Minority-owned firms are at significant economic risk due to the COVID-19 pandemic and the subsequent economic crisis caused by stay-at-home orders and social distancing. This is largely because minority-owned firms are smaller, on average, in a weaker position financially, and have less access to credit and capital. Couple this with various reports that minority firms were less likely to receive access to stimulus funding, and the challenges for these firms during the crisis become clear. This article provides an overview of the vulnerability of firms owned by minorities prior to the crisis, and shares insights from organizations that work with minority firms on how these firms are being affected during the crisis.

How vulnerable were minority-owned firms going into the crisis?

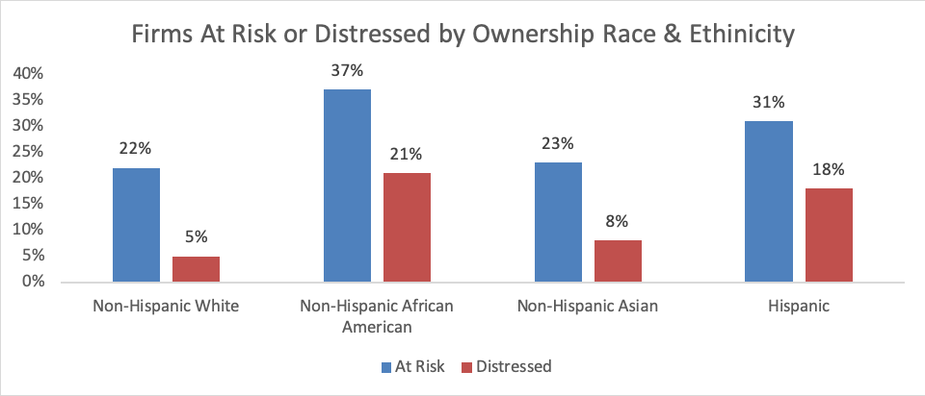

According to the 2019 Federal Reserve System External LinkSmall Business Credit Survey, of small firms, African-American and Latino firms were more likely to report that their businesses either were at risk or distressed compared with white- and Asian-owned businesses. This suggests that the consequences of the crisis on minority-owned firms would be more significant than on non-minority firms.

- Fifty-eight percent of African-American and 49% percent of Hispanic owner respondents shared that their businesses either were at risk or distressed.

- This compares with white and Asian respondents, who shared that their businesses either were at risk or distressed at 27% and 31%, respectively.

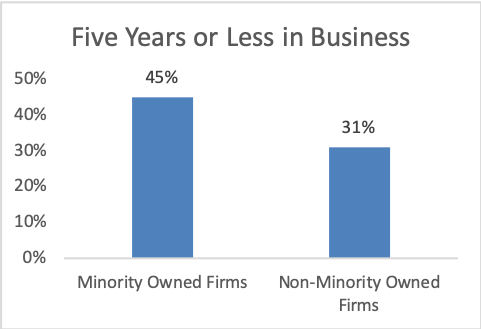

In addition, younger firms are more vulnerable. Minority firms, on average, are younger than non-minority firms.

- According to the 2019 Federal Reserve survey, 41% of firms less than five years old reported they either were at risk or distressed, compared with only 24% of firms older than five years.

- An External LinkEIG analysis of minority versus non-minority firm age showed that 45% of minority firms were 5 years old or less, compared with 31% of firms owned by non-minorities.

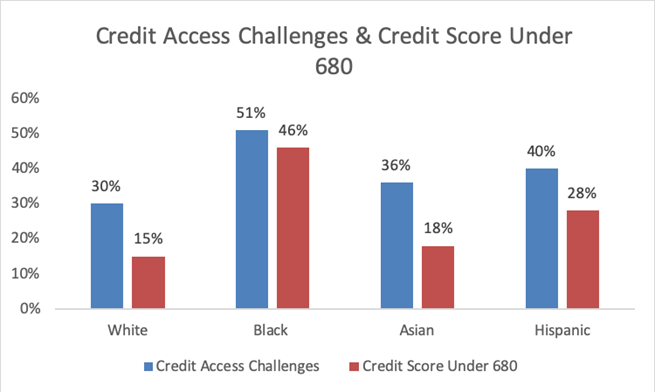

Access to capital also is a critical issue for minority firms during periods with or without an economic crisis. Capital provides firms the ability to weather economic cycles, and can fund growth and a pivot in strategy when necessary. According the 2019 Federal Reserve External LinkSmall Business Credit Survey Report on Minority-Owned Firms, credit access was a greater challenge for minority firms than non-minority firms. This, in part, is due to minority firm credit scores being lower on average.

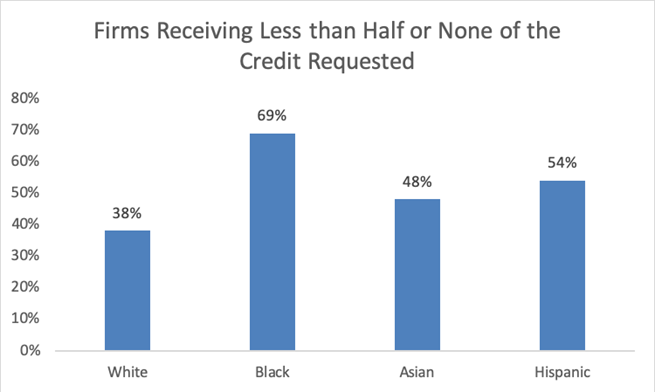

Minority firms are also more likely to report they received less than the amount of credit they requested. For example, 69% of Black firms reported they received half or none of the amount of credit they requested. This compares with 38% of white firms that reported they received half to none of the credit they requested.

Based on the increased vulnerability of minority firms prior to the economic crisis caused by COVID-19, it is likely that minority firms would be hit substantially harder during the crisis. An examination of the impact the Great Recession on minority firms seems to support this argument.

What lessons can the Great Recession teach us?

While we cannot draw complete comparisons from the Great Recession, that crisis offers insight into how minority businesses are likely to be affected by the COVID-19 crisis.

According to a 2011 economic commentary by the Federal Reserve Bank of Cleveland, External LinkThe Great Recession’s Effect on Entrepreneurship, “At the end of the recession, the United States had fewer businesses and self-employed people than it had before the downturn began.”

This was due to business closures during the recession as well as the slowdown of new business formation. AExternal Link Census Bureau report released in 2014 stated, “ … the recession appears to have impacted Black-owned and Hispanic-owned businesses more severely than their counterparts, in terms of employment growth as well as survival. This is also the case for continuing Black and Hispanic-owned firms.”

After the recession, however, the number of minority-owned firms increased faster than non-minority owned firms. This indicates that resources supporting COVID-19 recovery efforts can lead to a faster paced national recovery. According to a External LinkMinority Business Development Agency report: “While the overall impact of the recession was most definitely felt within the minority business community, according to Minority Business Development Agency (MBDA), Minority Business Enterprises (MBEs) continue to be the engine of employment in emerging and minority communities.”

External LinkResearch also shows that this growth in entrepreneurship is due, in part, to an increase in the unemployment rate and the subsequent turn to entrepreneurship by many minority-firm owners. While the number of minority-owned firms increased at a faster pace, they still were younger, had fewer employees per firm, and therefore were more vulnerable. This suggests there is a strong likelihood that young, minority firms again will face significant challenges during the COVID-19 crisis based on their pre-existing vulnerabilities. This also suggests, however, that robust support of minority firms during the recovery process can speed the national rate of economic recovery.

What are we learning from outreach to stakeholders during the COVID-19 crisis?

Little quantitative data is available on the effect COVID-19 has had on minority firms. However, community development staff members across the Federal Reserve System engaged stakeholders that work closely with minority firms. This insight can help illustrate the effect of the crisis.

According to a Federal Reserve Bank of Atlanta memo, “Small Businesses & COVID-19 needs, concerns with current policy response, and policy ideas,” produced in April 2020, “Smaller, minority and younger firms were particularly vulnerable to closure. There is a consistent concern that the responses will not filter to communities and people that need them the most.” This sentiment is shared by many stakeholders across the nation who provided insight to community development staff.

Other themes dealt with information and awareness. Stakeholders said minority firms had challenges in both accessing and understanding information on the various national and local policies that affect their businesses. This included not just information on what stimulus support was available to them, but also various local policies on when to close, safety precautions and other similar policies.

In addition to the information challenges, stakeholders also said many minority firms they work with did not have strong business infrastructures. This made it difficult to rapidly pull the information that bankers required for stimulus funding. In addition, many minority firms that had the potential to pivot to either digital models or tech-enabled models (such as a restaurant moving to online platforms for delivery services) did not have the skills to do so.

Some minority firms were challenged by their concerns about CARES Act-related stimulus funding. Stakeholders said owners of minority firms either were discouraged by previous borrowing attempts, did not know how the potential loans would affect their business over the long run, or attempted to apply for funding and either were turned away or put on a long wait list due to not having a pre-existing relationship with the lending institution.

Many stakeholders said many minority firms they worked with were likely to close, and potentially never reopen. This can be seen also in the Federal Reserve Bank of Atlanta memo, which said, “Overall, interviewees indicated that several clients had just a few weeks to survive (3 to 5) maximum. They stressed an urgency for accessible funds to help small businesses.”

What could we do that might have an effect?

While this article is not intended to provide policy recommendations, it provides insight into the vulnerability of minority firms both before and during the crisis. Strategies, policies and practices that are built to strengthen the vulnerabilities of these firms, which tend to be younger and smaller, can have greater effect than general small business strategies. Minority firms have an important role to play in the U.S. economy, and have an even greater role to play in their local communities. Ensuring their needs are considered both during and after the crisis can spur a faster recovery.

For more information on minority-owned firms visit:

External LinkFedsmallbusiness.orExternal Linkg

External Linkhttps://www.kansascityfed.org/community/smallbusiness/

The views expressed are those of the authors and do not necessarily reflect the positions of the Federal Reserve Bank of Kansas City or the Federal Reserve System.