Section A – First Quarter Survey of Terms of Bank Lending to Farmers

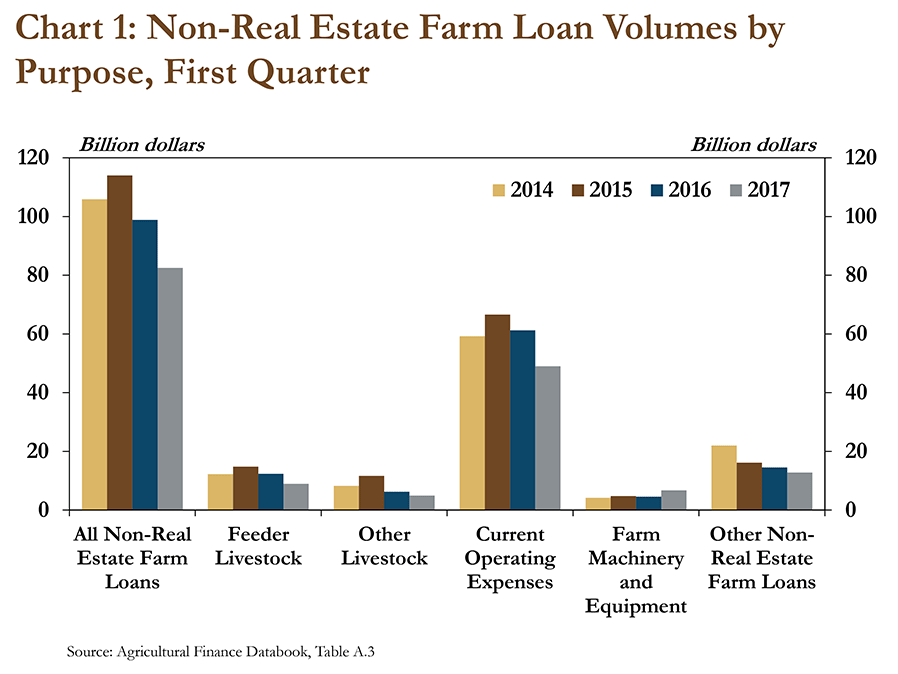

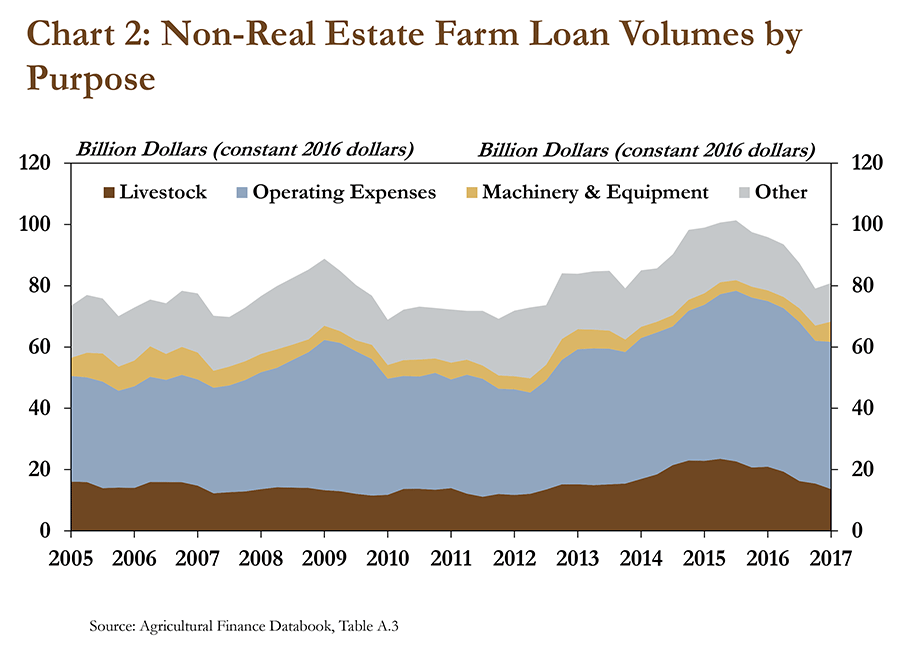

Farm lending at commercial banks continued to moderate in early 2017. The volume of non-real estate farm loans originated in the first quarter declined 16 percent from the previous year, according to the Survey of Terms of Bank Lending to Farmers (Chart 1). The decrease in the first quarter was the sixth consecutive year-over-year decline in the volume of new non-real estate farm loans and followed a significant drop in the fourth quarter of 2016 (Chart 2).

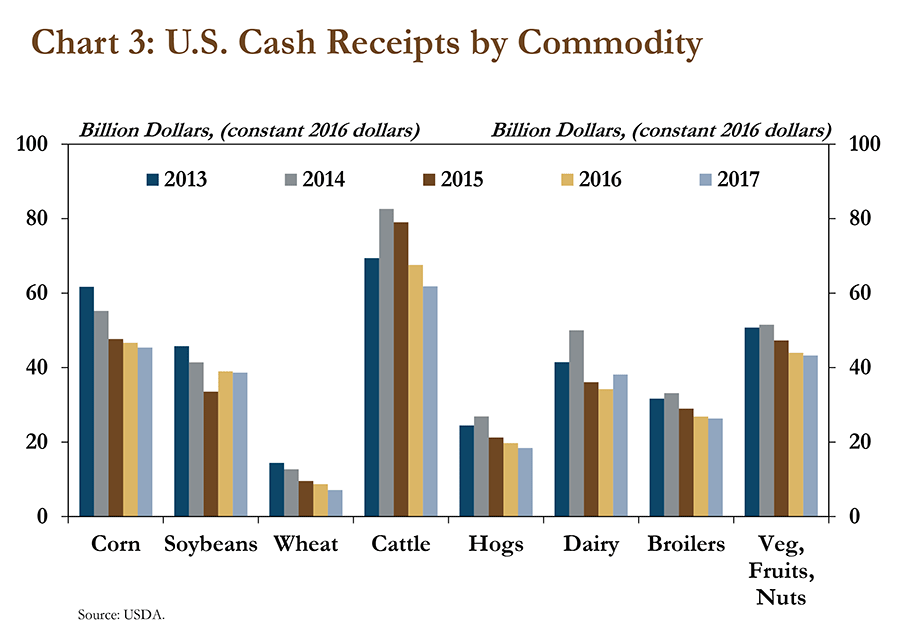

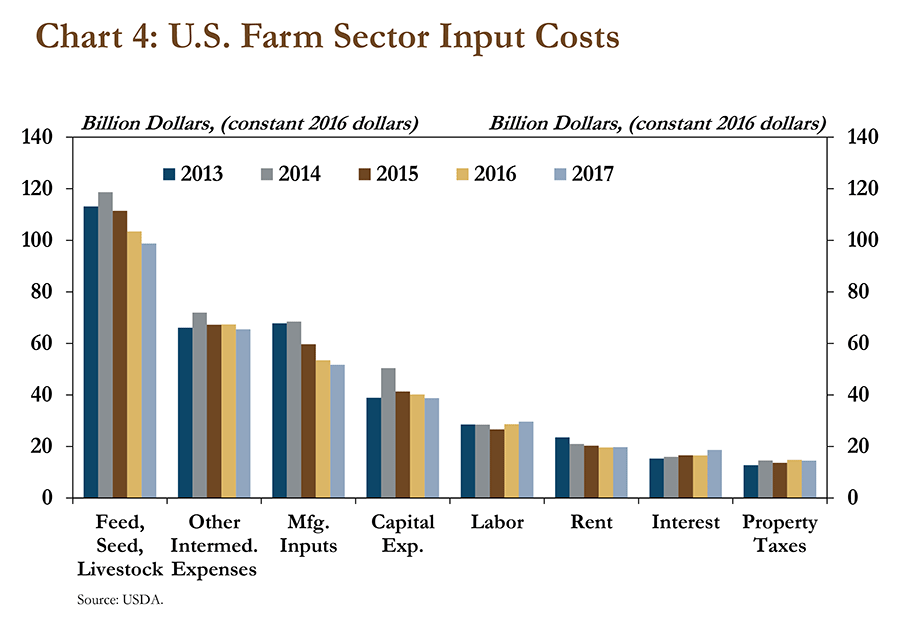

Persistent declines in farm income have remained a primary driver of reduced lending in the farm sector. Revenue from the production of most agricultural commodities is expected to decline again in 2017 (Chart 3). For example, cash receipts generated from the sale of corn, soybeans, wheat and cattle are forecasted to decline more than 5 percent from 2016. Some producers have sought to make adjustments to production practices by reducing input costs when it has been possible to do so (Chart 4). These reductions in farm spending, stemming from persistent declines in farm income, likely have contributed to reductions in the volume of new farm loans.

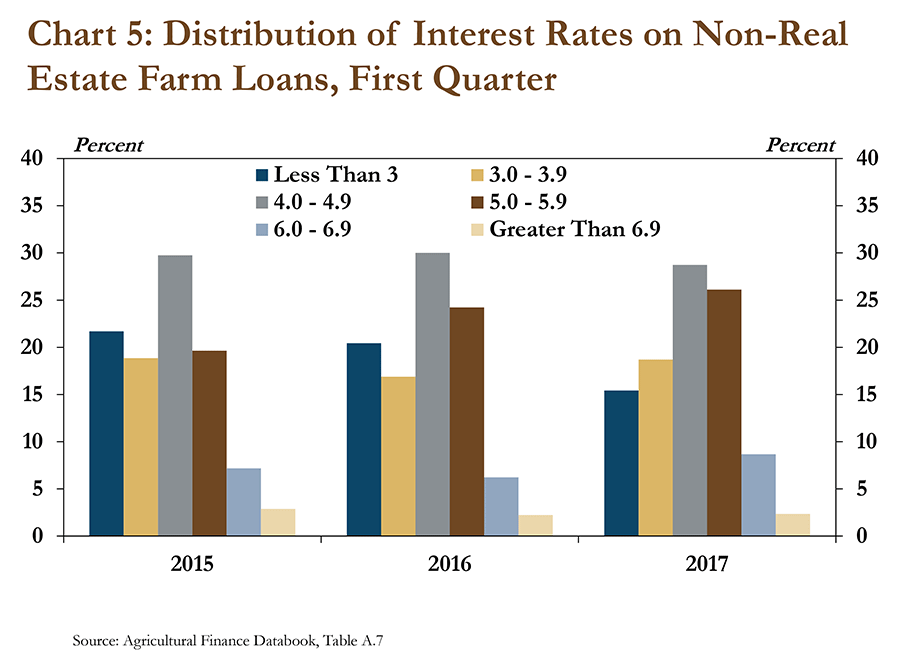

As farm income and farm finances generally have continued to tighten, agricultural lenders have made more adjustments to loan terms in recognition of the heightened risk. In the first quarter, the average interest rate of all agricultural loans increased 27 basis points from the previous year and fewer loans were extended with interest rates of less than 3 percent (Chart 5). In 2015, 22 percent of non-real estate farm loans were made with interest rates of less than 3 percent, but only 15 percent of those loans in the first quarter of 2016 were at rates less than 3 percent.

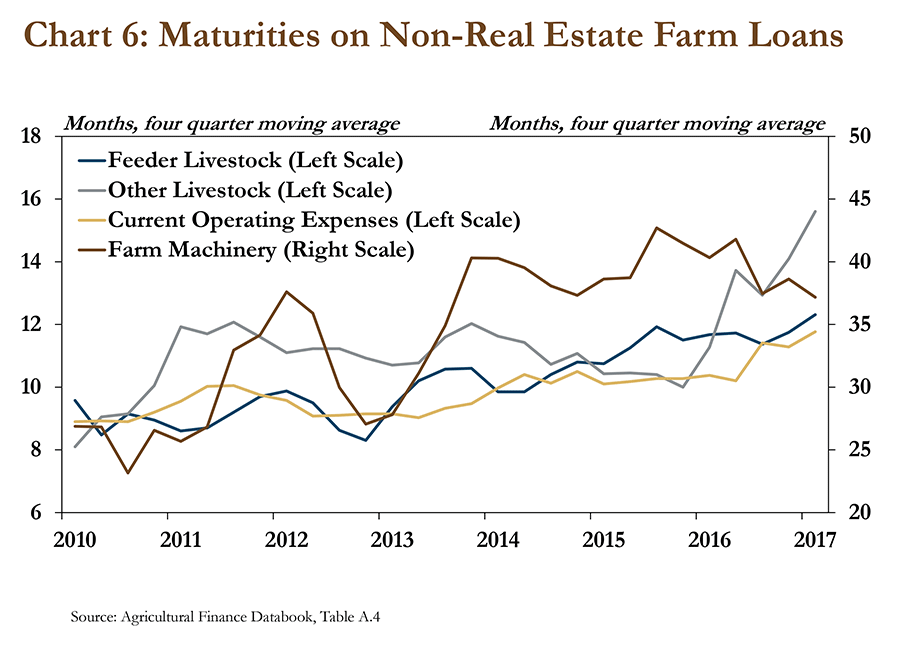

Bankers also continued to extend amortizations for most loan types in recognition of reduced capacity for repayment. Specifically, the maturity period for operating loans, which typically account for the majority of non-real estate lending at agricultural banks, increased 22 percent from 2016 and was three months longer than in 2010. Maturity periods for livestock loans also have continued to increase in recent years (Chart 6).

Section B – Fourth Quarter Call Report Data

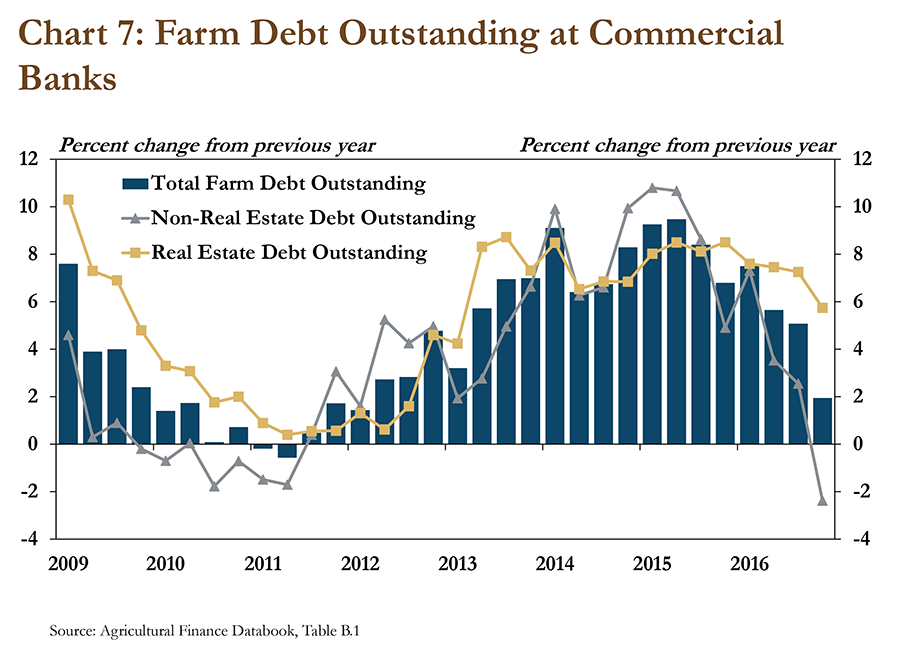

In the fourth quarter of 2016, total farm debt at commercial banks continued to increase, but at a much slower pace than previous quarters. According to Call Report data, total farm debt outstanding increased by slightly less than 2 percent from the previous year, the slowest growth since the first quarter of 2012 (Chart 7). Non-real estate debt decreased for the first time since 2011 and was the primary driver of slower loan growth in the fourth quarter. In 2011, however, non-real estate lending declined largely as a result of surging commodity prices and increased revenue in the farm sector. More recently, farm lending has slowed alongside persistent weakness in the farm economy.

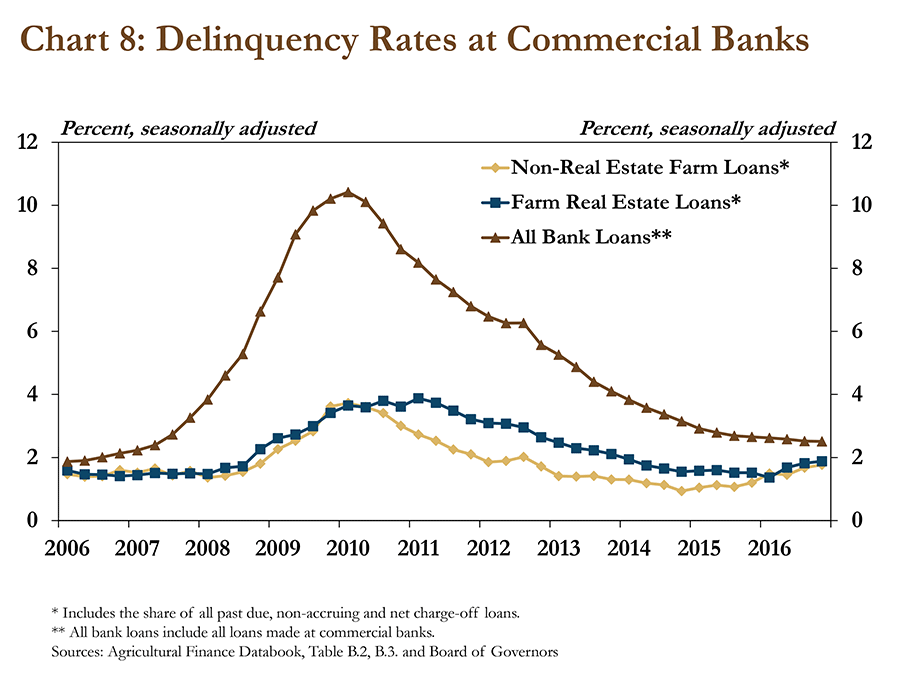

Ongoing weakness in the farm sector has continued to affect loan performance, but only at a very modest pace. Delinquency rates for farm real estate loans increased slightly in the fourth quarter, the third consecutive quarterly increase, but still remained historically low (Chart 8). Delinquency rates for non-real estate farm loans also increased, but for both real estate and non-real estate farm loans, delinquency rates remained significantly less than all loan categories combined.

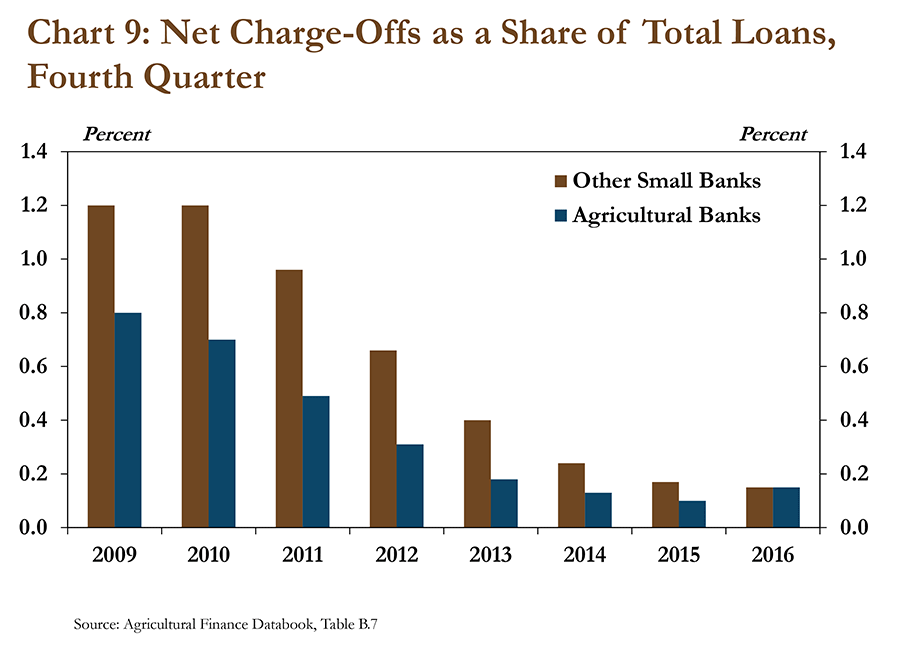

Alongside only slight increases in delinquency rates, loan performance at agricultural banks still was similar to non-agricultural banks. In the fourth quarter, the share of net charge-offs, a typical measure of loan performance, was similar to the share of net charge-offs at other small banks (Chart 9). Although charge-offs at agricultural banks increased in 2016, the total remained well below the historical average.

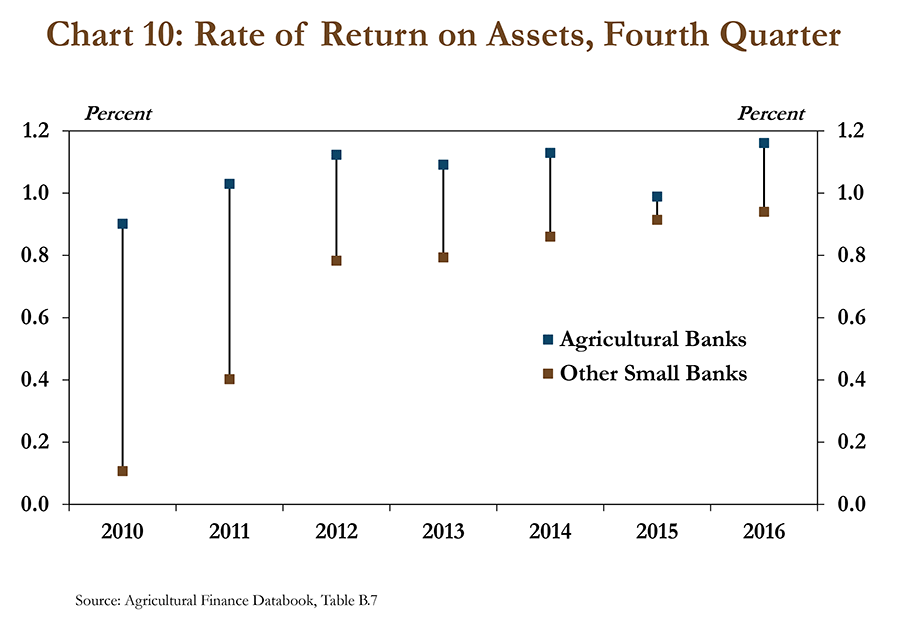

Returns at agricultural banks remained stable despite ongoing weakness in the farm economy. The rate of return on assets in the fourth quarter increased 0.17 percent from the prior year at agricultural banks and remained similar to the previous four years (Chart 10). Moreover, the rate of return at agricultural banks remained higher than at other similarly sized commercial banks.

Section C – Fourth Quarter Regional Agricultural Data

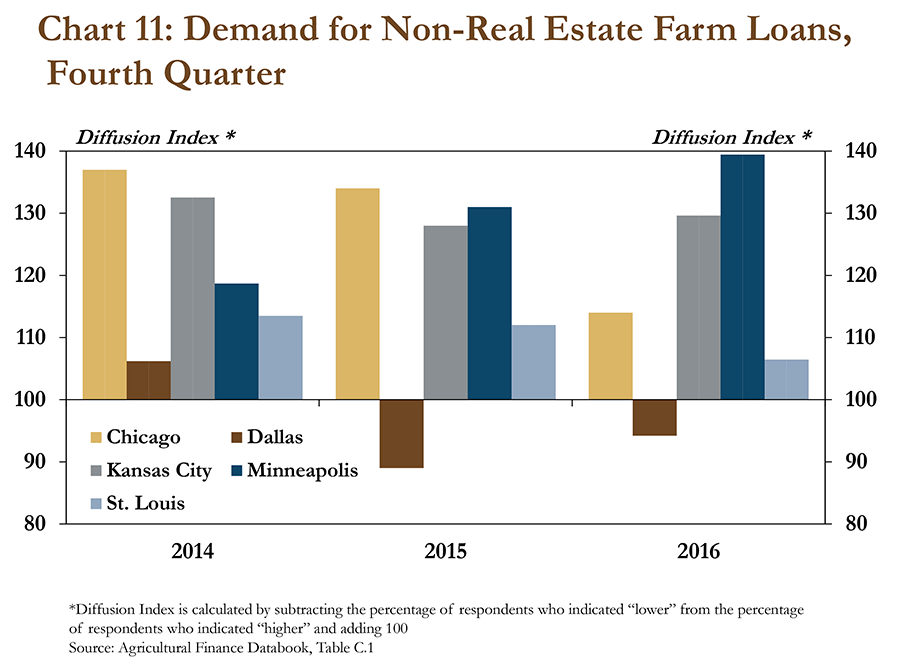

Despite slower lending activity in the farm sector, regional Federal Reserve surveys generally pointed to strong demand for farm loans, but at a somewhat slower pace. The surveys indicated demand for financing increased in the Chicago, Kansas City, Minneapolis and St. Louis districts in the fourth quarter of 2016 (Chart 11). However, the rate of increase was slower in the Chicago and St. Louis districts than in recent years. Ongoing cash flow shortages have remained a primary driver of demand for farm loans in these districts, but reduced farm spending and increased scrutiny on borrowers’ applications may have slowed the recent pace.

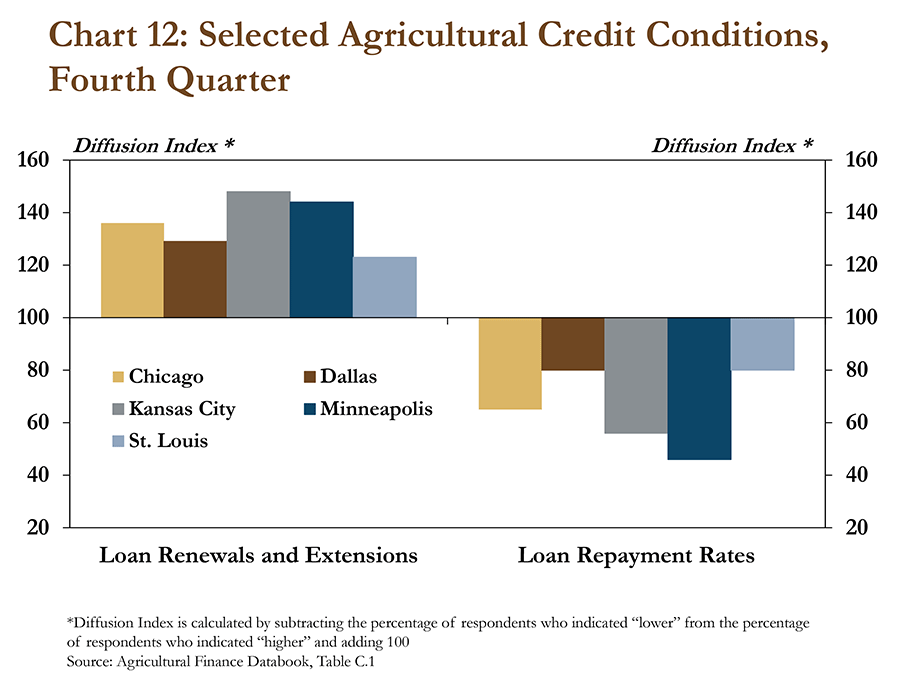

Demand for farm loan renewals and extensions also increased in the fourth quarter. In fact, each district that surveys its respective agricultural banks recorded increased demand for loan renewals and extensions at the end of 2016 (Chart 12). The fourth quarter was the eighth consecutive quarter that each district reported higher demand for loan renewals and extensions and lower repayment rates.

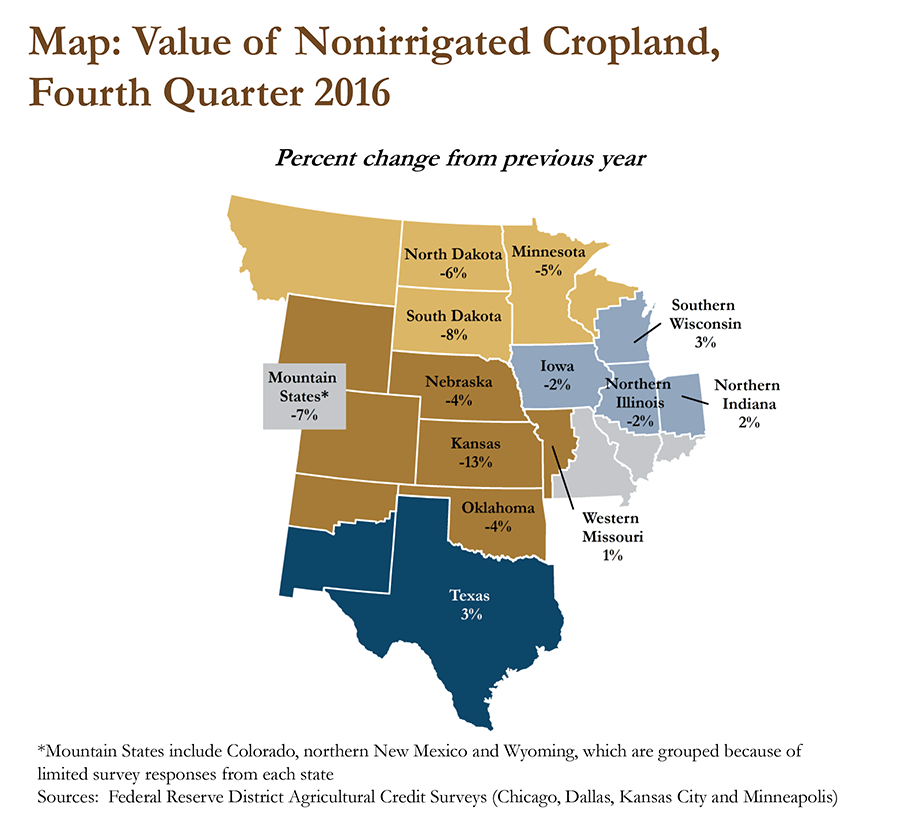

A gradual, but steady softening in the farm economy has continued to push down the value of farmland throughout agricultural-production regions. Farmland values in most states in the Chicago, Kansas City and Minneapolis districts declined at a moderate pace from the previous year (Map). Most bankers generally indicated they expect farmland values to continue to moderate in the coming months, which could intensify financial stress in the farm sector, particularly in regions that have experienced significant declines in farm income and farmland values.

Conclusion

Farm lending at commercial banks has declined significantly for two consecutive quarters, indicating that some adjustments are being made in an environment of persistent weakness in the farm economy. In the 1980s, the accumulation of debt during the early years of the downturn in the farm economy contributed significantly to the crisis that developed later. Although the current downturn has persisted for several years and could still intensify, the adjustments being made could also place the farm sector in a more stable longer-term position.

____________________________________________

The views expressed are those of the authors and do not necessarily reflect the positions of the Federal Reserve Bank of Kansas City or the Federal Reserve System.

Author