Farm income and credit conditions continued to deteriorate in the third quarter of 2018, according to the Tenth District Survey of Agricultural Credit Conditions. Expectations for farm income and loan repayment rates were lowest for areas and operations more concentrated in soybean, corn, hog and dairy production as uncertainties surrounding trade continued. Alongside lower repayment rates, working capital deteriorated moderately while bankers’ loan portfolios in crop-producing states showed slightly higher levels of risk. Although farmland values remained stable, increasing stress in the farm sector could put downward pressure on farm real estate moving forward.

Data and Information

Credit Conditions | Fixed Interest Rates | Variable Interest Rates | Land Values

Farm Income and Farmland Values

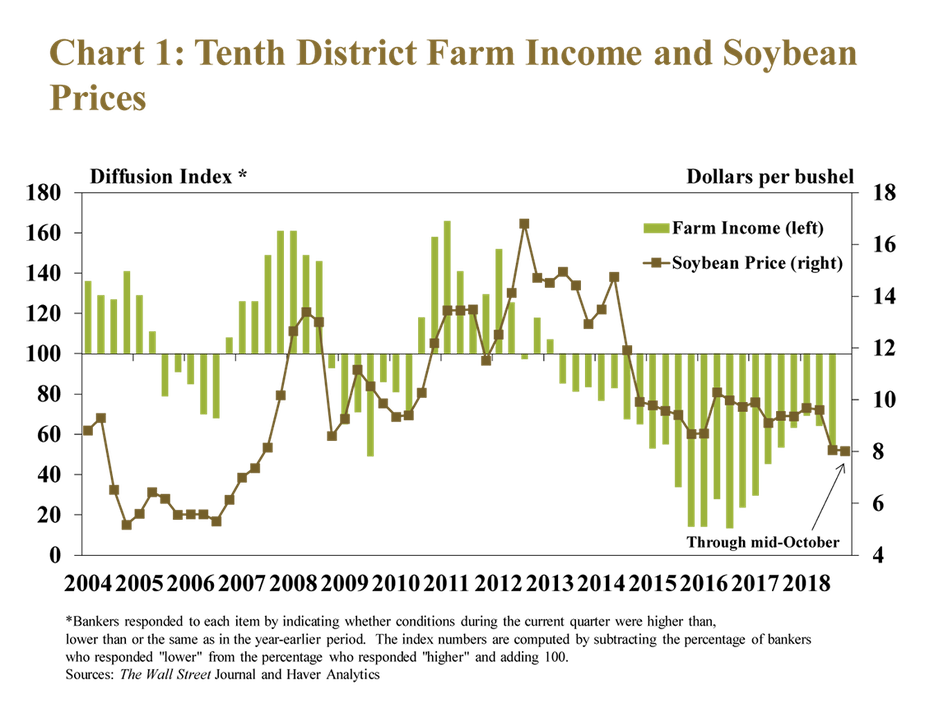

The decline in farm income accelerated slightly in the third quarter. Heading into the fall harvest, prices for most major commodities remained lower than a year ago amid elevated supply expectations and ongoing trade disruptions. Throughout the Tenth District, more than half of bankers reported lower farm income compared to a year ago, while less than 5 percent reported higher income (Chart 1). The drop was sharpest in states with higher concentrations in corn and soybeans. For example, more than 80 percent of bankers in Missouri and 60 percent of bankers in Nebraska reported lower income.

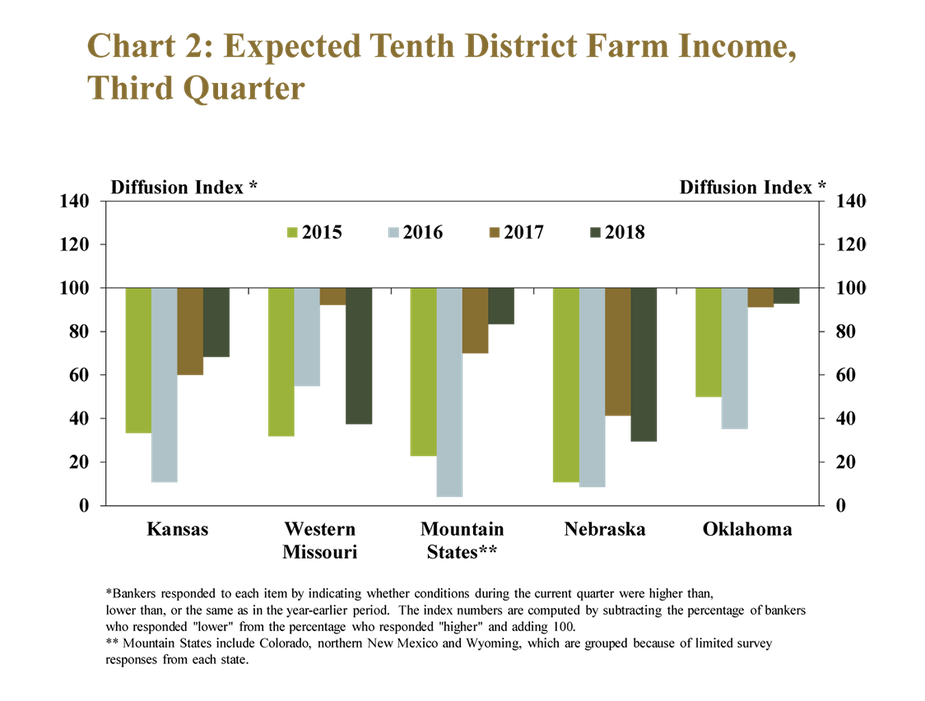

Farm income also was expected to weaken in coming months. Bankers in most states thought farm income would decrease but at a slower pace than in 2017 (Chart 2). Farm income was projected to decline at the fastest pace in states with higher concentrations of corn and soybeans. U.S. soybean exports to China were down 91 percent in the third quarter, elevating concerns that fourth-quarter exports also could decline significantly. More than 70 percent of respondents anticipated lower income in the next three months in Missouri and Nebraska, states where soybeans comprise 27 and 15 percent of farm revenues, respectively.

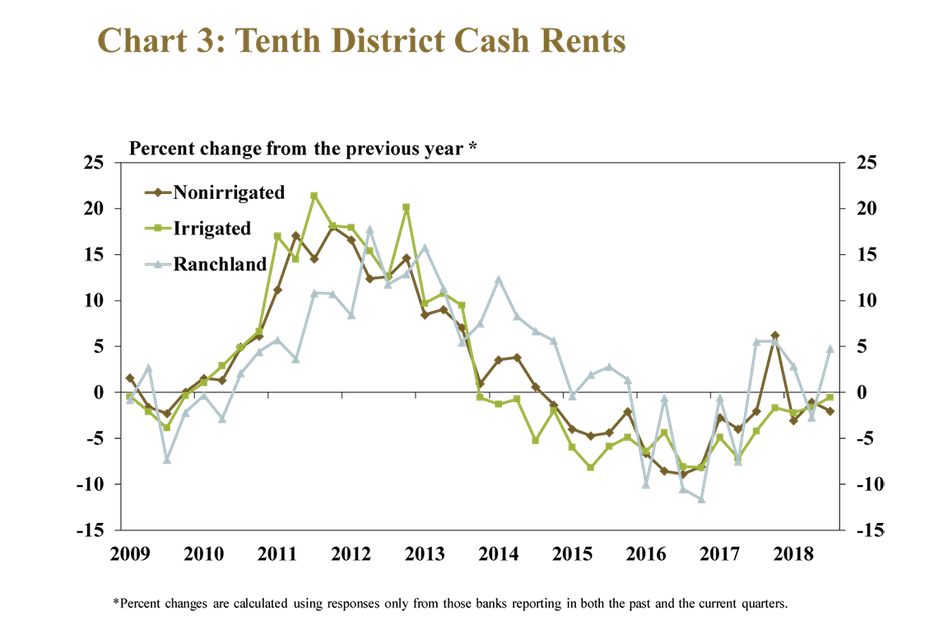

In addition to lower commodity prices, rising production costs remained an important factor for farm finances. Despite prolonged weaknesses in the farm economy and recent declines in farm income, cash rents have decreased only modestly and have appeared to stabilize in recent quarters (Chart 3). In fact, cash rents for ranchland increased almost 5 percent from a year ago. In addition, cash rents for irrigated farmland fell at the slowest pace since 2013 and the downward trend in nonirrigated farmland rents remained modest.

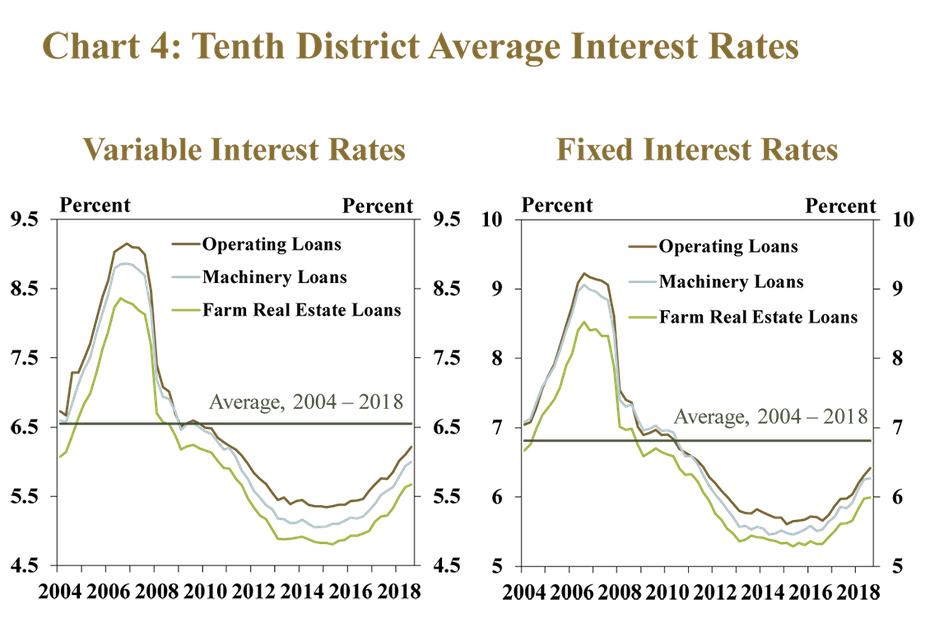

Higher interest rates also could put some upward pressure on financing costs, but interest rates still remain below the recent historical average. Despite increasing at a faster pace, rates on farm loans remained well below pre-recession levels (Chart 4). From 2006 to 2014, variable interest rates on operating loans decreased nearly 300 basis points. Since 2014, however, rates have increased nearly 100 basis points. As interest rates have risen, interest expenses increasingly have become an important component of farm profitability, but so far, the increase in interest expenses has been modest.

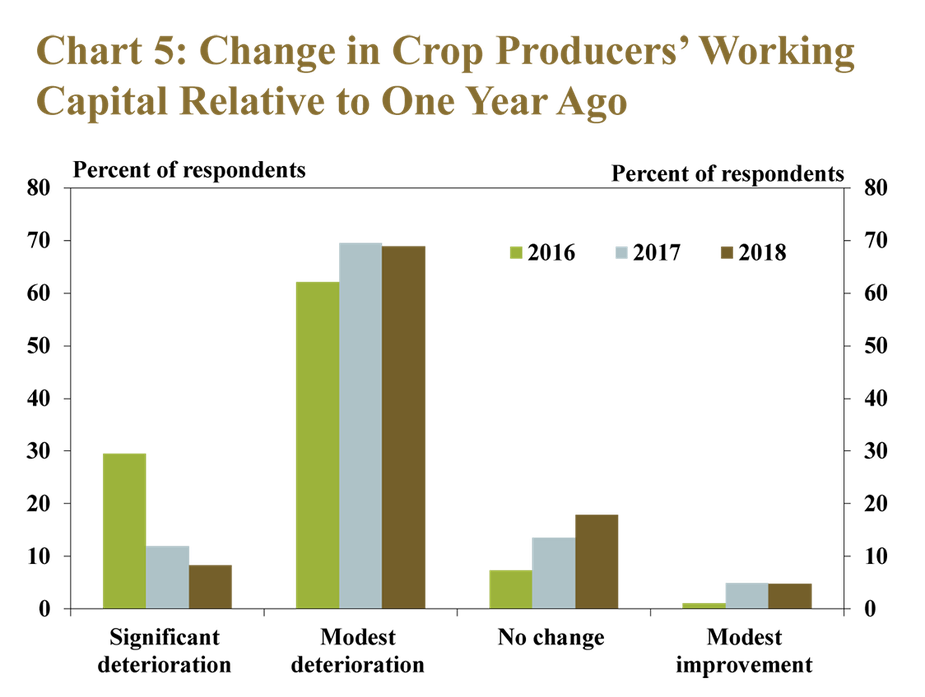

The prolonged period of depressed farm income has placed more pressure on borrower balance sheets. According to bankers across the District, a majority of crop producers in 2018 had a modest deterioration in working capital (Chart 5). While the number of bankers reporting no change in borrower liquidity increased in 2018, signs of continued weakness remained. For the fifth straight year, a majority of bankers reported having borrowers with some depletion of short-term operating funds.

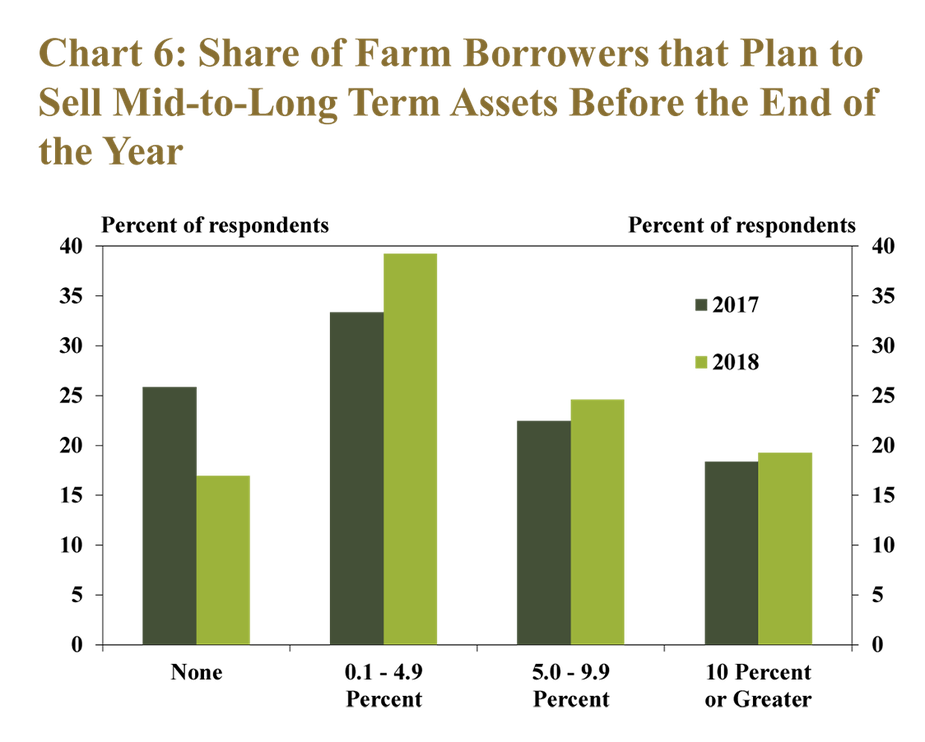

Stress on farm finances also contributed to an increase in the expected sale of mid- to long-term assets in 2018. The number of bankers expecting farm borrowers to sell assets to improve available working capital or make loan payments increased sharply from a year ago (Chart 6). In fact, nearly 85 percent of bankers reported that farm borrowers plan to sell mid- to long-term assets before year’s end, up from about 75 percent a year ago.

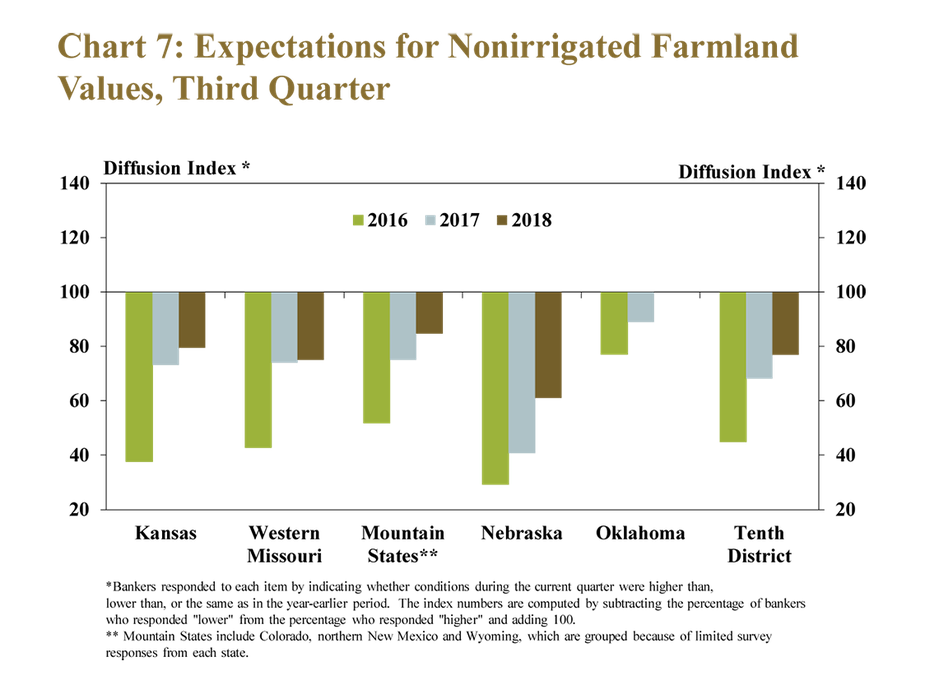

Alongside lower farm income and declining liquidity, a majority of bankers expected farmland values to decrease in the next quarter, but at a slower pace than in previous years. Similar to expectations for farm income, bankers in Nebraska, Kansas and western Missouri were also most pessimistic about the outlook for farmland values (Chart 7). Despite predicted declines, further deterioration of farm finances and rising interest rates, nonirrigated farmland values across the District decreased only 2 percent from a year ago.

Credit Conditions

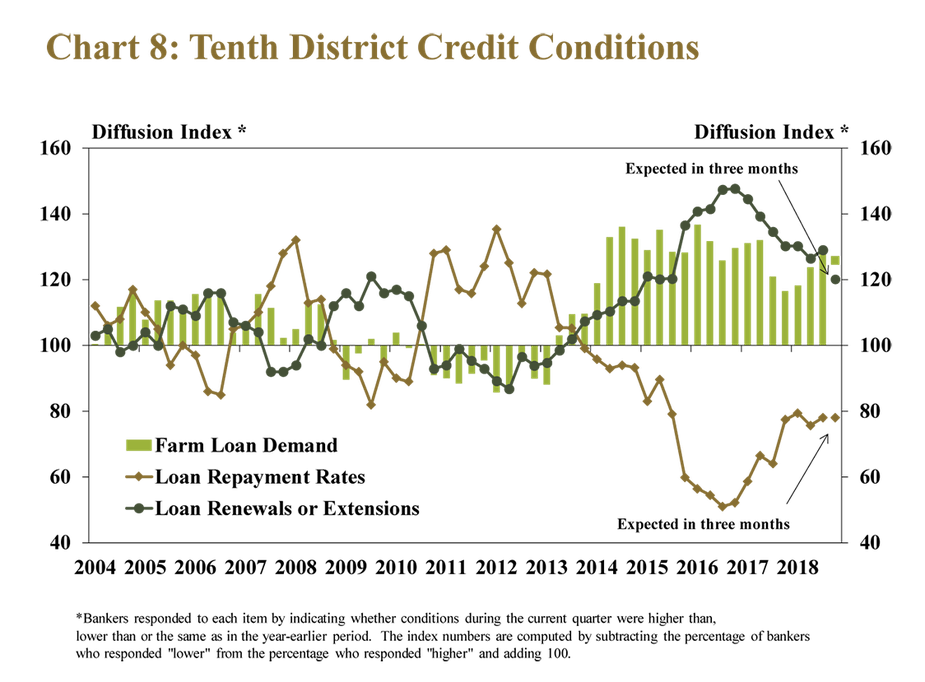

Alongside lower farm income, demand for farm loans increased. Although a majority of the District’s agricultural lenders have reported higher loan demand for five years, the pace of growth was the highest since the second quarter of 2016 (Chart 8). Some District bankers commented that increasing production expenses and lower commodity prices added stress to farm borrowers and likely boosted third-quarter demand for non-real estate farm loans.

In addition to higher loan demand, a majority of Tenth District bankers reported lower repayment rates on farm loans, although the pace of the decline remained stable. Bankers commented that some producers benefited from improved cattle markets, and repayment rates for cow/calf operations were higher for the second year in a row (Chart 9). Although the overall pace of decline in repayment rates remained stable—likely due to the influence of cattle markets—repayment rates for corn, soybean, hog and dairy operations declined faster than in 2017.

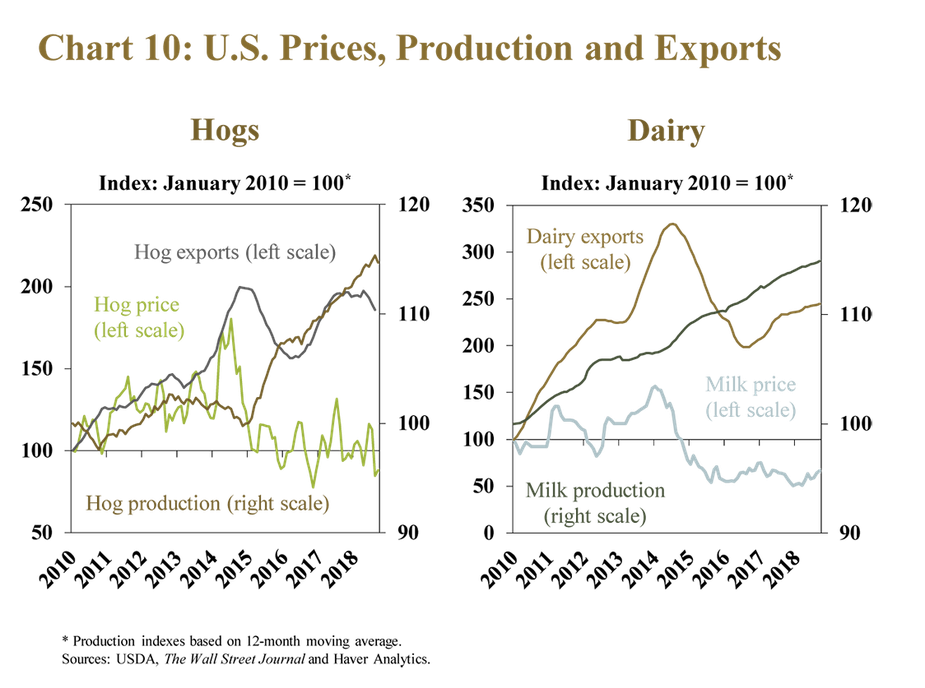

The faster decline in repayment rates on soybean, dairy and hog operations highlighted concerns of oversupply and trade uncertainty in key agricultural industries. In the milk and hog industries, production has steadily increased over the past decade (Chart 10). In addition, hog exports declined slightly in the third quarter compared to both the previous quarter and previous year, and dairy exports remained flat. Supply and demand issues in both industries have weighed on prices. Similar to other commodities affected by large supplies and trade disputes, low prices for milk and pork have reduced cash flow and darkened the outlook for farm finances.

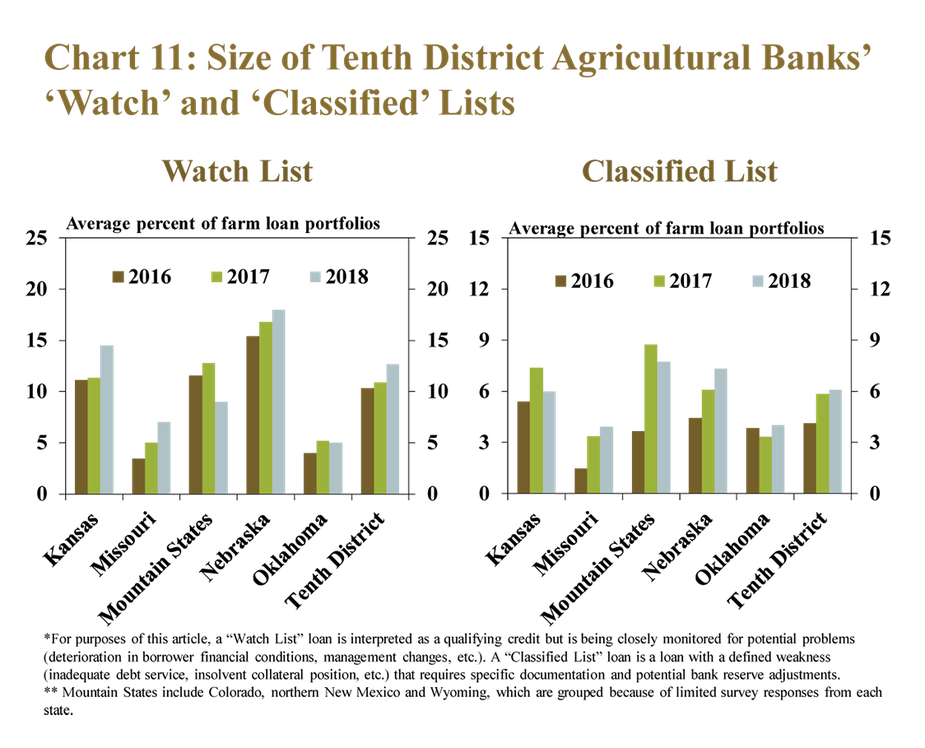

Lower repayment rates likely have contributed to expanded credit monitoring practices. Similar to expectations for farm income, farmland values and repayment rates, problem loan lists were relatively larger in states with higher concentrations of corn and soybeans (Chart 11). For example, bankers in Missouri and Nebraska reported the largest increases in both watch and classified lists. Although the average size of classified lists declined slightly in Kansas, watch lists in the state increased from 11 percent of farm loan portfolios in 2017 to 15 percent in 2018.

Conclusion

Farm income in the third quarter declined across the Tenth District. A majority of bankers expected repayment rates to decrease at a faster pace for soybean, hog and dairy operations, which seemed to reflect growing stress from elevated supplies and trade uncertainty in these industries. Lower income continued to strain working capital and the share of bankers with operators planning to sell mid- to long-term assets increased from a year ago. Farmland values remained stable and continued to support agricultural credit conditions. However, lower farm income and reduced liquidity could weigh on farmland values in future quarters.

________________________________________________________________________

Banker Comments from the Tenth District

Attracting and maintaining large and higher quality loan customers has become increasingly competitive. – Southeast Colorado

Crops in the area look good and some operators have benefitted from good cattle prices. – Southwest Kansas

Surprisingly, we are seeing stronger land prices despite current commodity prices. – Northeast Kansas

Higher interest rates, along with increasing fuel and repair costs are key concerns for producers. – Southwest Kansas

Much of our area was hit with significant drought, which paired with the currently low commodity prices has reduced capital for most producers. – Northeast Kansas

The real estate market has been slow lately, but we anticipate some sales this fall and winter. – Northeast Kansas

Abundant rain during the growing season will provide average yields. Yields should offset the commodity price declines. – Southwest Kansas

We seemed to have a good wheat harvest, and I think a good fall crop harvest is on its way. I believe that this will get our farmers through the year. - Northwest Kansas

Devaluation of land, cattle and equipment are causing adjusted analysis of borrowing capacity and cash flow. – Central Kansas

Current grain prices make it very hard for borrowers to cash flow. Trade agreements need to be worked out with other countries to hopefully help prices rebound. – Southwest Kansas

We are on the border line between drought and severe drought. Most farm customers will produce 60 to 80% of normal and will have income deficiencies. – Western Missouri

Yields on corn will be extremely variable due to lack of rain. Soybean yields should hold up with timely late rains but yields will not be record breakers. – Western Missouri

We expect farm operations to lose money in 2018 with many facing the need to restore working capital by refinancing land or possibly selling assets in spring of 2019. – Southeast Nebraska

Low commodity prices are going to negatively affect land values and rental rates. – Northeast Nebraska

It is going to be a tough renewal season. We have heard of a lot of land that is going to be pushed on the market this winter to shore up debt or liquidity positions. – Eastern Nebraska

There have been very few land sales in this area during the past three months with little change in values. – Southwest Nebraska

With current commodity prices, nobody is buying land. – Central Nebraska

Predictions of large 2018 corn supply and the current trade war is adversely affecting the agriculture sector in our area. – Western Nebraska

Deteriorating working capital and overall equity erosion of ag customers is starting to have a significant impact on producers and lenders. – Western Nebraska

A total of 176 banks responded to the Third Quarter Survey of Agricultural Credit Conditions in the Tenth Federal Reserve District—an area that includes Colorado, Kansas, Nebraska, Oklahoma, Wyoming, the northern half of New Mexico and the western third of Missouri. Please refer questions to External LinkCortney Cowley, economist or External LinkTy Kreitman, assistant economist, at 1-800-333-1040.

The views expressed in this article are those of the authors and do not necessarily reflect the views of the Federal Reserve Bank of Kansas City or the Federal Reserve System.

Authors

Cortney Cowley

Assistant Vice President and Oklahoma City Branch Executive