Housing Market and Prices

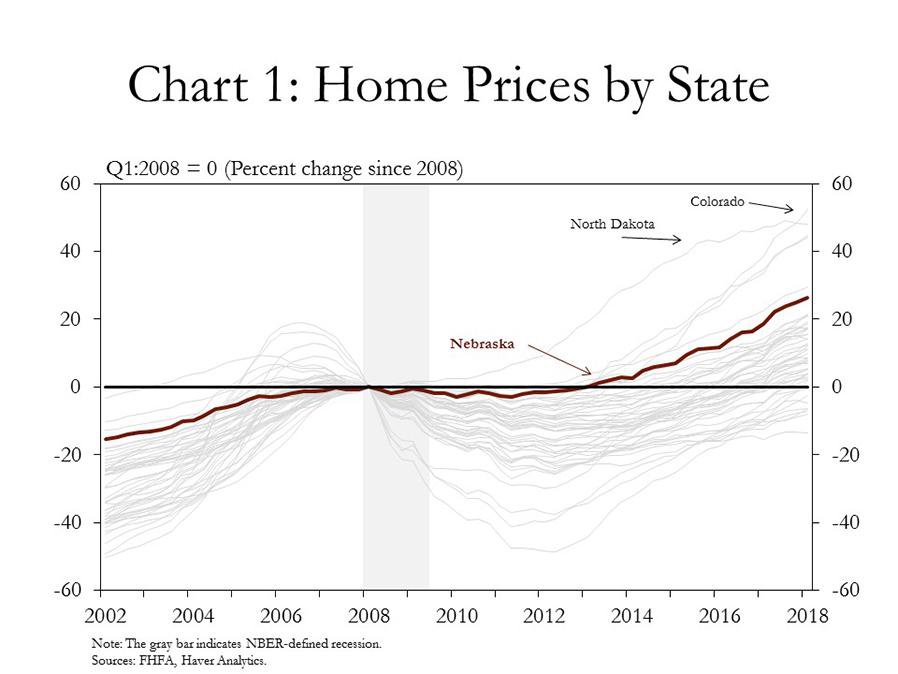

Home prices in Nebraska have accelerated over the past two years, and continued to rise in the second quarter. In the years ahead of the Great Recession in late 2007, increases in Nebraska trailed those of most other states (Chart 1). However, prices in Nebraska remained relatively stable throughout the 2007-09 recession. After remaining flat for several years during the ensuing recovery, prices began to accelerate in 2013. Through the first quarter of 2018, prices in Nebraska were 26 percent higher than at the beginning of the recession, the sixth-strongest rate of growth among all states over the past decade.

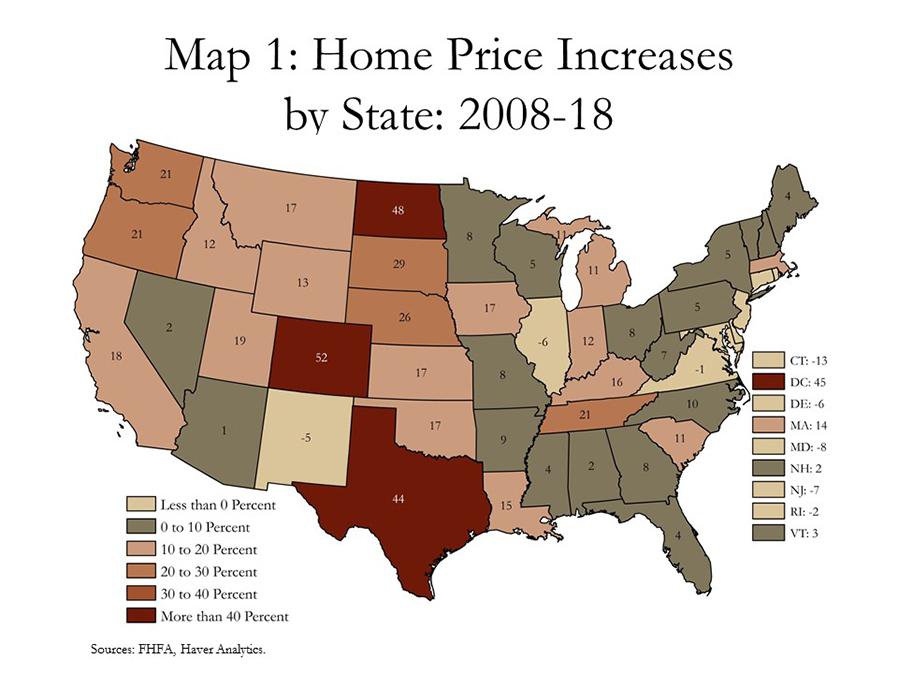

Since 2008, Nebraska’s home prices have risen faster, on average, than most of the nation. By the first quarter of 2018, only Colorado, North Dakota, the District of Columbia, Texas and South Dakota have posted stronger gains over the last decade (Map 1). The stability of Nebraska’s housing market during the recession partially contributed to this strength. Prices in many parts of the country that were most associated with the subprime mortgage crisis, such as Florida, Nevada, and many northeastern states, have only recently returned to pre-crisis levels, whereas home prices in Nebraska eclipsed their pre-crisis mark in 2013.

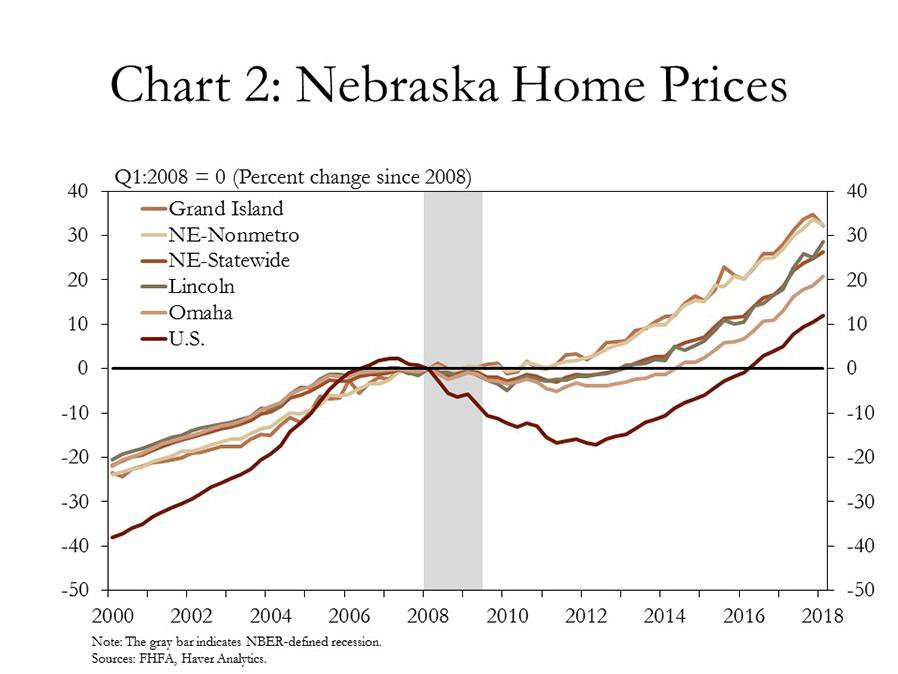

In addition, home prices have increased broadly across the state. Over the past few years, prices have strengthened most significantly outside of major metropolitan areas, but the increases in Omaha and Lincoln also have been notable (Chart 2). Moreover, average price gains over the past year in all areas of the state have been the strongest for a four-quarter period since the mid-1990s. In Lincoln, in fact, home prices have increased at an average rate of 8.4 percent in the past four quarters, exceeding even the growth rates of the 1990s.

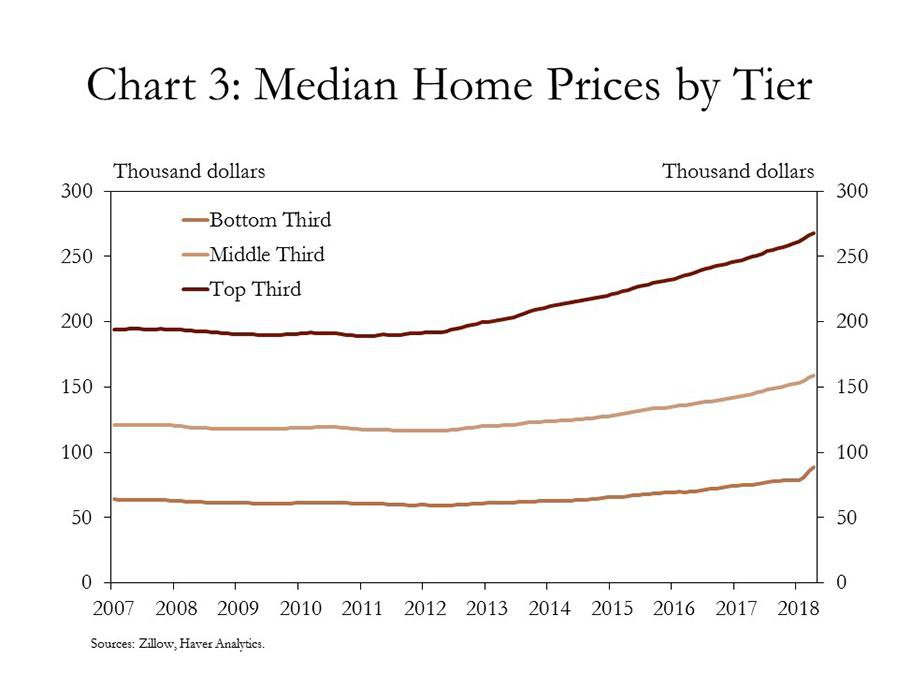

Since 2013, prices also have accelerated for homes of all price levels. Over the past five years, median home prices in Nebraska have increased more than 30 percent for high-, medium- and low-priced homes. Prices of the highest-priced homes have increased 34 percent since 2013, a gain of nearly $68,000 (Chart 3). Prices of medium- and low-priced homes have increased 32 percent and 45 percent, respectively. Perhaps most notably, the price of homes in the lowest tier increased sharply in the first few months of 2018, with a gain of about $10,000 since the end of last year.

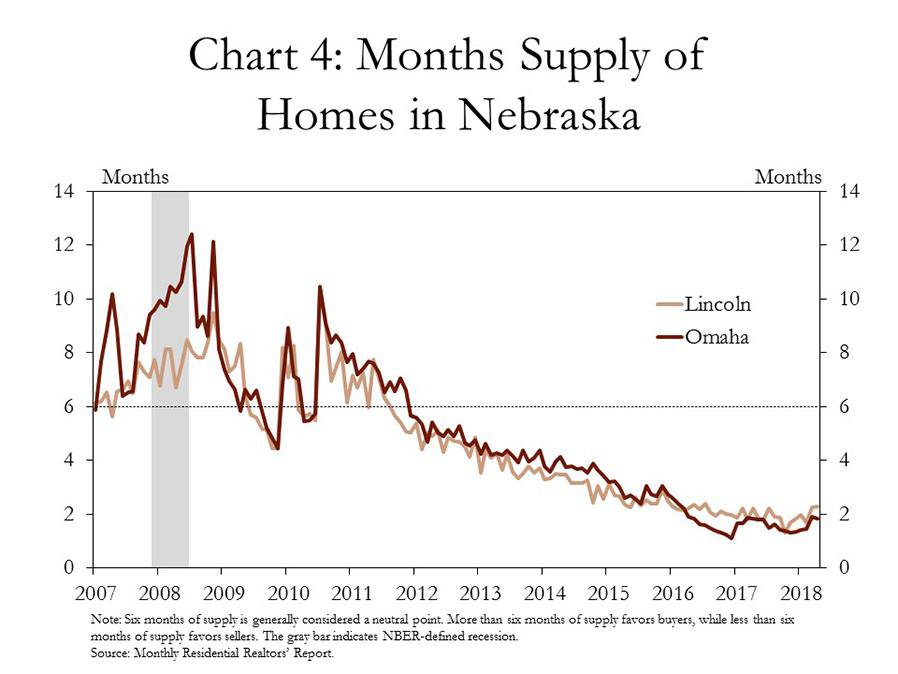

An extremely limited supply of homes has continued to be the primary driver of broad-based and steady price increases. Prior to the last recession, the number of homes available in Omaha and Lincoln amounted to more than six months of supply, meaning that if no new homes were placed on the market, it would take six months for all homes to be sold. The supply of homes in Omaha and Lincoln has steadily dwindled in recent years, and in both metros inventories have hovered near two months of availability, indicating a prolonged period of a very strong sellers’ market (Chart 4). In rural areas, residents and employers also have commented that a housing shortage is one of the most significant economic challenges that has emerged in recent years.

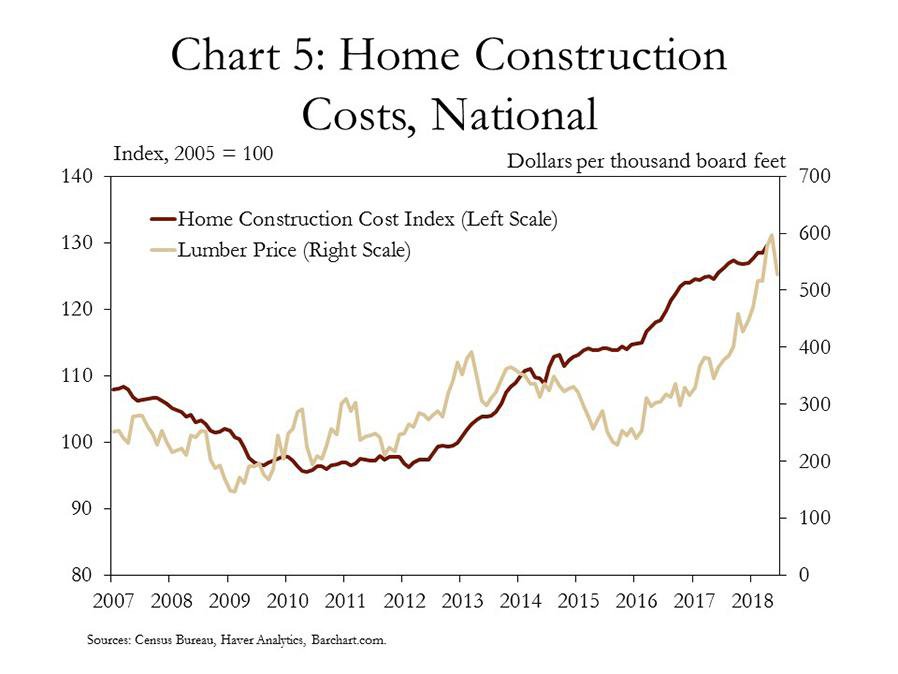

Increases in construction costs also have contributed to higher prices. According to the National Association of Home Builders, construction costs account for about 60 percent, on average, of the cost of a new home. After remaining relatively flat in the initial years following the 2007-09 recession, construction costs have increased significantly. Since the beginning of 2013, average construction costs, nationally, have increased almost 30 percent (Chart 5). The price of lumber, which accounts for a significant share of construction costs, has roughly doubled just in the past two years.

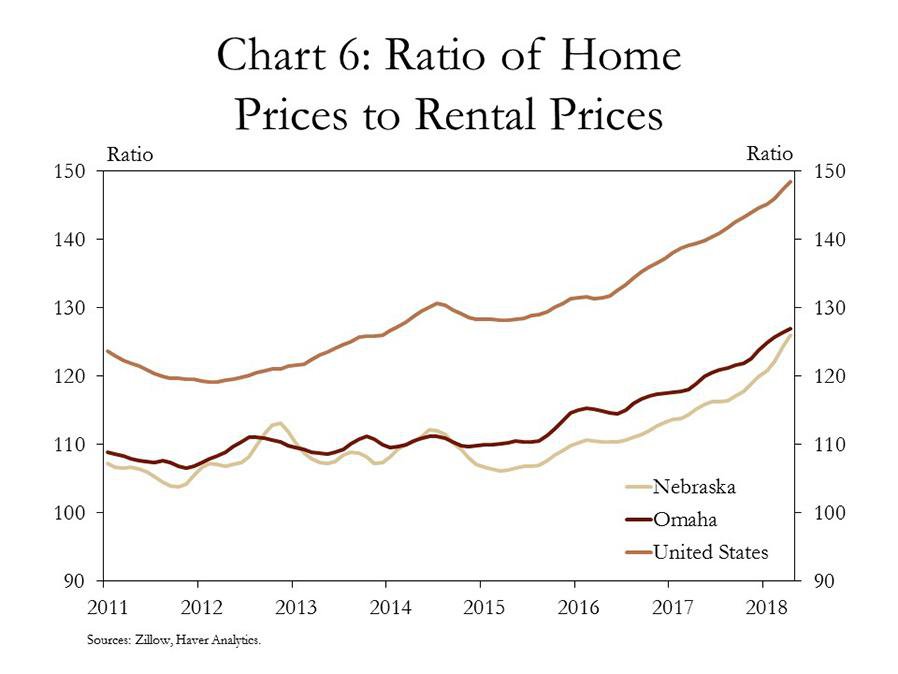

In recent months, home prices have risen more rapidly than rental prices. From 2010 through 2015, the ratio of home prices to rental prices was relatively steady throughout Nebraska, with monthly home prices approximately 108 times higher than monthly rental prices (Chart 6). Following national trends, however, the ratio has jumped to about 125 since 2015. In fact, since the beginning of 2018, home price gains in Nebraska have outpaced rental gains by nearly 20 percentage points, according to Zillow.

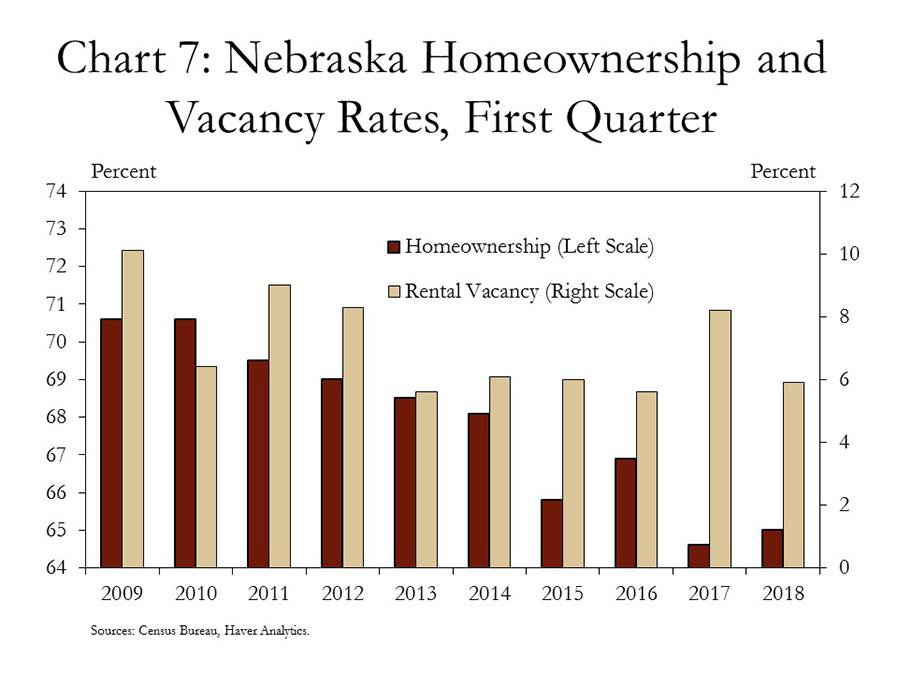

With a limited housing supply in Nebraska, and prices rising faster than rents, homeownership has trended lower. In the first quarter of 2018, the rate of homeownership in Nebraska was nearly 5 percentage points lower than in 2009 (Chart 7). Alongside a declining rate of homeownership, rental property vacancy rates also have edged lower despite a number of new apartment buildings in both Omaha and Lincoln. Since 2009, Nebraska’s rental property vacancy rate has declined about 4 percentage points.

Mortgage Debt and Household Finance

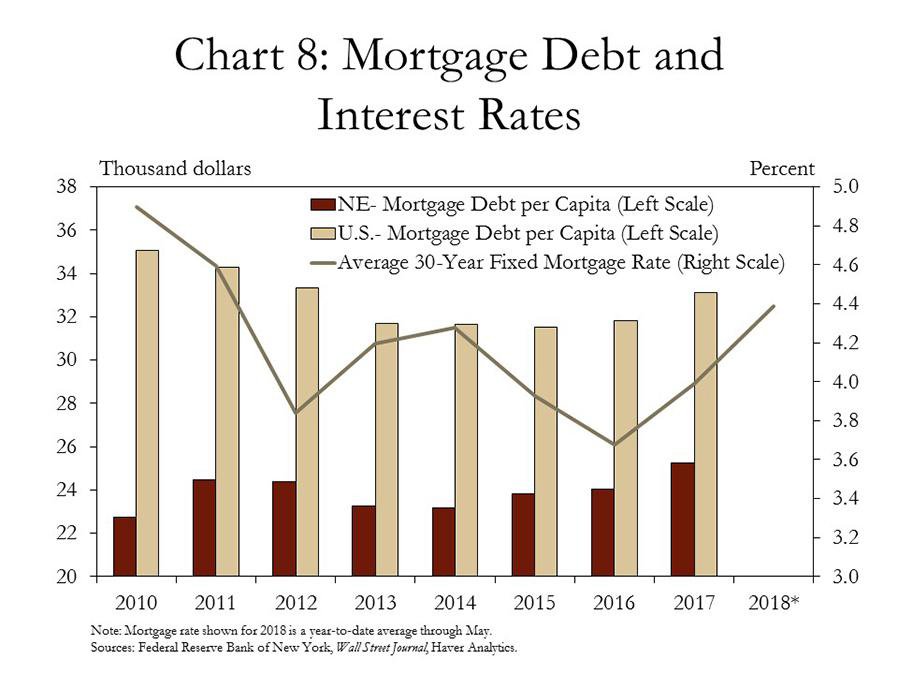

With home prices on the rise, and interest rates also higher than a year ago, overall mortgage debt has increased slightly. In 2017, mortgage debt in Nebraska increased 5.1 percent from the previous year, amounting to about $1,200 on a per capita basis (Chart 8). Meanwhile, the average interest rate for a 30-year mortgage increased 0.3 percentage points in 2017 and continued to rise in the first half of 2018. Despite the increased mortgage debt in Nebraska, however, the level of debt has remained significantly less than the nation, due primarily to lower home prices.

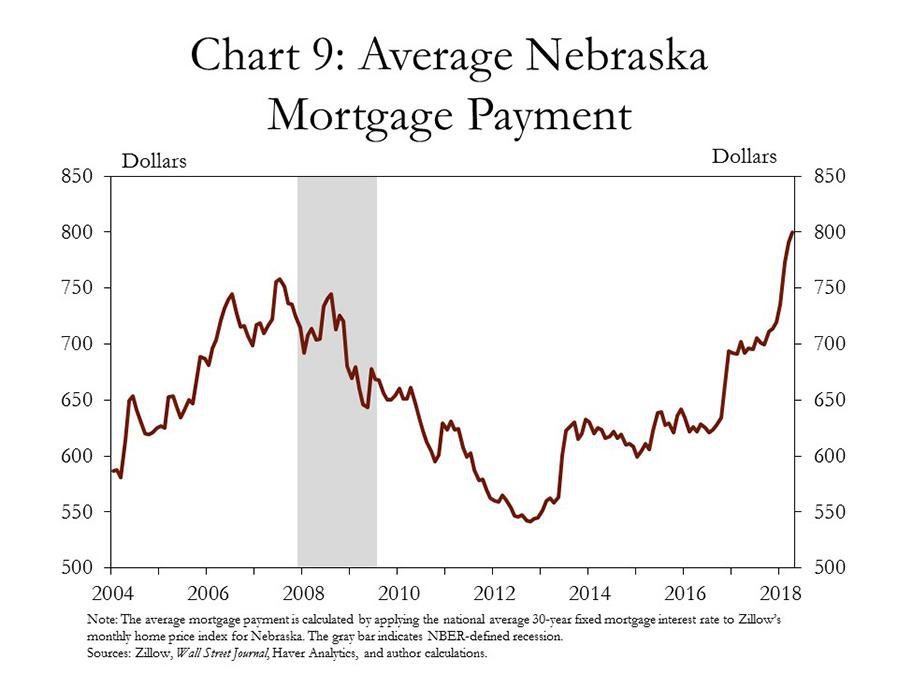

Average mortgage payments for new homes also have increased over the past year. The monthly payment for the average home in Nebraska, financed in April 2018, and applying a 30-year fixed mortgage rate, was $800 (Chart 9). This average payment was an increase of about $100 per month from a year ago, and nearly $250 since the beginning of 2013.

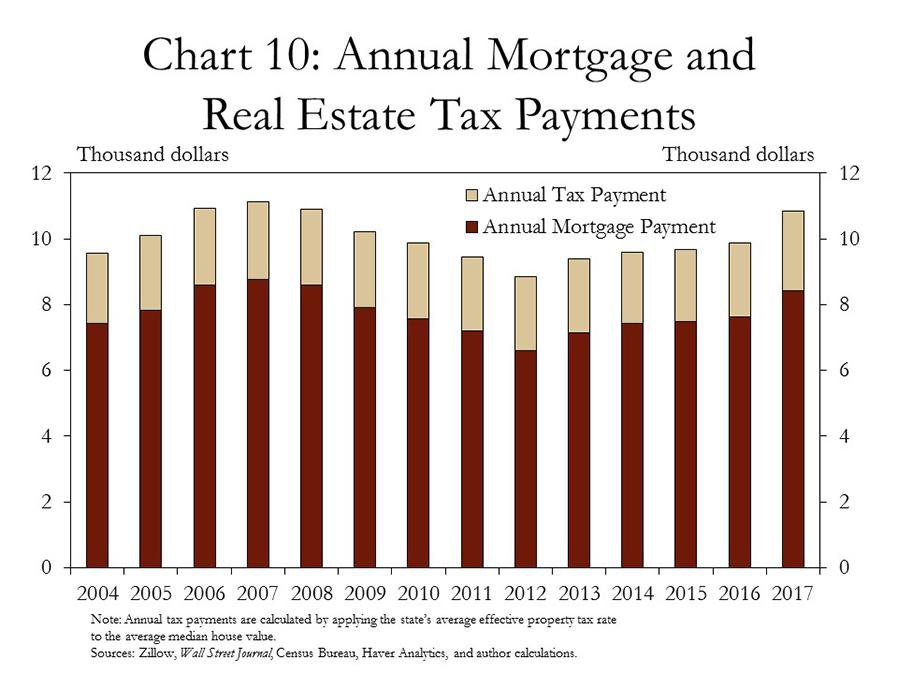

In addition to mortgage payments, real estate taxes also contribute to the overall cost of homeownership but generally have remained steady. While average mortgage payments have fluctuated annually in different price and interest-rate environments, the average payment of real estate taxes has remained relatively constant (Chart 10). Annual tax payments in recent years have ranged between $2,000 and $2,500. In 2017, the tax payment for a typical home in Nebraska was $2,434 when applying the state’s effective tax rate on residential property.

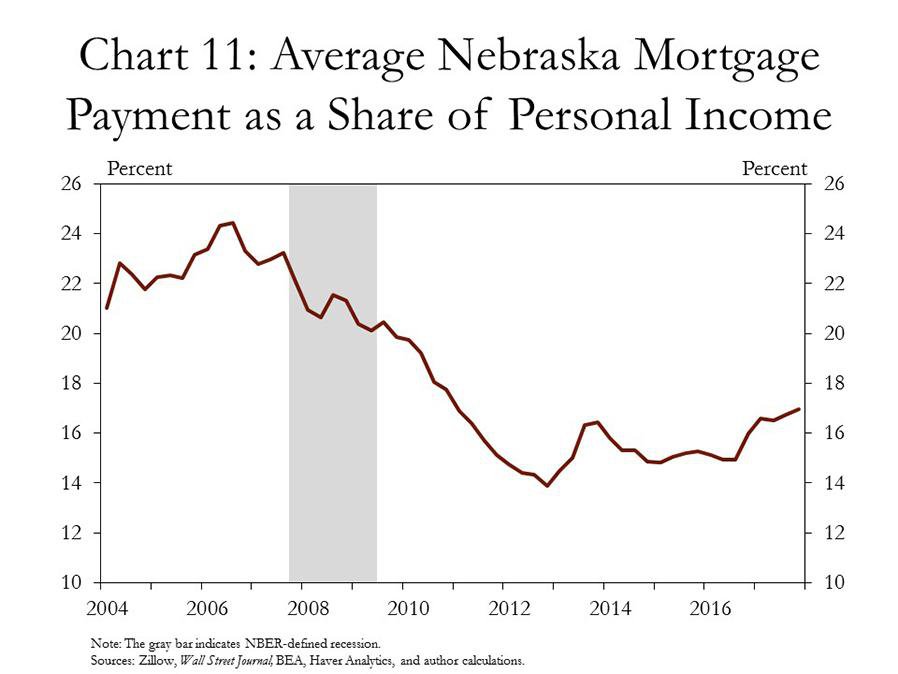

Despite the recent increases in the cost of home ownership for new buyers, though, increases in personal income have limited the overall effect on household budgets. Since the beginning of 2013, despite a significant increase in mortgage payments for a newly financed home, nominal per capita personal income has increased $4,360 in Nebraska. As a result of steady increases in incomes, mortgage payments as a share of personal income have increased only 2.5 percentage points since 2013 (Chart 11).

Nebraska households generally have remained well positioned to service their mortgage debt as wages and incomes have continued to rise alongside increased home prices. In the first quarter of 2018, mortgage payments considered past due were below their pre-recession level and remained less than the nation (Chart 12). In addition, home foreclosures also continued to trend lower in Nebraska and were at very low levels through the first quarter.

Conclusion

Broad-based and persistent gains in Nebraska’s housing market are a significant indicator of a strong state economy. Although debt obligations have risen slightly for buyers of new homes due to sharp increases in home prices and modest increases in interest rates, rising incomes and wages have mitigated some of these potential challenges for Nebraska households. The strength of the state’s job market and its overall economy has allowed homeowners to effectively manage their mortgage payments and build equity. The real challenge for many aspiring homeowners in Nebraska, however, has been to find a home available to buy in the first place.

The views expressed in this article are those of the authors and do not necessarily reflect the views of the Federal Reserve Bank of Kansas City or the Federal Reserve System.

Author