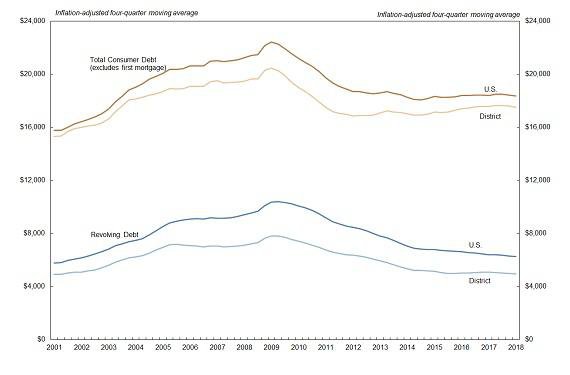

Average consumer debt for the Tenth District, defined for this report as all outstanding debt other than first mortgages and presented as a four-quarter moving average, increased $150 from the third quarter of 2015 to $16,590 in the first quarter of 2016 (Chart 1).1 Average consumer debt in the District has increased steadily since 2012 and is up $1,150, or about 7.5 percent (4.2 percent when adjusted for inflation). The increase in consumer debt is consistent with increases in employment and income.2 Higher incomes may make households more secure in their borrowing and make them better able to service debt. Moreover, higher incomes may loosen credit constraints.3 Many additional, sometimes confounding factors, however, can alter the relationship between income and the accumulation of debt, and income and debt do not always move together.

While average consumer debt in the District has been increasing steadily, it has grown at a slower, more sustainable pace than in the four-year period of growth prior to the recession, when average consumer debt increased 21 percent (11.2 percent adjusted for inflation). Nevertheless, national average consumer debt, while still exceeding District debt by about $1,000, increased only 2.4 percent over the last four years, declining in inflation-adjusted terms by 0.9 percent.

Chart 1: Outstanding Consumer Debt per Consumer and Revolving Debt per Consumer

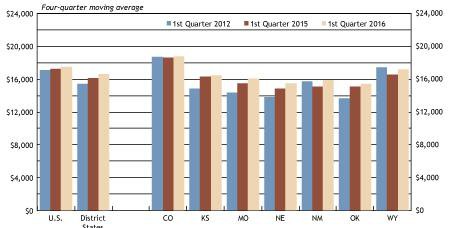

Average consumer debt has not grown uniformly across District states (Chart 2). States with the lowest 2012 levels of average consumer debt—Oklahoma and Nebraska—have seen the most rapid increases in average consumer debt since then: 13.1 percent and 12.4 percent, respectively. Colorado, which had the highest level of average consumer debt in 2012, saw growth of only 0.4 percent over the succeeding four years. Research suggests highly indebted households are more sensitive to fluctuations in income, but many other economic factors also affect levels of consumer debt across states.

The relatively rapid increase in consumer debt in Oklahoma likely reflects, in part, high oil prices and a strong energy sector in 2012-14. Since oil prices have fallen, consumer debt in energy-driven Oklahoma has been growing more slowly than in most other District states, and has declined in some sectors. In the first quarter of 2016, average balance on auto debt (four-quarter moving average) fell moderately from the previous quarter after rising steadily for several years. Average balance on equity lines also fell. The accumulation of debt in Wyoming also has slowed amid declining commodity prices. Nebraskans benefited from a booming agricultural sector early in the period, which may have made them more willing to take on debt. But Nebraska consumer debt continues to grow relatively rapidly, even as the agriculture sector has cooled. 4 Over the past year, average consumer debt has grown most rapidly in New Mexico at 5.4 percent. New Mexico faced economic struggles for a significantly longer period following the recession than did other District states and had been unique among District states in seeing declines in consumer debt. Its relatively nascent economic recovery, although still weak, likely has supported the recent accumulation of consumer debt. Socioeconomic factors also contribute to the variation in average debt across states and time, including demographics, cultural differences, trends in financial intermediation and public policy.5

Average revolving debt, which consists largely of credit cards and home equity lines of credit (HELOCs), inched up to $4,773 in the first quarter, still 28 percent below its recession-era peak (Chart 1). Almost all consumers (with credit reports) have credit cards, while about 6 percent have open HELOCs. The increase in total consumer debt far exceeded the small increase in revolving debt, which implies that installment debt (other than first mortgages) has continued to grow rapidly.

Chart 2: Outstanding Consumer Debt per Consumer

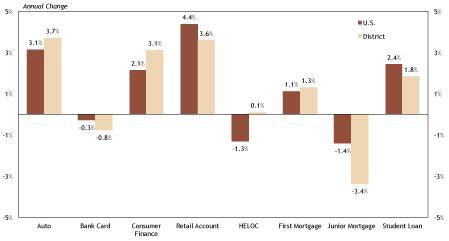

The bulk of installment lending has been in auto loans and student loans, particularly auto loans. Auto debt balances over the past year increased 3.7 percent in the District and 3.1 percent in the nation (Chart 3). The number of outstanding auto loans also has been increasing, as discussed later in this report. Retail accounts, which are revolving accounts, and consumer finance installment lending also have increased significantly, but average balances are small; growth in these accounts has a muted effect on total debt relative to auto and student loans.6

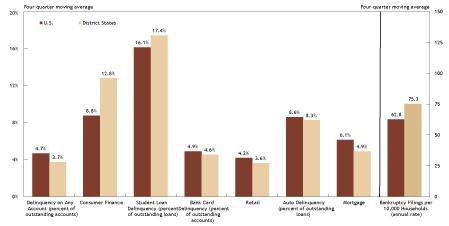

Overall credit delinquency in the first quarter was 3.7 percent in the District, down slightly from the previous quarter and significantly lower than the U.S. rate of 4.7 percent (Chart 4). Delinquencies are calculated as a share of open trade lines, or accounts.7 For example, bank card delinquency expresses the share of bank cards that is 30 days or more delinquent. The lower overall delinquency rate in the District is attributable largely to lower mortgage delinquency rates in District states. Specifically, the rate for mortgage delinquency (30 or more days past due, including foreclosure) in the District was 4.9 percent in the first quarter, down sharply from 5.7 percent in the third quarter and well below the U.S. rate of 6.1 percent. 8 The U.S. rate also was down significantly from 7.2 percent in the third quarter.

The first quarter District delinquency rate on consumer finance loans dropped to 12.8 percent from 14.2 percent in the third quarter but remained significantly higher than the U.S. rate of 8.8 percent. As noted in the December 2015 issue of the Tenth District Consumer Credit Report, the higher delinquency rate in the District has been driven by very high delinquency rates in Missouri (14.9 percent), New Mexico (18 percent) and Oklahoma (21.5 percent). Many factors help explain the level of debt and delinquency across states and time, as for consumer lending more generally. The consumer finance sector is less regulated than most lending sectors, even for closed-end installment loans. State-level variation in consumer law and policy is significant and is one factor in the variation of consumer finance delinquency rates across states.9

Auto delinquencies (expressed as share of accounts) continued to increase through the first quarter, rising to 8.3 percent from 8.1 percent in the third quarter. The student loan delinquency rate rose 0.1 percentage point to 17.4 percent in the District and 16.1 percent in the nation. The student loan delinquency rate includes loans that are not in active repayment, such as those in deferment or forbearance.10 If only loans in repayment are considered, delinquency rates are considerably higher, ranging from 16.7 percent in North Dakota to 49.6 percent in Mississippi.11 Delinquencies on retail loans ticked up from the third quarter to 3.6 percent.

Chart 3: Change in Debt Balances, 2015-2016 (first quarter)

Chart 4: Consumer Credit Delinquency Rates and Bankruptcy Filings, 2015-2016, (first quarter)

In This Issue: Subprime Auto Lending

During the recession, automobile sales in the United States declined sharply, especially for new vehicles. In the depths of the recession in February 2009, new autos in the United States sold at an annualized rate of 9.0 million (light vehicles, seasonally adjusted), well below the mid-2005 peak of an annualized rate of 20.6 million.12 The reduction in sales of new autos had the effect of increasing the average age of autos on the road from 9.8 years in 2005 to 11.5 years in 2015, the latest date for which data are available.13

The increased average age of autos on the road has increased the need for replacement, which along with gains in employment and income, has stimulated demand. Auto sales have increased significantly since the 2009 trough, reaching an annualized rate of 18.1 million (seasonally adjusted) in October 2015. By April 2016, the annualized rate of auto sales had decreased moderately to 17.3 million, but still above the 2000-15 average. The surge in sales has been accompanied by a surge in auto lending. Outstanding auto debt increased $13.5 billion to $1.1 trillion in the first quarter from the previous quarter and was up almost $80 billion over the past year.14

Recently, concerns have surfaced about subprime auto lending. 15 Subprime auto lending potentially can lead to some undesirable outcomes. Delinquency rates are much higher on subprime loans, as they are for all types of credit extended to subprime borrowers. S&P Global Ratings and Fitch Ratings both recently raised the issue of increasing risk in the auto loan asset-backed securities market.15 While high delinquencies can interrupt auto sales and segments of the financing apparatus, the implications are likely to be minimal compared to the “meltdown” in the subprime housing market concurrent with the recession and financial crisis. At $1.1 trillion, the auto loan market is much smaller than the $13.8 trillion mortgage market.16 Moreover, vehicles are more liquid assets than are houses and can be more easily marketed and sold, in some cases through repossession. There are significant risks in subprime auto lending to borrowers and lenders, and potentially investors, but a subprime “crisis” in the auto lending sector likely presents minimal systemic risk to financial markets.

The primary reason that subprime auto lending is up is because vehicle sales have surged, and along with that surge, all types of auto lending, including loans to subprime borrowers. The number of auto loans outstanding for those with a subprime credit score (defined for this report as scores less than 620) increased 7.8 percent over the last year, only modestly higher than the 7.4 percent increase in the number of auto loans outstanding for those with prime credit scores (700 and above for this report). Thus, subprime auto lending indeed has been increasing at a fairly rapid rate, but to date has not grown at a rate remarkably different than the prime credit cohort.

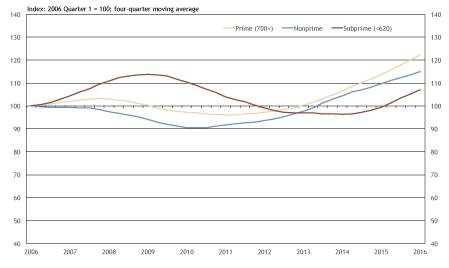

The trend in outstanding auto loans for subprime borrowers, however, generally has significantly lagged that of prime borrowers in every dimension (Chart 5). Pre-recession, outstanding auto loans peaked for prime borrowers in the fourth quarter of 2007, but the number of outstanding auto loans for subprime borrowers continued to climb until the first quarter of 2009. Auto loans reached a bottom in the first quarter of 2011 for prime borrowers, but not until the first quarter of 2014 for subprime borrowers. If the lag were to continue, subprime auto lending might be expected to outpace prime auto lending in the near term, but that scenario is in no way certain.

Chart 5: Outstanding Auto Loans

Endnotes

[1] Statistics in this report are derived from data in the Federal Reserve Bank of New York Consumer Credit Panel/Equifax, unless otherwise indicated. The data consist of a 5 percent sample of Equifax credit reports, which are devoid of any information that could be used to identify individuals. Average consumer debt is calculated by dividing the aggregate consumer debt of those in the credit report sample by the number of individuals in the sample. Credit and debt statistics can be calculated many ways, and thus these statistics may not be comparable to similar statistics published elsewhere, including by other Federal Reserve Banks. The Tenth District includes Colorado, Kansas, the western third of Missouri, Nebraska, the northern half of New Mexico, Oklahoma and Wyoming. In many cases in the report, data from all of Missouri and New Mexico are used, in which case the label for the region is "District States."

[2] See Jonathan Cook, 2001, “The Demand for Household Debt in the USA: Evidence from the 1995 Survey of Consumer Finance,” Applied Financial Economics, vol. 11, no. 1, pp. 83-91.

[3] See Kyoung Jin Choi, Hyeng Koo, Byung Hwa Lim and Jane Yoo, 2015, “The Determinants of Unsecured Credit Constraint,” Sept. 8. Available at SSRN: External Linkhttp://ssrn.com/abstract=2657352 or External Linkhttp://dx.doi.org/10.2139/ssrn.2657352.

[4] The agriculture sector started to cool around mid-2013, but cattle and hog producers continued to do well. Moreover, record high farm incomes in the previous few years mitigated early problems in the crop sector. By 2015, virtually all subsectors in agriculture were in decline.

[5] See, for example, Basak Kus, 2015, “Sociology of Debt: States, Credit Markets, and Indebted Citizens,” Sociology Compass, vol. 9, no. 3, pp. 212-223. See also Thomas Durkin et al., 2015, Consumer Credit and the American Economy (Oxford University Press USA). In the case of Nebraska, see Kevin Helliker, “The Corn Belt Gets Rich, Quietly,” The Wall Street Journal, Aug. 17, 2007.

[6] Average balances on various forms of consumer credit are discussed in the Dec. 3, 2015, issue of "Tenth District Consumer Credit Report" (see especially Chart 6).

[7] Delinquency is more commonly reported as the share of balances that is delinquent. See, for example, External LinkFederal Reserve Bank of New York, Quarterly Report on Household Debt and Credit, May 2016.

[8] Lender Processing Services Inc. [datafile].

[9] See National Consumer Law Center, July 2015, External Link"Installment Loans: Will States Protect Borrowers from A New Wave of Predatory Lending". While not necessarily the primary cause of District differences in delinquency rates for consumer installment loans, the states with the highest delinquency rates also are among the states with the most generous terms to lenders. Missouri and New Mexico are among the eight states with no cap on interest (New Mexico has a deceptive practices statute); the annual percentage rate (APR) in Oklahoma is capped at 116 percent, the highest among states that cap APR. Research suggests higher interest rates are associated with higher risk of default. See, for example, Jose Angelo Divino, Edna Souza Lima and Jaime Orrillo, 2013, “Interest Rates and Default in Unsecured Loan Markets,” Quantitative Finance, vol. 13, no. 12, pp. 1925-1934.

[10] Deferment allows borrowers to stop making loan payments if they are enrolled in school at least half time; currently serving on active duty; engaged in a full-time rehabilitation training program; or in cases of economic hardship, including unemployment, receipt of public assistance, Peace Corps service and certain income limitations. Forbearance allows those who do not qualify for a deferment to stop making student loan payments, temporarily make smaller payments, or extend the time for making payments. Common reasons for forbearance listed, according to the Department of Education, are illness, financial hardship, or serving in a medical or dental internship or residency. A forbearance can be granted automatically while processing a deferment, forbearance, cancellation, change in repayment plan, or consolidation, or if the borrower is involved in a military mobilization or emergency. Interest does not accumulate under deferment, while it does under forbearance.

[11] Wenhua Di and Kelly D. Edmiston, 2015, “State Variation of Student Loan Debt and Performance,” Suffolk University Law Review, vol. 48, no. 3, pp. 661-688.

[12] U.S. Bureau of Economic Analysis, “Light Weight Vehicle Sales: Autos and Light Trucks,” retrieved from FRED, Federal Reserve Bank of St. Louis, May 24, 2016.

[13] IHS Automotive, “Average Age of Light Vehicles in the U.S. Rises Slightly in 2015 to 11.5 years, IHS Reports,” Press Release, July 29, 2015.

[14] Federal Reserve, Series G.19: Consumer Credit, March 2016.

[15] See, for example, Center for Responsible Lending, “ ‘Reckless Driving’: Implications of Recent Subprime Auto Finance Growth,” January 2015.

[16] Rachel Koning Beals, “Second Credit-Ratings Agency Flags Increased Stress in Auto-Loan Market,” MarketWatch, May 23, 2016.

[17] Federal Reserve, External Link"Mortgage Debt Outstanding," March, 2016.

The views expressed are those of the authors and do not necessarily reflect the positions of the Federal Reserve Bank of Kansas City or the Federal Reserve System.