Over the past two decades, the housing sector in the United States has experienced a boom, a bust, and the initial stages of a modest recovery. Between 1994 and 2005, residential construction activity tripled across the nation, while home prices nearly doubled. However, few forecasters predicted the severe magnitude of the bust in residential activity that soon followed. Residential construction fell more than 70 percent from peak to trough, home prices declined more than 20 percent, and mortgage foreclosures increased as more homeowners became “underwater” on their mortgages. In the years since the 2007-09 recession, the U.S. housing market has taken small steps toward recovery. Home inventories have gradually declined, home prices have stabilized and started to increase in many areas, foreclosure rates have fallen, and construction has picked up slightly. Improvements have been gradual, however, and residential construction activity remains below pre-recession levels in most areas of the nation. This issue of The Rocky Mountain Economist examines the boom, bust and recovery in the Mountain States’ housing markets over the past 20 years.

The Boom

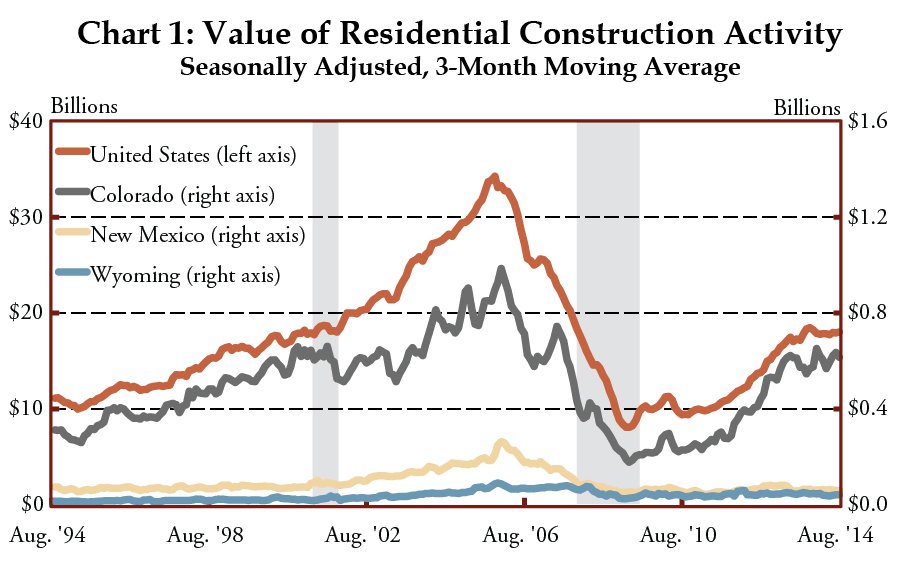

In the years leading to the 2007-09 recession, residential construction activity and the housing market across most of the nation experienced strong growth. Housing demand grew quickly as home ownership rates increased and housing was increasingly viewed as an investment. Residential construction activity also increased at a robust pace in response to rising demand and home prices. Chart 1 shows the value of residential construction activity over the past 20 years for the United States and the Mountain States.

In the United States and Colorado, residential construction activity rose at a fairly steady pace between 1994 and 2005. Colorado experienced a slight slump in residential construction during the 2001 recession as many technology-focused companies and the overall economy struggled. After a few volatile years following the 2001 recession, Colorado residential construction activity began growing again and quickly regained lost ground. The value of residential construction peaked in November 2005 in both the United States and Colorado after having tripled between 1994 and 2005.

The growth in residential construction activity in New Mexico and Wyoming was slower than that of the United States and Colorado between 1994 and 2001, and activity remained relatively flat. However, following the 2001 recession, New Mexico and Wyoming experienced faster residential construction growth, reaching peak levels in January 2006 and December 2005, respectively. Between 2001 and year-end 2005, residential construction increased at an average annual rate of more than 20 percent in New Mexico and Wyoming.

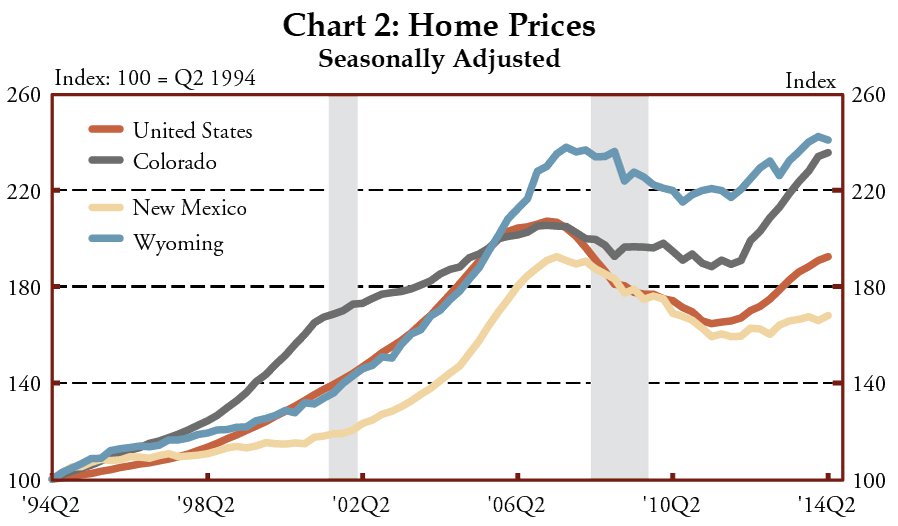

While residential construction was increasing, home prices were also steadily rising. Chart 2 shows the Federal Housing Finance Agency (FHFA) Purchase-Only House Price Index for the United States and the Mountain States. According to the FHFA House Price Index, average home prices approximately doubled in the United States and the Mountain States between the first quarter of 1994 and their pre-recession peaks in 2007. Between 1994 and 2001, Colorado home price appreciation outpaced New Mexico and Wyoming. However, following the 2001 recession, home-price increases moderated in Colorado, while gains in home prices in New Mexico and Wyoming accelerated. Between 1994 and 2007, average home prices increased at annual rates of 6.1, 6.0, 5.1 and 6.6 percent in the United States, Colorado, New Mexico and Wyoming, respectively. In the decade prior to the recent recession, the housing sector was booming in the United States and the Mountain States, yet few people predicted the magnitude of the following downturn.

The Bust

During the boom years, new residential construction and home prices experienced robust growth. However, near year-end 2005, the value of residential construction reached its peak and began to decline, with construction levels eventually falling more than 70 percent in the United States and the Mountain States (Chart 1). Shortly after new residential construction started to decrease, home prices began to fall in the first half of 2007 (Chart 2).

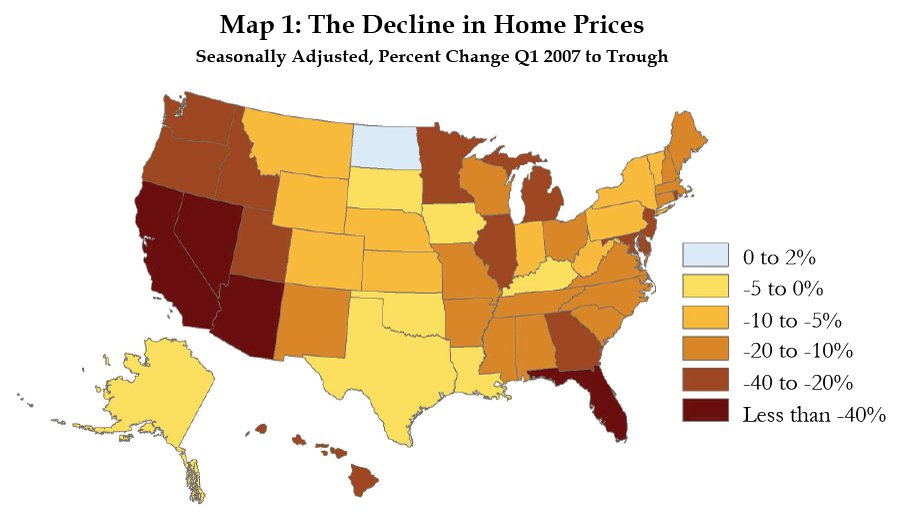

Most states experienced a sharp drop in home prices after the start of the recession. Map 1 shows the percentage drop in home prices between the first quarter of 2007 (the national peak in home prices) and each state’s trough in prices. Home prices fell 20.1 percent across the nation on average between the first quarter of 2007 and the second quarter of 2011. Home prices were hit particularly hard in Florida and the Western States, where Nevada led the nation with a decline of 58.5 percent. The Mountain States fared better than the nation, with home-price declines of 8.4, 16.6 and 6.4 percent in Colorado, New Mexico and Wyoming, respectively.

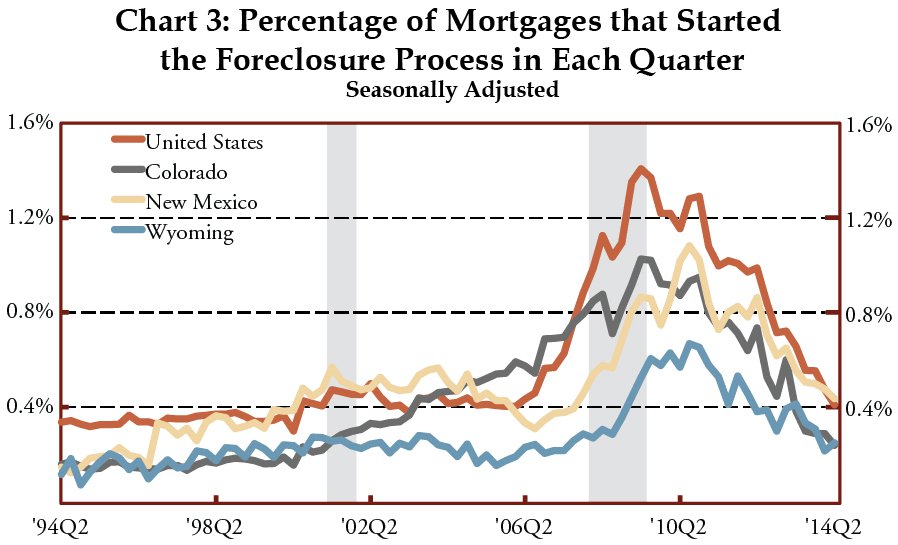

For many households, the decline in home prices led to a decline in household wealth, leaving many homeowners “underwater”—owing more on their mortgage than the new value of their home. The increase in homeowners underwater on their mortgages and the rise in alternative types of mortgage financing—including subprime—led to an increase in mortgage defaults. Chart 3 shows the percentage of mortgages during each quarter that went into foreclosure.

In the United States, New Mexico and Wyoming, mortgage foreclosures were relatively flat in the years leading to the recession. Foreclosures in Colorado started to increase around the 2001 recession and maintained an upward trend to their peak in the third quarter of 2009. Foreclosures in New Mexico, Wyoming and the United States began to climb around 2006. At their peak, the percentage of mortgages that entered foreclosure each quarter in the United States, Colorado, New Mexico and Wyoming reached 1.4, 1.1, 1.1 and 0.7 percent, respectively.

The Recovery to Date

More than five years after the end of the 2007-09 recession, the housing market has shown some initial signs recovery. Foreclosures have returned to pre-recession levels, and home prices have started to increase. In Colorado and Wyoming, home prices have surpassed their previous peaks. As of the second quarter 2014, Colorado and Wyoming are above previous peak values by 14.8 and 1.3 percent, respectively. Home prices in New Mexico, while slower to recover, have started to pick up, rising 5.5 percent from trough levels. Prices, however, remain 12.2 percent below peak levels. Similarly, home prices have been increasing on average across the United States, but remain 7.2 percent below peak values.

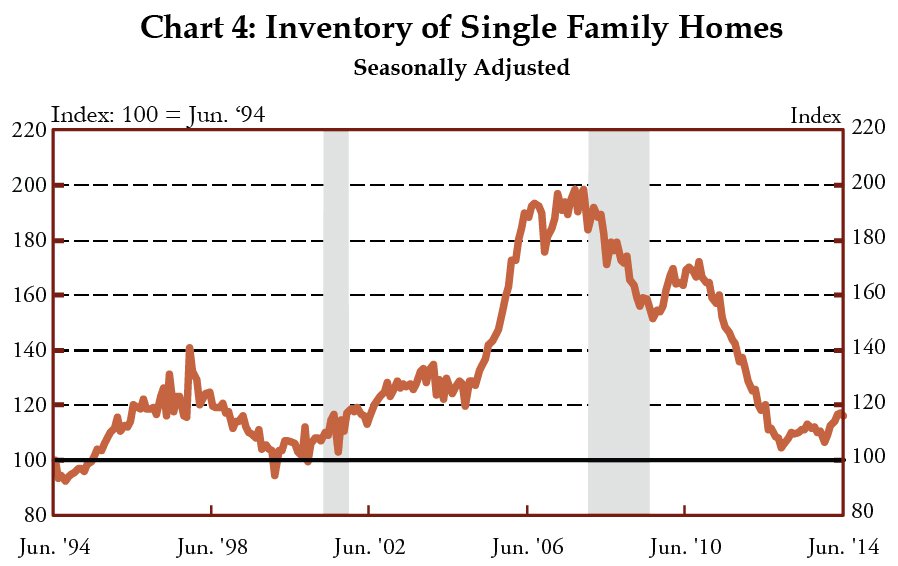

After a sharp rise in home inventories in the years before the recession, inventories of single-family homes for sale have fallen since 2008 (Chart 4). As inventories decline, the housing market is moving toward equilibrium, where the number of homes for sale meets the demand of potential buyers in the market. In parts of the country, the housing market has shifted from a buyer’s market (one with an excess supply of homes for sale) to a seller’s market (one with too few homes for sale). This dynamic has led to higher home prices in these areas.

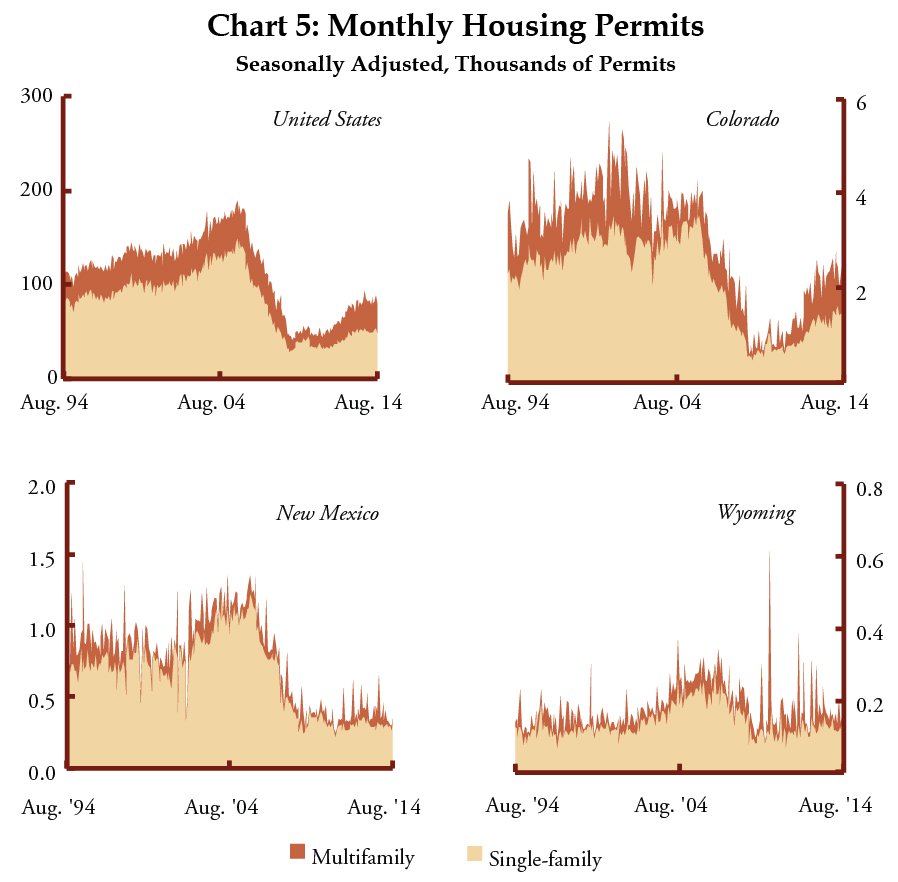

With inventories falling and home prices rising, residential construction and permitting activity has gradually increased (Chart 5), particularly in Colorado and the nation. Residential permitting has been slower to pick up in New Mexico and Wyoming. Across the three states and nation, however, residential permitting activity remains well below pre-recession levels. Single-family construction has been slower to bounce back than multifamily construction and although single-family permits still comprise the majority of total permits, the share of multifamily permits has steadily increased over the last several years. Growth in multifamily permitting has been particularly noteworthy in Colorado, where the share has increased from 10 percent in the first half of 2005 to almost 36 percent in the first half of 2014. Despite the post-recession growth of multifamily permits, both multifamily and total housing permits remain below pre-recession highs.

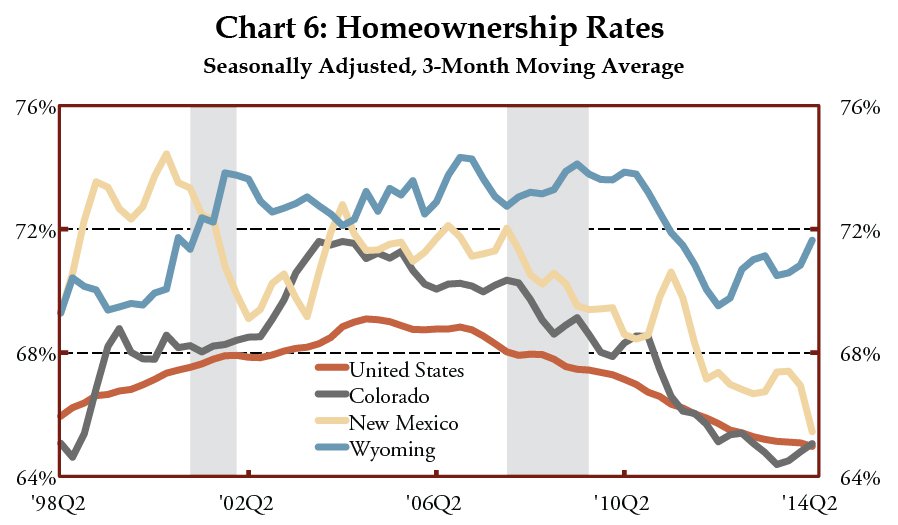

One reason for the strong increase in multifamily construction is the decline in homeownership rates across the United States and the Mountain States since the housing market began to cool (Chart 6). As of the second quarter 2014, homeownership rates for the United States, Colorado and New Mexico have continued to decline from pre-recession levels. Wyoming, however, has recently experienced an uptick in homeownership rates. The decreases in homeownership rates reflect a decline in household formation and a larger trend of Americans increasingly shifting toward rental units. Many factors lead consumers to rent rather than own. The severity of the recent recession and the nationwide decline in home prices has lowered the desire of many people to buy a home and left others unable to buy a home either because of scarred credit histories or tighter credit standards.

Overall, both monthly housing permits (Chart 5) and new residential construction activity (Chart 1), both leading indicators of future housing supply, have been slow to recover despite rising home prices and a declining inventory of homes available for sale. However, pre-recession peaks of housing inventory and construction appear to have been at unstable and speculative levels, and thus a return to pre-recession activity may not be healthy for the housing market nor the economy overall. Furthermore, housing demand and homeownership rates also remain below pre-recession peaks and may remain lower in the future due to demographic trends, reduced appetites for home ownership and tighter lending standards. In general, the severity of the recent downturn in the housing market may have lasting effects on many potential homeowners, investors, and construction-related businesses.

The views expressed are those of the authors and do not necessarily reflect the positions of the Federal Reserve Bank of Kansas City or the Federal Reserve System.

Authors

Alison Felix

Senior Policy Advisor