The farm economy in the Tenth District weakened in the first quarter of 2017, but conditions varied from east to west. Farm income, loan repayment rates and the value of most types of farmland all trended lower in each of the District’s seven states. However, the deterioration in the western portion of the District was more severe than the moderate weakness in the eastern portion. Although agricultural credit conditions were weaker throughout the region, much of the recent weakness has been driven by intensifying challenges in the western portion of the District.

Farm Income

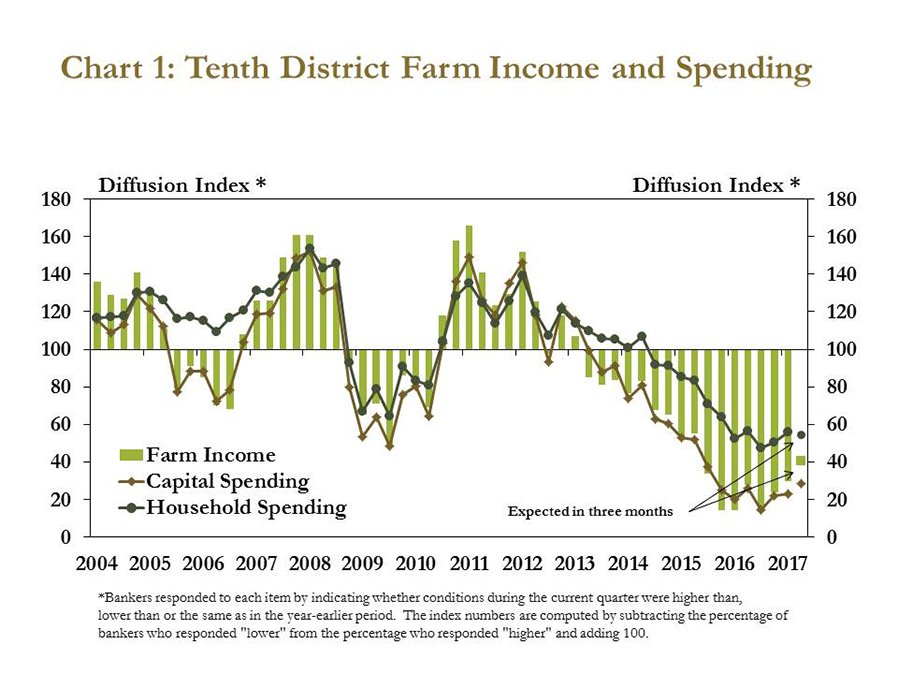

Farm income in the Tenth District continued to decline in the first quarter, but at a slightly slower pace than in recent quarters. According to the survey, 73 percent of bankers reported farm income was lower than the year before. The decline in the first quarter marked the fourth consecutive year that District bankers reported farm income was lower than a year earlier (Chart 1). Despite the persistent decline, the pace of softening appeared to slow in the first quarter. For example, 24 percent of bankers indicated farm income remained unchanged from the previous year, the largest share since the third quarter of 2015. Bankers expected farm income to decline further in the coming months, but also at a slower pace than in recent quarters.

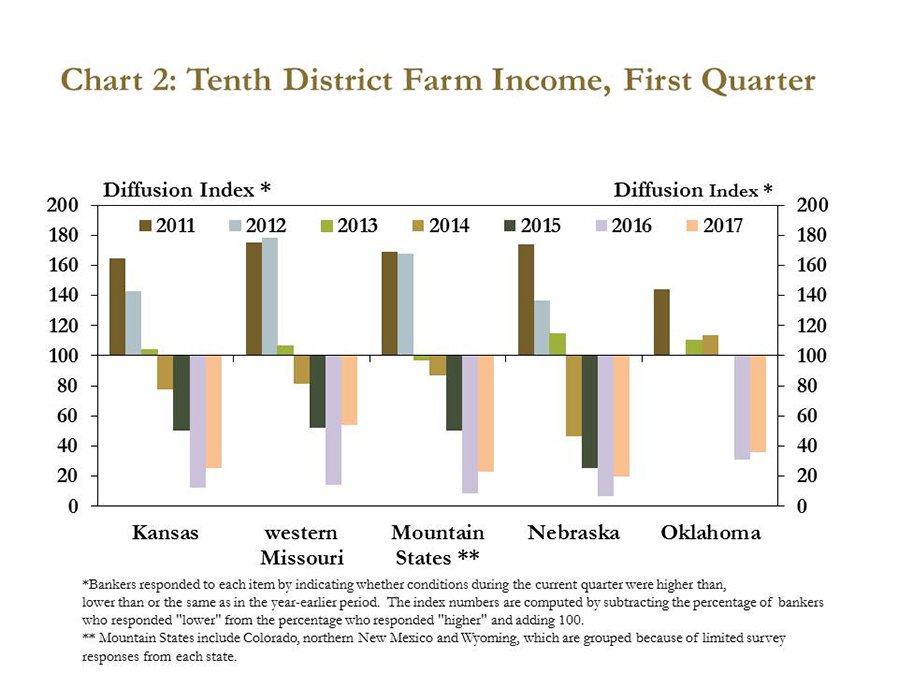

Similar to a year ago, bankers indicated that farm income had declined in each state in the Tenth District. Despite a recent rebound in cattle prices, a prolonged downturn in cattle and wheat markets caused bankers in regions with a strong concentration in those markets to express concerns about the local farm economy. In particular, farm income remained subdued in Kansas and the Mountain States, regions with relatively more cattle and wheat production (Chart 2). Although farm income continued to decline in western Missouri, bankers were slightly more optimistic in their assessment for farm income in that region, where crop yields were particularly strong last fall.

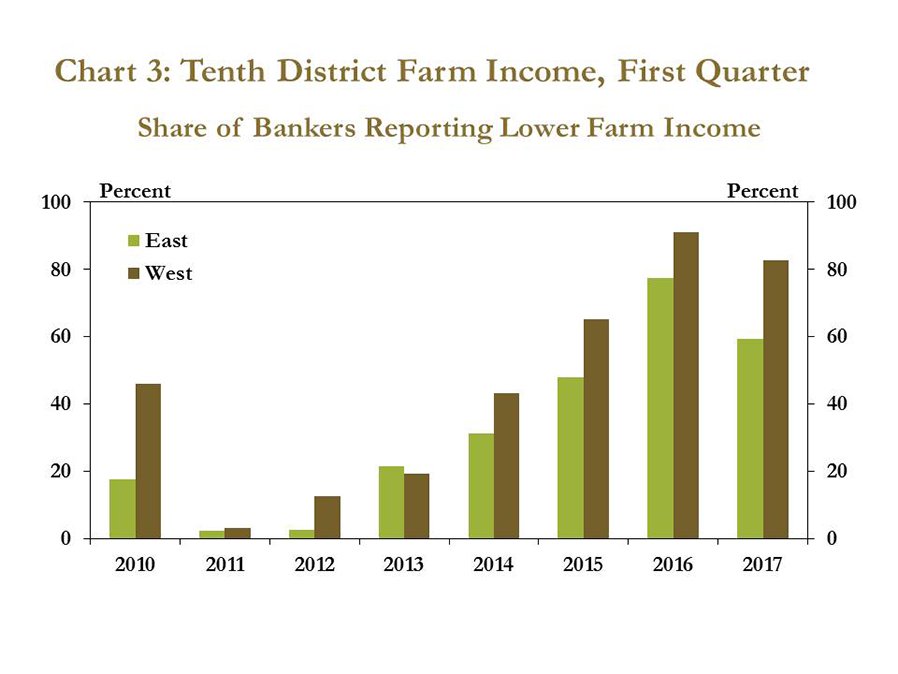

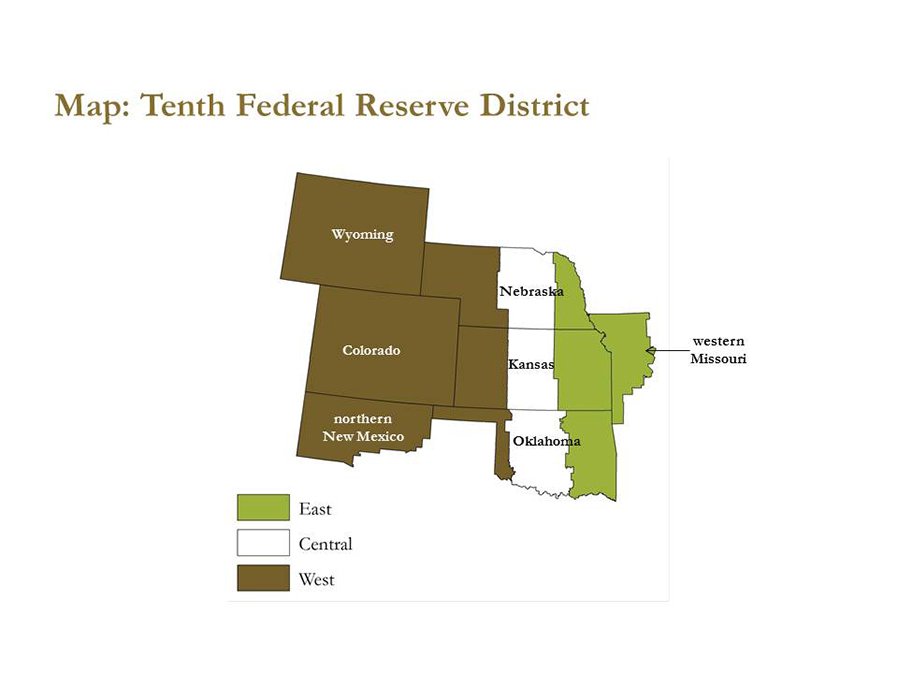

More generally, farm income has declined at a stronger pace in the western part of the District. Since 2014, following a drop in the prices of major row crops, farm income has fallen more sharply in the Mountain States and the western portions of Nebraska, Kansas and Oklahoma (Chart 3 and Map). According to the survey, the gap in the performance of the farm sector between the District’s eastern and western portions widened in the first quarter. Alongside persistent weakness in cattle and wheat markets, more than 80 percent of bankers indicated farm income was lower than a year ago in the western part of the District versus about 60 percent in the eastern part.

Credit Conditions and Lending

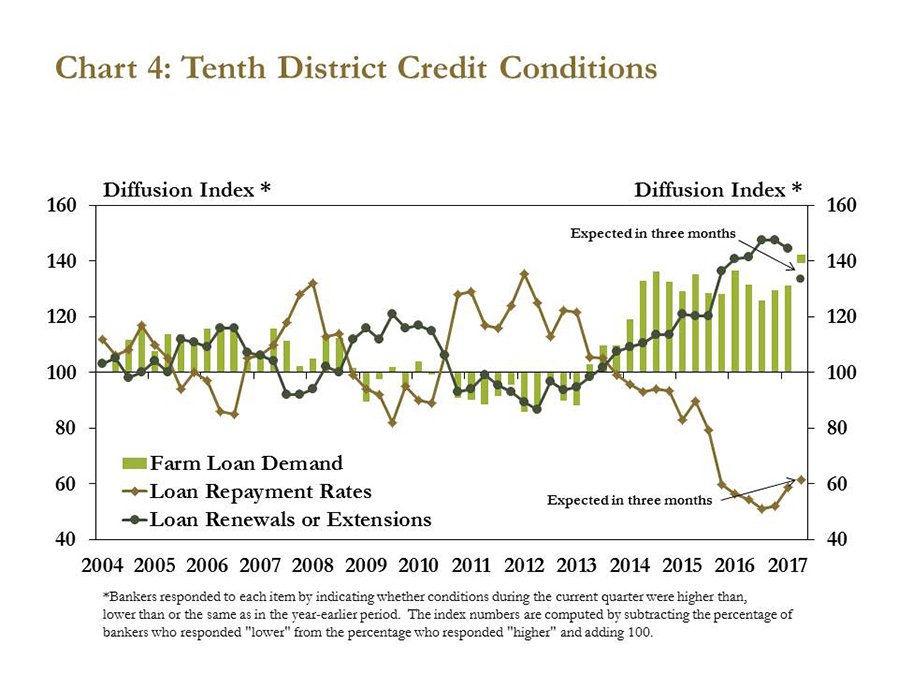

A prolonged downturn in the farm economy continued to weigh on agricultural credit conditions in the District, but also at a softer pace than in recent quarters. Loan demand remained high in the first quarter and was expected to continue to rise in the coming months (Chart 4). Bankers also reported farm loan repayment rates continued to weaken, but not as sharply as in 2016. In fact, similar to farm income, 49 percent of bankers indicated loan repayment rates were unchanged from a year ago, a larger share than the previous two quarters.

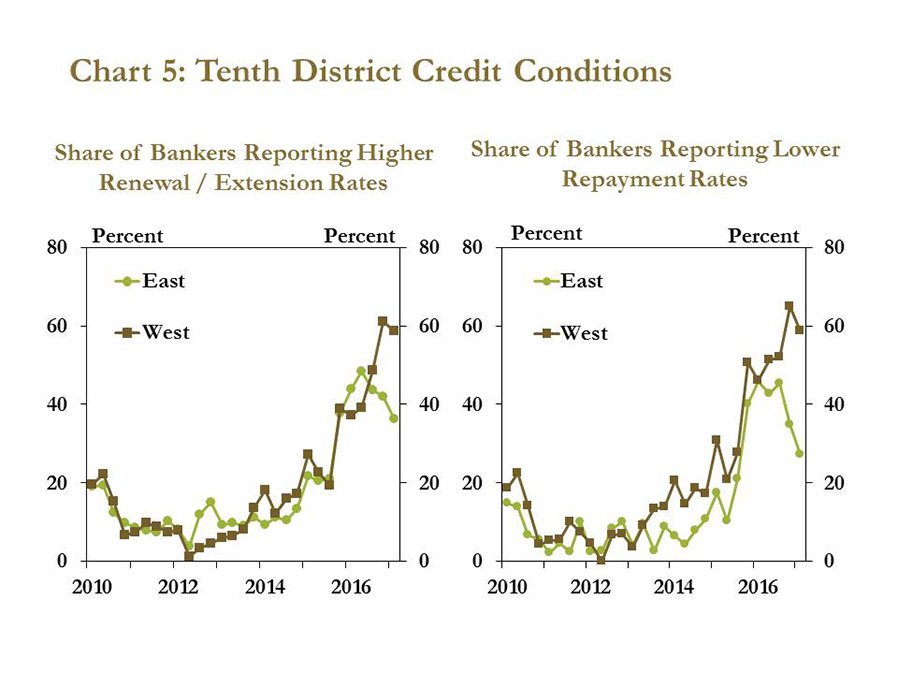

Despite some signs of optimism in the eastern portion of the District, agricultural credit conditions worsened more significantly in the west. Over the past several years, the share of bankers reporting higher rates of loan renewals and lower repayment rates had been similar throughout the Tenth District (Chart 5). Since mid-2016, however, the rate of deterioration in these two metrics has increased in the west, but generally has softened in the east, reflecting an emerging regional divide in agricultural finance conditions. Whereas bankers throughout the District have expressed ongoing concerns about the state of the farm economy, concerns from bankers further west have been elevated and were reflected in the recent survey data.

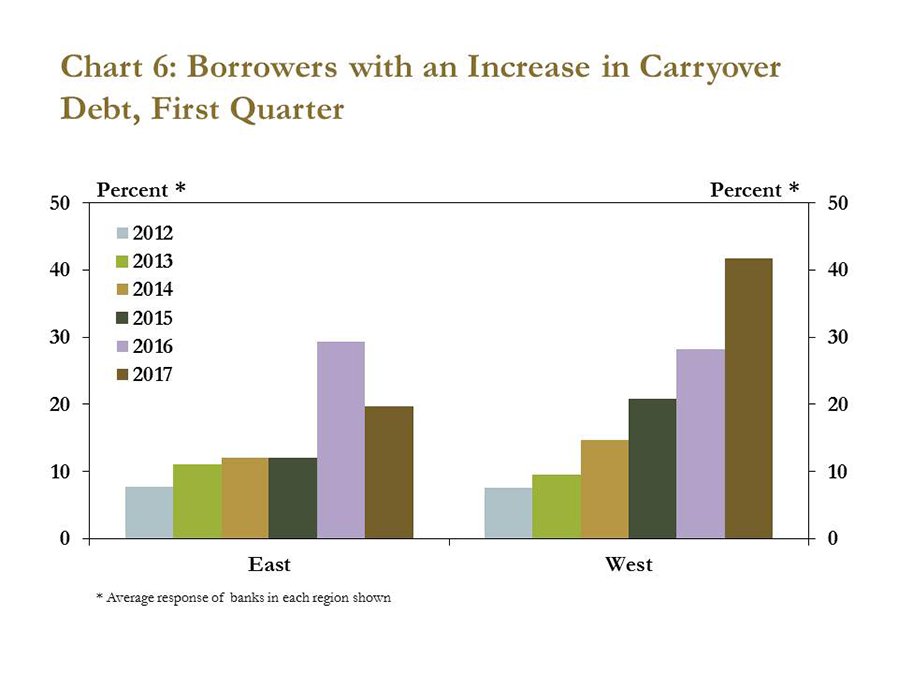

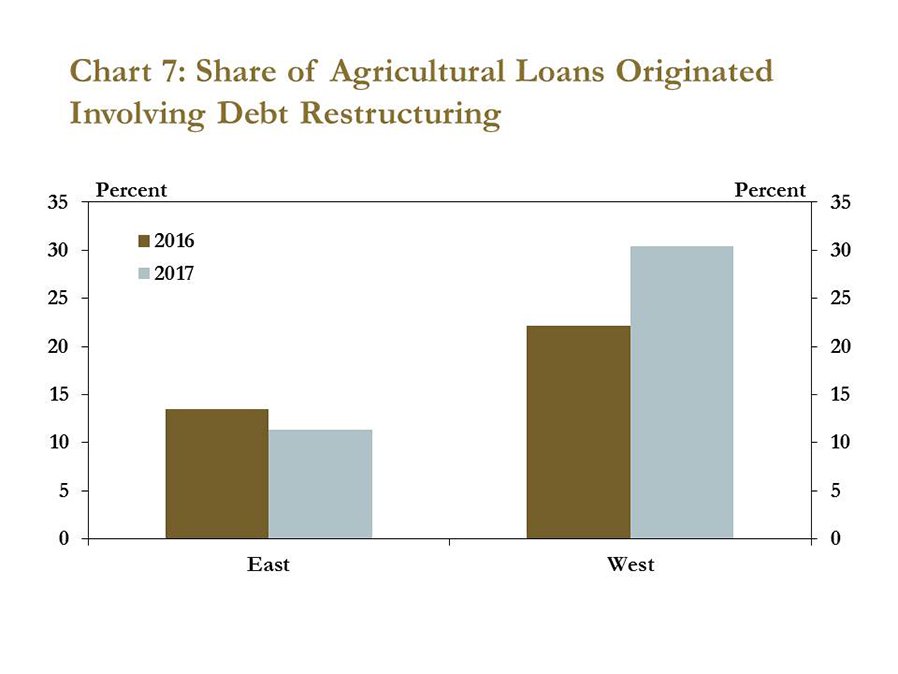

The pace of carry-over debt also quickened in the western portion of the District, but declined in the east. In 2016, about 29 percent of farm borrowers carried over more debt from the previous year (Chart 6). In the first quarter of 2017, however, more than 40 percent of bankers in the west noted that carry-over debt increased, while less than 20 percent in the east reported an increase in borrowers with carry-over debt. In addition, the share of agricultural loans that involved debt restructuring in response to persistent shortages in cash flow increased again in the west, but generally remained stable in the east (Chart 7).

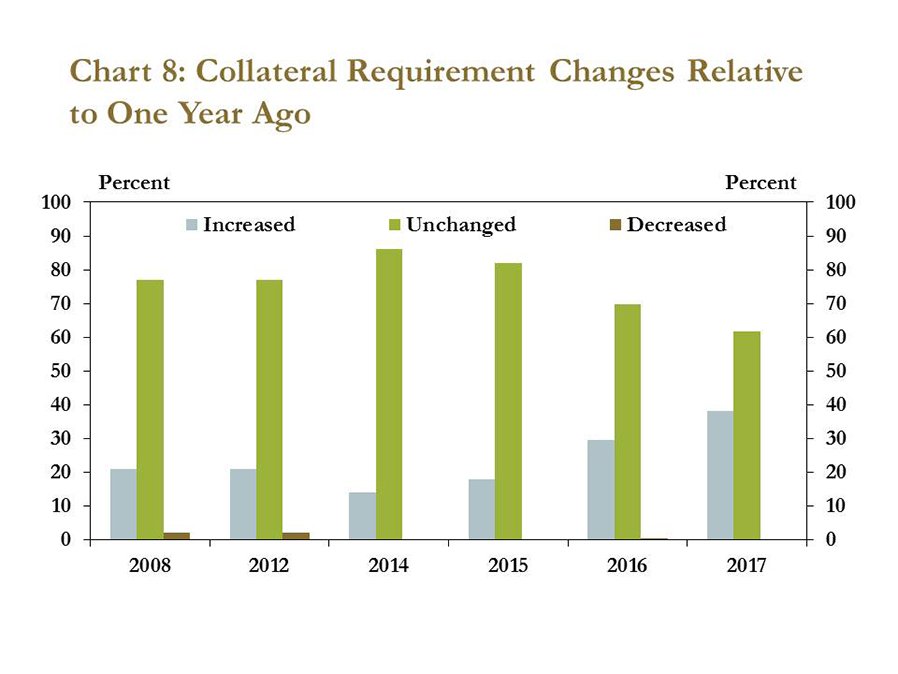

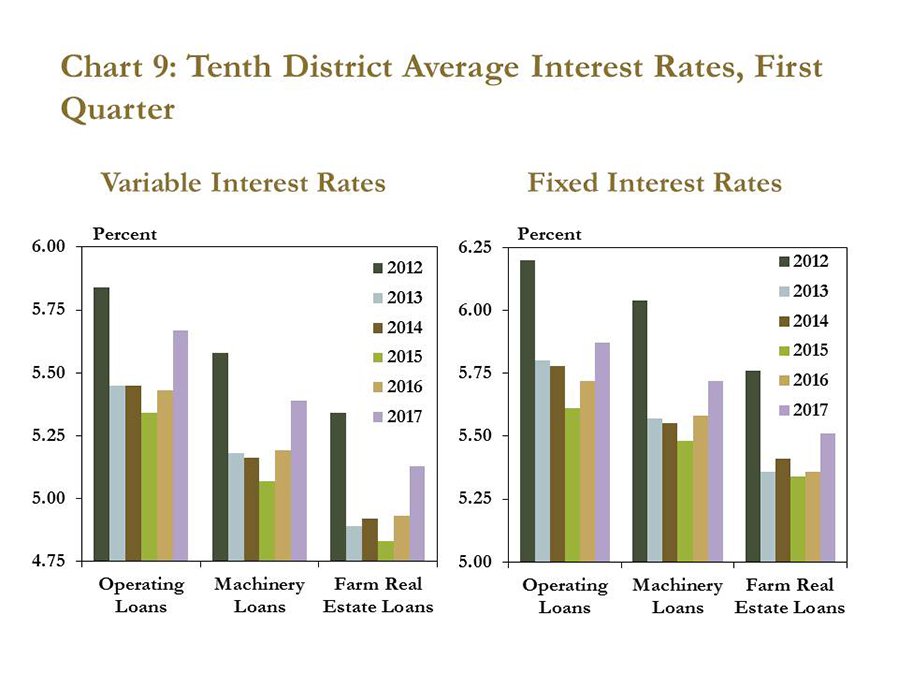

Alongside ongoing difficulties in the District farm economy, bankers continued to raise collateral requirements and interest rates for farm borrowers at a modest pace. In the first quarter, nearly 40 percent of bankers noted that collateral requirements increased from the year before, reflecting a steady increase from recent years (Chart 8). Interest rates remained historically low, but increased 24 basis points, on average, for variable rate operating loans and 15 basis points for fixed rate operating loans from a year ago (Chart 9).

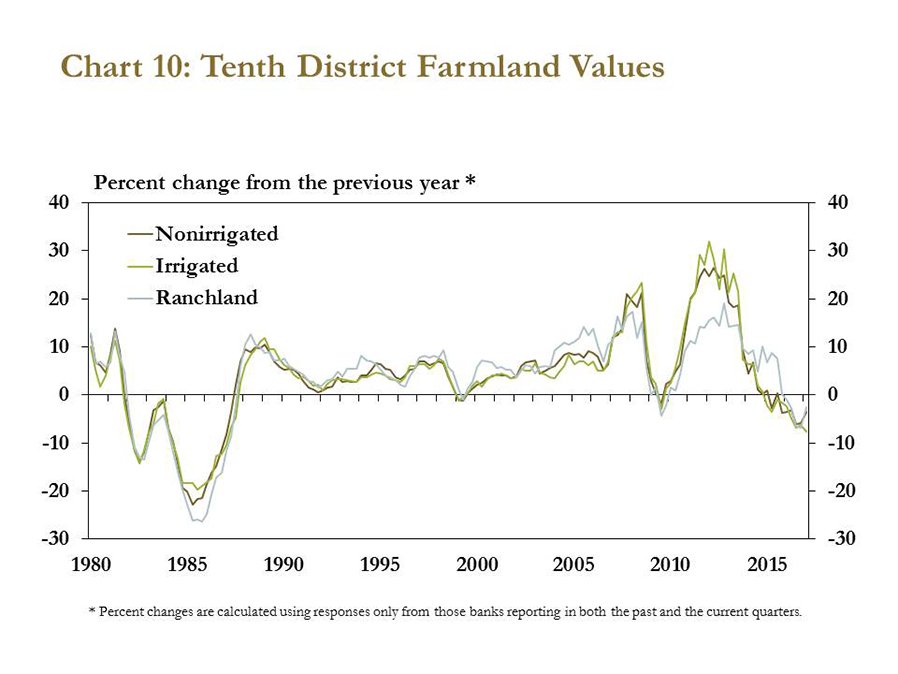

As expected, based on recent surveys, District farmland values trended lower in response to conditions in the regional farm economy. The value of nonirrigated cropland declined 3 percent in the first quarter, following similar declines in 2016 (Chart 10). The value of irrigated cropland and ranchland also decreased in the first quarter. Although farmland values continued to trend lower alongside ongoing weakness in the farm economy, the declines have remained relatively modest in comparison to the crisis of the 1980s.

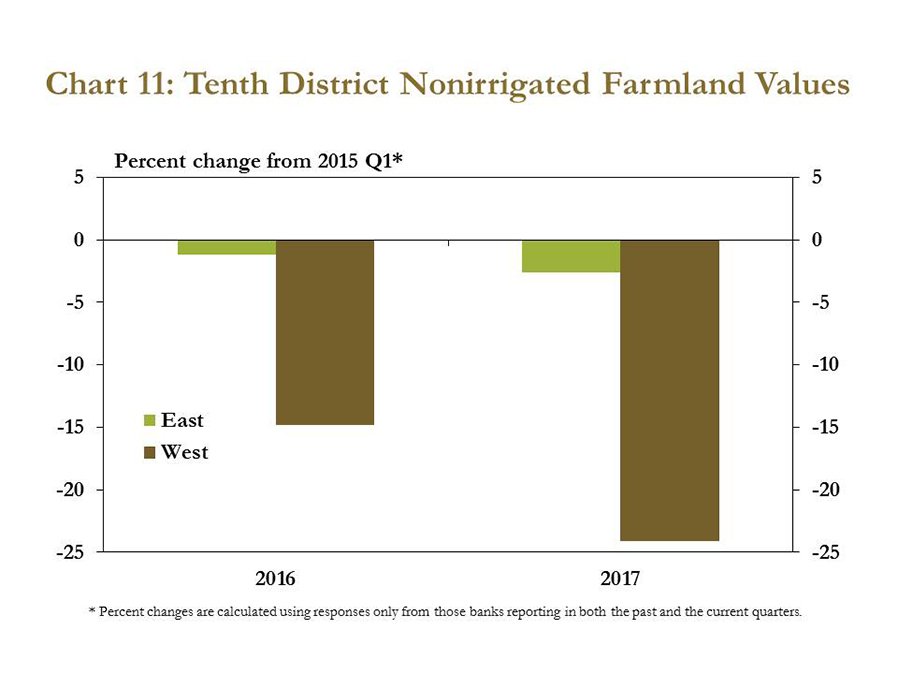

The recent declines in farmland values in the Tenth District, however, also have been sharper in the west. The value of nonirrigated cropland began to soften in 2013 throughout the District, but recent declines have been more substantial in the west (Chart 11). In fact, according to the survey, nonirrigated cropland values have fallen only 3 percent in the east since the first quarter of 2015, but have dropped 24 percent in the western portion of the District.

Conclusion

In the first quarter, bankers throughout the Tenth District indicated that profit margins and cash flow remained tight. However, financial stress among agricultural producers and concerns among lenders have become more regional as economic conditions have worsened more significantly in the western portion of the District than in the east. As the farm economy remains under pressure, it is possible that challenges may intensify in some regions even as conditions may begin to stabilize in other areas.

The views expressed in this article are those of the authors and do not necessarily reflect the views of the Federal Reserve Bank of Kansas City or the Federal Reserve System.

Author