Farm income and agricultural credit conditions improved significantly according to agricultural lenders across major portions of the U.S. in the fourth quarter. Despite tumultuous conditions related to the ongoing pandemic throughout 2020, the prices of several key agricultural commodities increased sharply in the final months of the year. Dramatic improvements in crop prices drove the sharpest turnaround in agricultural lending conditions in more than a decade.

Fourth Quarter Federal Reserve District Ag Credit Surveys

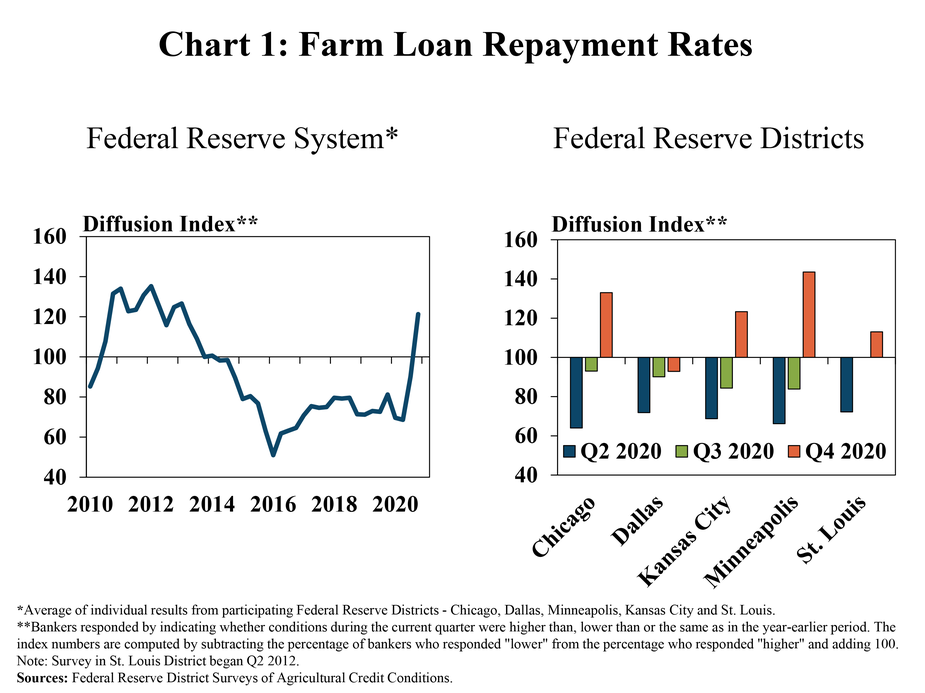

Following years of steady deterioration, various measures of agricultural credit improved in the fourth quarter. On average, farm loan repayments increased for the first time since 2013 according to regional Federal Reserve surveys of agricultural lending (Chart 1). The rate of loan repayment increased from a year ago in all participating Districts expect Dallas, with the fastest pace of increase reported in the Minneapolis and Chicago Districts.

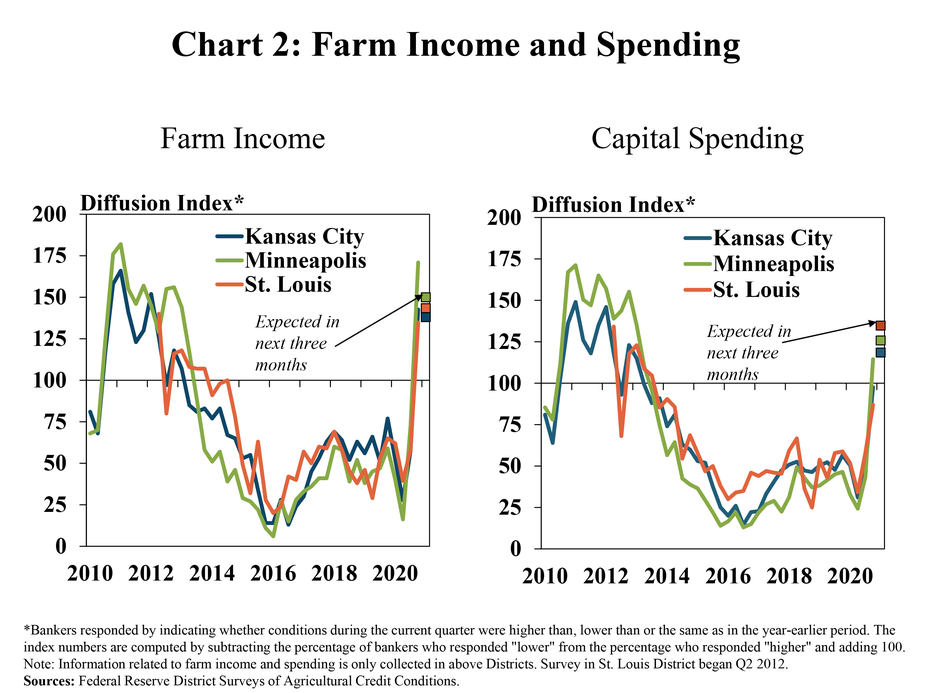

An increase in farm income in the fourth quarter appeared to be a primary driver of the recent strength in agricultural credit conditions. Similar to loan repayment rates, farm income was higher than a year ago across all participating Districts (Chart 2). With better financial outcomes in 2020, capital spending plans of farm borrowers also strengthened in the fourth quarter and were expected to increase in all Districts in coming months.

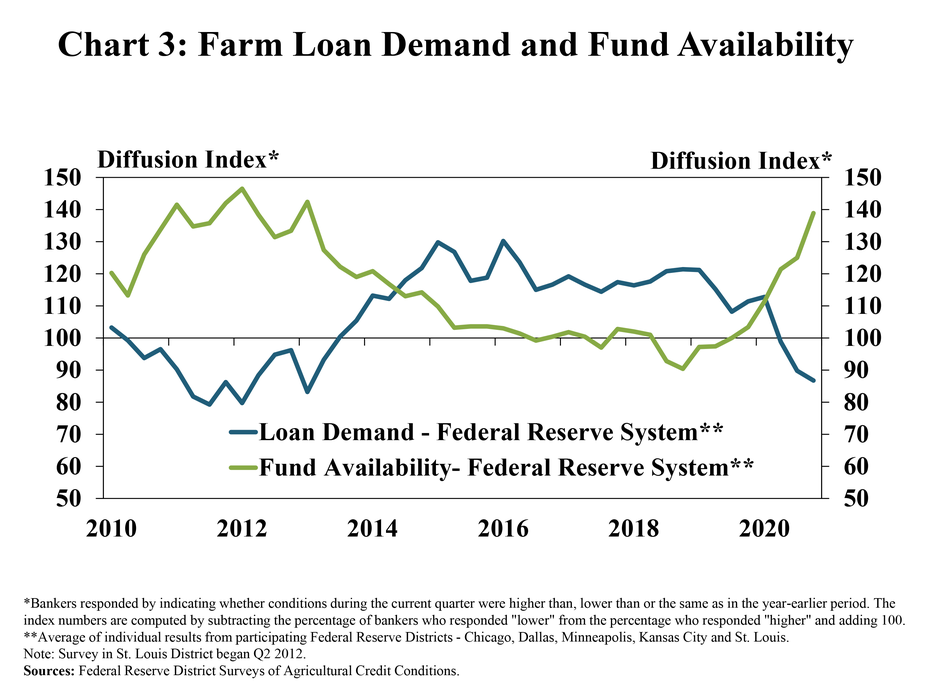

Other financial indicators also shifted quickly in the fourth quarter as borrowers experienced relief from previous years of financial stresses. On average across all Districts, loan demand contracted at the fastest pace since 2013 and fund availability increased at the fastest pace since 2013 according to agricultural bankers (Chart 3). The path of both indicators was consistent across all regions, but loan demand declined at the quickest rate in the Dallas District and liquidity growth was strongest in the Chicago District.

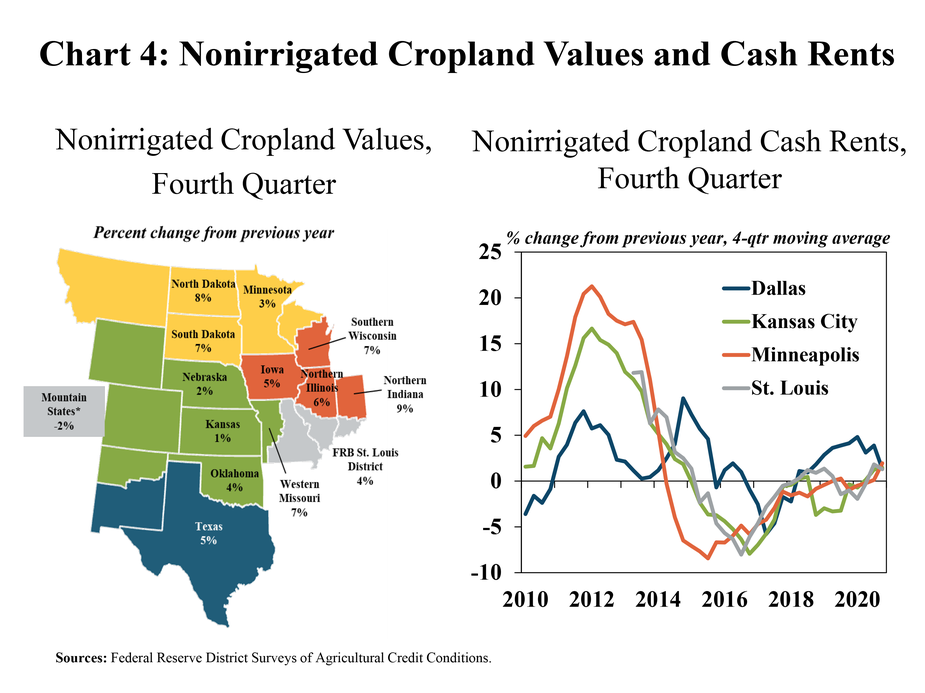

Farmland values and cash rents remained strong across most reporting states. Although drought seemed to put some pressure on farm real estate markets in the Mountain States, values for nonirrigated cropland increased in all other states in the fourth quarter (Chart 4). Gains were strongest in the Upper Plains and Corn Belt, where farmland values rose by 8% in North Dakota and 9% in Northern Indiana. Cash rents on nonirrigated cropland also increased moderately. In the Dallas, Kansas City, Minneapolis, and St. Louis Districts, cash rents rose an average of about 2% in the fourth quarter.

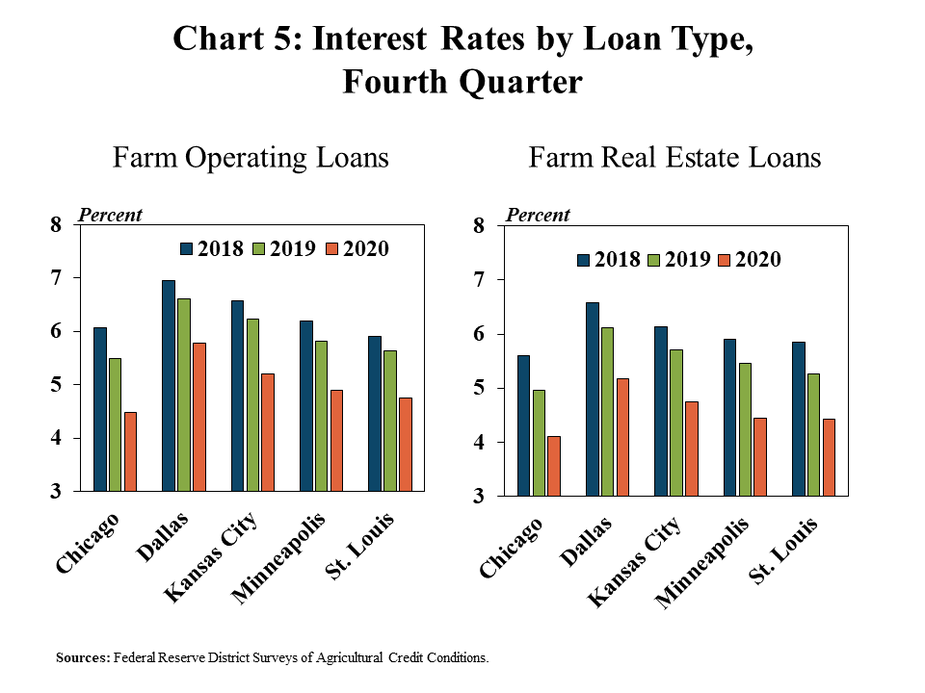

Lower interest rates have likely provided some support to farm finances and the values of farm real estate. Compared to the previous year, rates on short-term operating loans and long-term farm real estate loans fell by approximately one percentage point at agricultural banks across the United States in the fourth quarter (Chart 5). The sharpest pace of decline was reported in the Chicago District, where interest rates on operating loans have fallen by 1.6 percentage points since 2018.

Conclusion

Agricultural credit conditions improved in the fourth quarter alongside increases in commodity prices and strong support from government payments. Bankers reported an increase in farm income for the first time in eight years, driving an increase in farm loan repayment rates, a decrease in loan demand and expected increases in spending. Stronger economic and credit conditions in the sector also supported gains in farm real estate in numerous regions. While continued weakness in cattle markets and harsh weather conditions still left headwinds for some producers, the overall outlook for agricultural credit conditions going into 2021 was markedly more optimistic than recent years.

Data and Information

Federal Reserve Ag Credit Surveys Historical Data

The views expressed in this article are those of the authors and do not necessarily reflect the views of the Federal Reserve Bank of Kansas City or the Federal Reserve System.

Author