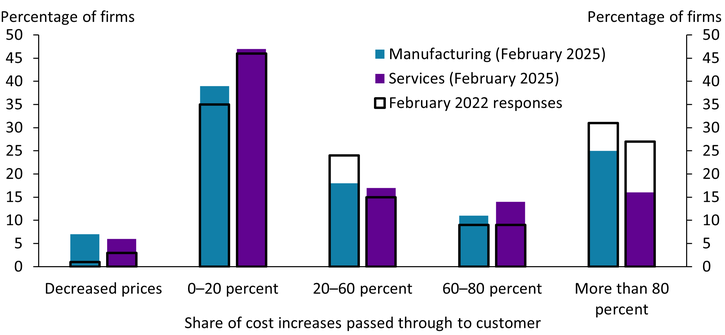

Indeed, survey data show that firms’ ability to pass through cost increases has waned since the inflationary surge in 2021–22, especially for services firms. Chart 2 shows the share of cost increases that manufacturing firms (blue bars) and services firms (purple bars) reported they were able to pass through to consumers in February 2025 compared with February 2022 (black borders). Both manufacturing and services firms have reported a reduced ability to pass through cost increases in recent years. In February 2022, when the surveys’ price indexes were near their peak, 31 percent of manufacturing firms and 27 percent of services firms passed through more than 80 percent of cost increases to customers. In February 2025, however, only 25 percent of manufacturing firms and 16 percent of services firms were able to pass through 80 percent of their cost increases. Passthrough has been especially low for services firms, which include firms that ultimately sell goods to end customers._ For instance, in February 2025, 53 percent of services firms reported passing through less than 20 percent of their cost increases to customers, compared with 46 percent of manufacturing firms. This reduced passthrough could strain firms’ profit margins, especially if sustained.

Chart 2: Tenth District firms are passing through a smaller share of cost increases to customers than in 2022

Note: Chart shows firms’ responses to the survey question, “If your firm is facing higher costs (inputs and labor), what share of those increases are you able to pass through to customers in the form of higher prices?”

Source: Federal Reserve Bank of Kansas City.

Several factors may influence a firm’s ability to pass through price increases to customers, including the strength and flexibility of demand as well as a firm’s position in the supply chain. According to several regional Federal Reserve Bank surveys, 82 percent of firms reported strength of demand as a top factor influencing their pricing decisions (Dogra and others 2023). In addition, flexibility of demand—that is, a consumer’s ability to substitute other goods, services, or producers—can also influence passthrough. Lastly, a firm’s proximity to the end consumer could influence the degree to which they pass cost increases on to consumers. As goods move along the supply chain from producer to consumer, their contribution to the total cost of the final output declines, while contributions from other costs, such as labor and infrastructure, increase. Accordingly, passthrough to the final consumer is delayed and limited for final goods such as food, coffee, and beer (Scott and others 2024; Nakamura and Zerom 2010; Goldberg and Hellerstein 2013).

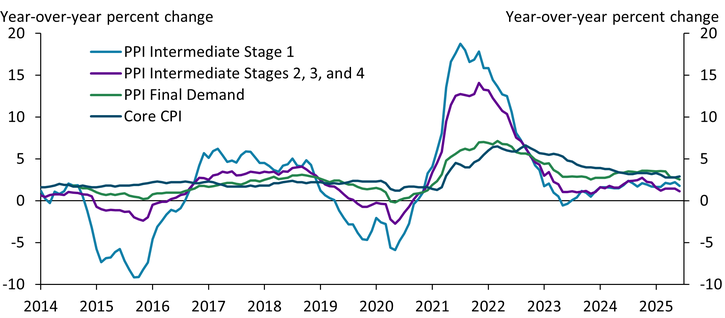

This diminished passthrough for goods sold to end consumers is reflected in the Producer Price Index (PPI), which measures changes in input prices for goods and services at four stages of intermediate demand as well as selling prices of goods and services sold as final demand. Chart 3 separates the PPI for goods and services in Stage 1 of intermediate demand—that is, the most upstream industries, such as metal and chemical manufacturing—from goods and services in Stages 2, 3, and 4, such as machinery and motor vehicle parts manufacturing. Input prices for goods in Intermediate Stage 1 (light blue line) changed frequently by large margins, with year-over-year changes ranging from −9 percent to 6 percent over the 2014–20 period. Although input prices for goods in Stages 2, 3, and 4 (purple line) moved concurrently with input prices for goods in Stage 1, the magnitude of the changes was much smaller. Consistent with this diminished passthrough, the magnitude of changes of the price of goods and services sold as final demand (green line), such as a car sold from a manufacturer to a dealership, was even smaller, suggesting these prices are more stable.

Chart 3: Cost changes can decrease in magnitude as goods move along the supply chain

Notes: PPI intermediate and final demand indexes shown exclude food, energy, and trade services. Core CPI excludes food and energy prices. Intermediate demand indexes shown average the following indexes for each stage weighted by their relative importance: goods inputs excluding food and energy to goods producers; services inputs less trade, transportation, and warehousing to goods producers; goods inputs excluding food and energy to services producers; and services inputs less trade, transportation, and warehousing to services producers. The purple line shows an average of Stage 2, Stage 3, and Stage 4 weighted by their relative importance.

Sources: U.S. Bureau of Labor Statistics (Haver Analytics) and authors’ calculations.

Further down the supply chain, changes in the prices paid by end consumers vary even less than producers’ selling prices, indicating the amount of cost increases firms pass through to consumers changes over time. The dark blue line in Chart 3 shows that changes in the final prices consumers pay (as measured by the core Consumer Price Index, or CPI) are generally more stable than producer prices. From 2014 to 2020, yearly core CPI growth averaged 2.0 percent with a 0.3 percentage point standard deviation—substantially smaller than the 0.9 percentage point standard deviation for final demand PPI. The smaller and more stable movements in consumer prices—which include wholesale and retail markups—relative to producer selling prices suggest that the degree of passthrough to the end consumer changes over time. This variability may reflect limited or delayed passthrough in response to changing cost pressures and demand conditions.

In conclusion, input prices have increased for Tenth District firms in 2025, but fewer firms—especially fewer services firms—have reported rising output prices recently than have reported rising input prices, indicating some firms have not passed all their cost increases to the customer. This response is consistent with other data and research showing that firms’ ability to pass through costs diminishes as goods move along the supply chain. Additionally, manufacturing and services firms that have raised output prices reported passing through a smaller share of costs to customers than they did during the inflationary surge in 2021–22. This slowdown in price pass through could suggest smaller price increases for consumers in the immediate future, though it is unclear whether firms can sustain the apparent compression in their profit margins.

Endnotes

-

1 The Tenth Federal Reserve District encompasses Colorado, Kansas, Nebraska, Oklahoma, Wyoming, and parts of Missouri and New Mexico.

-

2 The Kansas City Fed’s services survey includes firms in the wholesale, retail, construction, transportation, real estate, professional services, education, healthcare, restaurants, and leisure and hospitality sectors.

Article Citation

Cowley, Cortney, and Chase Farha. 2025. "Amid Rising Input Costs, Many Tenth District Firms Report Passing Along Fewer Costs to Customers." Federal Reserve Bank of Kansas City, Economic Bulletin, August 1.

References

Dogra, Keshav, Sebastian Heise, Edward S. Knotek II, Brent H. Meyer, Robert W. Rich, Raphael S. Schoenle, Giorgio Topa, Wilbert van der Klaauw, and Wändi Bruine de Bruin. 2023. “External LinkEstimates of Cost-Price Passthrough from Business Survey Data.” Federal Reserve Bank of New York, Staff Reports, no. 1062, June.

Goldberg, Pinelopi Koujianou, and Rebecca Hellerstein. 2013. “External LinkA Structural Approach to Identifying the Sources of Local Currency Price Stability.” Review of Economic Studies, vol. 80, no. 1, pp. 175–210.

Nakamura, Emi, and Dawit Zerom. 2010. “External LinkAccounting for Incomplete Pass-Through.” Review of Economic Studies, vol. 77, no. 3, pp. 1192–1230.

Scott, Francisco, Amaze Lusompa, David Rodziewicz, Cortney Cowley, and Jacob Dice. 2024. “The Passthrough of Agricultural Commodity Prices to Food Prices.” Federal Reserve Bank of Kansas City, Research Working Paper no. 24-16, December.

Cortney Cowley is an assistant vice president and the Oklahoma City branch executive at the Federal Reserve Bank of Kansas City. Chase Farha is a research associate at the bank. The views expressed are those of the authors and do not necessarily reflect the positions of the Federal Reserve Bank of Kansas City or the Federal Reserve System.

Authors

Cortney Cowley

Assistant Vice President and Oklahoma City Branch Executive