Entering the next decade, Nebraska’s economy is well-positioned to continue the steady growth that has marked the past two decades. Statewide, growth in population, employment and household income has trended higher at a modest but steady pace since the end of the 1990s, and appears likely to remain relatively stable into the next decade. Recent trends also suggest, however, that the additional growth will largely be concentrated in or near metropolitan areas and connected to service-based industries such as health care, finance, insurance and technology firms.

Although economic growth in Nebraska is likely to remain stable, it appears that disparities will persist. Growth in the state’s rural areas could remain limited alongside population losses and ongoing challenges in agriculture. Within metro areas, income gains among high earners have outpaced those closer to the median, and demand for high-skilled professionals is likely to remain strong. In addition to a persistently tight labor market and intense competition for talent, a strong housing market also will provide ongoing support to household wealth, even as the gap between high- and low-priced homes widens.

Against a backdrop of steady growth amid ongoing disparities, this edition of the Nebraska Economist examines overarching trends in Nebraska’s economy over the past two decades as context for how the next decade might unfold.

Population

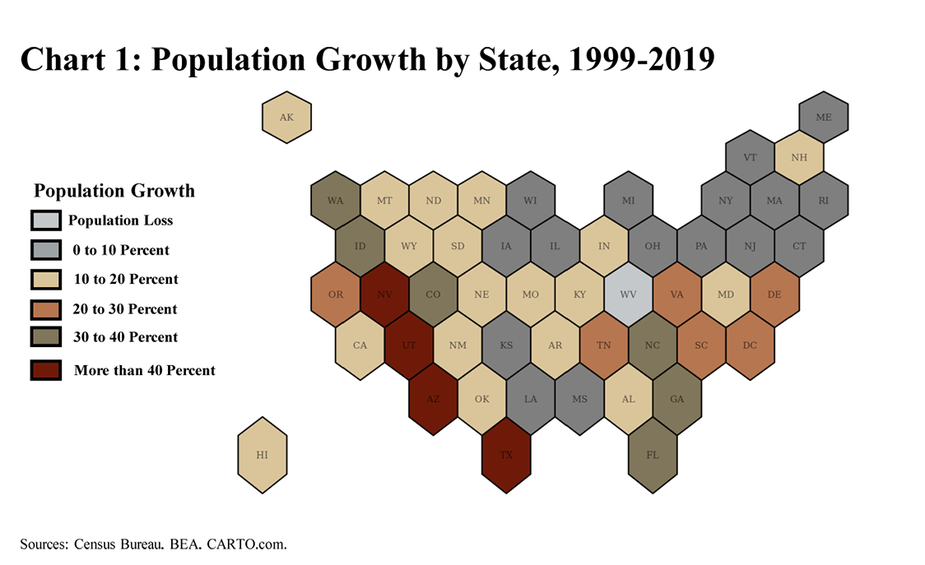

Population growth in Nebraska has trailed the nation the past two decades, but has remained stable. Since 1999, Nebraska’s population has increased about 230,000, an average annual increase of 0.6 percent. Over the past 20 years, population growth has been strongest in states in the southern and western United States (Chart 1). Although Nebraska’s rate of population growth has been more modest, the rate has increased from 0.45 percent in the early 2000s to an average of 0.56 percent the past three years.

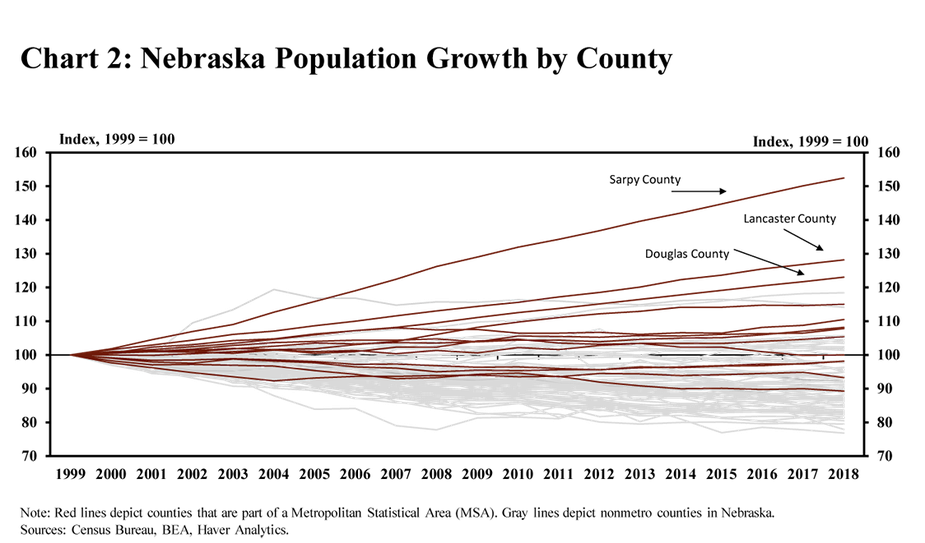

Counties in the state’s metropolitan areas have accounted for much of Nebraska’s increase in population. Since 1999, population growth in Sarpy County has led the state, followed by other metro counties in the Omaha and Lincoln areas (Chart 2). In an ongoing trend of growing disparity between the state’s urban and rural areas, only 16 percent (13 total) of nonmetro counties have added population in the past two decades.

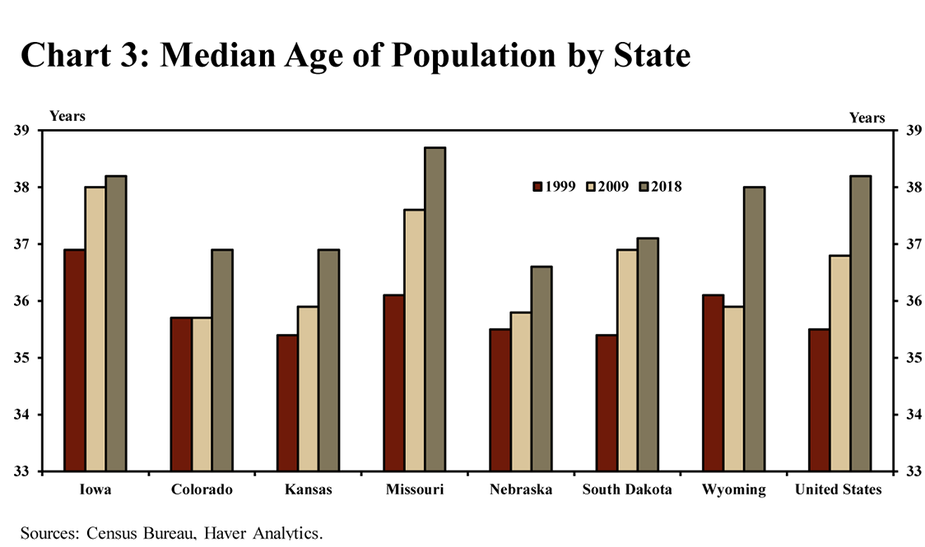

Similar to national trends, Nebraska’s population has continued to age, but not as quickly as the nation or most surrounding states. From 1999 to 2018 (the most recent data available), the median age in Nebraska has increased from 35.5 to 36.6 (Chart 3). Nationally, the median age has increased by 2.7 years, and also at a faster rate in each of Nebraska’s neighboring states.

Employment

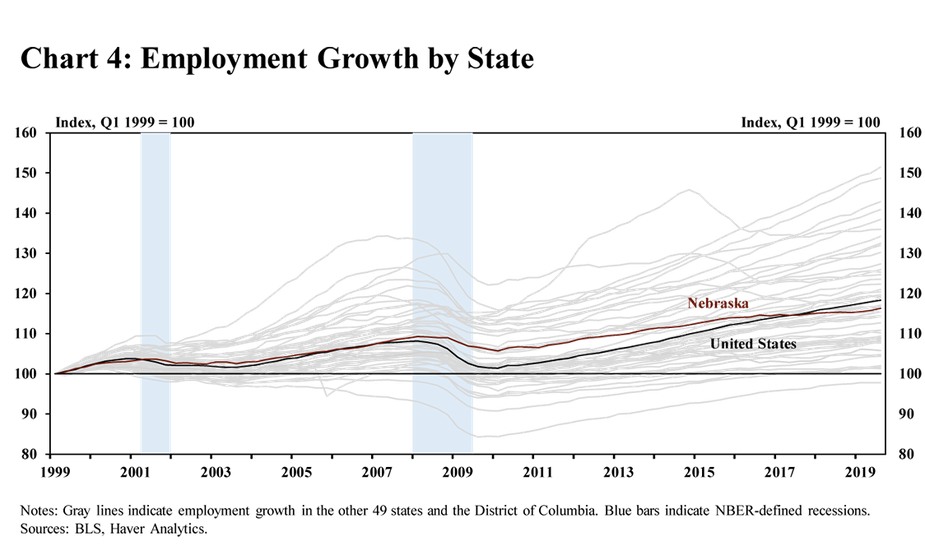

Employment in Nebraska has expanded steadily in recent decades. Since 1999, employment has increased 16 percent, ranking 26th among all states (Chart 4). Although job growth has been slightly less than the nation’s average, the growth also has been relatively stable, falling only modestly during the last recession. States in the West and South have led the nation in employment growth the past two decades, and only Michigan had fewer jobs in 2019 than in 1999.

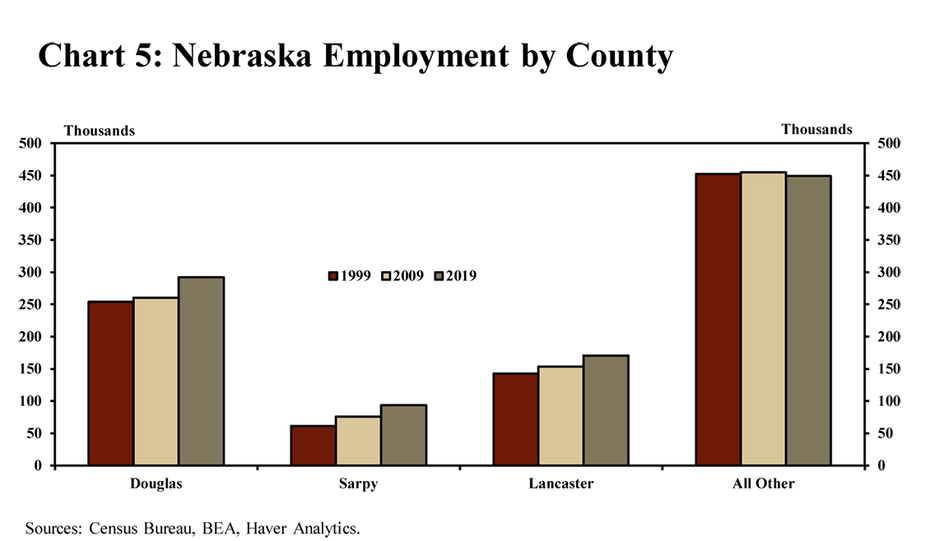

Similar to changes in population, Nebraska’s metro counties have accounted for most of the state’s job growth. In 1999, three counties (Douglas, Sarpy and Lancaster) accounted for 50 percent of employment in Nebraska. Two decades later, these counties now account for more than 55 percent of jobs in the state, as residents in rural areas continue to relocate to more urban locations (Chart 5).

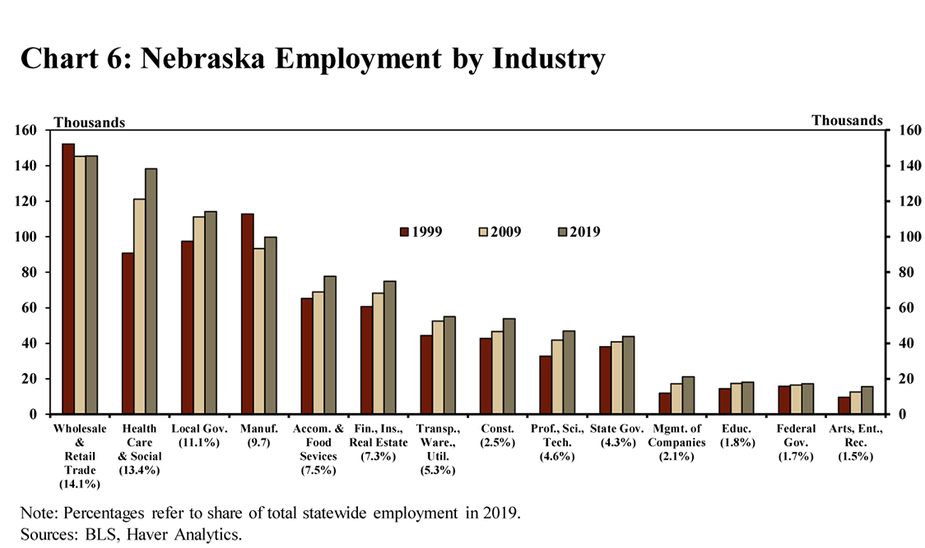

Several of Nebraska’s service-providing industries in its urban areas have accounted for a large share of the state’s job growth. Most notably, the health-care industry has added nearly 50,000 jobs statewide since 1999 (Chart 6). Most other industries also have added jobs at a modest pace in recent decades with the exception of retail trade and manufacturing alongside the emergence of online retailers and automation.

Industry Composition

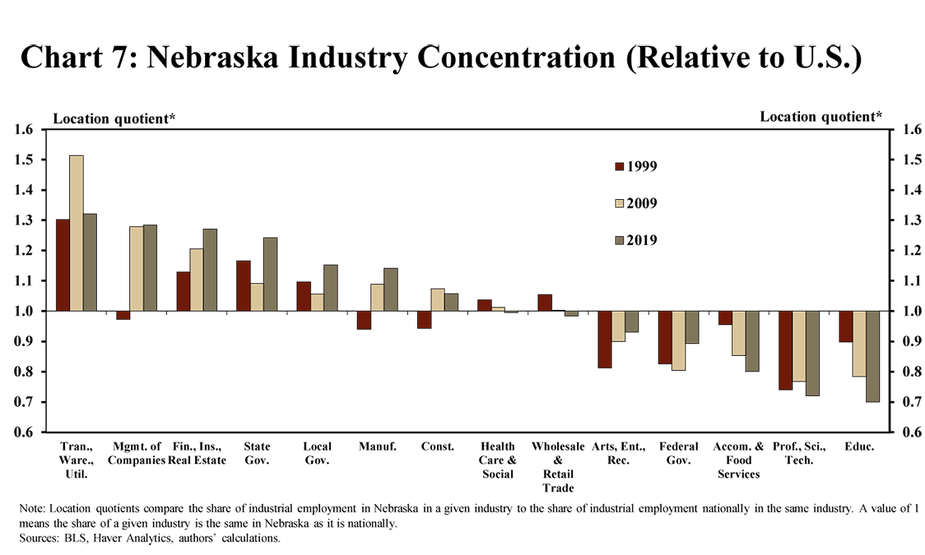

Over time, the concentration of industries in Nebraska has shifted. Some key industries have become more concentrated since 1999 relative to the nation, such as manufacturing and finance, insurance and real estate (Chart 7). Other key industries have seen their relative prominence in Nebraska decline, such as health care and social assistance, and wholesale and retail trade. This reduced prominence, despite ongoing job growth in industries such as health care, has reflected a more significant expansion in those industries elsewhere in the nation.

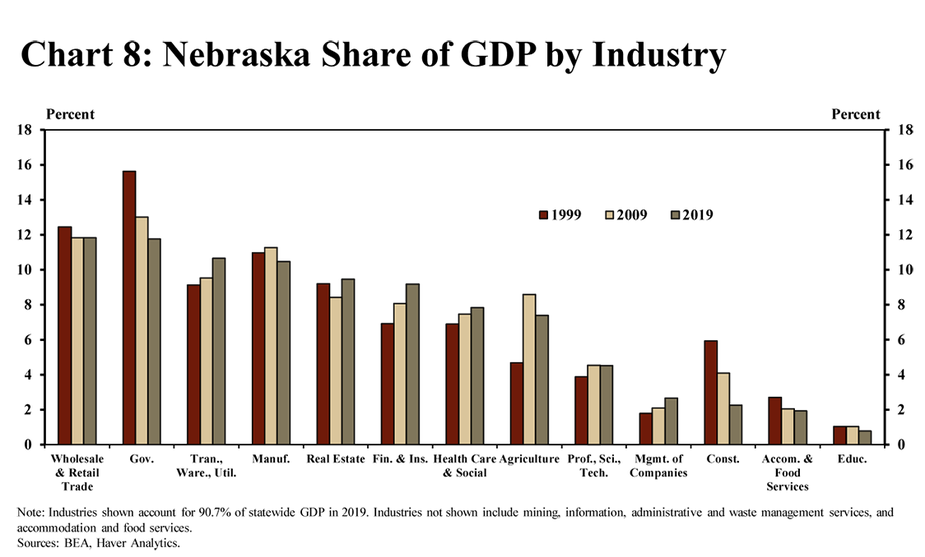

Similarly, economic output in Nebraska has also shifted over the past 20 years. In percentage terms, output from agriculture and the state’s finance and insurance industries has increased most significantly. Agriculture’s share of the economy increased from 4.7 percent in 1999 to a peak of nearly 10 percent in 2016, and declining slightly to 7.4 percent in 2019 (Chart 8). Similar to an increased employment concentration, the finance and insurance industry has increased its share of GDP in Nebraska by 2.3 percentage points. Outside of agriculture, other goods-producing industries (manufacturing and construction) accounted for a smaller share of Nebraska’s GDP in 2019 than in 1999.

Incomes

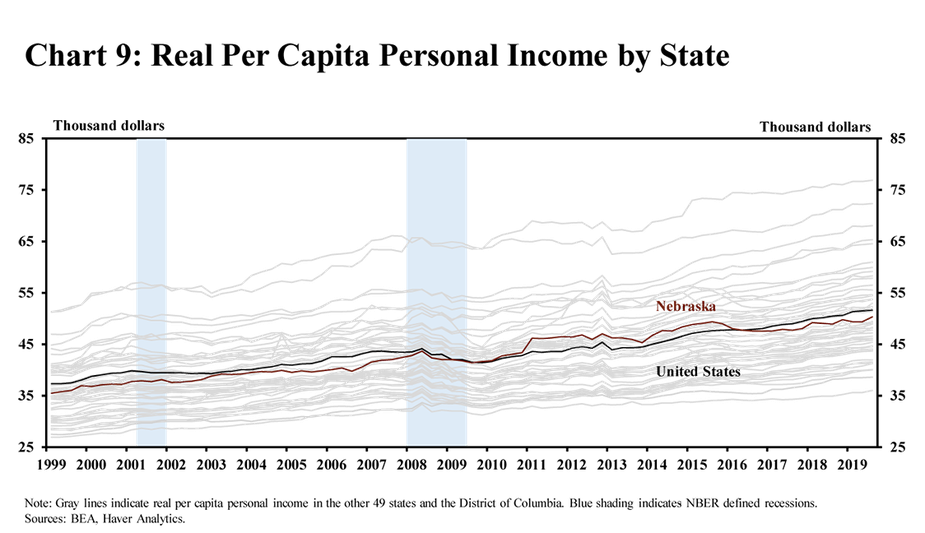

Personal income in Nebraska has increased steadily at a rate generally similar to that of the nation. In 1999, real per capita personal income in Nebraska was $35,516, and has increased to about $50,000 after adjusting for inflation. This increase of 41.7 percent, places Nebraska 19th among all states (Chart 9). Per capita income in Nebraska grew most significantly from 2010 to 2013 alongside a strong agricultural sector, but has softened more recently alongside weaker farm incomes.

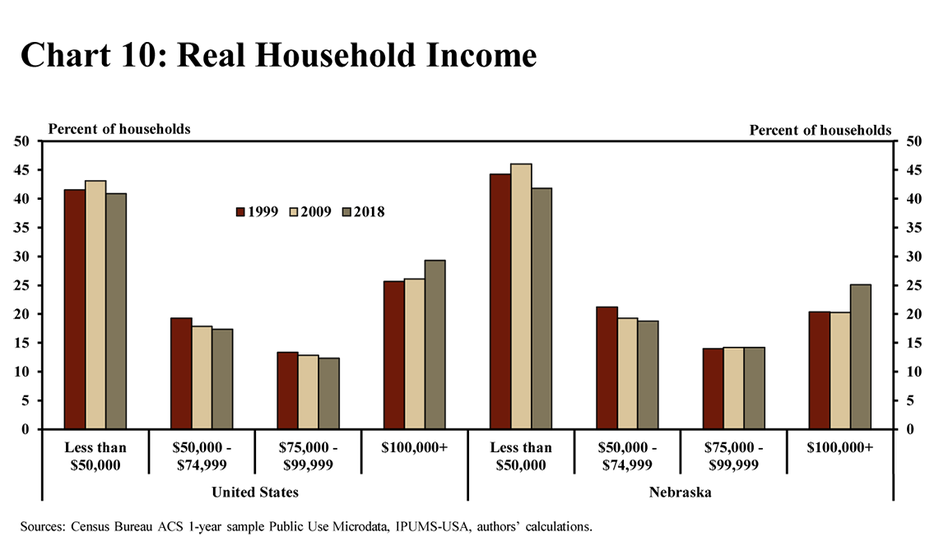

Although incomes generally have continued to increase in Nebraska, disparities have intensified somewhat alongside national trends. In 1999, only 20.4 percent of households in Nebraska earned more than $100,000 (Chart 10). In 2018 (the most recent data available), 25.1 percent of households reported income in excess of $100,000. A large number of households continued to earn less than $50,000 per year in 2018, with relatively little change in the percentage of households earning between $50,000 and $100,000.

Housing

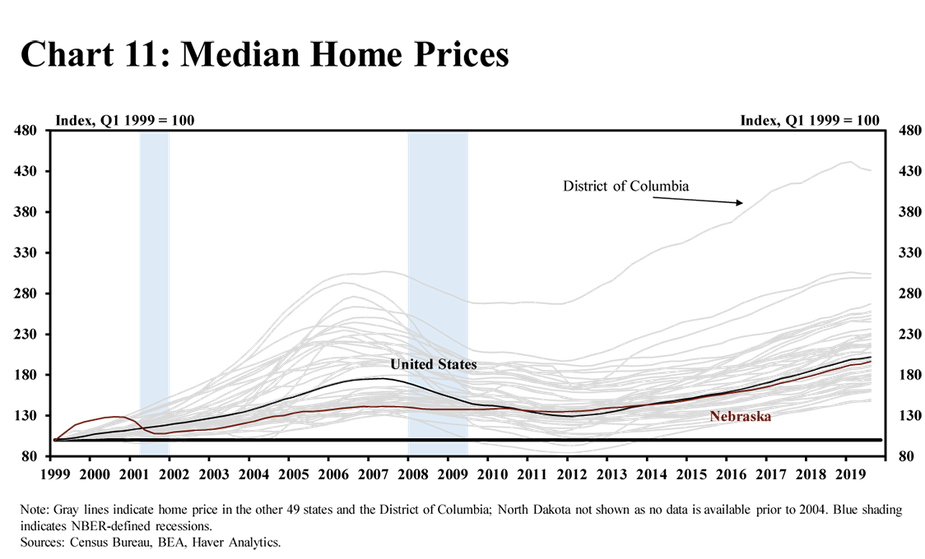

Home prices in Nebraska have continued to rise, and the pace has accelerated in recent years. Since the end of the 1990s, Nebraska’s median home price has increased 97 percent, or $83,000 (Chart 11). In the mid-2000s, and through the most recent recession, Nebraska’s housing market remained relatively stable in contrast to sharper fluctuations in other states. Since 2013, however, home prices in Nebraska have appreciated at a more rapid pace, growing 5.3 percent on average over the past seven years.

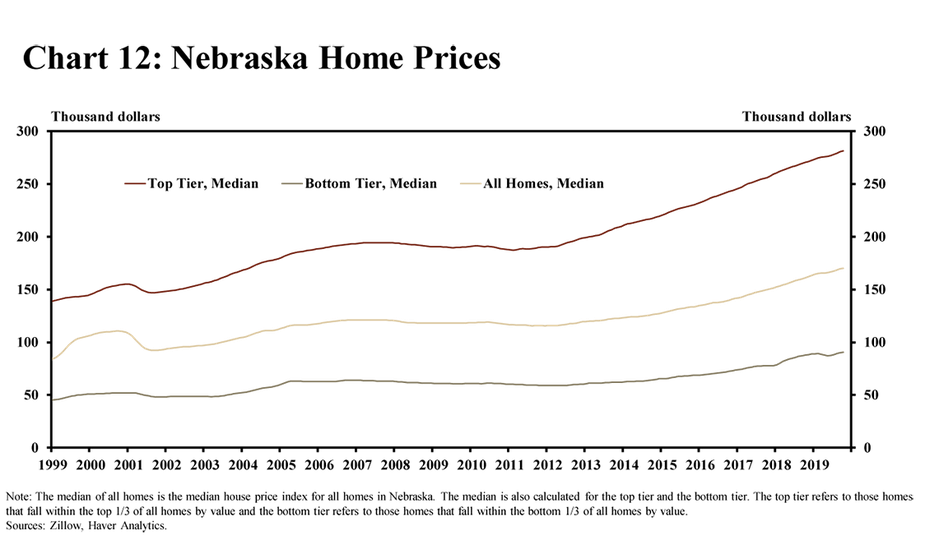

Notably, homes at all price levels have doubled in value over the past 20 years. Since 1999, both higher- and lower-priced homes have increased more than 100 percent even as homes at the higher end of the market have increased more in absolute value (Chart 12). For homes at all price levels, the most significant increases of the past two decades have occurred in the last seven years, and have provided a considerable boost to household wealth among homeowners.

Banking

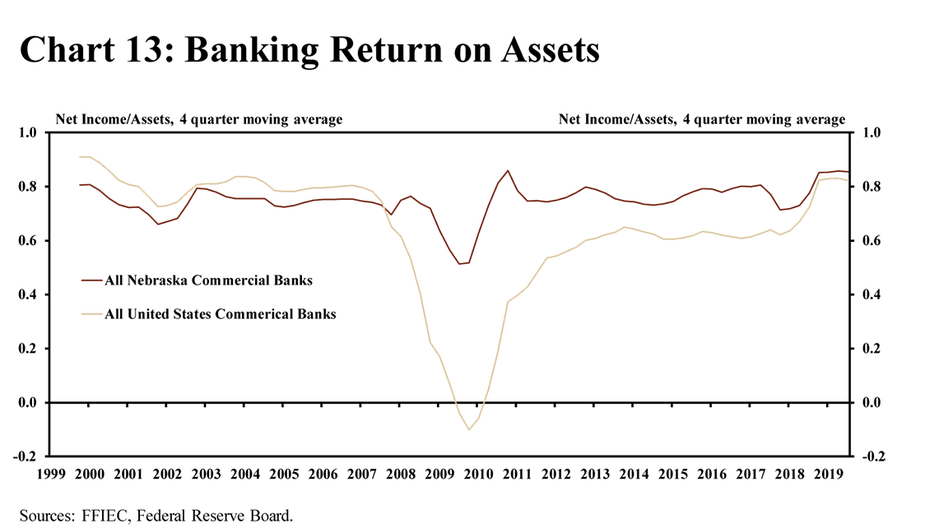

The relative strength and stability of Nebraska’s economy over the past two decades has supported returns in the state’s banking industry. The return on assets at commercial banks consistently has exceeded that of the nation since 2007 (Chart 13). Similar to the relative stability of Nebraska’s housing market during the last recession, returns at banks in Nebraska also declined only slightly, particularly when compared with banks nationally. Moreover, the rate of return at Nebraska banks through 2019 has been the strongest of the past two decades, with the exception of an initial post-recession rebound in 2010.

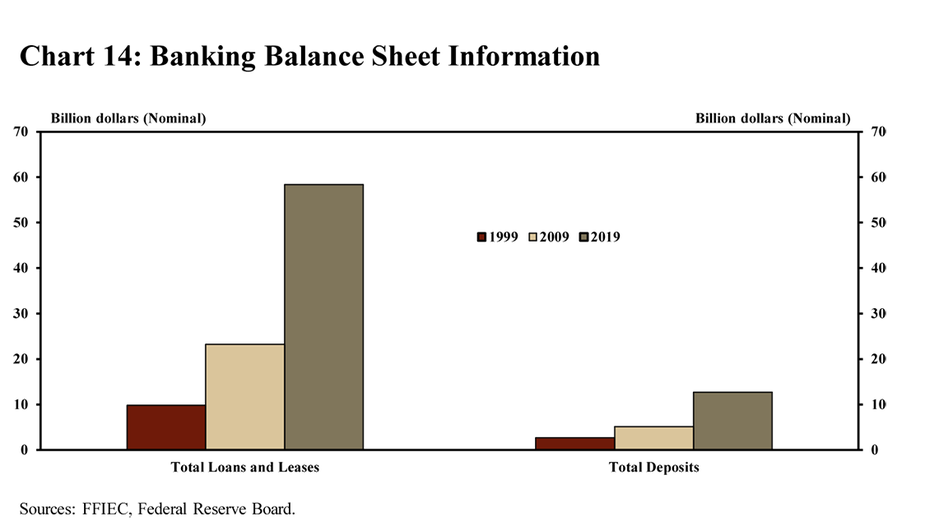

Financing activity at commercial banks in Nebraska also has increased significantly since the late 1990s. From 1999 to 2019, the total amount of loans and leases in Nebraska’s banking industry has increased from $9.8 billion to $58.4 billion, a gain of nearly 500 percent (Chart 14). Deposits also have grown significantly, though at a slightly slower pace than financing activity. Deposits at banks headquartered in Nebraska increased from $2.7 billion to $12.7 billion (377 percent) between 1999 and 2019.

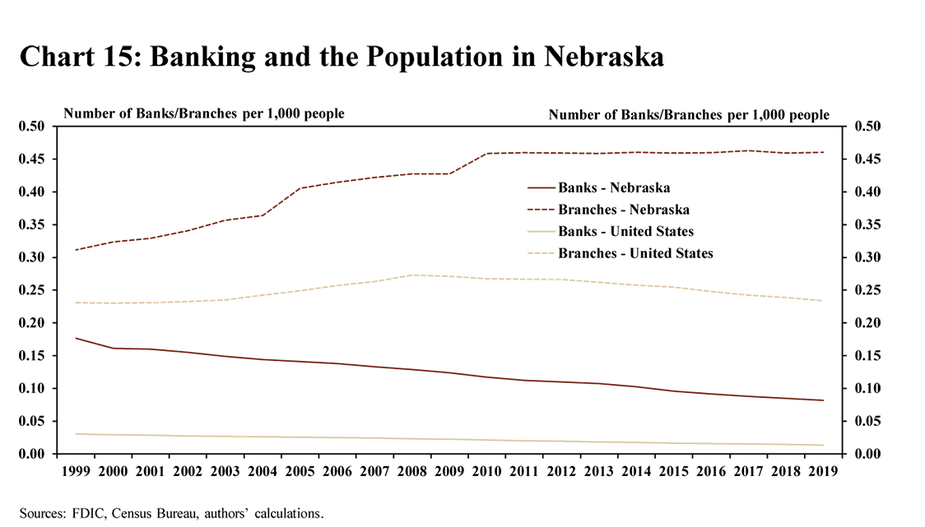

Strong returns among Nebraska’s financial institutions have resulted in an increased banking presence relative to the nation. The number of branches per 1,000 people in Nebraska has increased from 0.31 in 1999 to 0.46 in 2019 (Chart 15). Although the number of banks has declined, the increase in the number of bank branches has driven the increase in banking presence in the state. In contrast, the number of both banks and branches, nationally, has declined over the past two decades.

Agriculture

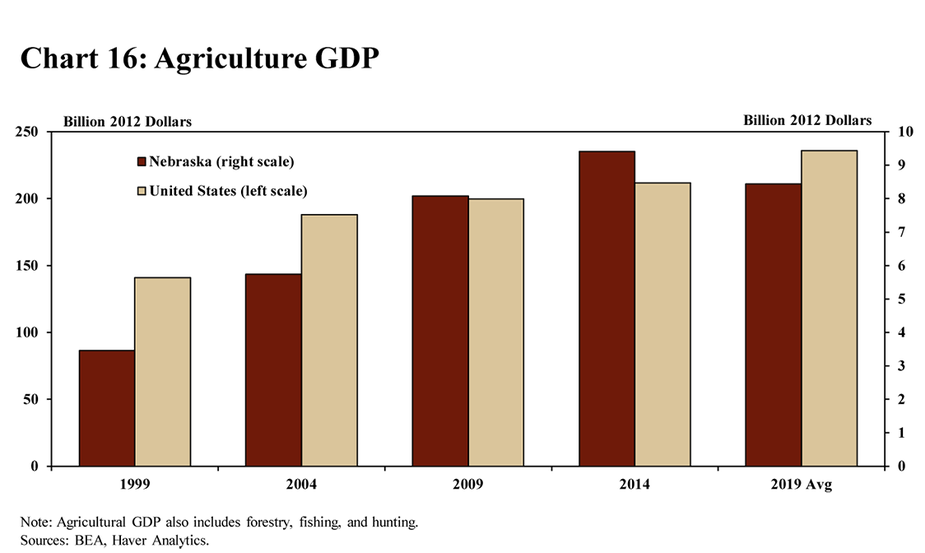

Many of Nebraska’s commercial banks provide financing for the state’s agricultural industry, which has expanded sharply since the 1990s despite a more recent slowdown. Agricultural output in Nebraska, measured by real GDP, has increased about $5 billion since 1999, a gain of 144 percent alongside rising global demand for food and agricultural products (Chart 16). Agriculture has also expanded throughout the nation, but the gains have been more pronounced in Nebraska and other states in the Midwest, which are highly concentrated in the production of bulk commodities such as corn and soybeans.

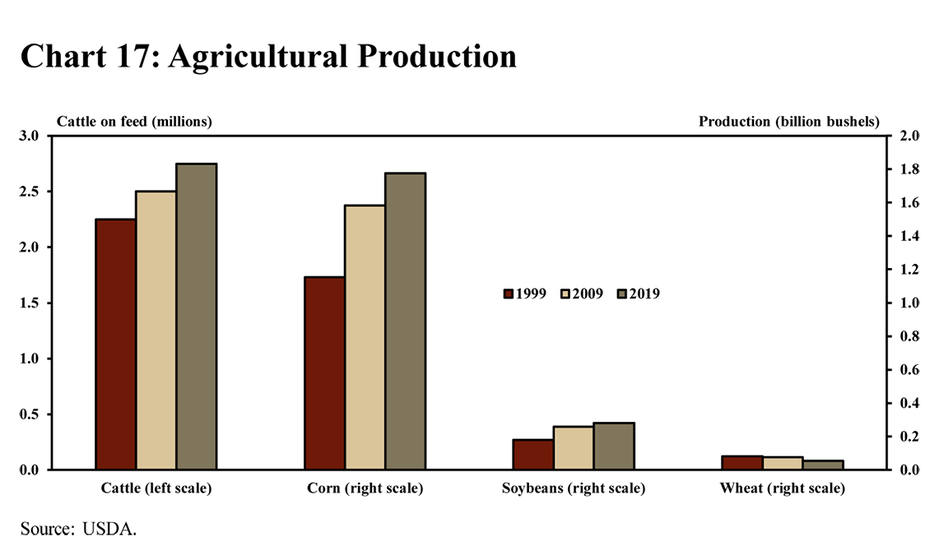

Nebraska has remained one of the nation’s most concentrated agricultural states, and production of several key commodities has increased significantly. In just 20 years, the number of cattle raised to produce beef in Nebraska has increased 500,000 (Chart 17). Alongside the increased global demand for meat products, in addition to the emergence of biofuels (i.e., ethanol), Nebraska’s production of corn also has surged more than 50 percent since 1999.

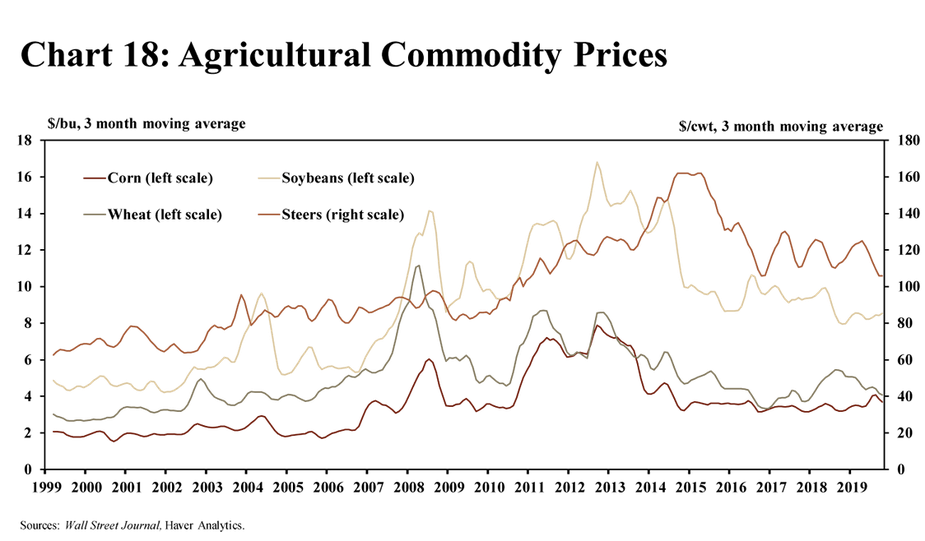

Although agriculture has remained a prominent industry, agricultural commodity prices have declined in recent years and continue to weigh on farm profits. After increasing more than 200 percent from 1999 to 2013, the price of corn has dropped 38 percent from those peaks (Chart 18). The prices of other major commodities, such as soybeans and wheat, also have declined sharply as production growth in recent years has surpassed growth in global consumption.

Manufacturing

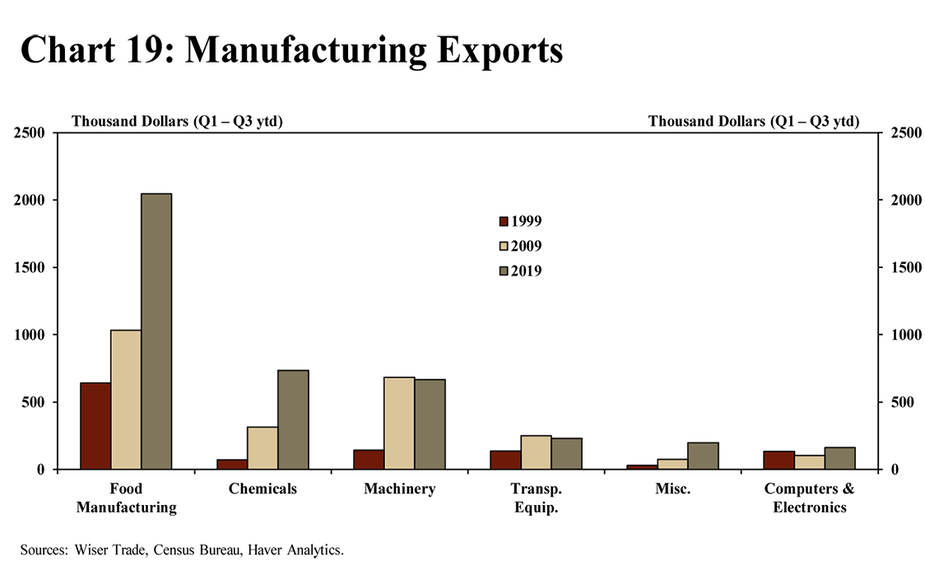

Fueled by ongoing demand for food and agricultural exports, Nebraska’s manufacturing sector has expanded in recent decades. In fact, Nebraska’s export of manufactured food products (which includes beef), has increased more than 200 percent since the late 1990s (Chart 19). Although food products have accounted for the largest growth among Nebraska’s manufactured exports, other categories, such as chemicals and machinery, also have seen significant increases.

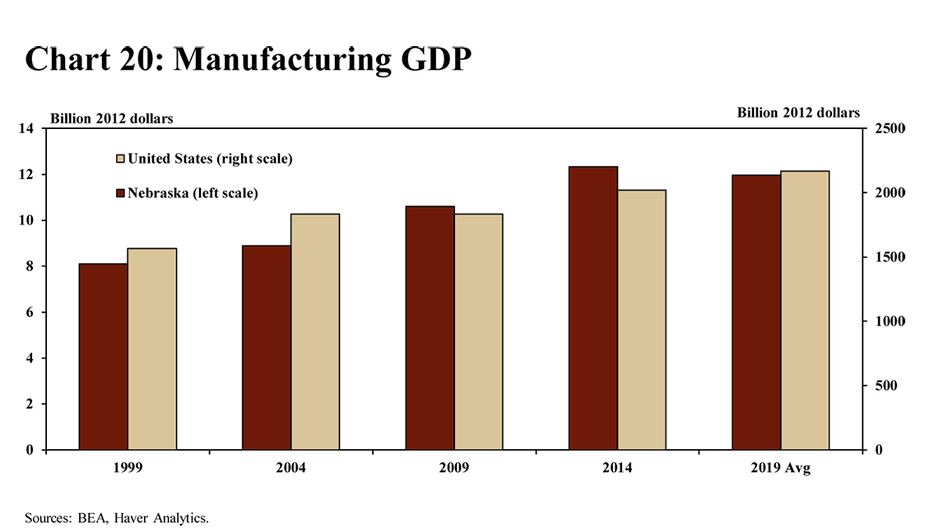

More broadly, manufacturing output in Nebraska has increased since the 1990s, despite a more recent slowdown in activity. Alongside ongoing challenges in agriculture, and manufacturing segments tied to agricultural prospects, manufacturing output in Nebraska has declined modestly since 2014 (Chart 20). Taking a longer view, however, real GDP attributable to the manufacturing sector has increased $3.9 billion since 1999. This increase, an average annual rate of 2.2 percent, has outpaced the nation despite the recent slowdown in Nebraska.

Exports

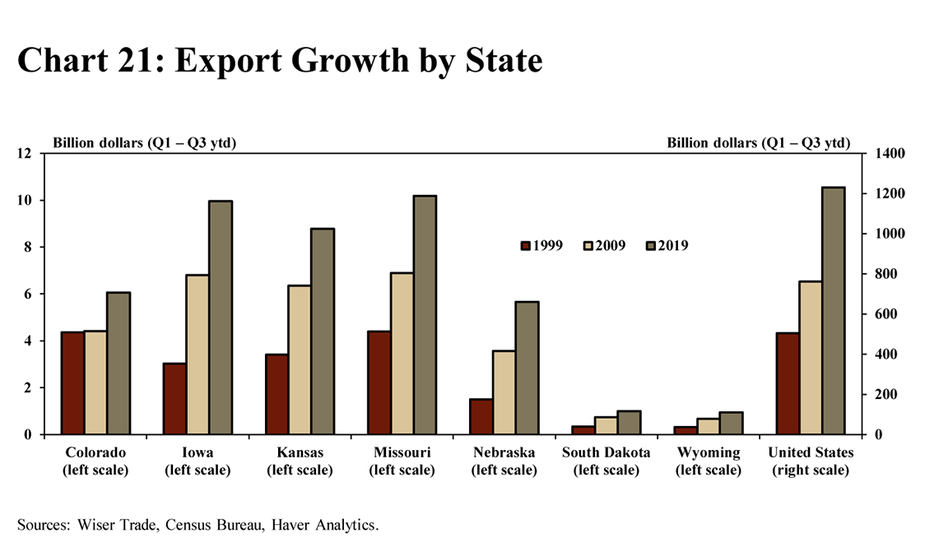

The long-term increases in agricultural and manufactured food product exports have been a primary contributor to a significant increase in total exports originating from Nebraska. Through the first three quarters of 2019, exports from Nebraska amounted to $5.7 billion, an increase of 274 percent since 1999 (Chart 21). This increase in exports has exceeded Nebraska’s neighboring states in percentage terms, and that of the United States more broadly.

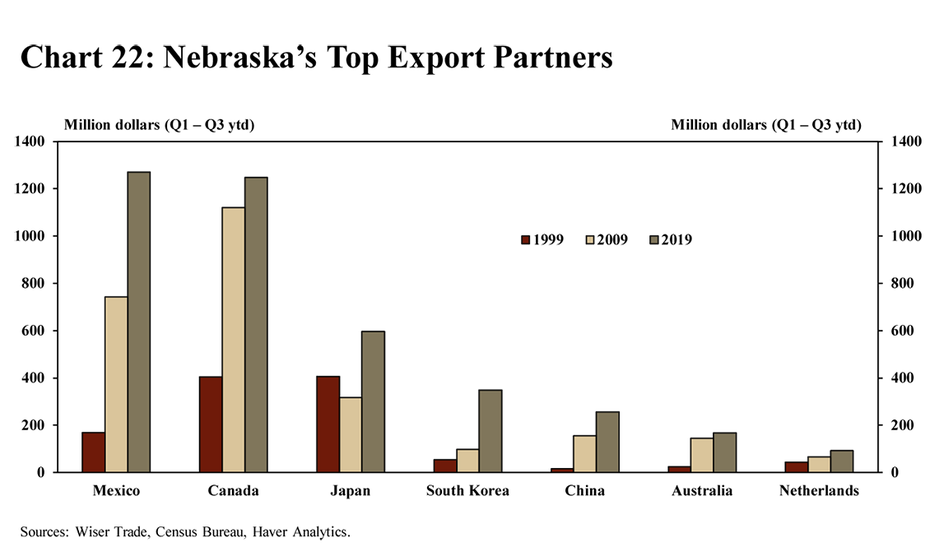

A sharp increase in exports to Mexico has been a primary factor behind the increase in shipments from Nebraska. From 1999 to 2019, exports to Mexico increased more than six-fold in addition to a significant increase in exports to Canada (Chart 22). In addition, exports to China increased from a negligible amount in 1999 to more than $200 million in 2019, placing China among Nebraska’s top five trading partners.

Conclusion

By many measures, Nebraska’s economy enters 2020 with a long-term trend of stable growth. Notwithstanding ongoing disparities within the state, this momentum appears likely to continue into the next decade, but will be heavily influenced by economic conditions both nationally and globally, particularly as it relates to trade developments and growth in export markets.

The views expressed in this article are those of the authors and do not necessarily reflect the views of the Federal Reserve Bank of Kansas City or the Federal Reserve System.

Author