Interest rates on farm loans continued to increase in the first quarter of 2018. Following a prolonged period of historically low rates, interest rates on most types of farm loans at commercial banks have increased between 1.0 and 1.5 percentage points since 2015. Although farm debt also has continued to rise alongside higher rates, the increase in interest expense has remained relatively small. Additional increases in rates could put more pressure on some farm operations, but delinquency rates on farm loans remained low through 2017, and the performance of most agricultural banks has remained solid.

Section A: First Quarter Survey of Terms of Lending to Farmers

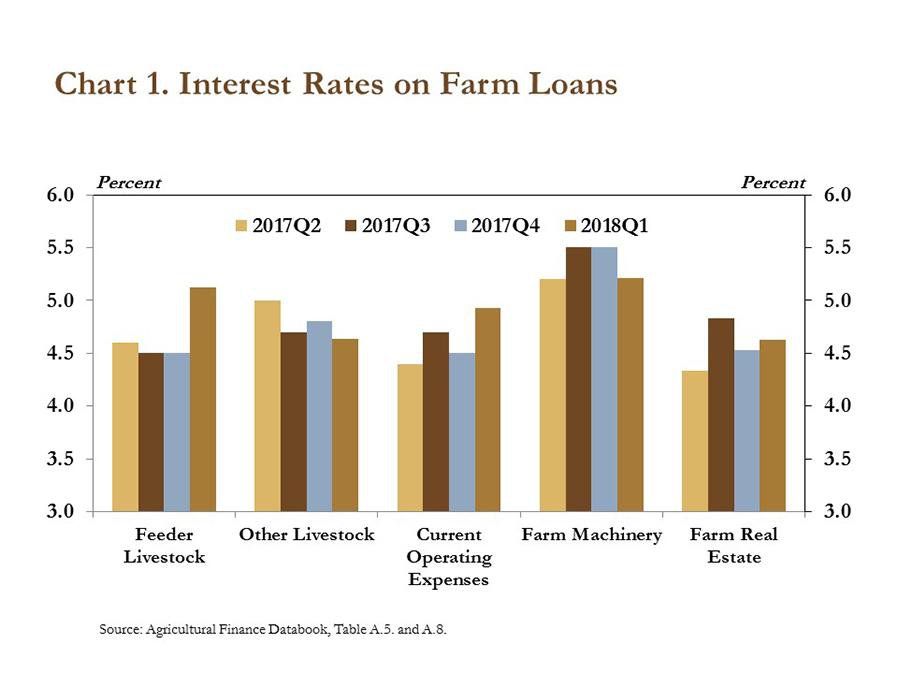

Interest rates on most types of farm loans continued to increase in the first quarter. Following modest increases in benchmark short-term rates, commercial banks raised interest rates on loans used to finance various farm sector purchases (Chart 1). Over the past four quarters, the target range for the federal funds rate has increased 100 basis points. During that time, interest rates on loans used to finance operating expenses have increased 52 basis points. Interest rates for most other types of farm loans have increased in a similar fashion over the past year.

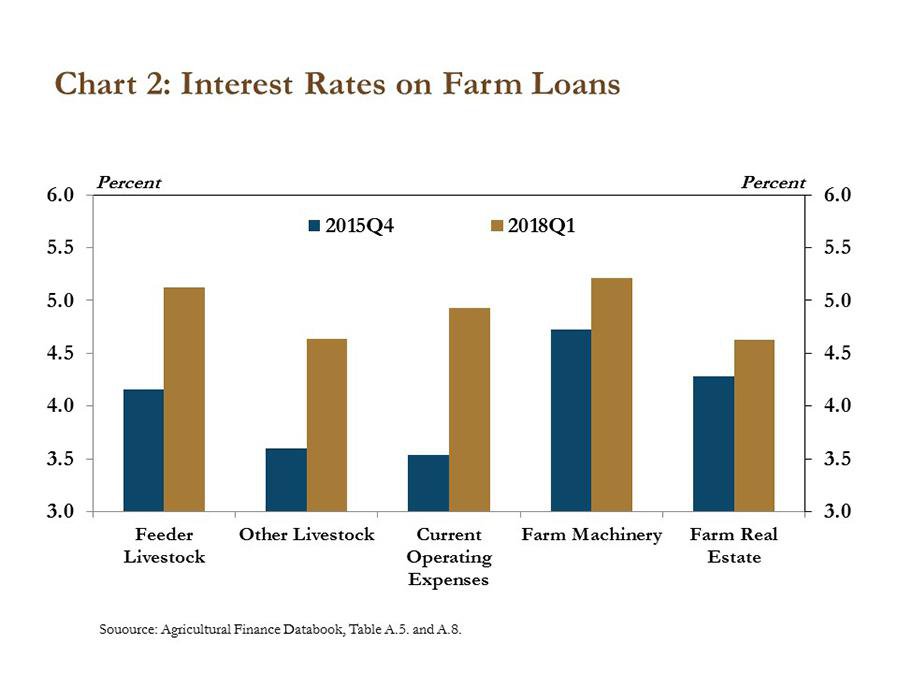

Following historical lows in 2015, interest rates have increased most significantly on loans used to finance operating expenses. In fact, interest rates on operating loans at commercial banks have increased from a low of 3.5 percent in the fourth quarter of 2015, to 4.9 percent in the first quarter of 2018 (Chart 2). Interest rates on other types of loans also have risen steadily in recent years, but at a somewhat slower pace. The increase in rates on operating loans, however, is perhaps even more notable because these loans account for about 60 percent of the volume of new non-real estate farm loans at commercial banks.

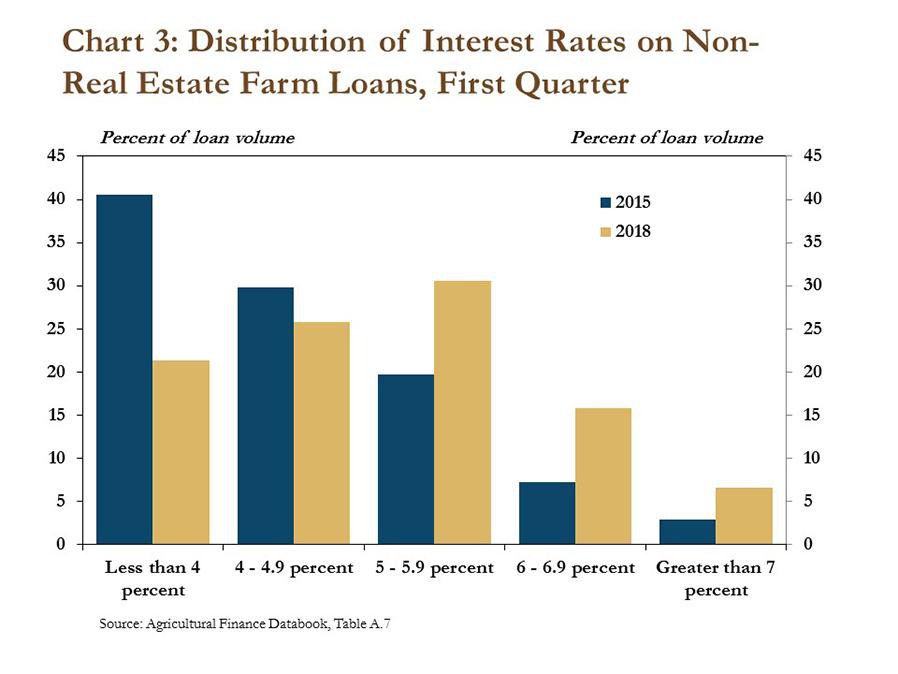

In addition to the steady increase in average interest rates, very few loans in the first quarter were made at an interest rate of less than 4 percent. In 2015, more than 40 percent of farm loans used to finance non-real estate purchases were originated with an interest rate of less than 4 percent (Chart 3). At that time, only about 10 percent of these farm loans carried an interest rate of more than 6 percent. In the first quarter of 2018, only 21 percent of non-real estate loans, by volume, were originated with an interest rate less than 4 percent. About 22 percent of loans had an interest rate greater than 6 percent.

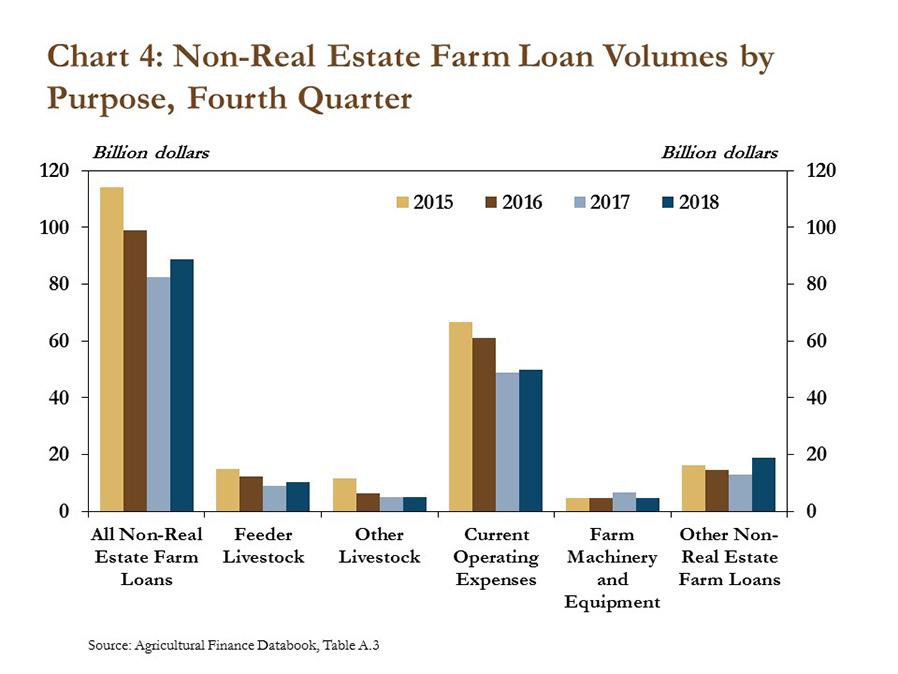

Lending activity remained strong in the first quarter as interest rates on farm loans continued to rise. Although the volume of non-real estate farm loans has declined slightly since 2015, lending increased in the first quarter compared with the same quarter of 2017 (Chart 4). The volume of loans for most types of farm purchases remained steady in the first quarter, but a modest increase in uncategorized farm loans (labeled “Other Non-Real Estate Farm Loans”) accounted for most of the increase.

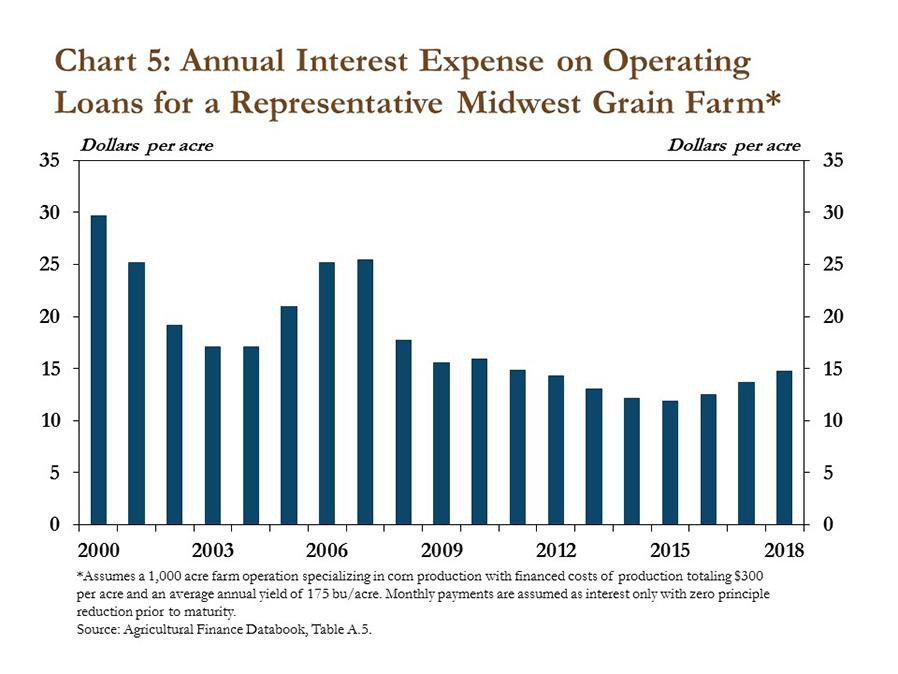

Higher interest rates have increased farmers’ debt obligations on new loans, but the effect on short-term loans has been relatively small. In 2015, the annual interest expense for a hypothetical Midwest farm operation specializing in corn production was about $12 per acre for its operating loans (Chart 5). Despite the increase in interest rates since 2015, the annual interest expense for this typical farm has increased by less than $3 per acre as of the first quarter of 2018. In the context of production, this increase in interest expense amounts to less than one bushel of corn per acre. In fact, interest rates on operating loans would need to increase to 5.2 percent to equal the dollar value of one bushel of corn per acre for this farm in the current price environment.

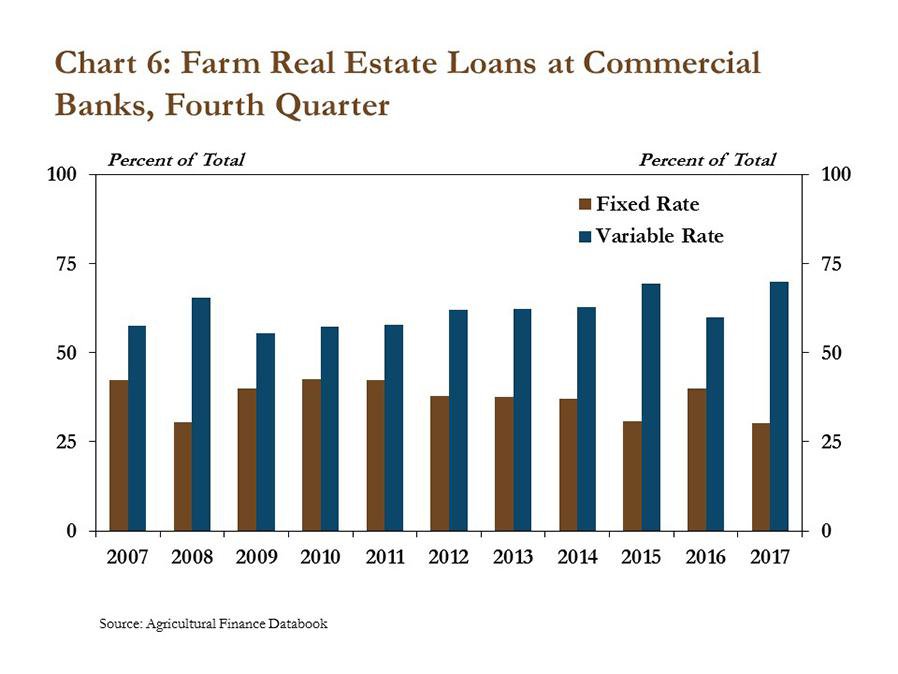

In contrast to short-term farm loans, the effect of higher rates on interest expenses has been more pronounced for longer-term loans. For example, increasing the interest rate on a $1 million farm real estate loan with a 20 year maturity from 4 percent to 5 percent would increase interest expenses over the life of the loan by $130,000. Moreover, higher interest rates also are likely to have placed some downward pressure on the value of farm real estate, which is an important source of collateral for many farm borrowers. Despite the effects of higher interest rates on farm finances, however, nearly half of all new farm real estate loans were originated with fixed interest rates over long time horizons when interest rates were at historical lows several years ago (Chart 6). Thus, interest expenses on many farm real estate loans have remained steady even as interest rates have continued to rise.

Section B: Fourth Quarter Call Report Data

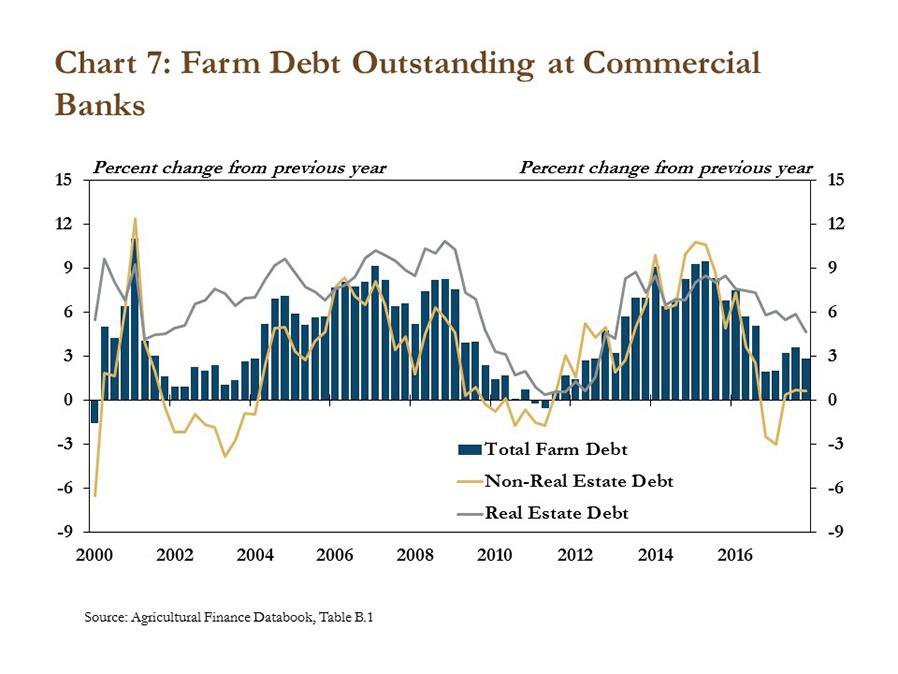

Fourth quarter Call Report data from commercial banks showed that outstanding farm debt continued to rise. The total amount of farm debt outstanding at commercial banks increased 2.9 percent in the fourth quarter, a pace that was similar to each of the previous two quarters (Chart 7). Although the pace of debt accumulation has slowed over the past two years, an additional increase in farm real estate debt accounted for most of the increase in the fourth quarter. The total amount of non-real estate farm debt outstanding at commercial banks also increased at a modest pace, similar to the previous two quarters.

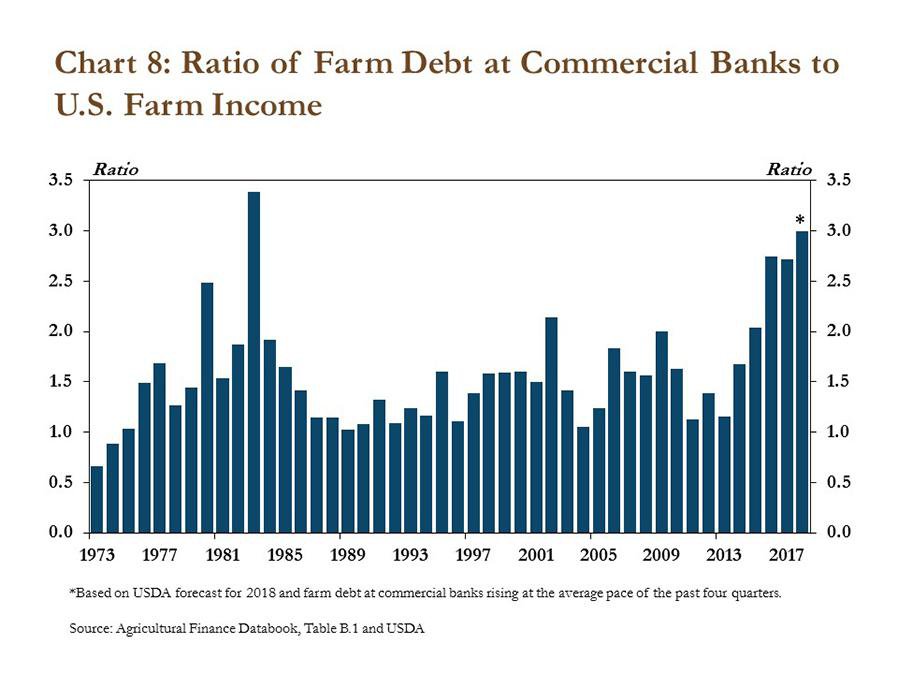

A steady increase in outstanding farm debt, coupled with expectations of reduced U.S. farm income, point to a slight increase in farm sector leverage in 2018. The U.S. Department of Agriculture forecasts that farm income in 2018 is expected to decline about 7 percent. If farm debt at commercial banks continues to rise at the average pace of the past four quarters, the ratio of farm debt to income would rise to 3.0 this year, the highest since 1983 (Chart 8).

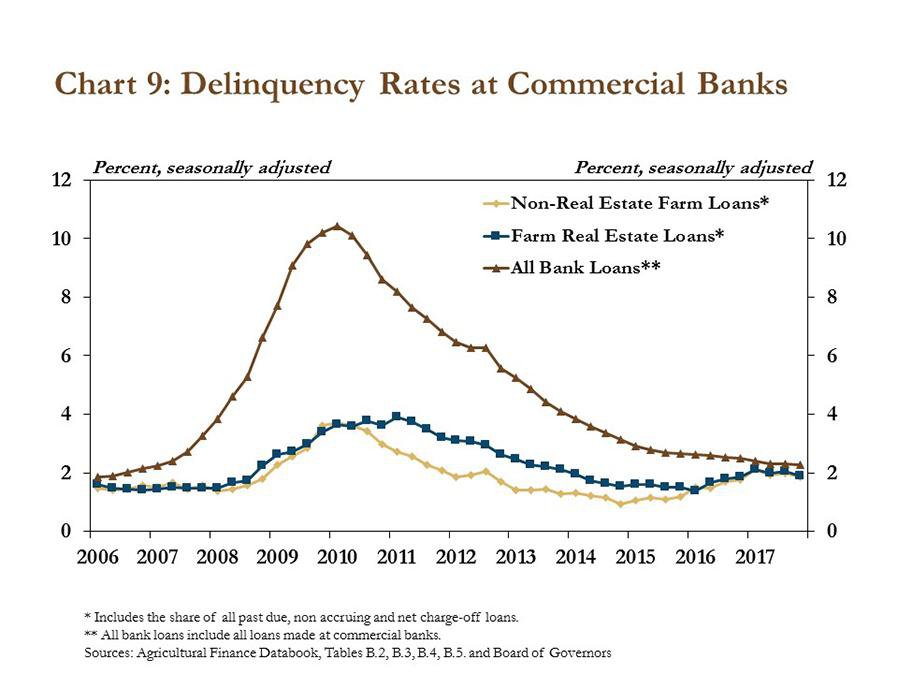

Despite the persistent increases in debt and leverage in the farm sector, the rate of delinquencies on farm loans has remained low. In the fourth quarter, delinquency rates on both farm real estate and non-real estate loans edged lower, to slightly less than 2 percent (Chart 9). Similar to recent quarters, problem loans at commercial banks with a concentration in agriculture have remained less than nonagricultural loans more generally.

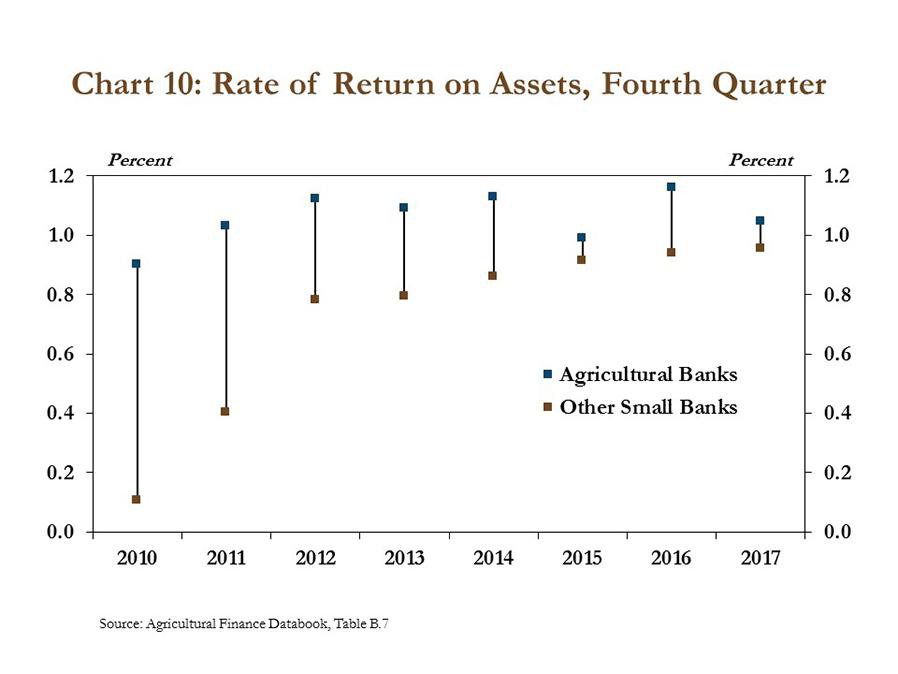

In addition, returns at agricultural banks remained strong in the fourth quarter. Despite ongoing concerns of reduced farm income and slight increases in leverage, the rate of return on assets at agricultural banks remained higher than that of nonagricultural banks (Chart 10). Although the gap between returns at agricultural banks and other banks of similar size has narrowed in recent years, agricultural banks generally have outperformed their non-agricultural peers since the mid-1990s.

Section C: Fourth Quarter Regional Agricultural Data

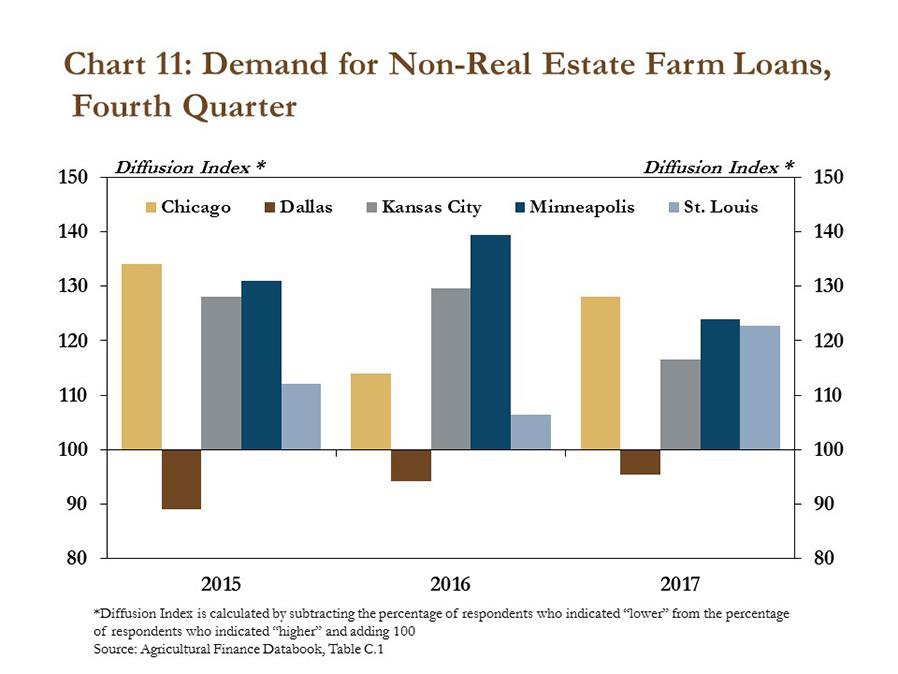

In addition to fourth quarter Call Report data from commercial banks, regional Federal Reserve surveys showed that demand for farm loans continued to increase throughout most of the nation’s concentrated agricultural regions. Demand for non-real estate farm loans continued to strengthen in the Chicago, Kansas City, Minneapolis and St. Louis Districts in the fourth quarter (Chart 11). Only the Dallas District reported a slight decrease in demand for non-real estate farm loans.

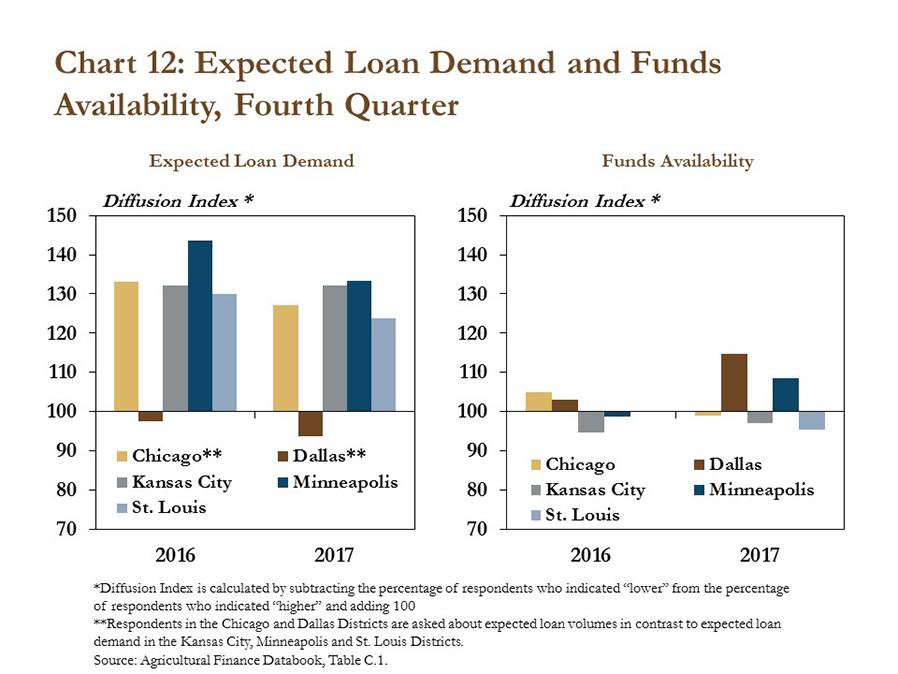

Although loan demand was expected to remain strong in the first quarter of 2018, measures of credit availability generally have remained steady. Based on their regional surveys of commercial banks, most Federal Reserve districts expected farm loan demand to continue to strengthen in early 2018 (Chart 12). Despite the ongoing strength in demand for farm loans, though, credit availability generally has remained steady. Although the availability of funds at agricultural banks declined slightly in the Chicago, Kansas City and St. Louis Districts in 2017, the decreases were relatively modest.

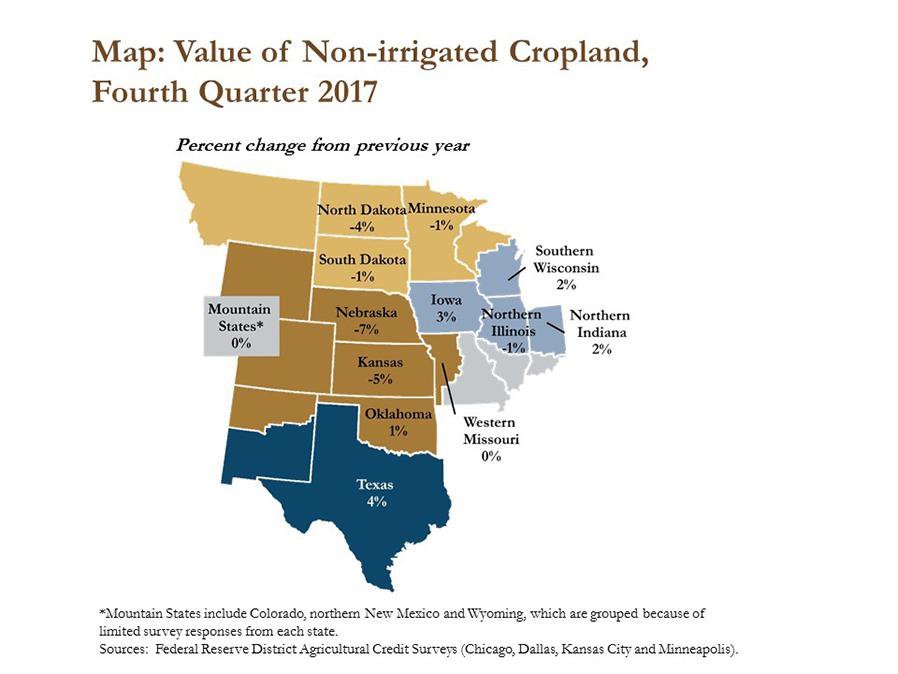

Farm real estate values also generally remained steady in the fourth quarter. Although the value of non-irrigated cropland declined in states located in the central and northern Plains, values increased slightly in other states throughout the Midwest (Map). After declining by an annual average rate of 4 percent from 2013 to 2016, cropland values in Iowa increased about 3 percent in 2017 when compared with a year earlier.

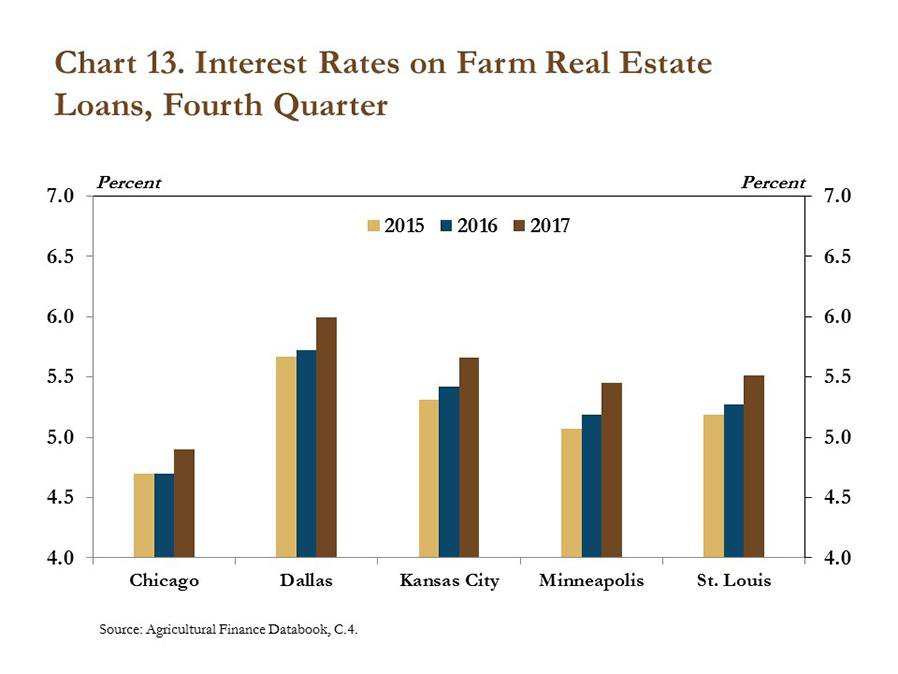

Consistent with national trends, however, interest rates on farm real estate loans increased in all regions in the fourth quarter. According to Federal Reserve district surveys of agricultural banks of varying sizes, interest rates on farm real estate loans increased by about 25 basis points between the fourth quarter of 2016 and the fourth quarter of 2017 (Chart 13). Although the increases have been relatively modest, additional increases could continue to put downward pressure on the value of farmland in states throughout the Midwest and the Plains.

Conclusion

Interest rates on farm loans have continued to inch higher, but the increases have had a rather modest effect on producers’ overall expenses. Despite the modest increase in interest expenses, higher interest rates typically are expected to place downward pressure on farmland values, which may still have a more significant effect on farm finances than interest expenses directly. Farmland values, however, have continued to remain relatively steady and, even in a higher interest rate environment, have provided ongoing stability to farm sector balance sheets and agricultural lending.

Data and Information

The views expressed are those of the authors and do not necessarily reflect the positions of the Federal Reserve Bank of Kansas City or the Federal Reserve System.

Author