Agricultural credit conditions in the Tenth District of the Federal Reserve continued to weaken in the second quarter of 2015, but despite that weakening most bankers reported few significant problems with loan repayment. Bankers also reported that a weakening agricultural economy has further boosted loan demand, lowered cropland values and generally slowed Main Street business activity in the District’s agricultural regions. Demand for non-real estate farm loans increased in every state, but only a small percentage of operating loan applications was denied. Lower crop prices continued to put downward pressure on cropland values, especially nonirrigated cropland values, which fell significantly from the previous quarter. Ranchland values, however, continued to increase, supported by strong profit margins in the cow-calf sector.

Farm Loan Demand and Credit Conditions

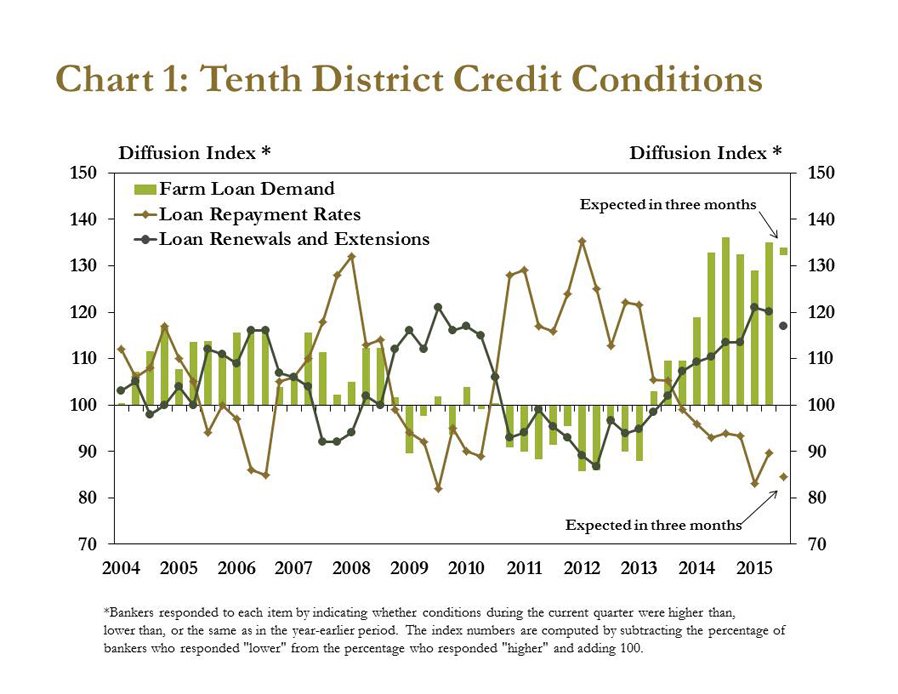

Loan demand continued to grow in the second quarter, and credit conditions weakened slightly, according to respondents in the Tenth District Survey of Agricultural Credit Conditions. Loan repayment rates continued to decline, and loan renewals, referrals and extensions increased modestly from the previous year (Chart 1). Although bankers overall reported further declines in loan repayment rates, 75 percent of respondents reported repayment rates were unchanged from a year ago. Furthermore, the number of bankers reporting lower loan repayment rates than in the last quarter declined 8 percent.

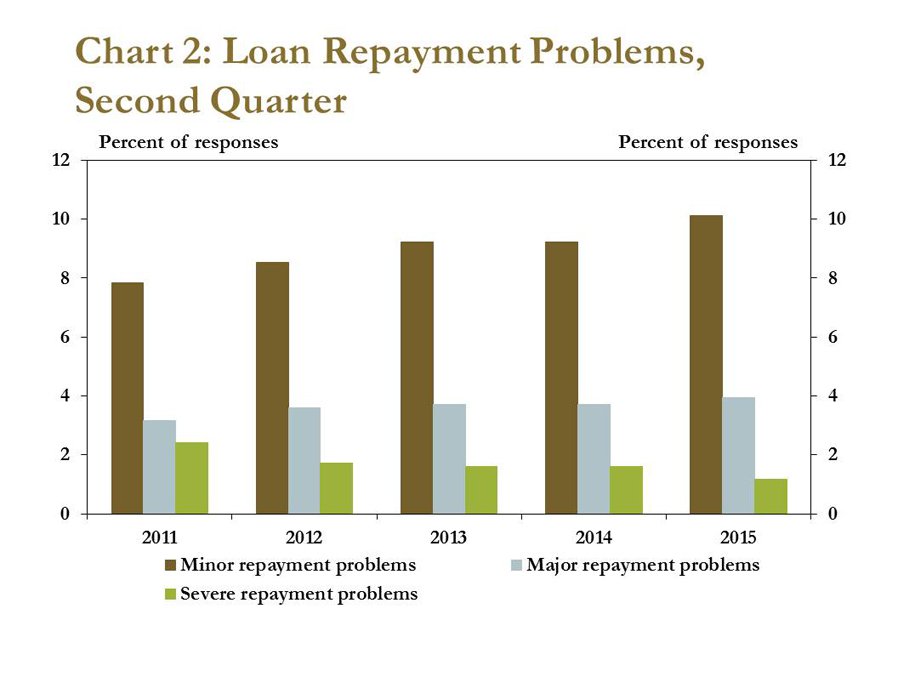

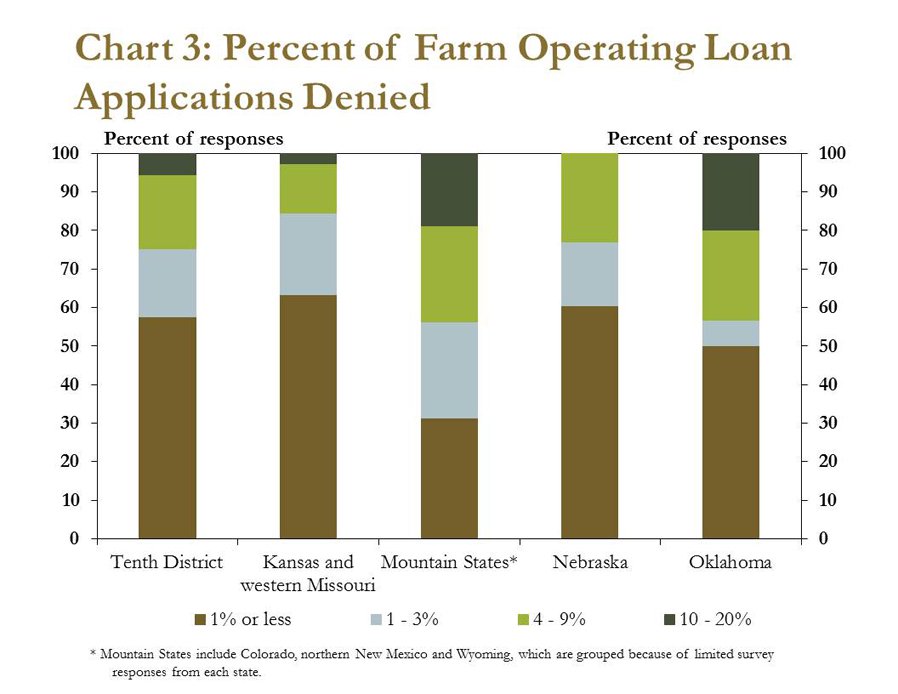

Although repayment rates declined in most of the District, the deterioration over the past year has been relatively minor. Bankers reported only slight increases in minor repayment problems compared to last year (Chart 2). In addition, bankers reported that few operating loan applications were denied, and most of the denied applications were for new rather than existing customers (Chart 3). The survey index for availability of funds remained steady, and only 1 percent of banks reported that loans were reduced or refused due to fund shortages.

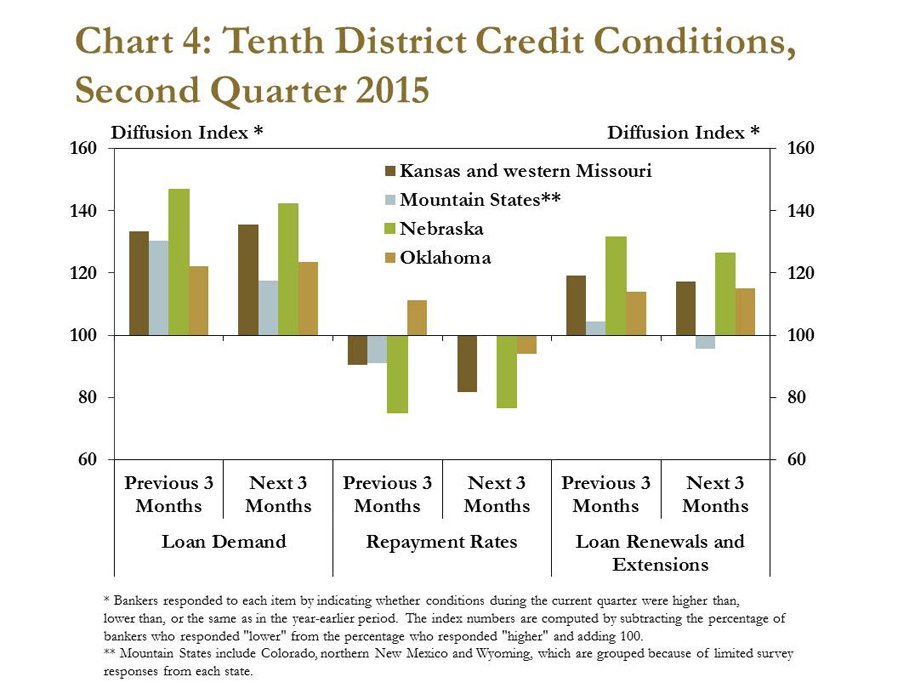

Survey measures for loan repayment, renewals and extensions varied slightly across the District, but demand for loans was consistently higher in all states. Specifically, low crop prices and variable weather conditions led to a more pessimistic outlook in crop-producing states. Compared with other states, more bankers in Nebraska reported lower repayment rates and more loan renewals and extensions (Chart 4). Similarly, 30 percent of bankers in Kansas and western Missouri indicated they expect loan repayment rates to be lower in the next three months compared to the same period last year. In contrast, bankers in Oklahoma reported slightly higher loan repayment rates from a year ago, and loan renewals and extensions in the Mountain States were expected to decline over the next three months.

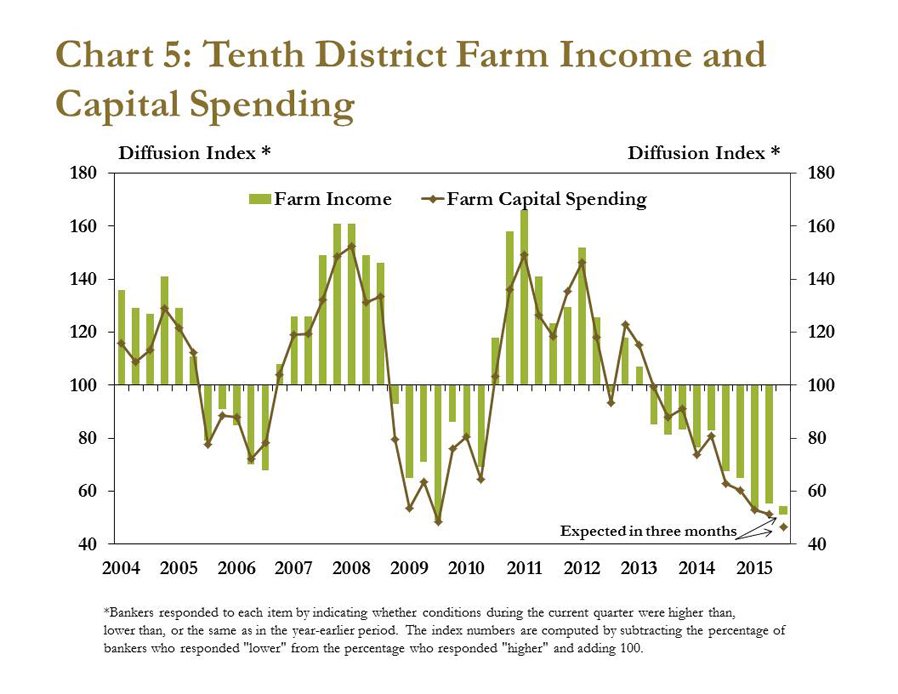

Farm Income

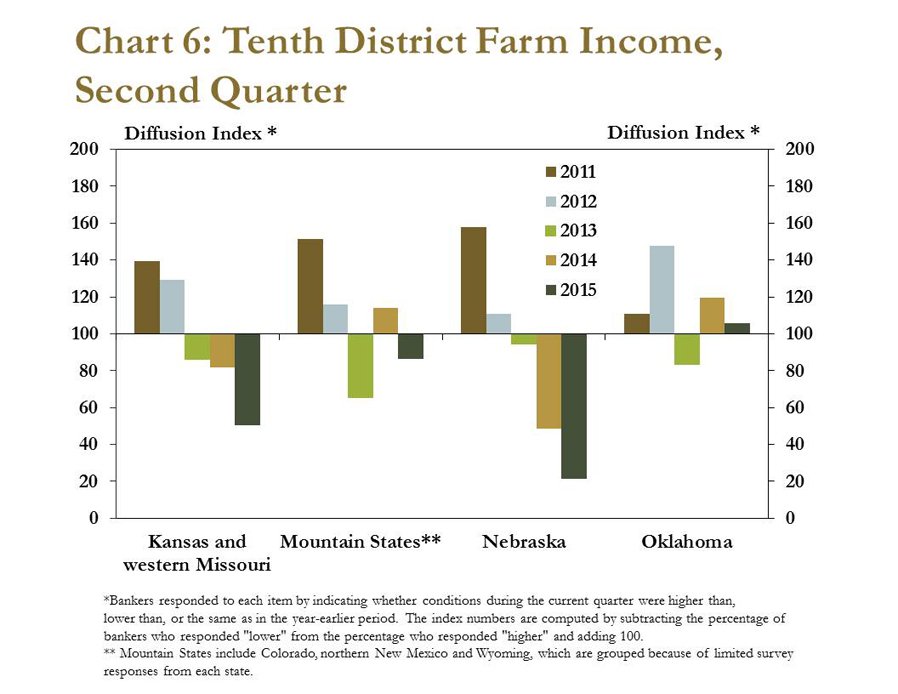

Expectations of increasing loan demand and weakening repayment rates were likely due to continued declines in farm income. More than half of survey respondents reported lower farm income in the second quarter compared to last year, marking the ninth consecutive quarterly decline (Chart 5). Regionally, farm income declined in every state but Oklahoma, where incomes continued to be supported by positive profit margins for cow-calf producers (Chart 6). Prospects in Missouri were especially pessimistic, where none of the responding bankers reported higher farm income compared to a year ago. Low crop prices and variable weather patterns also appeared to be holding down expectations for farm income in the next three months.

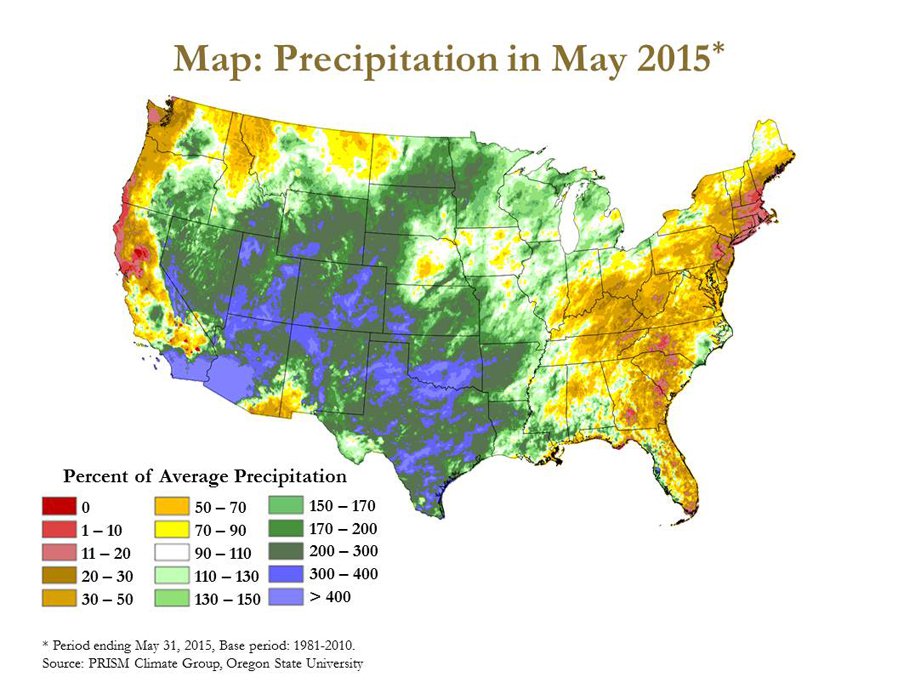

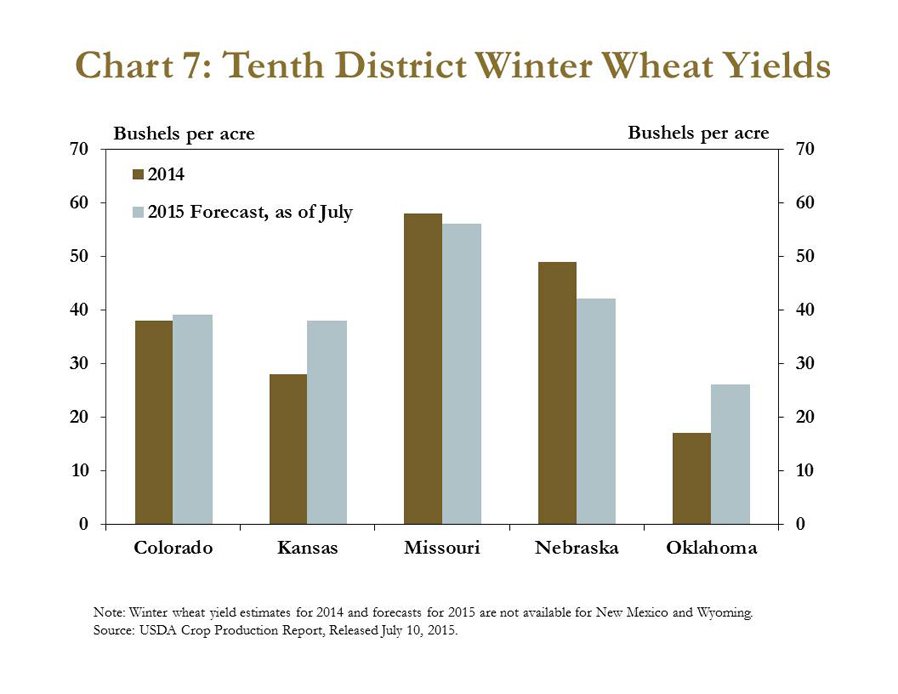

Several survey respondents mentioned the challenges of wet weather conditions and lower crop prices in the midst of steady input costs. A large portion of the Tenth District experienced abnormally heavy precipitation in the second quarter, with some areas receiving rain totals as much as 300 to 400 percent more than the historical average (Map). Bankers in Colorado commented that recent rains filled reservoirs, improved crop yield potential and increased optimism (despite low crop prices). However, bankers throughout Kansas, Missouri and Nebraska commented that too much rain had resulted in wheat rust, delayed the wheat harvest, prevented planting of soybeans and limited opportunities to cut and bale hay. The heavy spring rains, however, had varying effects on winter wheat yields in the District. Compared to last year, wheat yields in Oklahoma and Kansas were expected to improve dramatically, while yields in Nebraska were forecast to decline (Chart 7).

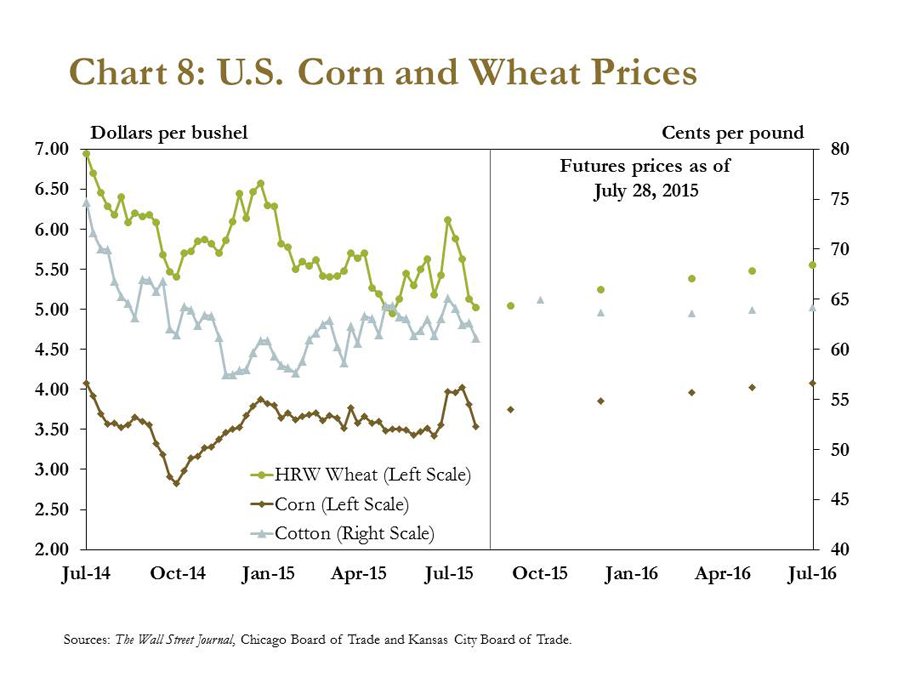

Abnormal weather and yield variability generated some uncertainty in agricultural commodity markets in the second quarter, and recent prices have been volatile. In early May, for example, wheat prices were near annual lows, and corn prices were trending downward. Then, after spiking in the last week of June due to expectations of reduced crop yields, corn prices again declined significantly as crop conditions evolved further during key summer growing months (Chart 8).

Not all commodities produced in the Tenth District, however, have experienced increased price volatility. For example, cotton prices remained relatively steady in the second quarter, partly due to the significance of global developments in that market. Although reduced demand from China, increased production in India, Brazil and Bangladesh, and improving conditions for the 2015 U.S. cotton crop could put downward pressure on cotton prices, upward price pressures could offset these effects. For example, U.S. cotton production was still expected to be 11 percent less than 2014 levels due to decreased planted area.

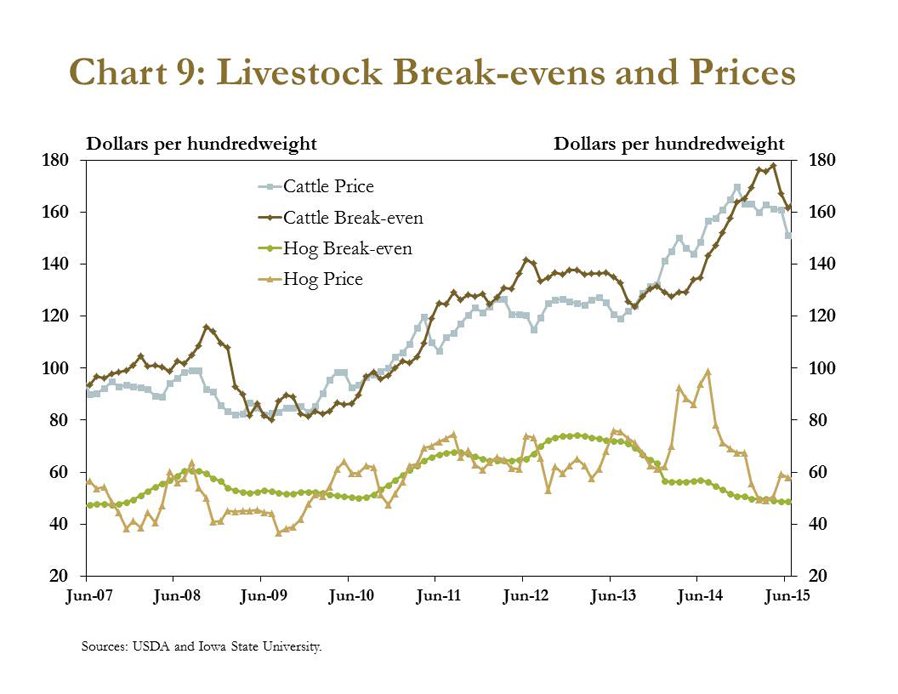

Although crop prices generally have remained depressed relative to recent years, feeder cattle prices have remained historically high. High prices for feeder cattle, combined with increases in cow-calf returns and improved forage and pasture conditions, have encouraged cow-calf producers to rebuild their herds. Some bankers commented that cow-calf producers had continued to maintain solid profit margins, supporting farm income in their areas. For feedlot operators, however, the break-even cost for cattle surpassed cattle prices at the beginning of 2015, and profit margins have been negative since January (Chart 9). Hog prices rebounded slightly in May, but looking forward, increasing feed costs were expected to dampen producers’ profit margins.

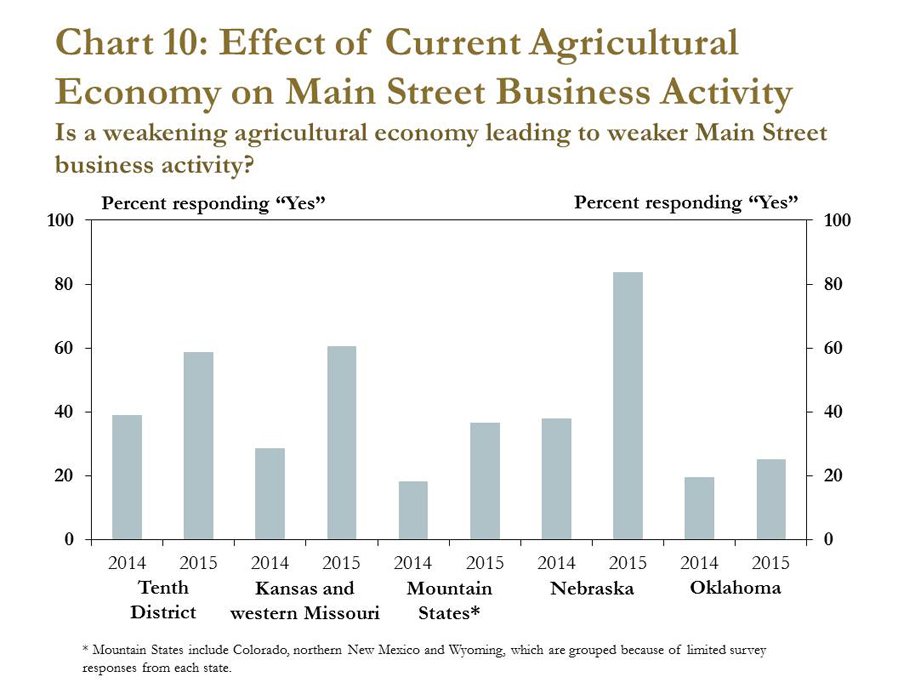

Persistently lower crop prices and emerging stress in the farm economy have affected the overall economic outlook on Main Street. In evaluating the relationship between the local agricultural economy and general business activity, many Tenth District bankers reported that a weakening agricultural economy had weakened Main Street business activity in their lending areas (Chart 10). In 2014, 39 percent of bankers reported weaker business activity as the agricultural economy began to soften, but that number increased to 59 percent in 2015. The largest evidence of weakening occurred in Nebraska, where 84 percent of survey respondents reported that a weakening agricultural economy was adversely affecting Main Street, up from 38 percent in 2014. In contrast, regions not as dependent on crop production as Nebraska, such as Oklahoma and the Mountain States, were less pessimistic about the connection between the agricultural economy and Main Street.

Farmland Values

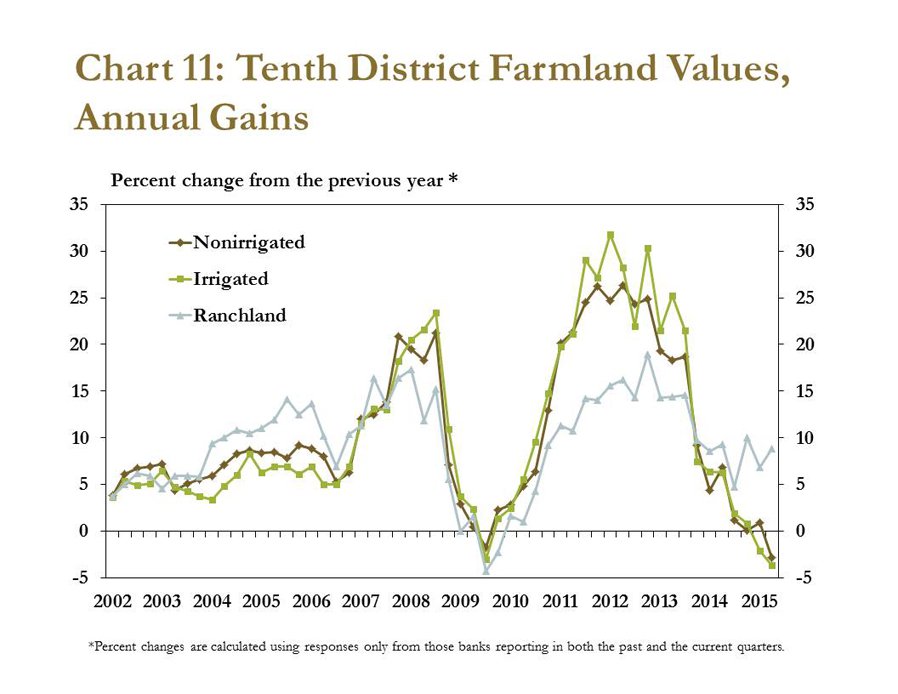

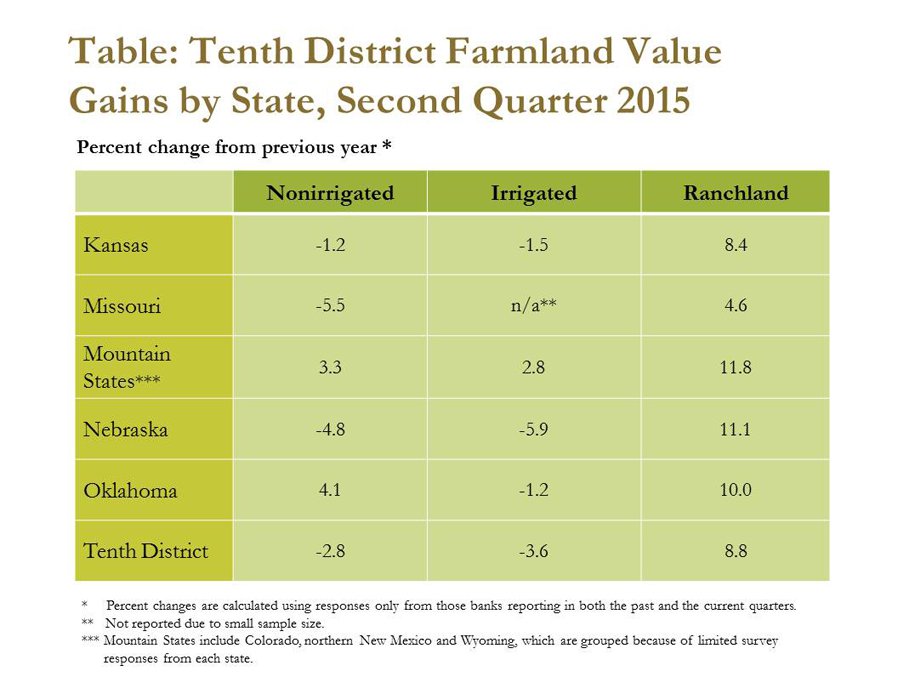

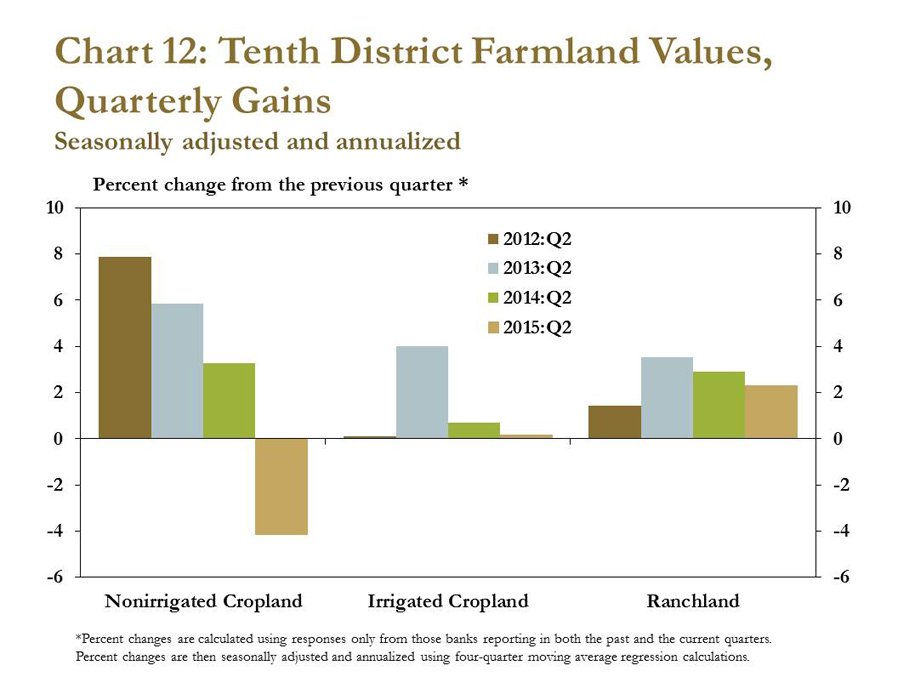

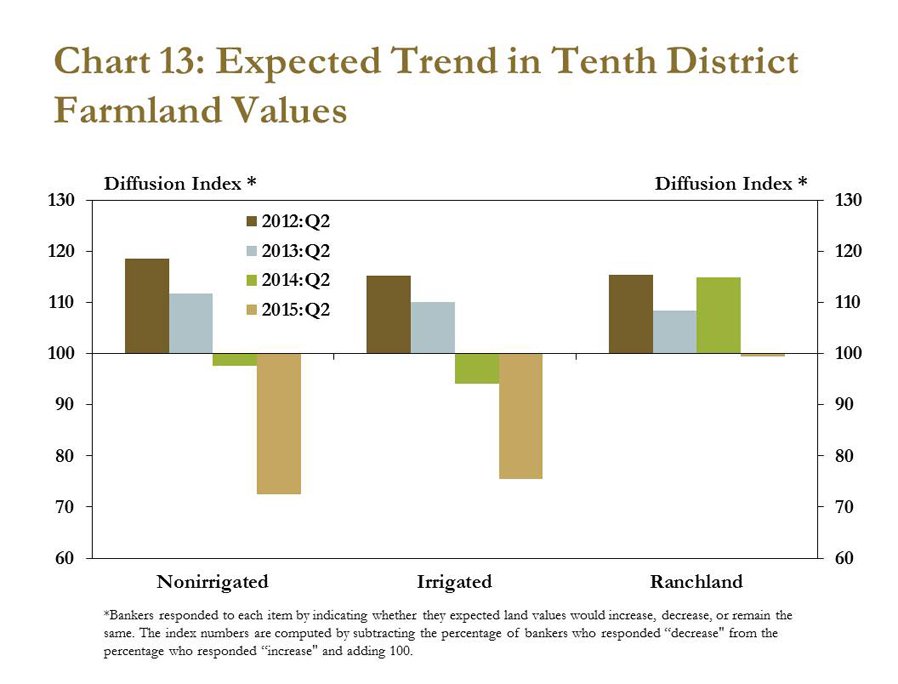

Amid lower farm income and expectations that crop prices may not improve significantly, cropland values continued to soften. Nonirrigated cropland values declined almost 3 percent, on average, from last year (Chart 11). The declines were largest in Nebraska and Missouri, while values increased modestly in Oklahoma and the Mountain States (Table). From the first quarter to the second, nonirrigated cropland values declined more than 4 percent (Chart 12). Although irrigated cropland values remained steady on a quarter-over-quarter basis, irrigated cropland values were 3.6 percent lower in the second quarter when compared with the previous year, driven mostly by declines in Nebraska and Kansas. In contrast, ranchland values posted modest gains due to continued profitability in the cow-calf sector. Although bankers expected nonirrigated and irrigated cropland values to decline further, they also expected ranchland values to moderate in the coming months (Chart 13).

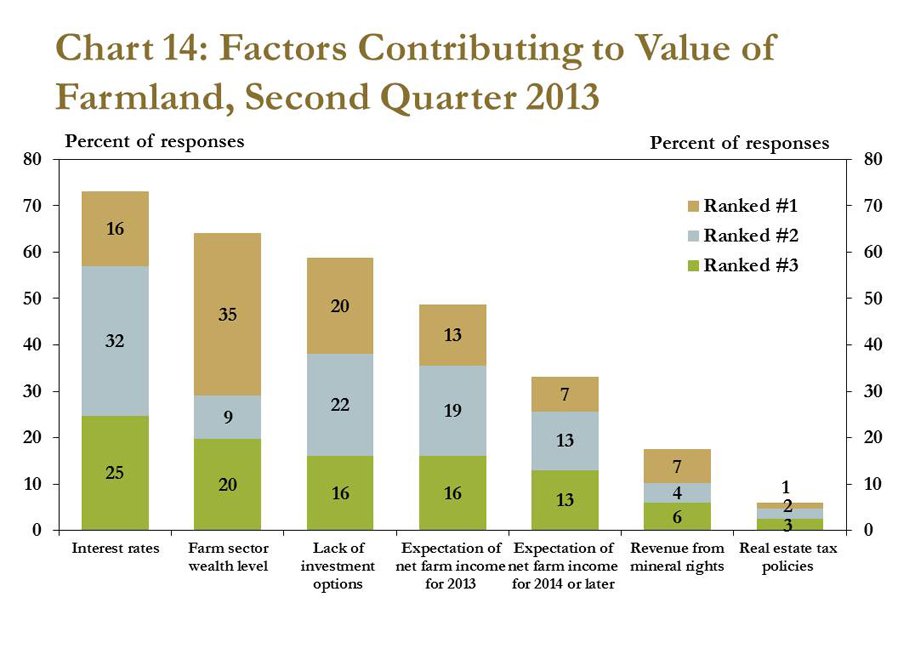

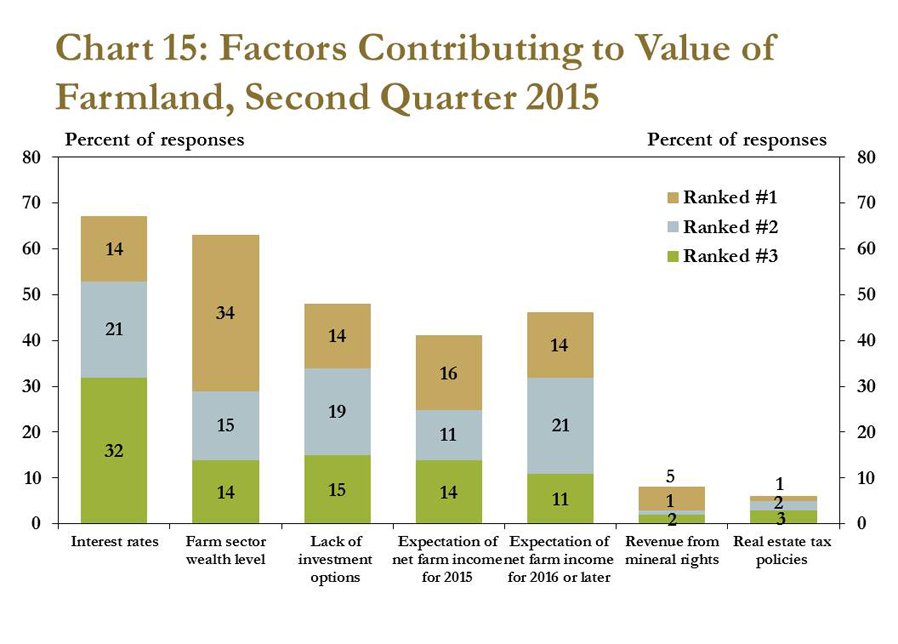

As in 2013, weaker farm income was not the only factor driving farmland values in the second quarter of 2015. Similar to two years ago, District bankers reported the overall wealth of the farm sector, the current interest rate environment and a lack of alternative investment options have had significant effects on farmland values (Chart 14). However, unlike two years ago, more agricultural lenders cited farm income expectations for next year as a primary contributor to recent developments in farmland values (Chart 15). With the recent downturn in oil prices, land-lease revenue from mineral rights was identified as less important than in 2013.

Conclusion

Agricultural credit conditions were expected to weaken further in coming months alongside subdued farm income and a growing demand for farm loans. In the second quarter, bankers were concerned that potential yield losses, coupled with lower crop prices, could put further pressure on crop producers’ profit margins. Although loan repayment problems were reported to be only minor thus far, and few loan applications were denied, weaker cash flow could continue to intensify financial stress for some producers as the fall harvest approaches.

The views expressed in this article are those of the authors and do not necessarily reflect the views of the Federal Reserve Bank of Kansas City or the Federal Reserve System.

Authors

Nate Kauffman

Senior Vice President, Economist, and Omaha Branch Executive; Executive Director of the Center for Agriculture and the Economy