After a run of profits fit for the record books from 2010 to 2013, many crop producers have been facing progressively tighter margins and incomes. The conditions that brought record profits have quickly eroded during the past two years, causing the debt servicing and operating structures for many producers to change considerably. An increased debt burden, persistently lower profit margins and existing headwinds for crop prices could continue to affect the U.S. farm economy into 2016, and further intensify concerns about emerging financial stress for the sector.

Farm Income

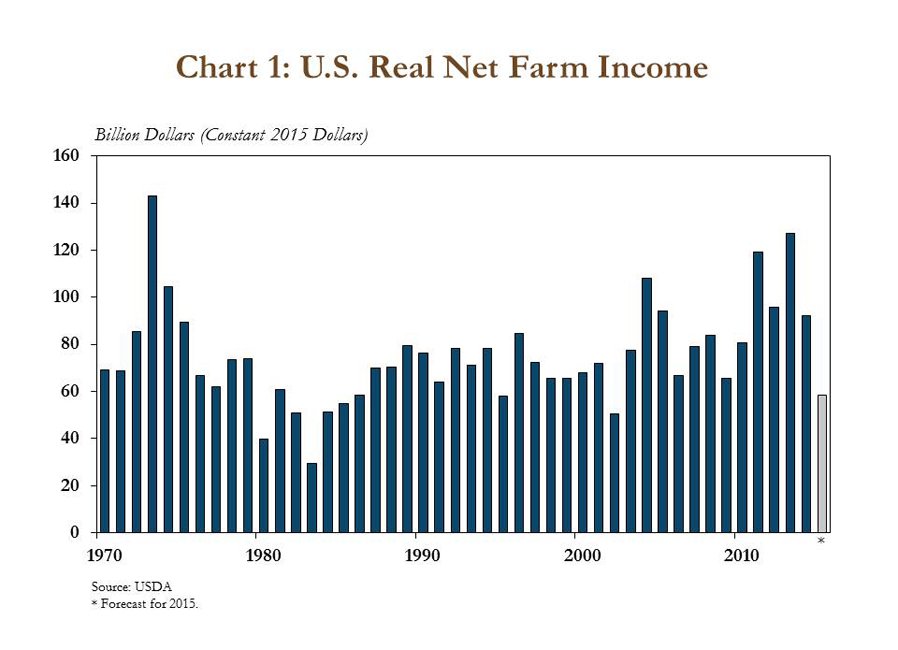

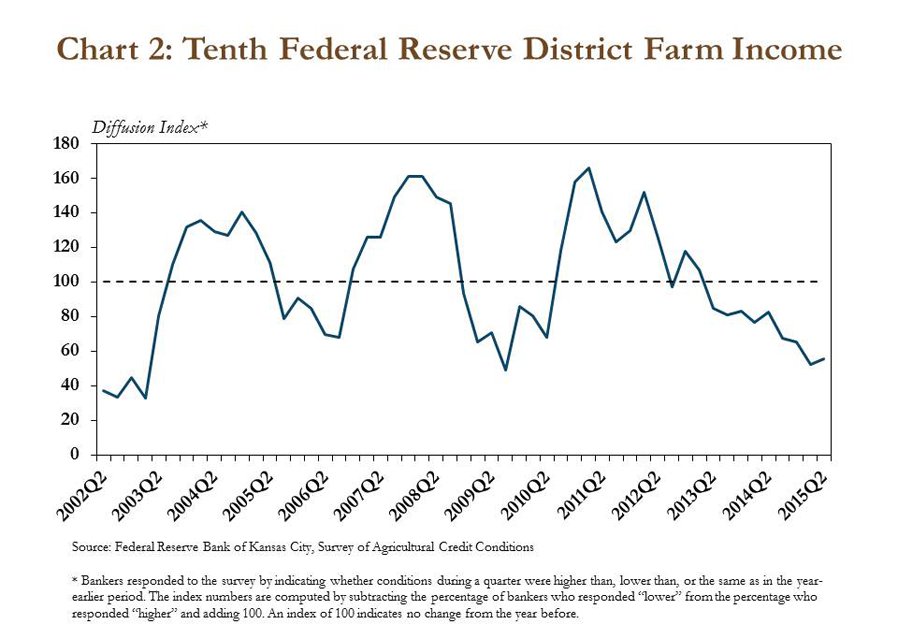

Farm income has continued to drift lower since 2013. In August of this year, the United States Department of Agriculture (USDA) lowered its forecast for 2015 net farm income to $58.3 billion (Chart 1). The Federal Reserve Bank of Kansas City’s Survey of Agricultural Credit Conditions has shown a similar decline in farm income for states in the Tenth Federal Reserve District (Chart 2). If the USDA’s 2015 farm income forecast stands, it would represent a 36 percent drop from 2014 and a 54 percent plunge from just two years ago. Moreover, the forecast for 2015 would also represent the second lowest measure of farm income since the mid-1980s.

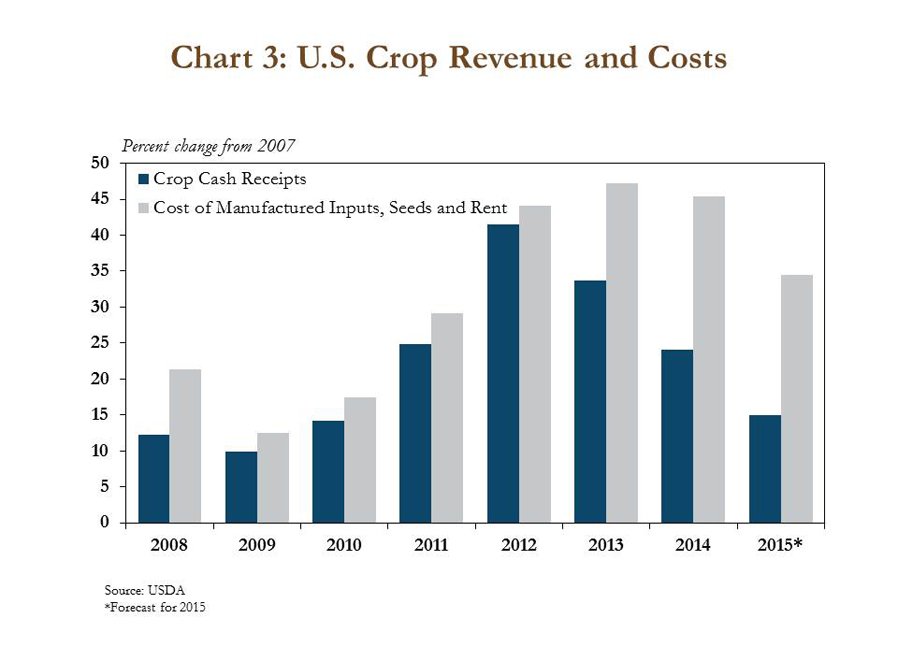

A sharp decline in U.S. crop revenue and “sticky” input prices have been major factors contributing to the projected decrease in farm income. According to the USDA, feed, food and oil crop cash receipts are expected to drop more than $12.5 billion in 2015, a decline of 37 percent from the year before (Chart 3). Meanwhile, crop production expenses, though forecasted to be slightly lower in 2015, have remained relatively high. Dairy and beef cash receipts are also expected to fall by $22 billion from 2014 levels, a decline of 37 percent. In the case of livestock products, however, 2014 represented a record year for profits among many operations, and returns in the cow-calf sector have remained strong through 2015.

Debt Structure

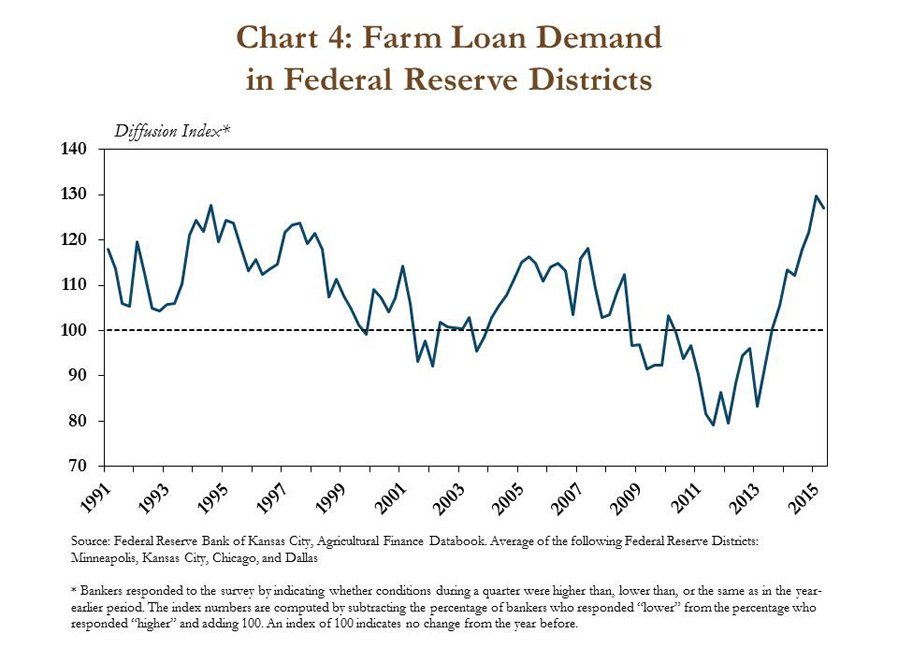

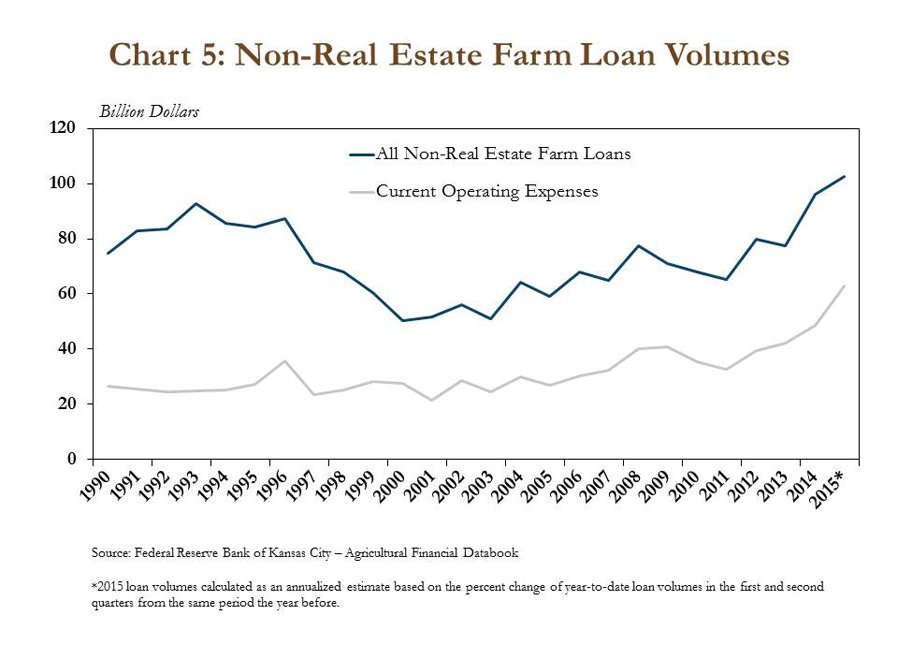

Weaker farm income and depressed crop prices have forced operators to burn through working capital and increase their usage of operating loan lines. As highlighted in the Federal Reserve Bank of Kansas City’s Agricultural Finance Databook , bankers throughout Federal Reserve Districts located in concentrated agricultural regions have reported steady increases in loan demand since the second quarter of 2013 (Chart 4). Moreover, the increased lending activity has been primarily due to a greater need for financing operating expenses (Chart 5).

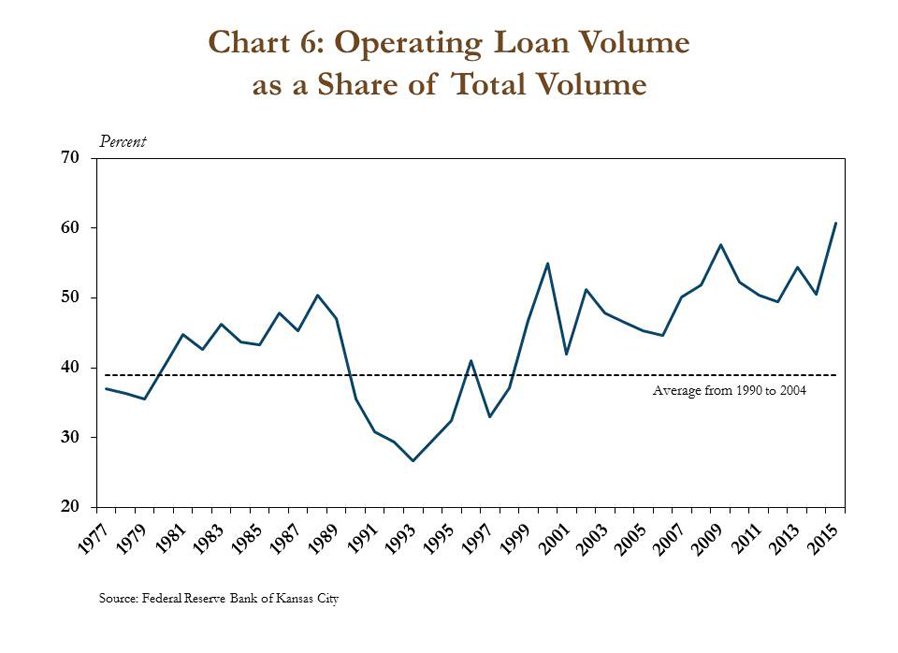

The increase in operating loans has significantly altered the debt structure for many agricultural producers. According to the Agricultural Finance Databook, the volume of loans used to finance operating expenses now accounts for more than half of new non-real estate farm loans originated at agricultural commercial banks (Chart 6). This ratio compares with an average of 39 percent from 1990 to 2004.

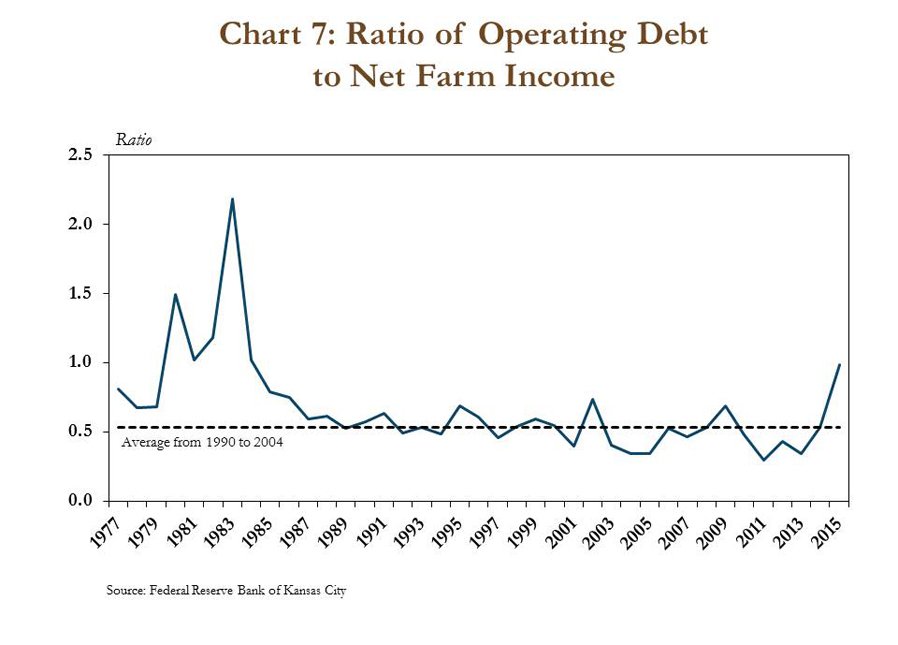

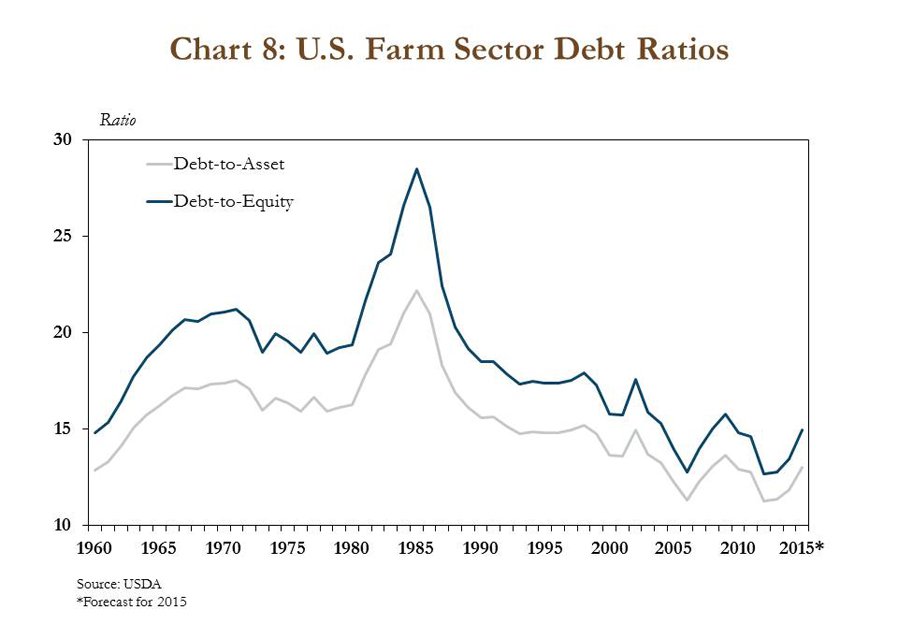

Perhaps warranting more concern, however, is that the increased short-term debt burden has occurred alongside two consecutive years of declining farm income. Using data from the Agricultural Finance Databook and USDA, the ratio of operating loans to net farm income has surged dramatically the past two years (Chart 7). A ratio above 1.0 is a level where producers would ultimately need to draw on other income sources or accumulated wealth to pay for recurring operating costs. Since the mid-1980s, this ratio has averaged only 0.54. In 2015, however, the ratio has spiked to 0.99, and could soon eclipse the 1.0 mark for the first time since the early 1980s. This sign of an increasing debt burden is also consistent with USDA’s expectation of a slight uptick in both debt-to-equity and debt-to-asset ratios (Chart 8).

Crop Price Structure

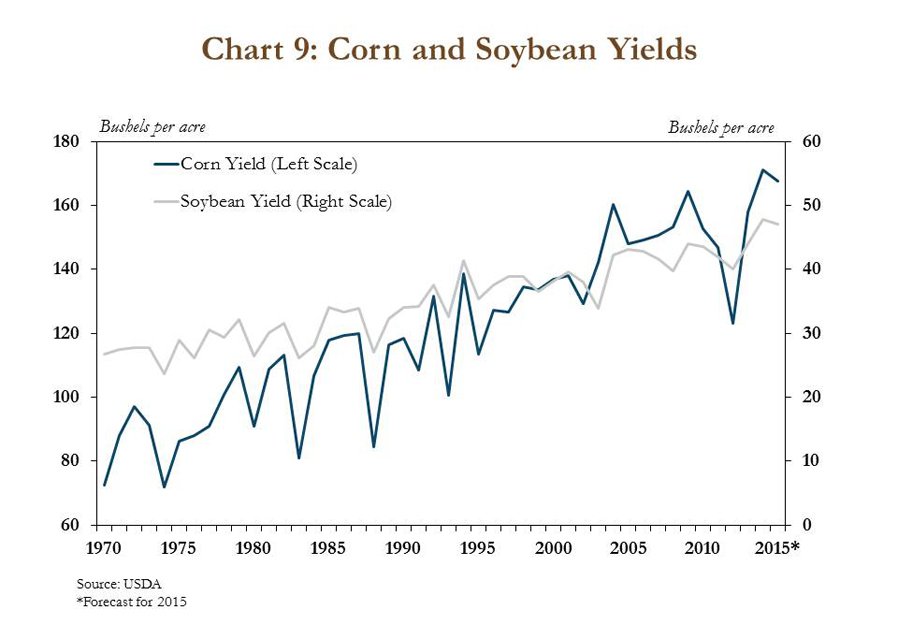

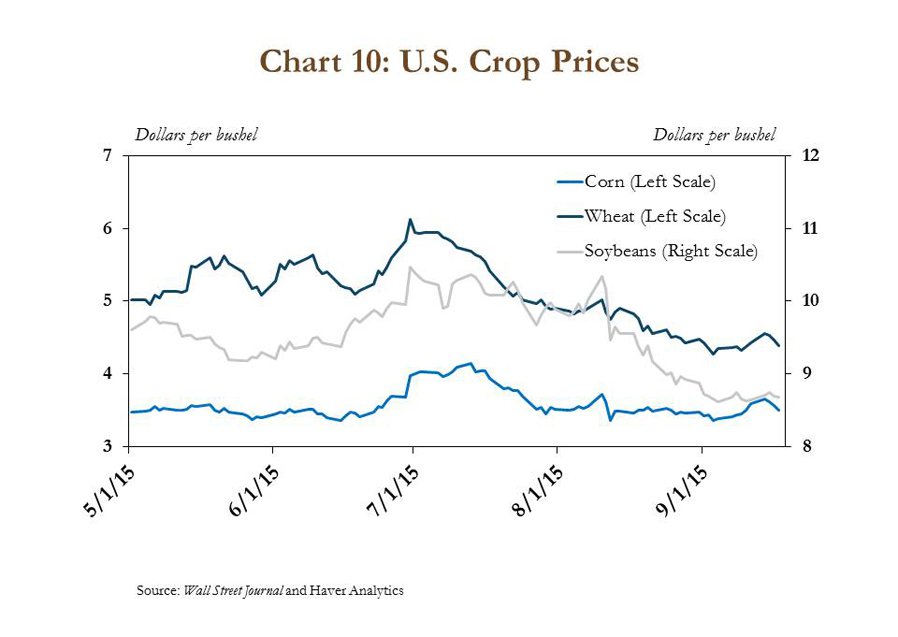

Concerns surrounding farm finances will significantly depend on the outlook for agricultural commodity prices in the coming year. Crop prices were somewhat volatile during this year’s summer growing months but appear to have generally stabilized recently. Despite some remaining uncertainty surrounding the fall crop harvest in the United States, though, corn and soybean yields are expected to be historically high in 2015 (Chart 9). Corn, soybean and wheat prices have all returned to levels at, or below, those observed before the mid-summer run-up due to the relatively strong harvest expectations (Chart 10).

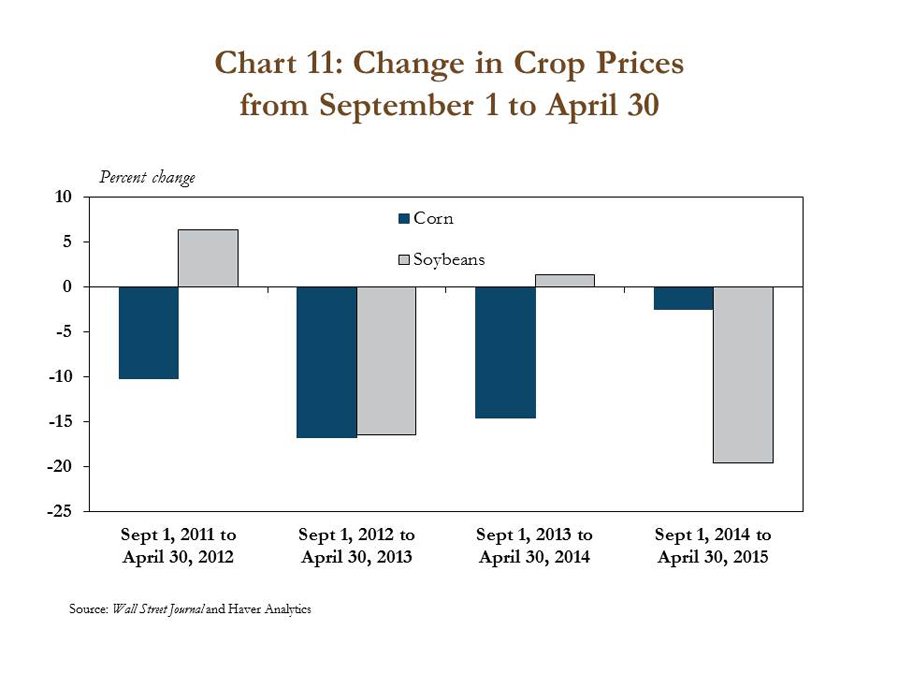

Looking ahead, it is noteworthy that recent years have shown very few price gains from the fall harvest in one year to the next year’s planting season. Since 2011, significant declines in corn and soybean prices have, in fact, been more common than notable price increases (Chart 11). With expectations of a relatively strong harvest this year, a substantial rebound in U.S. crop prices before next year’s growing season, then, would likely need to come from significant demand growth or international supply disturbances.

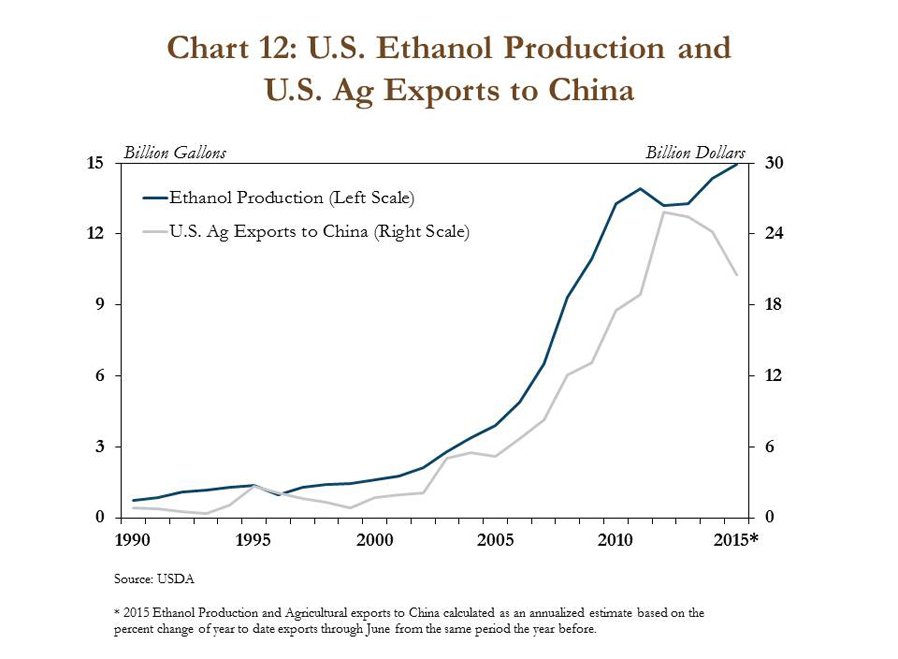

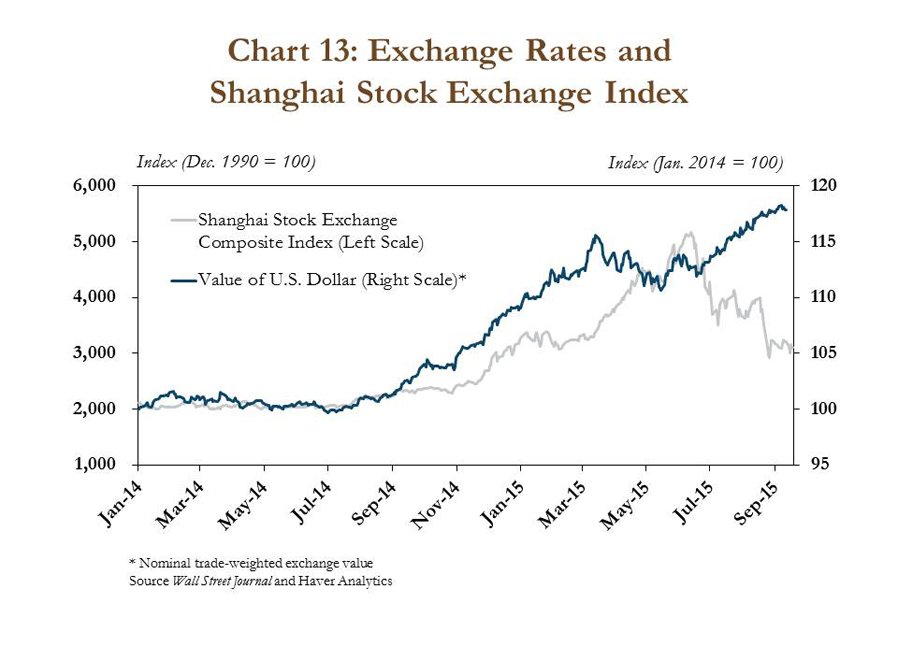

Barring significant supply setbacks in the coming months, however, recent demand trends point to further headwinds for U.S. crop prices. Two primary demand factors driving gains in crop prices over the past decade have been growth in Chinese consumption of U.S. agricultural products and an expanding U.S. biofuels sector. Since 2012, however, growth in U.S. ethanol production has slowed, and the value of agricultural products exported to China has declined (Chart 12). Recent volatility in the Chinese economy and a strengthening U.S. dollar, making U.S.-based exports more expensive for foreign buyers, have added to concerns about the potential for near-term demand growth originating from China (Chart 13). Sluggishness in both of these demand drivers, key in recent years, appears likely to keep downward pressure on crop prices heading into 2016.

Conclusion

Concerns about future financial stress in the farm sector have steadily intensified alongside a second consecutive year of declining farm income and rising debt levels. As 2015 winds down, underlying trends in the supply and demand for crops also appear unlikely to support major advances in crop prices in the coming months. Many producers have remained in a financially sound position through 2015, but a prolonged downturn through 2016 could start to challenge some of those financial positions.