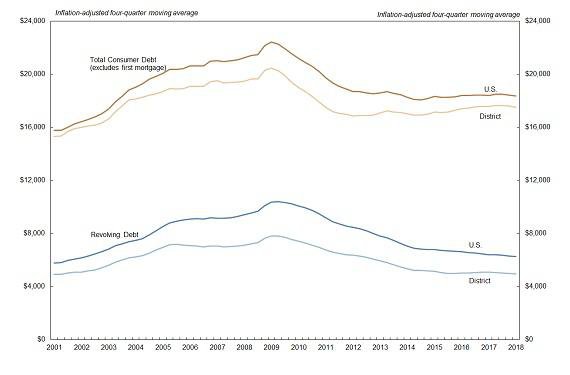

Download Article| Average consumer debt for the Tenth District, defined for this report as all outstanding debt other than first mortgages and presented as a four-quarter moving average, grew from $16,588 in the first quarter of 2016 to $16,904 in the third quarter of 2016—an increase of 1.9 percent (Chart 1).1 Over the same period, consumer debt nationally was up 1.4 percent to $17,758.

From its post-recession low in the first quarter of 2012, average consumer debt in the District has increased at an annual rate of 2 percent. National average consumer debt over the same period increased at an annual rate of 0.8 percent. Thus, the gap between District consumer debt and national consumer debt in recent years has narrowed significantly. However, growth in District consumer debt was much slower than it was before the recession (2004 to 2009), when average consumer debt increased at an annual rate of 4.9 percent.

Chart 1: Outstanding Consumer Debt per Consumer and Revolving Debt per Consumer

The recent increase in District consumer debt is consistent with increases in employment and income. Higher incomes and more stable labor markets may make households more secure in their borrowing decisions and better able to service debt.2 Moreover, higher incomes may loosen credit constraints. Research suggests income is the most significant determinant of a household’s unsecured borrowing limit.3 Other, sometimes confounding factors, however, can alter the relationship between income and the accumulation of debt, which do not always move together. For example, in hard times, some may use debt to pay for basic necessities.

District average revolving debt, largely credit cards and home equity lines of credit (HELOCs), continued to tick up over the last two quarters, reaching an average of $4,853. After falling consistently from the second quarter of 2009, average revolving debt in the District over the last year has increased 2.5 percent. Still, District revolving debt remains 27 percent below its recession-era peak. Almost all consumers (with credit reports) have credit cards, while about 6 percent have open HELOCs.

Total consumer debt continues to increase faster than revolving debt, which implies installment debt (other than first mortgages) has increased more significantly than other forms of debt—particularly auto loans and student loans. Over the past year, average student loan debt (per consumer with student loan debt) increased about 6 percent to $28,487 in the District and $30,059 in the nation (Chart 2). Growth in auto debt balances (per outstanding loan) in the last year has slowed to 2.5 percent in the District and 2.8 percent in the nation.

Chart 2: Outstanding Auto and Student Loan Debt per Borrower

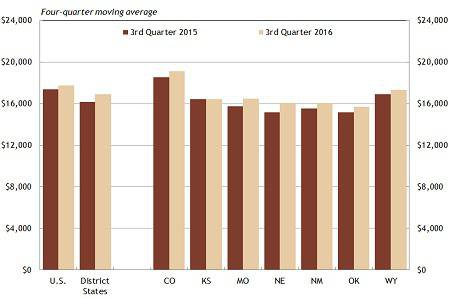

Average consumer debt varied significantly across District states, from $15,715 in Oklahoma to $19,199 in Colorado (Chart 3). Coloradans consistently carry more debt than consumers in other District states, likely due in part to a higher cost of living—especially for housing—and above-average incomes.4 Socioeconomic factors also contribute to the variation in average debt across states and time, including demographics, cultural differences, trends in financial intermediation and public policy.5

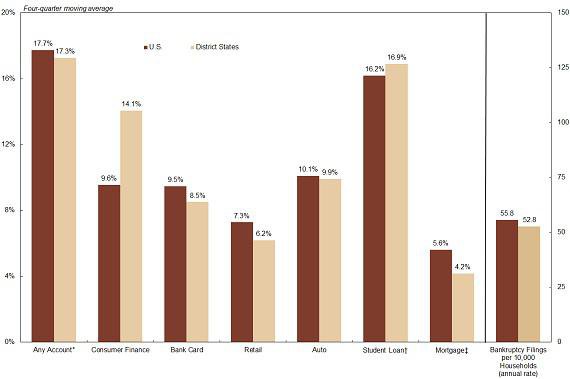

Overall credit delinquency in the third quarter of 2016 was 3.6 percent in the District, down from 3.8 percent in the third quarter of 2015 and significantly lower than the U.S. rate of 4.4 percent (Chart 4). Except for student loans, delinquencies are calculated as a share of open trade lines, or accounts.6 For example, bank card delinquency expresses the share of bank cards delinquent 30 days or more. The District’s lower overall delinquency rate is attributable largely to lower mortgage delinquency rates in District states. The District rate for mortgage delinquency (30 or more days past due, including foreclosure) of 5.1 percent in the third quarter was down significantly from 5.7 percent in the third quarter of 2015 and well below the U.S. rate of 6.3 percent.7 The U.S. rate also was down significantly from 7.1 percent in the third quarter of 2015.

The District delinquency rate on consumer finance loans dropped significantly to 12.6 percent in the third quarter from 14.2 percent in the third quarter of 2015, but remained significantly higher than the U.S. rate of 8.8 percent. As noted in the December 2015 issue of the Tenth District Consumer Credit Report, the District’s higher delinquency rate has been driven by very high delinquency rates in Missouri (14.6 percent), New Mexico (18 percent) and Oklahoma (21.4 percent). Many factors help explain specifically the level of debt and delinquency across states and time and more generally for consumer lending. The consumer finance sector is less regulated than most lending sectors, even for other closed-end installment loans.8 Variation in consumer law and policy by state is significant and is one factor in the variation of states’ consumer finance delinquency rates.9 The wide discrepancy in delinquency rates on consumer finance accounts is highlighted by Nebraska’s rate of just 3.5 percent.

Chart 3: Outstanding Consumer Debt per Consumer

Chart 4: Consumer Credit Delinquency Rates and Bankruptcy Filings

Auto delinquencies (expressed as share of accounts) continued to increase through the third quarter, rising to 8.3 percent. Auto loans to subprime borrowers recently have shown moderately faster growth than auto loans to prime borrowers, which may push the auto delinquency rate higher in the near term.10 The student loan delinquency rate rose 0.3 percentage point to 16.7 percent in the District, slightly higher than the national rate of 16.2 percent. The student loan delinquency rate includes all loans in the denominator, many of which are not in active repayment, such as those in deferment or forbearance.11 The inclusion of loans not in repayment results in a much lower delinquency rate. If only loans in repayment are considered, the delinquency rate in several states exceeds 30 percent.12 This subject will be discussed in more detail in the next issue of this report. Delinquencies on retail loans ticked up from the third quarter to 3.9 percent.

In This Issue: Credit Card Balances

Credit card balances can be an important indicator of financial decision-making and financial health. Credit cards typically are unsecured and carry higher interest rates than most other traditional forms of consumer credit. In the third quarter, average credit card interest rates ranged from 13.1 percent for those with “excellent credit” to 21.5 percent for those with “fair credit.”13 The average “penalty” rate for those with late/missing payments was 28 percent. Credit cards also carry non-interest penalty fees for late payments, cash advances and over-the-limit purchases; some have annual fees.

If consumers pay their balances in full every billing cycle, no interest is charged on purchases. The American Bankers Association (ABA) classifies these accounts as “transactor” accounts.14 Transactor accounts show balances in the quarter but no finance charges in any month during the quarter. In August 2016, the ABA reported 28.8 percent of bank credit card accounts were transactor accounts (they did not evaluate retail credit card accounts). “Revolvers,” those who roll over at least part of their balances into the following month, accounted for 43.6 percent of bank credit card accounts in August. The remainder of accounts was “dormant” (no activity in the quarter).

Credit cards can offer great value in facilitating purchase transactions and providing a relatively low-cost vehicle for short-term, small-dollar loans, but most personal finance specialists would agree that continuously rolling over credit card debt is not a sound financial decision for most people.15 In addition to the cost, the availability of a credit card has been shown to significantly increase impulse and compulsive buying.16 Some consumers find themselves with seemingly insurmountable debt and/or have difficulty making payments.17 In a 2014 survey of consumers, 20 percent of respondents reported that “accumulating too much debt,” commonly citing credit card debt specifically, is their biggest financial regret.18 The most common cause (33 percent) of bankruptcy cited by filers is “high debt/misuse of credit cards.”19

There are a number of rationales for rolling over credit card debt. Debt may stem from an emergency expense or other necessary expense that exceeds the borrower’s ability to pay in one billing cycle. Other cases, however, result from being a “spendthrift” or having problems with self-control.20 Interestingly, a number of analyses of personal financial data, typically from surveys, find a substantial share of consumers who roll over credit card balances also have sizeable balances in cash or other financial assets in low-earning accounts. These low-earning assets could be used to pay down high-cost debt. A number of rationales have been offered to explain this “puzzle.”21 One possibility is that the cash holdings are already committed to future purchases. Other rationales include a desire to maintain liquidity for future cash-only purchases or insurance against credit shocks.22

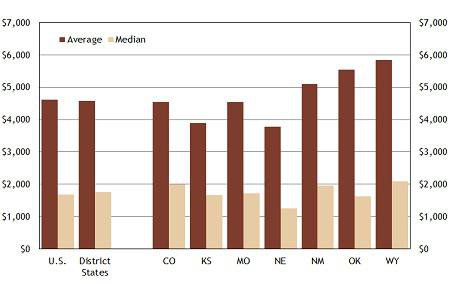

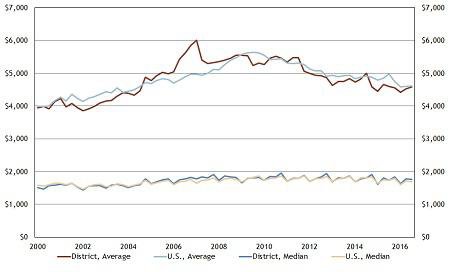

Chart 5 shows average and median bank credit card balances for the United States, Tenth District overall and Tenth District states using data from the New York Fed Consumer Credit Panel/Equifax (CCP). The statistics are for credit card holders (excluding retail cards) who had a balance in the third quarter of 2016. Average credit card debt per consumer with credit card debt was $4,583 for District states and $4,617 nationally. Median credit card debt was $1,761 and $1,685, respectively. Median debt is arguably more representative of a typical consumer because even a small share of credit cards with massive balances would pull up the average significantly but should not affect the median. These values are roughly consistent with data from the Federal Reserve’s 2013 Survey of Consumer Finances, which showed average credit card debt of those with balances was $5,700, while the median was $2,300.23 The calculated average is also consistent with Experian’s 2015 estimate of $4,400.24

Chart 5: Average and Median Credit Card Balances Across District States (Third Quarter 2016)

Average credit card debt varies significantly across District states, from $3,779 in Nebraska to $5,834 in Wyoming. Surprisingly, average credit card debt does not appear to be well correlated with average consumer debt across the District, as shown in Chart 2. In the third quarter, District states with the highest average balances also were struggling the most economically, largely from the energy downturn: New Mexico, Oklahoma and Wyoming. Credit card debt increased 10.6 percent in Oklahoma in the past year and 9.1 percent in New Mexico. The average credit card balance in Wyoming grew at a more moderate rate of 3.8 percent, but still well above the District rate of 1.8 percent.

Average credit card balances increased steadily prior to the financial crisis in both the District and the nation (Chart 6). From the first quarter of 2002 until the financial crisis began in the fourth quarter of 2007, average credit card debt increased 32.4 percent in the District and 23.8 percent in the nation. Average credit card debt since 2008 has fallen 7.7 percent in the District and 7.1 percent in the nation. These trends are consistent with other consumer debt trends presented earlier in this report and in Charts 1 and 2.

Although average credit card debt shows a familiar pattern for those who have followed consumer credit trends, particularly in the Tenth District Consumer Credit Report, median credit card debt has a very different pattern. Specifically, the trend in median debt in the last 15 years is flat. Moreover, District and U.S. medians are roughly identical and over time have followed nearly identical patterns. The data suggest a small fraction of credit card users largely is responsible for volatility in credit card balances and reports of high credit card debts.

Chart 6: Average and Median Credit Card Balances Over Time (For Those With a Balance)

Endnotes

[1] Statistics in this report are derived from data in the Federal Reserve Bank of New York Consumer Credit Panel/Equifax, unless otherwise indicated. The data consist of a 5 percent sample of Equifax credit reports, which are devoid of any information that could be used to identify individuals. Average consumer debt is calculated by dividing the aggregate consumer debt of those in the credit report sample by the number of individuals in the sample. Credit and debt statistics can be calculated many ways, and thus these statistics may not be comparable to similar statistics published elsewhere, including by other Federal Reserve Banks. The Tenth District includes Colorado, Kansas, western Missouri, Nebraska, northern New Mexico, Oklahoma and Wyoming. In many cases, this report uses data from all of Missouri and New Mexico, in which case the label for the region is “District States.”

[2] See Jonathan Cook, 2001, “The Demand for Household Debt in the USA: Evidence from the 1995 Survey of Consumer Finances,” Applied Financial Economics, vol. 11, no. 1, pp. 83-91.

[3] Kyoung Jin Choi, Hyeng Koo, Byung Hwa Lim and Jane Yoo, 2015, “The Determinants of Unsecured Credit Constraint,” Sept. 8. Available at External Linkhttp://dx.doi.org/10.2139/ssrn.2657352.

[4] In the case of credit cards, for example, see “Cost of Living and Debt, State by State,” NerdWallet, Dec. 9, 2015. Available at External Linkhttps://www.nerdwallet.com/blog/credit-cards/cost-of-living-debt-metros-states/. See also Erin El Issa, “2015 American Household Credit Card Debt Survey,” NerdWallet, undated. Available at External Linkhttps://www.nerdwallet.com/blog/credit-card-data/average-credit-card-debt-household/. The analysis used data collected in an online Harris poll of 2,000 adults.

[5] See, for example, Basak Kus, 2015, “Sociology of Debt: States, Credit Markets, and Indebted Citizens,” Sociology Compass, vol. 9, no. 3, pp. 212-223; Thomas Durkin et al., 2015, Consumer Credit and the American Economy (Oxford University Press USA).

[6] The number of people who have student debt is used as the divisor because some borrowers may have up to 20 student loan accounts. Average loan balance per account would be a deceptively low number with little value. Delinquency is often reported as the share of balances that is delinquent. See, for example, Federal Reserve Bank of New York, Quarterly Report on Household Debt and Credit, May 2016. Available at External Linkhttps://www.newyorkfed.org/microeconomics/data.html. The purpose of this report is to look at a typical consumer, making per person (for debt) or per account (for delinquency) calculations most relevant.

[7] Lender Processing Services Inc. [datafile].

[8] In a closed end loan, the full loan amount is disbursed when the loan closes. Mortgages and auto loans typically are closed-end loans.

[9] See National Consumer Law Center, July 2015, “Installment Loans: Will States Protect Borrowers from A New Wave of Predatory Lending,” available at External Linkwww.nclc.org/images/pdf/pr-reports/report-installment-loans.pdf. While not necessarily the primary cause of District differences in delinquency rates for consumer installment loans, the states with the highest delinquency rates also are among the states with the most generous terms to lenders. Missouri and New Mexico are among the eight states with no cap on interest (New Mexico has a deceptive practices statute); the annual percentage rate (APR) in Oklahoma is capped at 116 percent, the highest among states that cap APR. Research suggests higher interest rates are associated with higher risk of default. See, for example, Jose Angelo Divino, Edna Souza Lima and Jaime Orrillo, 2013, “Interest Rates and Default in Unsecured Loan Markets,” Quantitative Finance, vol. 13, no. 12, pp. 1925-1934.

[10] See Tenth District Consumer Credit Report, Federal Reserve Bank of Kansas City, June 9, 2016. Available at https://www.kansascityfed.org/publications/community/consumer-credit-reports.

[11] Deferment allows borrowers to stop making loan payments if they are enrolled in school at least half time; currently serving on active duty; engaged in a full-time rehabilitation training program; or in cases of economic hardship, including unemployment, receipt of public assistance; Peace Corps service; and certain income limitations.Forbearance allows those who do not qualify for a deferment to stop making student loan payments, temporarily make smaller payments, or extend the time for making payments. Common reasons for forbearance listed, according to the Department of Education, are illness, financial hardship, or serving in a medical or dental internship or residency. A forbearance can be granted automatically while processing a deferment, forbearance, cancellation, change in repayment plan, or consolidation, or if the borrower is involved in a military mobilization or emergency. Interest does not accumulate under deferment, while it does under forbearance.

[12] See Wenhua Di and Kelly D. Edmiston, 2015, “State Variation of Student Loan Debt and Performance,” Suffolk University Law Review, vol. 48, no. 3, pp. 661-688.

[13] Alina Comoreanu, 2016, “2016 Credit Card Landscape Report,” WalletHub, Sept. 28. Available at External Linkhttps://wallethub.com/edu/credit-card-landscape-report/24927/.

[14] American Bankers Association, Credit Card Monitor, August 2016.

[15] See, for example, Cliff A. Robb and Deanna L. Sharpe, 2009, “Effect of Personal Financial Knowledge on College Students’ Credit Card Behavior,” Journal of Financial Counseling and Planning, vol. 20, no.1, pp. 25-43 (in particular, p. 29).

[16] See, for example, Wan-Rung Lin, et al., 2013, “The Effect of Credit Card on the Compulsive Buying Behavior Intention,” Journal of Accounting, Finance & Management Strategy, vol. 8, no. 2, pp. 45-74.

[17] See, generally, Pew Charitable Trusts, “The Complex Story of American Debt: Liabilities in Family Balance Sheets,” July 2015. Available at External Linkhttp://www.pewtrusts.org/~/media/assets/2015/07/reach-of-debt-report_artfinal.pdf.

[18] The survey was conducted by Op4G for Money-Rates. For additional details, see Erika Rawes, 2014, “Top 5 Money Problems Americans Face,” USA Today, Sept. 20 or External Linkhttp://money-rates.com.

[19] Michelle J. White, 2009, “Bankruptcy: Past Puzzles, Recent Reforms, and the Mortgage Crisis,” American Law and Economics Review,” vol. 11, no. 1, pp. 1-23. Credit card debt could mask some more fundamental drivers of bankruptcy, such as medical costs paid with a credit card or living expenses paid with a credit card by an unemployed worker. A 1996 question in the Panel Study of Income Dynamics, a well-known and commonly used data source for analysis of personal and family finances, asked respondents if they had ever filed for bankruptcy, and if so, what was the primary reason for filing. Only 21 percent claimed job loss and 16 percent claimed medical issues (Michelle J. White, 2007, “Bankruptcy Reform and Credit Cards,” Journal of Economic Perspectives, vol. 21, no. 4, pp. 175-199). Although a large number of, indeed most, sources suggest medical debt is the chief driver in a majority of bankruptcies, more sophisticated analyses that identify causation (as opposed to simple correlation) find the share to be well below 20 percent. See David Dranove and Michael L. Millenson, 2006, “Medical Bankruptcy: Myth versus Fact,” Health Affairs, vol. 25, no. 2, pp. 74-83.

[20] Unsurprisingly, individuals with “present-biased time preferences” (value the present much more than the future, nearsighted) are more likely to have credit card debt and have significantly higher amounts of credit card debt (Stephan Meier and Charles Spenger, 2010, “Present-Biased Preferences and Credit Card Borrowing,” American Economic Journal: Applied Economics, vol. 2, no. 1, pp. 193-210).

[21] Olga Gorbachev and María José Luengo-Prado, 2016, “The Credit Card Debt Puzzle: The Role of Preferences, Credit Risk, and Financial Literacy,” Federal Reserve Bank of Boston Working Paper No. 16-6.

[22] Ibid. “Liquidity” is the ease with which an asset can be converted into cash without significantly altering the asset’s price. Cash is clearly the most liquid asset, but many financial assets, such as stocks and bonds, are highly liquid as well. When access to additional credit is unavailable because of a credit shock, the cardholder may default to preserve cash or use cash advances to build up a cash buffer.

[23] Jesse Bricker, Lisa J. Dettling, Alice Henriques, Joanne W. Hsu, Kevin B. Moore, John Sabelhaus, Jeffrey Thompson and Richard A. Windle, 2014, “Changes in U.S. Family Finances from 2010 to 2013: Evidence from the Survey of Consumer Finances,” Federal Reserve Bulletin, vol. 100, no. 4.

[24] Experian, “2015 State of Credit.” Available at External Linkhttp://www.experian.com/live-credit-smart/state-of-credit-2015.html. Many other organizations report average credit card balances, some of which vary dramatically from the statistics above. For example, a 2015 Harris poll of 2,000 households, commissioned by the online blog NerdWallet, pegged average household credit card debt at $15,675 for those indebted with credit card balances (Erin El Issa, 2015, op. cit.). The very different statistics across providers is often a source of confusion. Many factors contribute to differences in debt calculations, including the definition of a credit card, what is considered to be a balance, the way cards are used, and so on.

The views expressed are those of the authors and do not necessarily reflect the positions of the Federal Reserve Bank of Kansas City or the Federal Reserve System.