First quarter banking conditions reflect stresses across the banking industry. Higher interest rates and the collapse of three banks_ functioned as a catalyst in driving balance sheet and earnings trends.

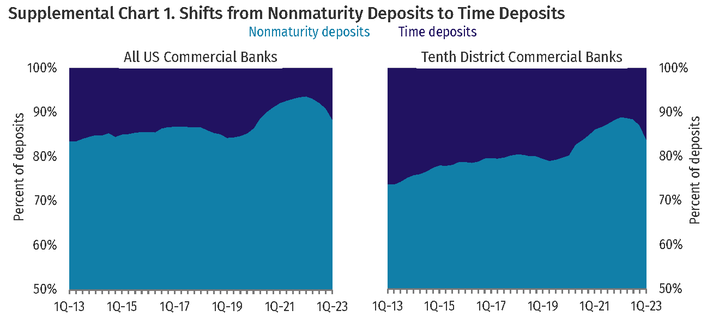

On the asset side (see Chart C3), District banks saw loan growth slow in the first quarter, with total loans growing at just 1.6 percent quarter-over-quarter (q/q). Apart from agricultural loans, all major loan types saw growth, with construction and land development (CLD) showing the largest increase at 3.7 percent q/q (see Chart C4). District banks boosted their cash reserves 23.6 percent q/q, the largest quarterly increase since the start of the pandemic (see Chart C16). On the liability side, District banks continued to see deposit run off, with 52 percent of banks experiencing declines in their core deposits in the first quarter. The higher rate environment is also causing changes in bank deposit compositions, as pricing pressures and changing consumer behaviors have resulted in shifts from nonmaturity into time deposits (see Supplemental Chart 1). As deposits have run off, District banks have turned to wholesale funding sources to boost their asset-based liquidity (cash reserves). In the first quarter, total borrowings increased over $7.5 billion, with Federal Home Loan Bank borrowings increasing $4.4 billion and other borrowings (which include Discount Window activity and Bank Term Funding Program funds) having increased $3.1 billion (see Chart D10). District banks have also utilized brokered deposits, which grew by over $5.8 billion in the first quarter.

Though loan growth slowed in the first quarter, overall loan-to-deposit ratios continue to increase, as deposit growth has not kept pace with loan growth (see Chart D6). The liquid asset ratio declined to 15.7 percent at District banks, down from 17.8 percent at year-end (see Chart D9). Liquid assets have been restricted by large levels of unrealized losses in securities portfolios. While unrealized positions have improved over the past couple of quarters, unrealized losses remain sizeable.

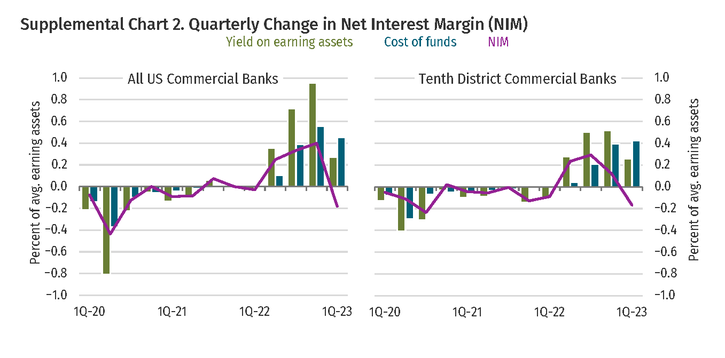

Pricing pressures caused District bank margins to compress in the first quarter (see Chart A11). Funding costs increased 43 basis points (bps) q/q, with yields on earning assets increasing only 26 bps during the same time (see Supplemental Chart 2). Deposit betas continue to rise in response to increasing market rates and deposit competition. Though funding costs have increased, almost 77 percent of total borrowings plus time deposits will mature within a years’ time. Earnings performance remained stable at District banks as compressed margins were partially offset by reductions in total expenses (see Chart A4). Return on average assets (ROAA) totaled 1.24 percent as of first quarter at District banks, compared to 1.22 percent at year-end 2022 (see Chart A6).

Asset quality metrics remain benign, with low levels of noncurrent loans across all major loan types (see Charts B6 and B8). Loans past due 30-89 days saw a slight uptick in the first quarter, with agricultural loans showing the largest increase. Most District banks implemented the new Current Expected Credit Loss standard on January 1. The allowance for credit losses (ACL) increased as a percentage of loans, totaling 1.42 percent in the first quarter, up from 1.28 percent at year-end 2022.

Provision expense remains mostly stable across District banks, though did decline to 0.19 percent of average assets in the first quarter compared to 0.20 percent at year-end 2022 (see Chart B2).

Capital ratios have improved, with District leverage ratios increasing to 9.73 percent in the first quarter (up from 9.66 percent at year-end 2022) as assets remained stable and Tier 1 capital increased (see Chart A2). The total risk-based capital ratio also improved to 13.6 percent (up from 13.3 percent at year-end 2022), as loan growth slowed.

Endnotes

-

1 In Q1 2023, there was one voluntary self-liquidation and two commercial bank failures. Silvergate Bank announced that it was voluntarily self-liquidating on March 8; and the FDIC closed Silicon Valley Bank and Signature Bank on March 10th and March 12th.

The views expressed are those of the authors and do not necessarily reflect the positions of the Federal Reserve Bank of Kansas City or the Federal Reserve System.

Author