COVID-19 Updates & Key Demand Drivers for Agriculture

U.S. Ag Policy

June 22, 2020

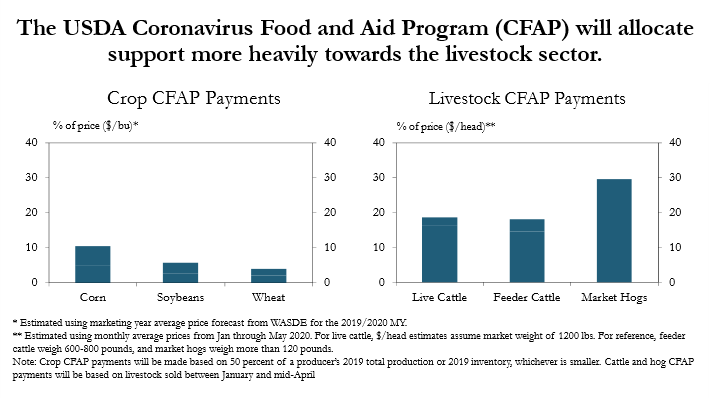

The USDA announced details of the Coronavirus Food and Aid Program (CFAP) in May and allocation of support is expected to be more heavily directed towards the livestock sector. Assistance was made available to producers of agricultural commodities with a price decline of at least 5 percent due to the pandemic and those facing increased marketing costs for inventories resulting from unexpected surplus and disrupted markets. On average, corn, soybean, and wheat farmers are expected to receive payments equal to about 5 to 10 percent of market price on half of 2019 production, or 2 to 5 percent of support on their entire crop. Aid for livestock producers, however, is expected to be comparably higher. Payments to cattle producers could amount to 20 percent of the average price received for cattle, while support for hog producers could be as high 30 percent.

U.S. Ag Exports

June 22, 2020

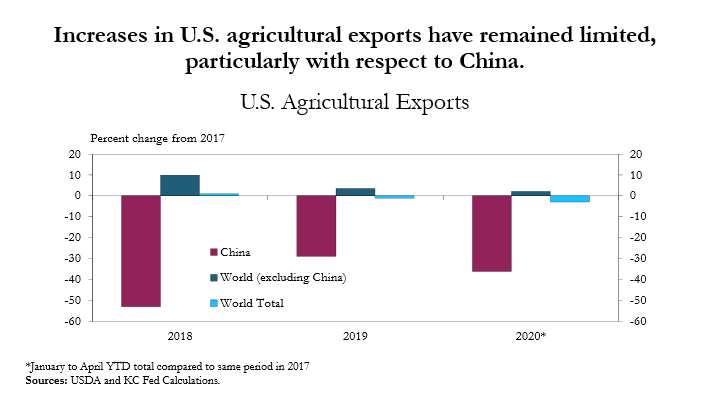

Amid the global economic contraction, increases in U.S. agricultural exports have been limited, particularly with respect to China. Growth in trade with China, a key source of demand for many major U.S. agricultural commodities, remained subdued through April. Exports to China increased about 18 percent from the same period a year ago, but remained well below levels reached during this time in 2017. Exports to all other destinations remained slightly higher than 2017, but the increase was not enough to offset the reduction in exports to China.

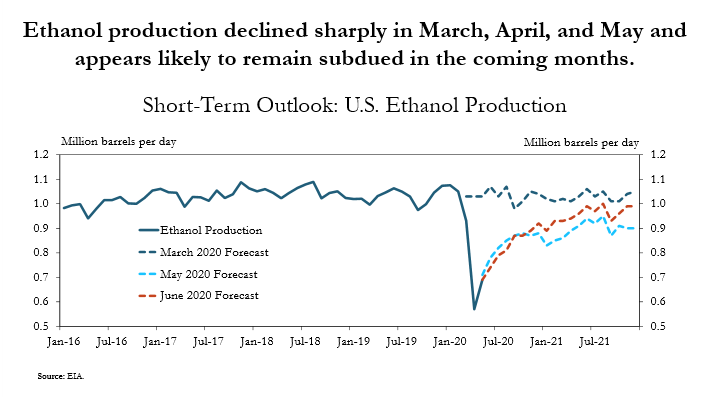

U.S. Ethanol Production

U.S. Meat Production

June 22, 2020

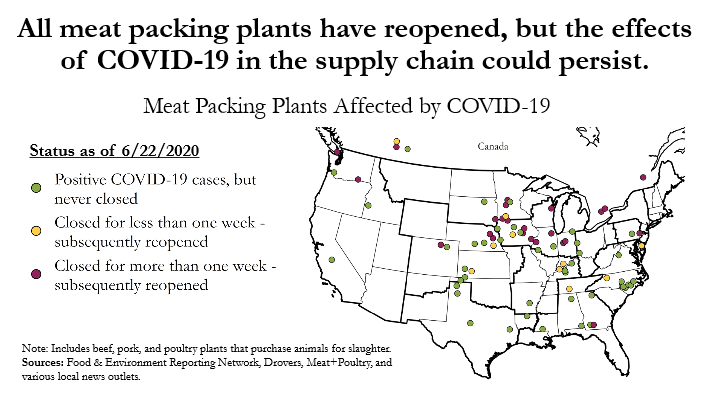

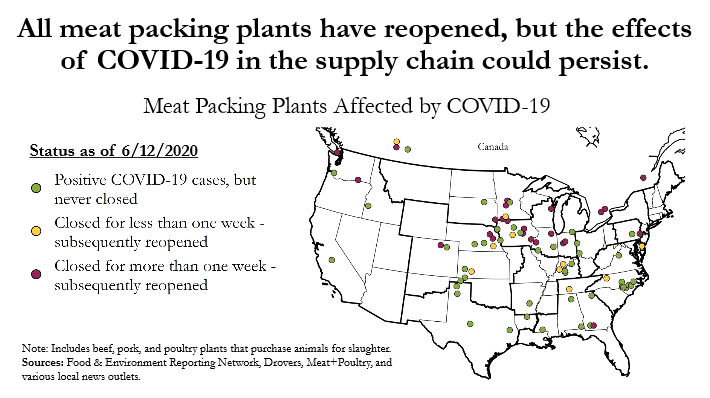

All previously idle meat packing plants have reopened, but effects of COVID-19 continued to impede supply chain functions. The first outbreak of COVID-19 in the meat packing industry occurred on March 31, 2020, at a beef packing plant in Pennsylvania. Since then, almost half of plants that reported an outbreak closed for some period of time. In fact, most facilities that did close were shut down for more than one week. As of June 22, 2020, all beef, pork, and poultry packing plants that had closed due to COVID-19 were reopened and operating. However, the magnitude and duration of closures and ongoing concerns about the spread of the virus has raised questions about implications for meat production and the supply chain moving forward.

June 22, 2020

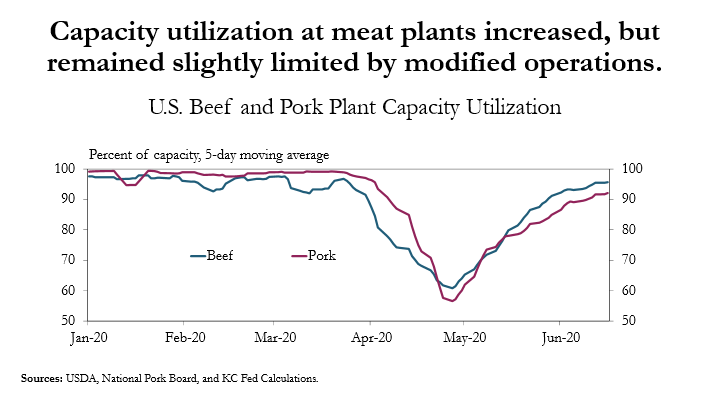

Capacity utilization at meat packing plants increased slightly since early May, but appeared to remain slightly limited by modified operations. After declining sharply alongside closures, the percent of total capacity being used at U.S. beef and pork plants expanded as facilities reopened. Despite fewer plant closures, modified operations related to social distancing and other precautionary measures have continued to impact overall production capabilities. Through the third week of June, beef and pork plants were utilizing about 95 percent and 92 of pre-pandemic capacity, respectively.

June 22, 2020

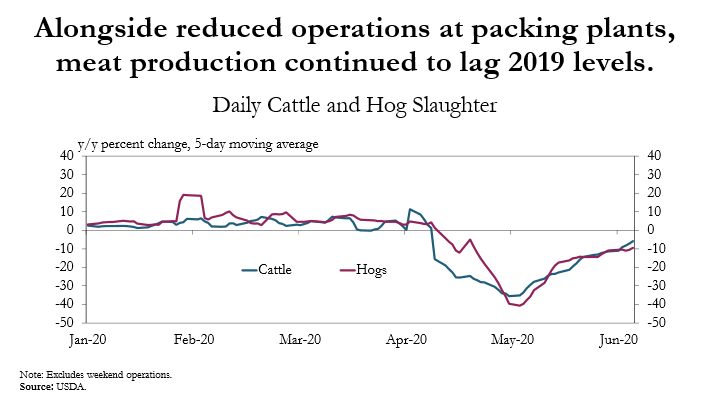

Alongside reduced operational capacity at packing plants, meat production continued to lag 2019 levels. As packing plants reopened, daily slaughter of cattle and hogs increased from lows reached in early May. However, both beef and pork production remained more than 5 percent lower than a year ago during the first week in June. It appeared that modified operations and revised processes related to COVID-19 have continued to put some constraints on production, even as plants have resumed operations.

June 12, 2020

All previously idle meat packing plants have reopened, but effects of COVID-19 continued to impede supply chain functions. The first outbreak of COVID-19 in the meat packing industry occurred on March 31, 2020, at a beef packing plant in Pennsylvania. Since then, almost half of plants that reported an outbreak closed for some period of time. In fact, most facilities that did close were shut down for more than one week. As of June 12, 2020, all beef, pork, and poultry packing plants that had closed due to COVID-19 were reopened and operating. However, the magnitude and duration of the closures has raised questions about the implications for meat production and the supply chain moving forward.