Farm debt at commercial banks continued to ease in the second quarter. Agricultural loans balances decreased by 5% from the previous year due to a relatively large decline in production loans. Although farm lending increased at some banks, loan balances dropped by more than 10% from a year ago at a relatively large number of banks. Declines were most substantial among lenders with both the smallest and largest farm loan portfolios and among agricultural banks with high concentrations of farm loans.

The U.S. agricultural economy remained strong through the first half of the year and farm income was projected to reach an eight-year high in 2021. The quick recovery in farm finances from weakness in recent years has contributed to reduced levels of debt at commercial banks and is likely to continue supporting improvements in agricultural loan performance. In addition to stronger farm income and credit conditions, interest rates have remained at historic lows, providing ongoing support to farmland markets.

Second Quarter Commercial Bank Call Report Data

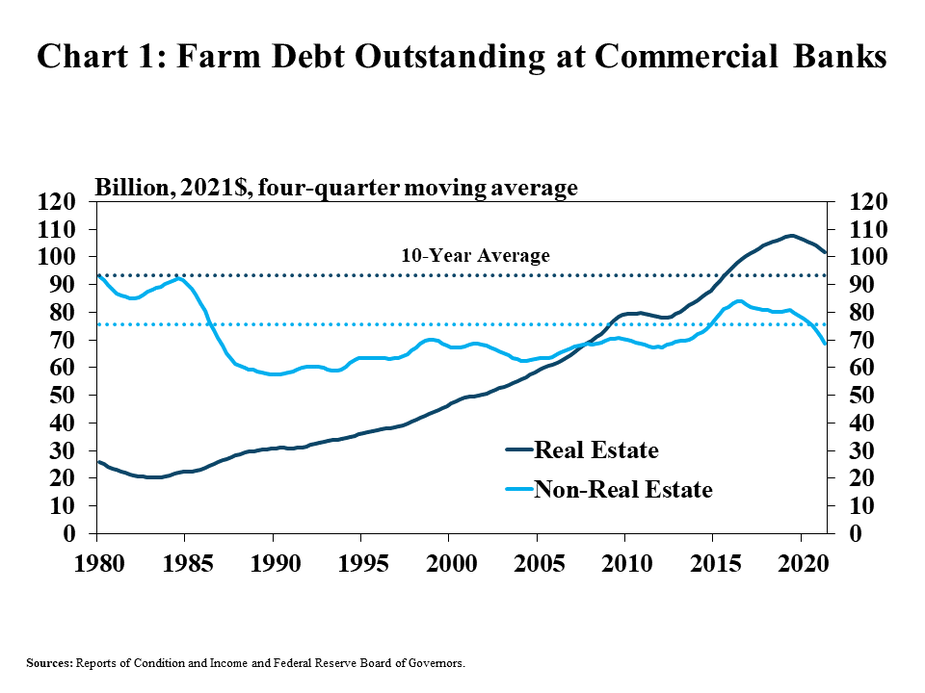

Farm loan balances at commercial banks continued to decline through the first half of the year according to recent Call Report data. Total farm debt decreased toward the historic average on a rolling four quarter basis in real dollar terms and the stabilization has mostly been driven by a pullback in production loans (Chart 1). As of the second quarter, farm real estate debt remained about 8% above the average of the past decade while non-real estate debt was about 13% less than the average over that same period.

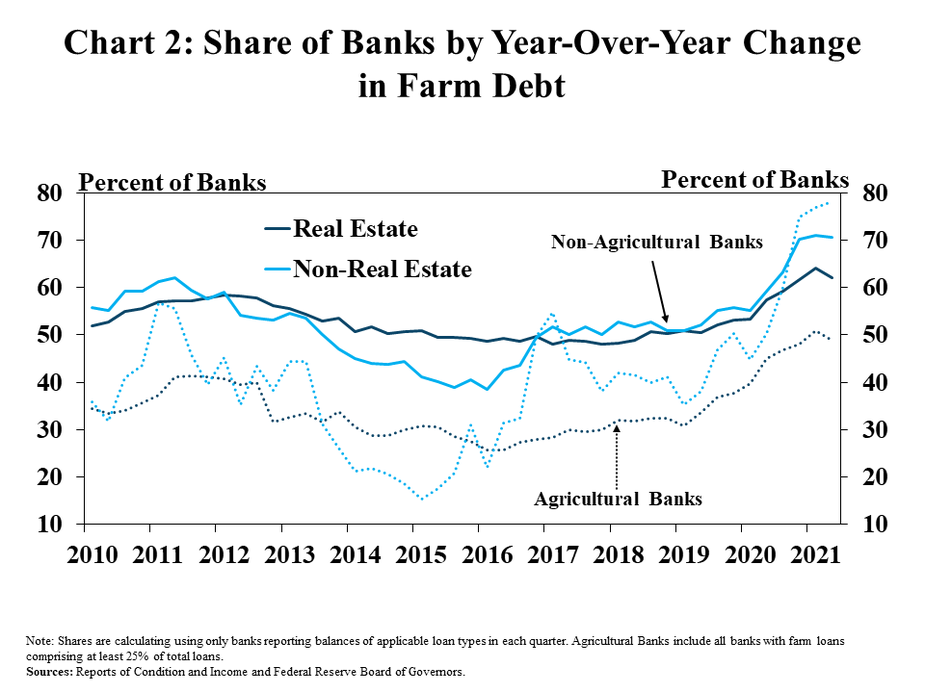

Farm debt declined at a large number of banks, but decreases in real estate debt were less prevalent than declines in non-real estate debt. Production loans were less than a year ago at about 70% of non-agricultural banks and nearly 80% of agricultural banks in the second quarter (Chart 2). In contrast, farm real estate debt was less than a year ago at about 60% of non-agricultural banks and only about 50% of agricultural banks.

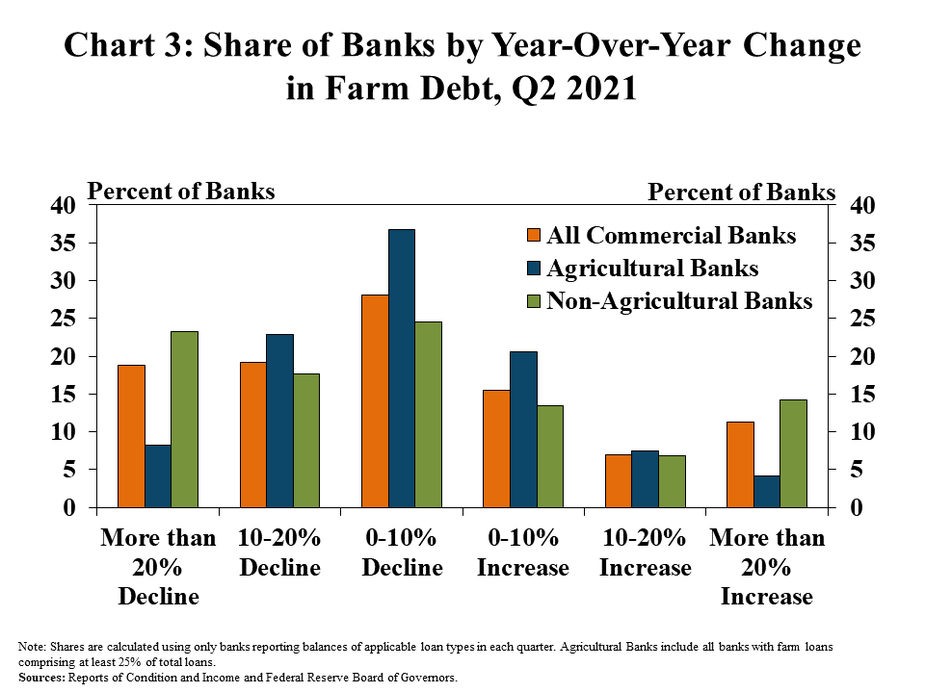

The share of banks with significant declines in outstanding farm debt was also notable. Nearly 40% of non-agricultural banks and 30% of agricultural banks had farm loan balances fall 10% or more from a year ago (Chart 3). While farm debt was lower at the majority of banks, a sizeable share of banks also had an increase of more than 10%.

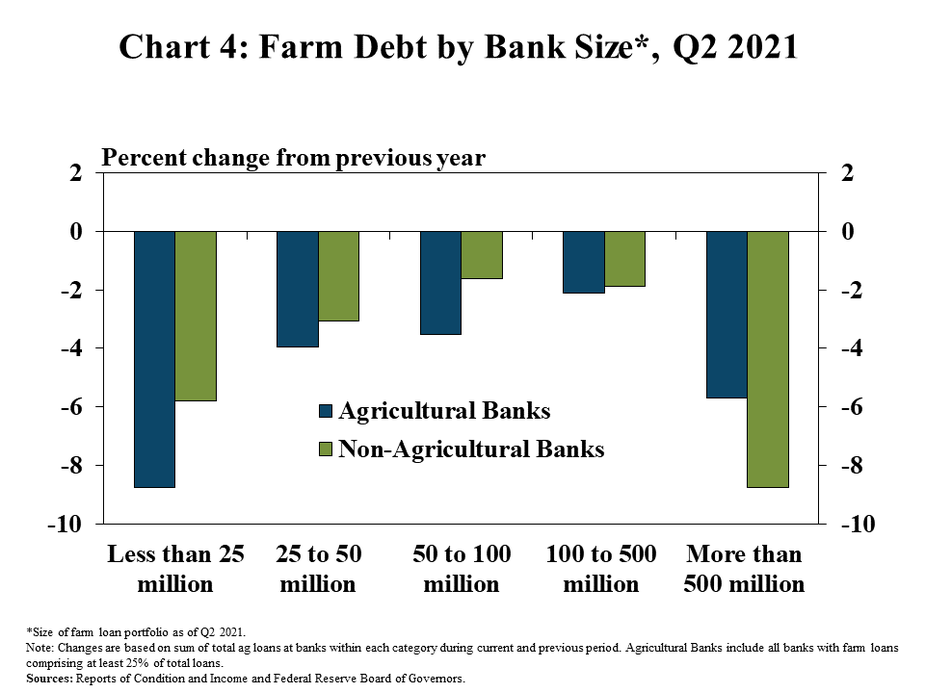

Lenders with the smallest and largest agricultural loan portfolios had the sharpest decrease in farm loan balances. Farm debt declined by more than 5% among banks with farm loan portfolios less than $25 million and more than $500 million (Chart 4). The decline was comparatively less for lenders with mid-sized portfolios.

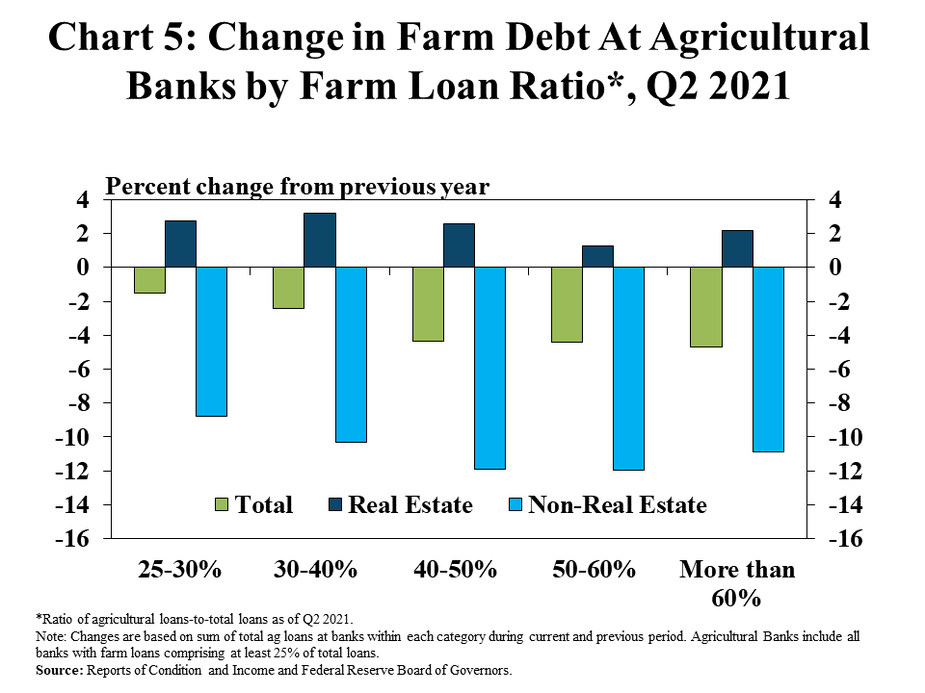

Decreases in farm debt were slightly greater at agricultural banks with relatively high concentrations of agricultural loans. In total, farm loan balances decreased only about 2% from a year ago at banks where agricultural loans comprised less than 40% of all loans. In contrast, farm loan balances dropped by more than 4% at banks with a larger concentration of agricultural loans (Chart 5). Across all groupings of farm loan concentration, the decrease in farm debt was driven by lower balances of non-real estate loans.

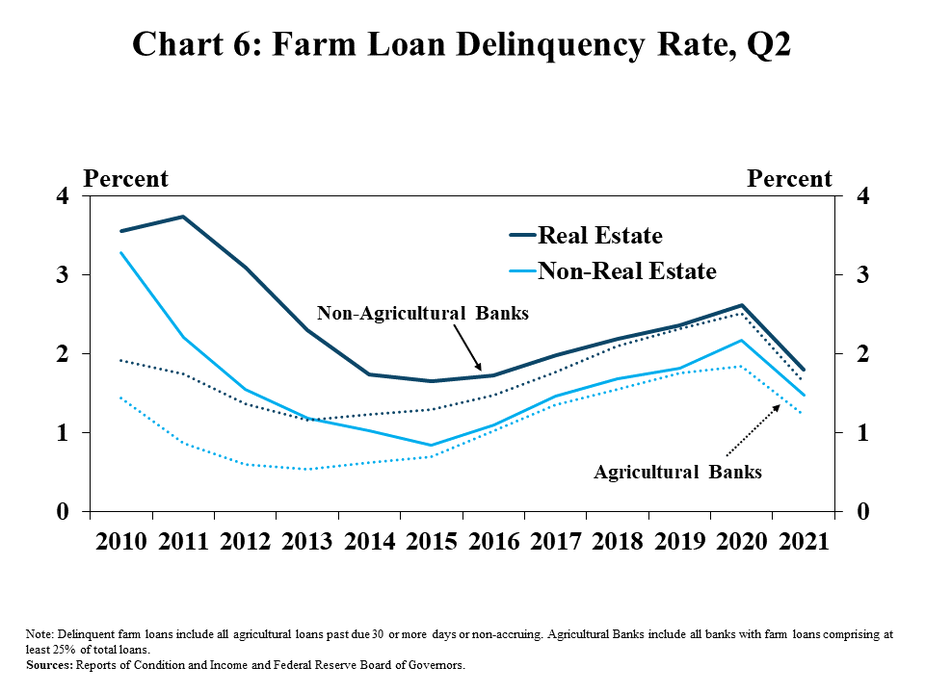

Alongside reduced agricultural debt and External Linkstronger farm finances, loan performance also continued to improve. Delinquency rates on both real estate and non-real estate farm loans were about 80 and 70 basis points less than a year ago, respectively (Chart 6). Similar to recent years, delinquency rates remained slightly lower at agricultural banks than other lenders.

Data and Information

Commercial Bank Call Report Historical Data

The views expressed are those of the authors and do not necessarily reflect the positions of the Federal Reserve Bank of Kansas City or the Federal Reserve System.

Authors

Nate Kauffman

Senior Vice President, Economist, and Omaha Branch Executive; Executive Director of the Center for Agriculture and the Economy