The outlook for the agricultural economy has continued to become more pessimistic. Crop prices remained subdued in the second half of 2015 after stable growing conditions led to another year of near-record production forecasts in the United States and abroad. At the same time, flat consumption has bolstered domestic inventories, and the strengthening dollar and increasing competition from foreign markets have heightened concerns about declining U.S. agricultural exports. Recent supply and demand fundamentals have weighed on crop prices amid continued expectations for falling farm income in all states in the Tenth Federal Reserve District. Bankers have noted that farm household spending has remained elevated in some cases and that they are closely monitoring working capital and credit quality.

Production Outpacing Consumption

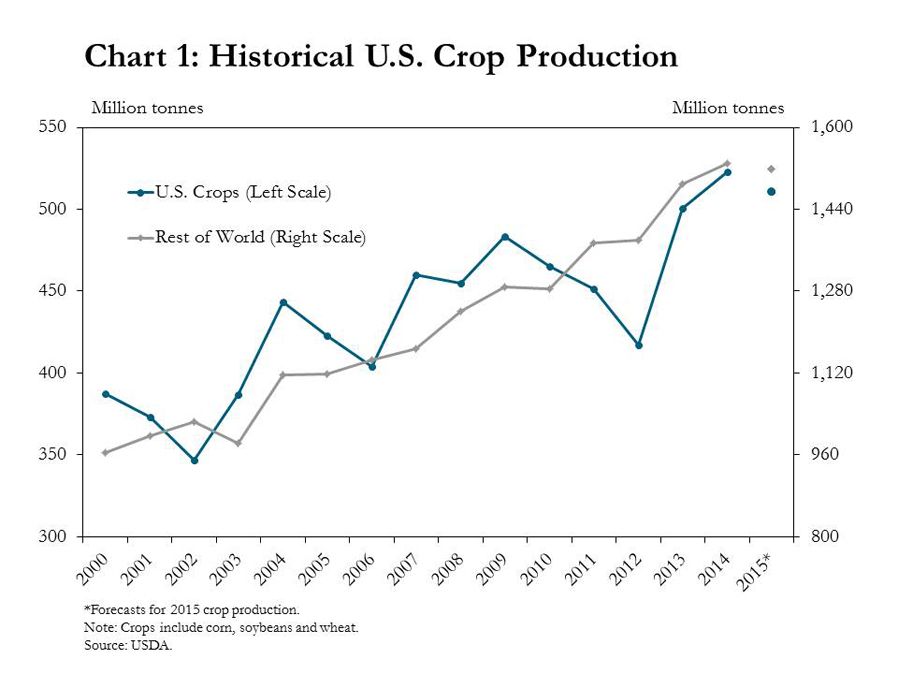

The U.S. Department of Agriculture (USDA) forecasted global crop production to remain near record levels in 2015. Following widespread drought that damaged the 2012 crop, production in the U.S. has been strong for three consecutive years (Chart 1). In November 2015, the USDA projected the soybean crop to be the largest in history and expected that the corn harvest could be the third largest ever. Production has also steadily expanded in the rest of the world with reports of near-record harvests in Brazil and the Black Sea region, for example.

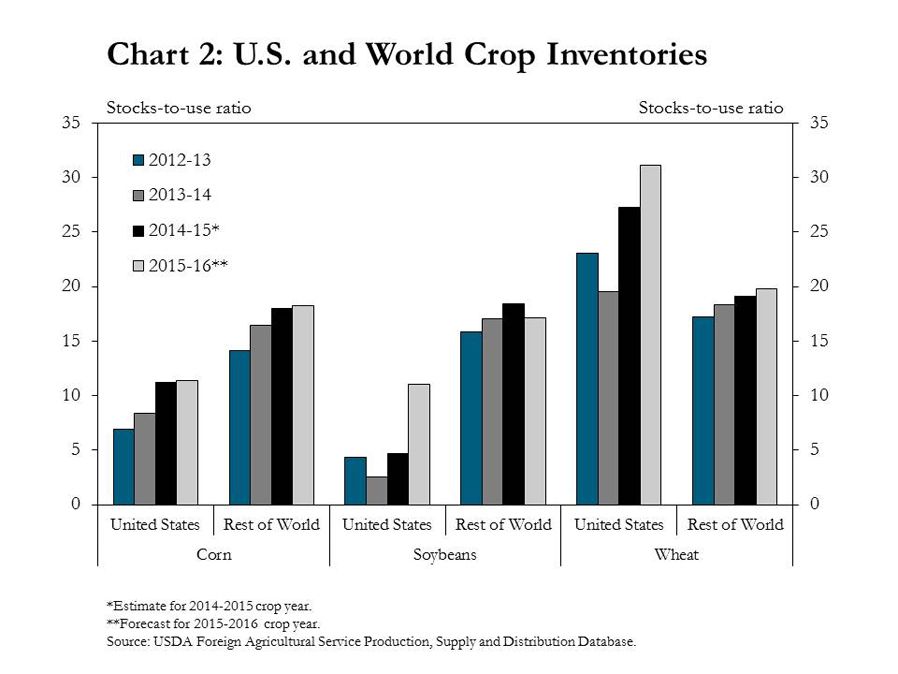

However, production in the United States since 2012 has expanded faster than consumption. Domestic consumption of key commodity crops has flattened over the last two years, and inventories are expanding across the globe, but particularly in the U.S. (Chart 2). On average, U.S. inventories of corn, soybeans and wheat have increased more than 100 percent since 2013, while use (or consumption) has increased just 7 percent over the same period.

Strong Dollar Hampering U.S. Ag Exports

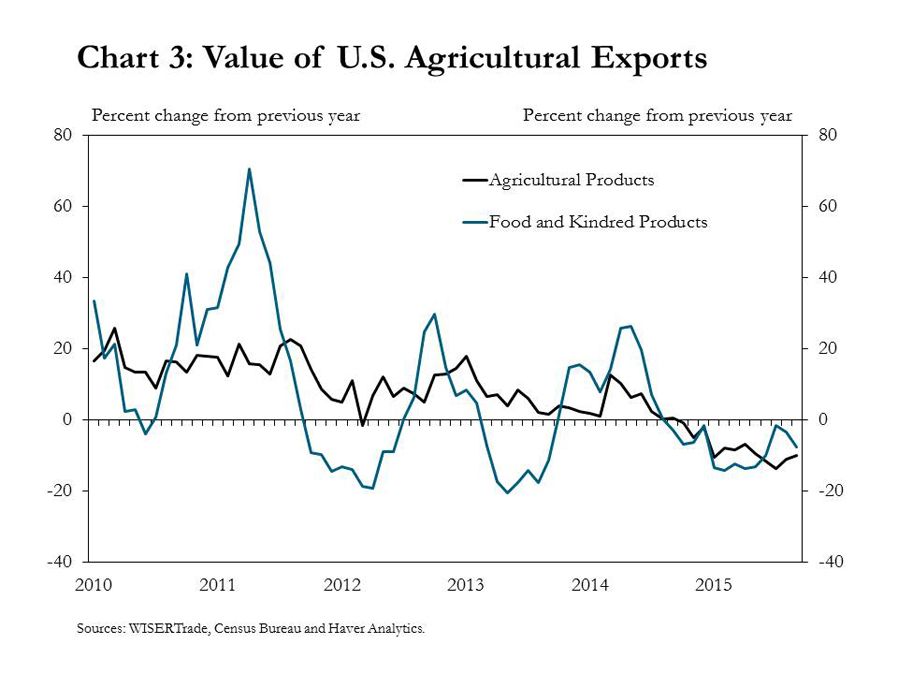

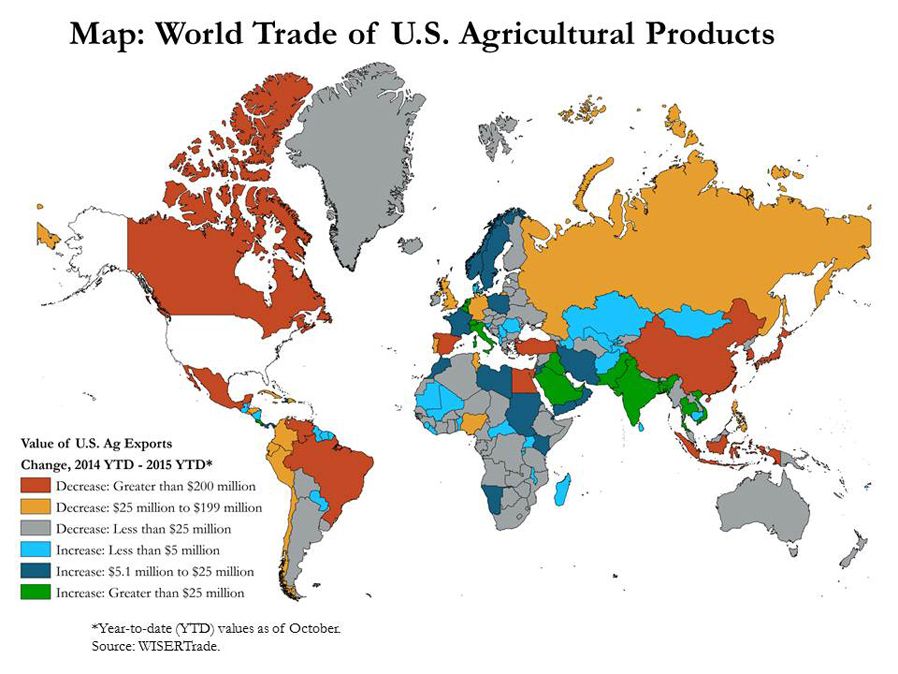

In addition to stagnant domestic demand, softening global demand and growing competition are hampering U.S. exports of agricultural products. In fact, exports of food and kindred products, including processed meat products, have declined for 14 consecutive months (Chart 3). Exports of agricultural products, including bulk commodities, also have continued to decline. Exports decreased about 10 percent, on average, each month in 2015 compared to 2014. As of October 2015, the value of U.S. agricultural exports declined from 2014 by more than $6 billion. China accounted for 20 percent of the loss in export value, with other major losses stemming from Canada, Mexico, Brazil, Japan, Egypt and South Korea (Map).

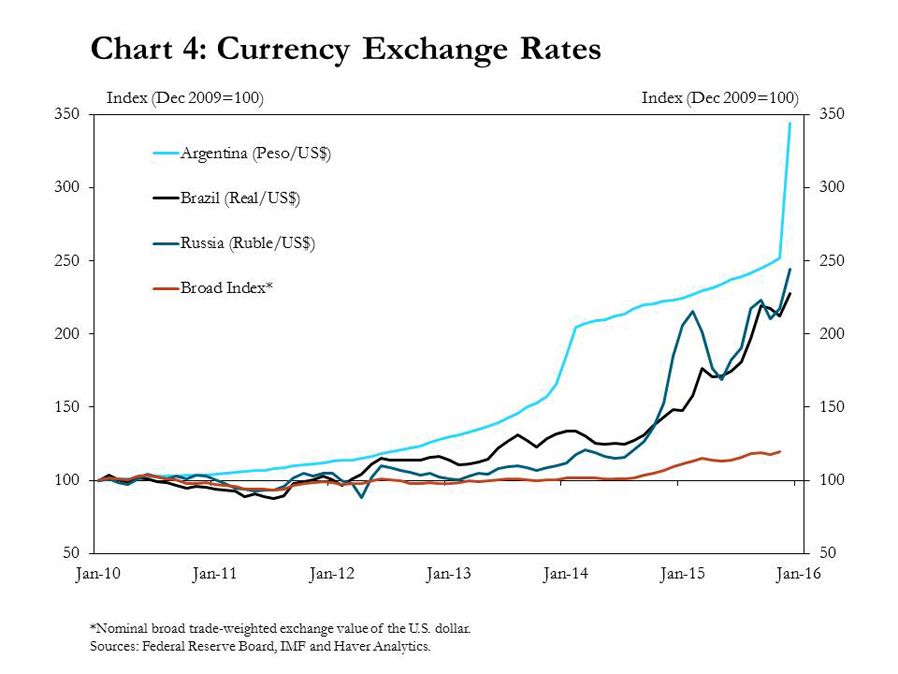

One reason for the recent drag on U.S. agricultural exports has been the strengthening dollar. In addition to the broad measure of currency exchange rates, the value of the dollar has risen against two regions that are significant competitors for global agricultural exports: South America and the former Soviet Union (hereafter abbreviated FSU) (Chart 4). Anecdotally, contacts with ties to commodity markets in the Tenth District have reported that weak exports have negatively affected their businesses, and most have attributed a significant portion of such weakness to a strong dollar.

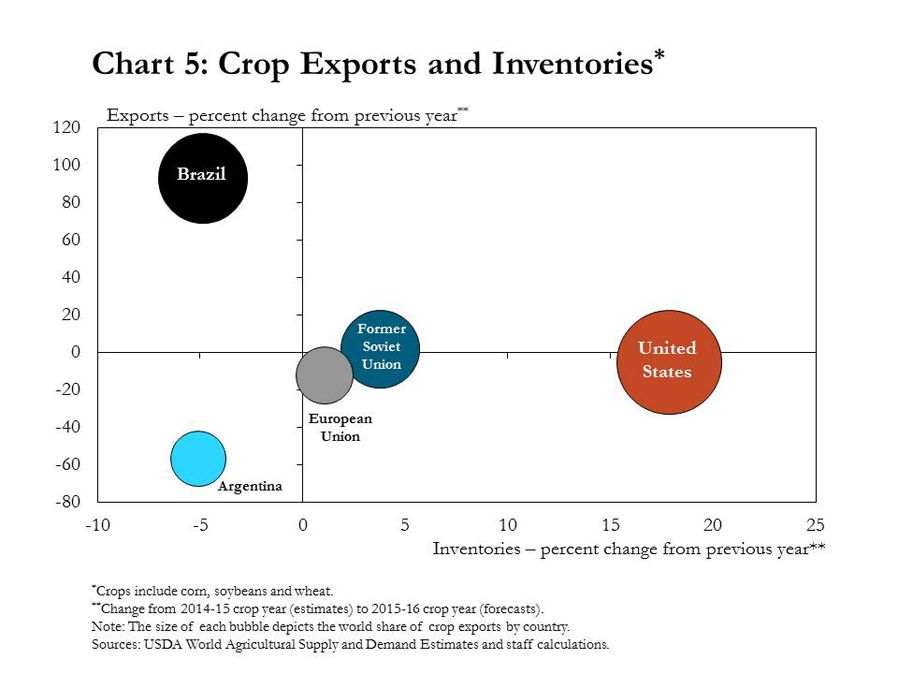

Recent developments in currency exchange rates corresponded to growing competition for global agricultural exports of three major commodity crops: corn, soybeans and wheat. The United States, the European Union, Brazil, Argentina and the FSU countries collectively represent about 80 percent of world crop production and exports. The United States has maintained the largest share of crop exports (28 percent in 2015), followed by Brazil and the FSU (Chart 5). Although shares of exports from the United States and FSU have remained relatively constant, the USDA estimated that Brazil’s share of world crop exports would double between the 2014 and 2015 crop years.

Current trends in agricultural exports and U.S. inventories have highlighted two important points. First, compared to other major crop exporters, the United States is projected to see the largest increase in inventories for the coming year, even as inventories among other competitors are expected to remain steady, or even decline as is the case in Brazil and Argentina. Second, the scale of the expected increase in Brazilian exports was estimated to be 90 percent more than a year ago and primarily driven by significant increases in soybean exports. The recent election in Argentina also could be an important event for agriculture, as the elimination of export restrictions could lead to substantial increases in crop exports from Argentina in the coming years.

Outlook for the Ag Economy

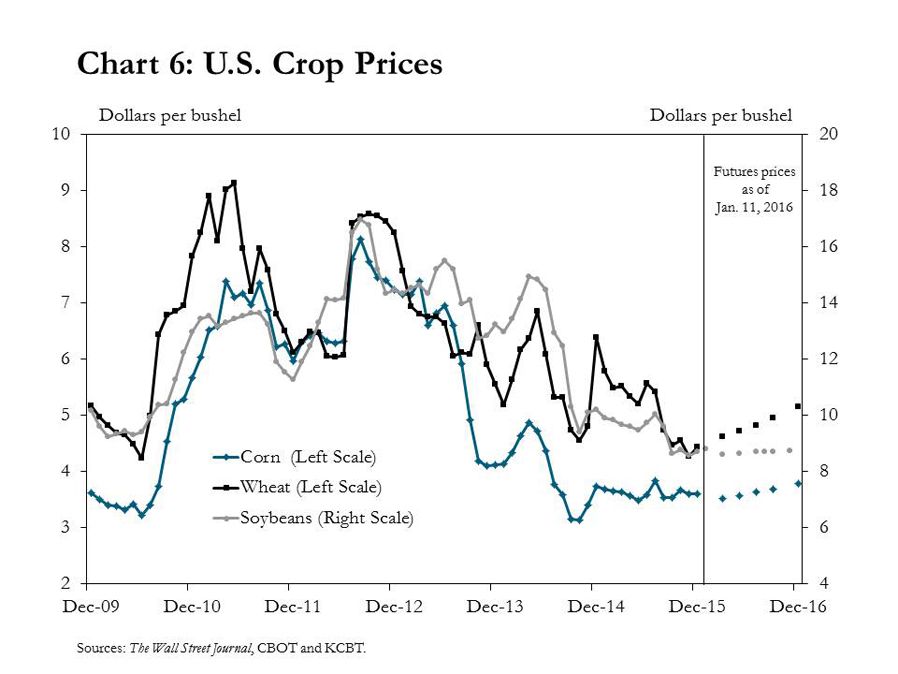

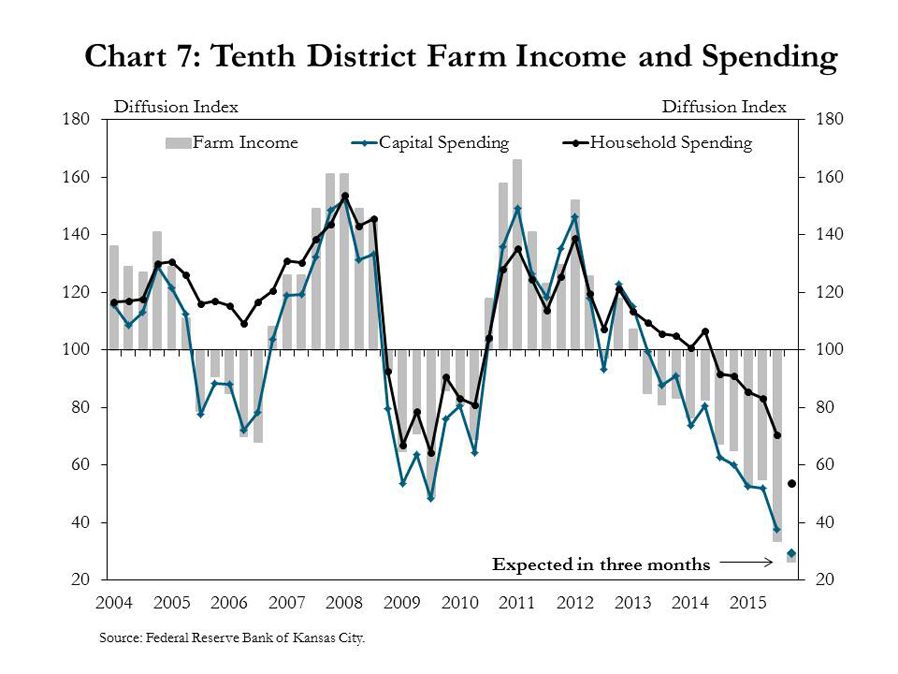

The supply and demand outlook continues to point to generally pessimistic prospects for the farm economy. Headwinds from a strong dollar, booming production and weak demand have put downward pressure on U.S. crop prices, and depressed crop prices have continued to weigh on farm income in the Tenth District (Chart 6). Compared to the same period a year ago, farm income and capital spending declined for the 10th consecutive quarter and potentially have been exacerbated more by recent weakness in the livestock sector (Chart 7). In fact, in the third quarter of 2015, farm income showed a decline in every District state for the first time since 2011.

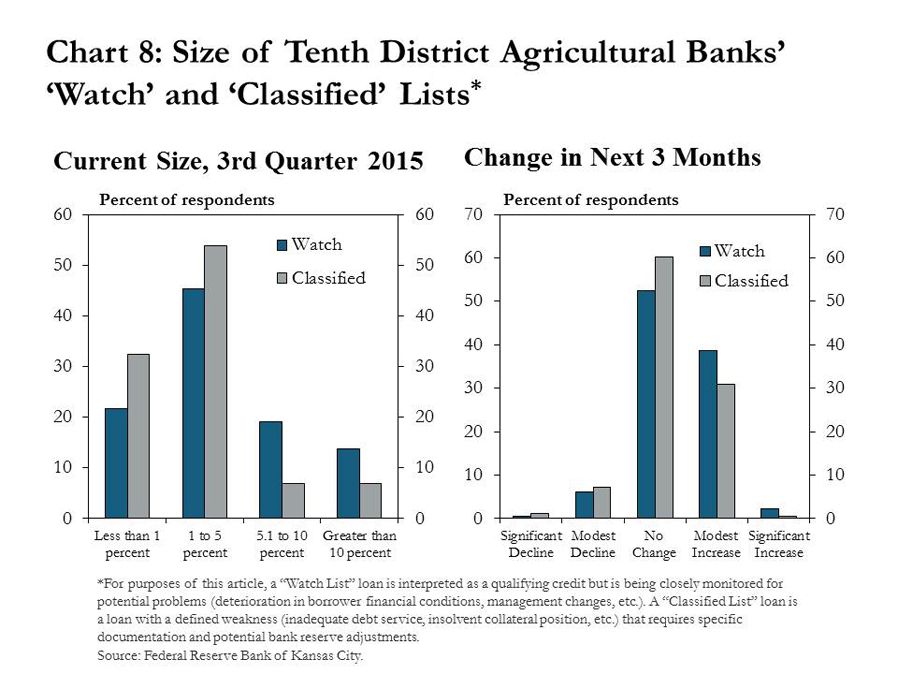

Lower farm income has also steadily affected spending in the farm sector. In general, farmers have adjusted capital spending in line with declines in farm income. However, household spending has been slower to adjust. As a result, several survey contacts have indicated customers should reduce household spending to avoid further deterioration in credit conditions and that their watch and classified lists could expand slightly over the next three months (Chart 8).

Conclusion

With the 2015 harvest completed, accompanied by reports of record production, U.S. crop inventories could continue to grow in 2016. The strong dollar has limited demand for U.S. exports, and flat domestic consumption has contributed to growing U.S. inventories. These fundamentals continue to point to further tightening in the agricultural economy, both in the Tenth District and nationally, as lenders also have voiced increasing concerns about 2016 farm finances.