Farm real estate markets in the Tenth District remained relatively stable in the fourth quarter of 2017. The stability in farmland values was due, in part, to fewer sales, and a significant number of bankers expect values to remain steady in 2018. Farm income in the fourth quarter continued to decline, and credit conditions remained weak, but the pace of deterioration has continued to slow. The relative strength of farmland values has provided support for farm finances despite the ongoing pressure of low agricultural commodity prices on farm income.

Data

Credit Conditions | Fixed Interest Rates | Variable Interest Rates | Land Values

Farmland Values

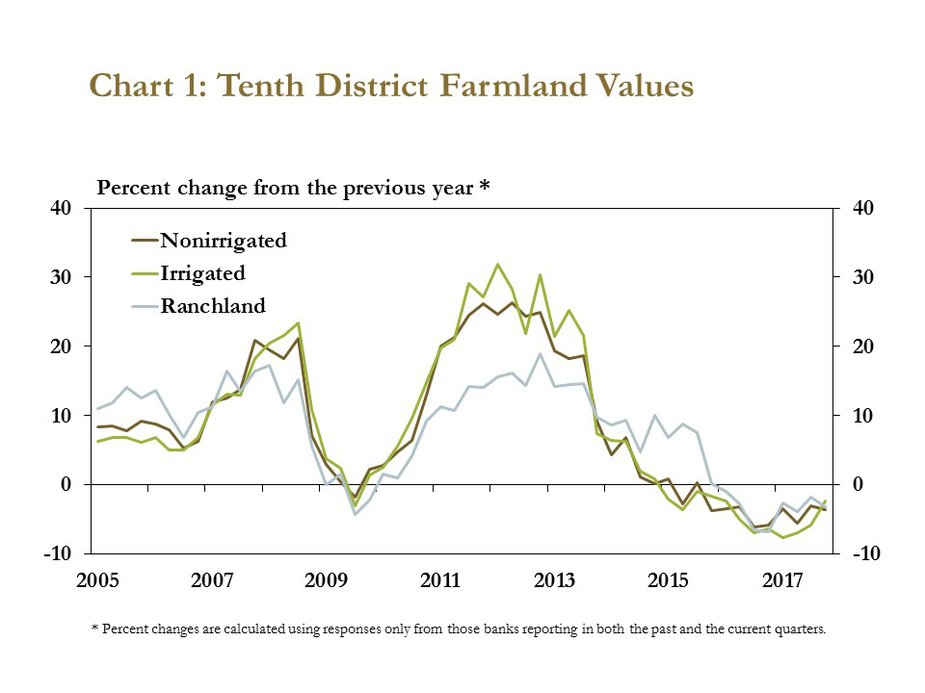

Farmland markets held firm in the fourth quarter, according to the Tenth District Survey of Agricultural Credit Conditions. On average, values for all types of farmland declined only 3 percent from a year ago (Chart 1). Prior to the fourth quarter, farmland values had declined at an annual pace of 5-7 percent, but those declines appear to have slowed more recently. The value of irrigated cropland decreased only 2 percent in the fourth quarter after dropping 8 percent in the first quarter of 2017.

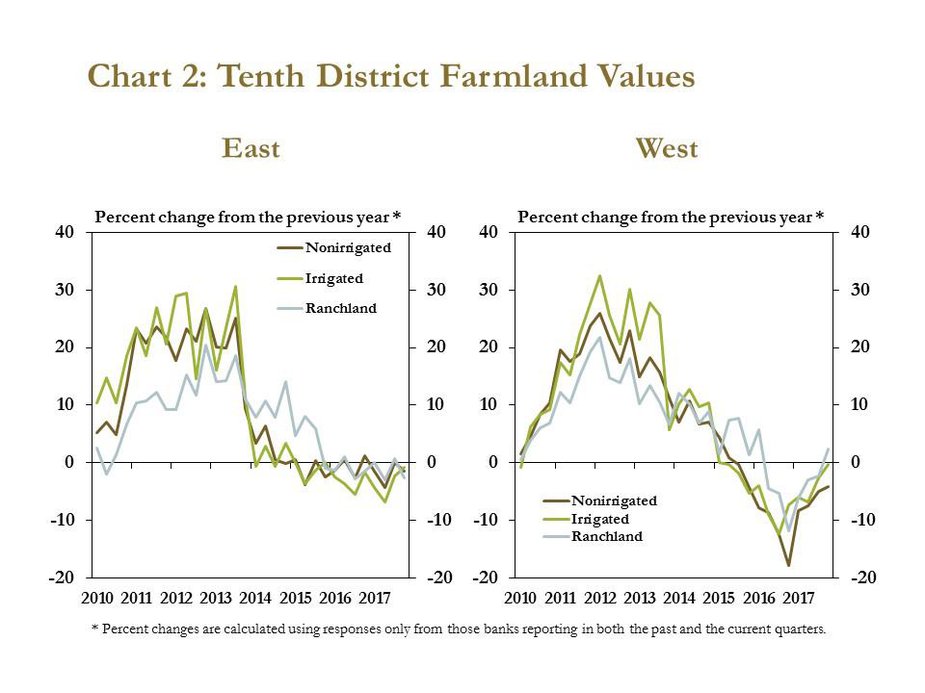

The recent stabilization of Tenth District farmland values has been driven by improvements in farm real estate markets in the western part of the District. In the eastern portion, values for all types of farmland during the last three years have remained relatively steady (Chart 2, left panel). In the western portion, however, values for farmland rebounded from steep declines in 2016 as economic conditions in the livestock sector improved (Chart 2, right panel).

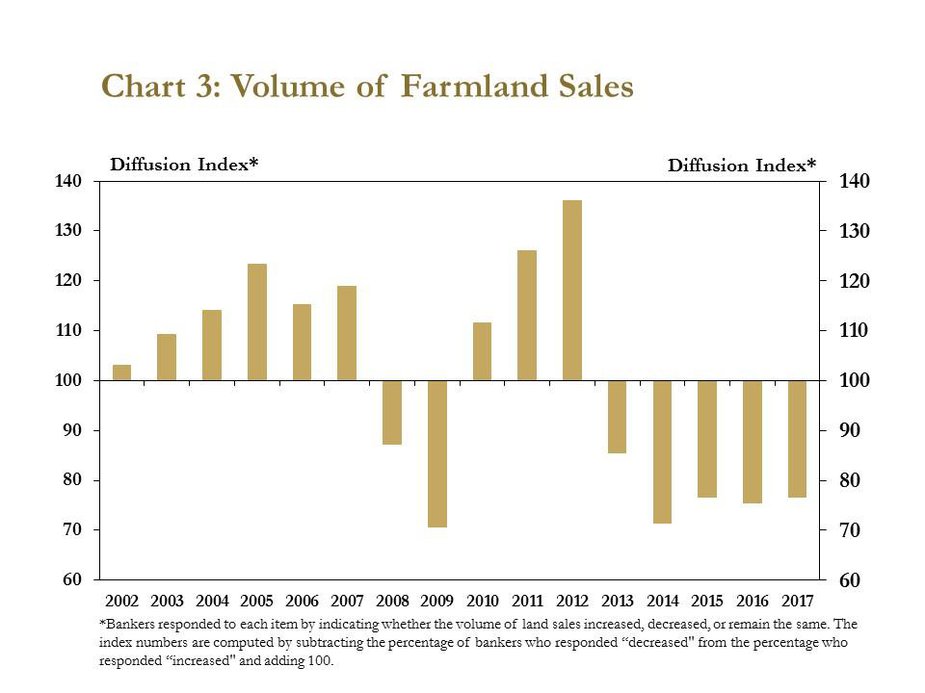

A limited number of farmland sales have contributed to the stability of farmland values. For the fifth straight year, a majority of bankers reported a decline in the volume of farmland sold (Chart 3). In fact, 80 percent of bankers indicated that compared with a year ago farmland sales either were lower or unchanged in their lending area. Although several bankers commented that limited sales supported farmland values, most also mentioned that they expect sales in 2018 to increase.

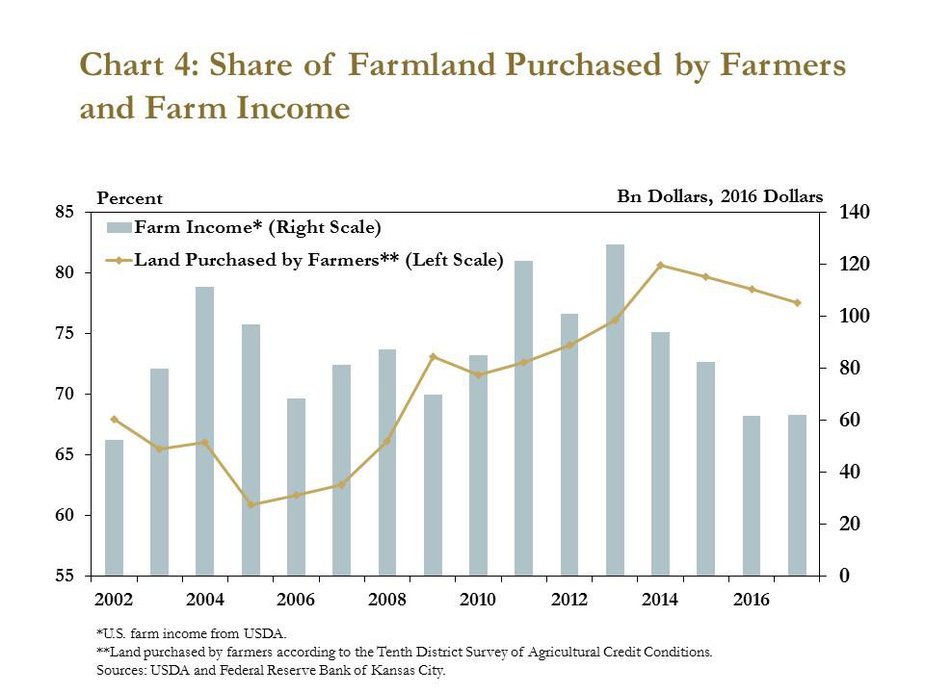

Sales remained muted in 2017, but farmers still purchased a large share of farm real estate. More than 75 percent of farmland sold in the District was purchased by farmers despite a slight decrease from a few years ago and sharp declines in U.S. farm income (Chart 4). Declines in farm income likely have curbed farmers’ purchases of farmland somewhat, but farmers generally have remained active buyers. A decade ago, and prior to the surge in farm income from 2008 to 2013, farmers accounted for only 65 percent of farmland purchases. More recently, the number of sales has declined, but demand for land in the farming sector has remained strong.

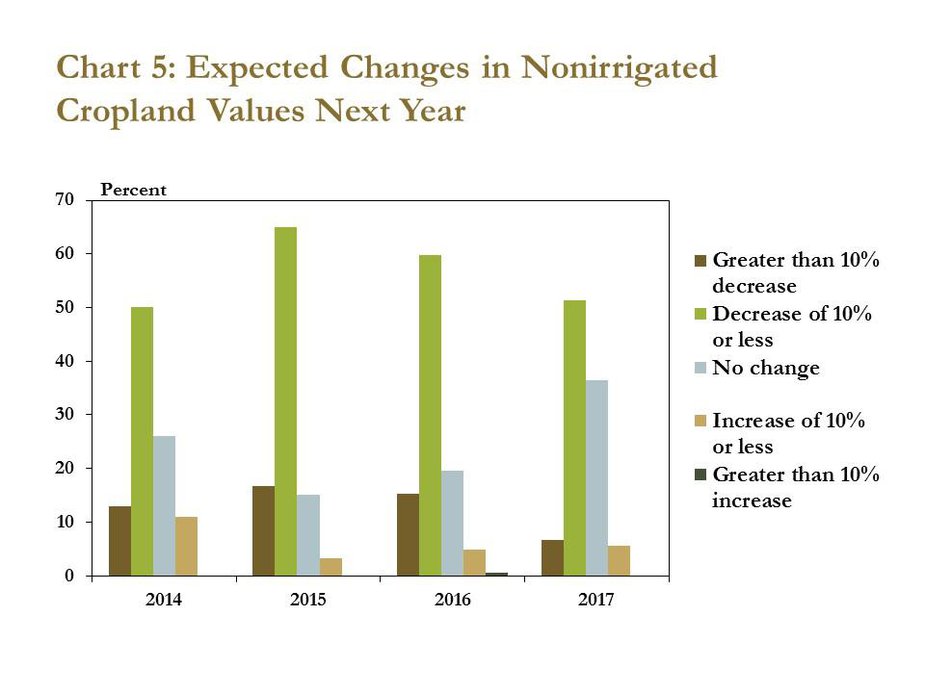

Looking ahead, more bankers indicated they expect farmland values to remain steady. More than 40 percent of bankers surveyed expected cropland values in the coming year either to increase or remain unchanged (Chart 5). In each of the past two years, less than 25 percent of bankers expected values to increase or remain stable. Moreover, only 7 percent of bankers expected double-digit declines in the next 12 months, which was half the number of bankers that expected double-digit declines a year ago.

Farm Income

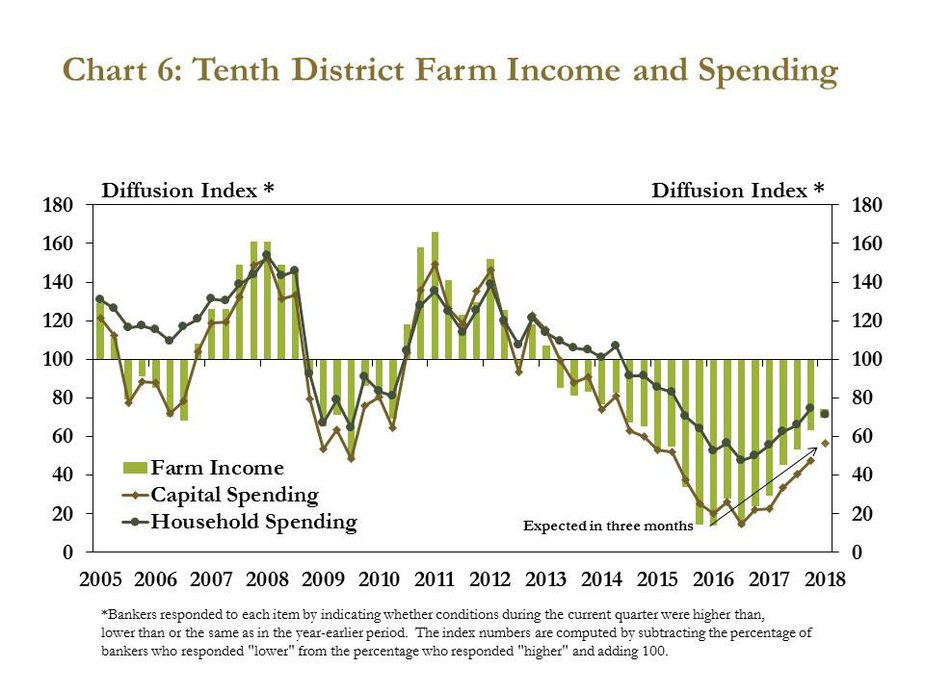

Farm income continued to decline but at a slower pace than in previous quarters. In addition to some stabilization in farmland markets, smaller declines in farm income also suggested that the farm economy in the Tenth District may be stabilizing. Several bankers commented that producers seem to be adjusting slowly to lower commodity prices. One adjustment made by producers is a reduction in capital spending and household spending (Chart 6). These expenses continued to decrease in the fourth quarter, but also have shown some signs of stabilizing from sharper declines in 2016.

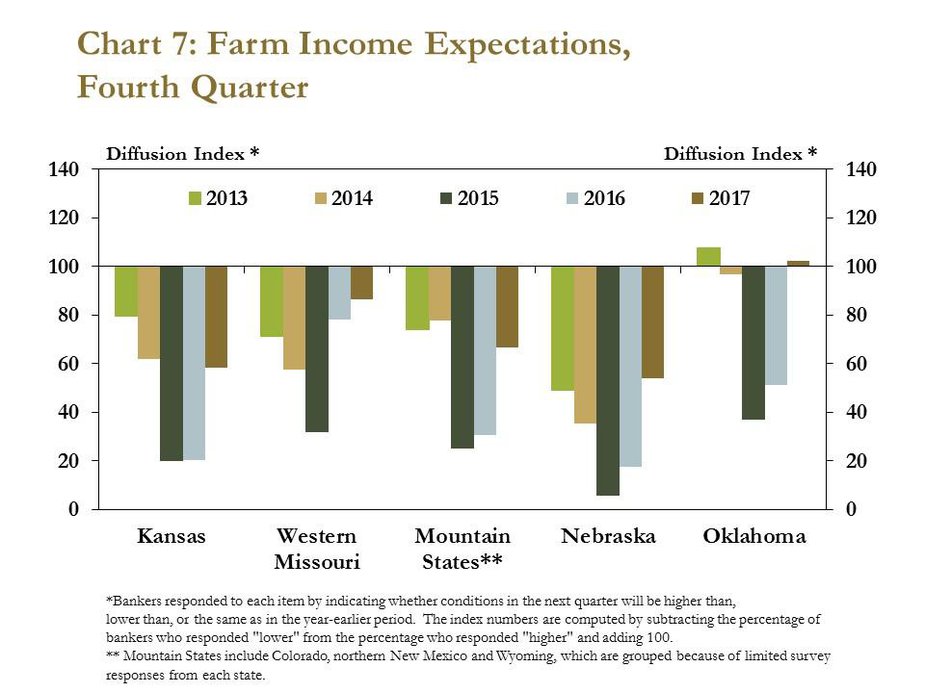

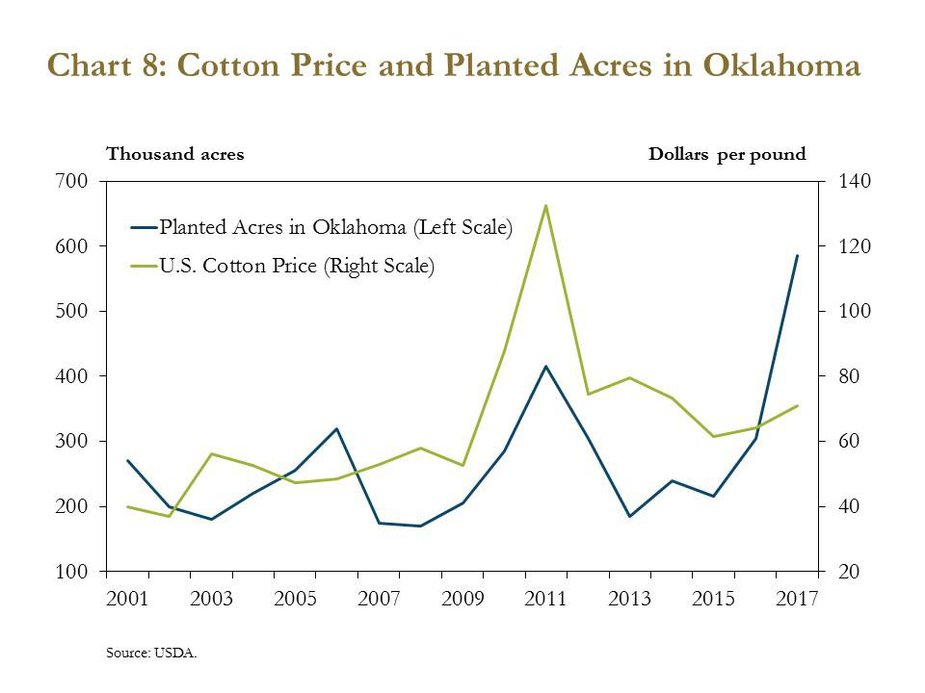

Compared to previous years, fewer bankers in each District state expected farm income to decline in the coming months. For each of the past two years, more than half of survey respondents indicated they expected farm income to continue to decline. A year ago, 80 percent of bankers in Nebraska and Kansas expected further declines in coming months. In contrast, less than half of bankers in these two states expected additional declines in farm income in the coming months (Chart 7). In Oklahoma, a majority of bankers expected an increase in farm income in the first quarter of 2018. Some of the optimism in Oklahoma likely was due to the increase in cotton acreage and the relative strength in cotton prices (Chart 8).

Credit Conditions

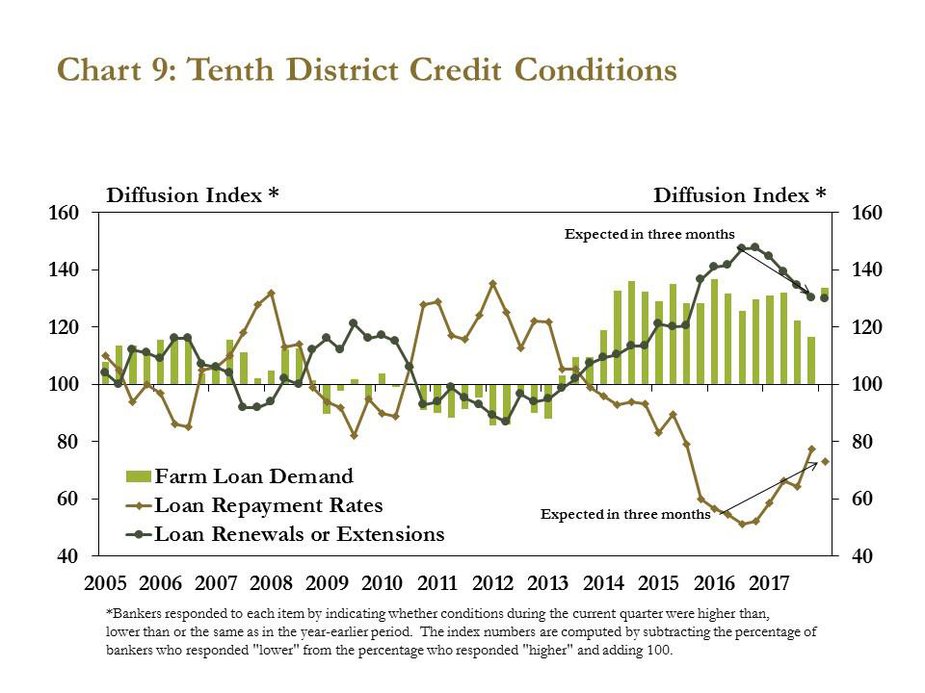

Similar to farm income, agricultural credit conditions stabilized modestly but continued to show signs of weakness. The pace of decline in farm loan repayment rates abated somewhat, as fewer bankers reported lower repayment rates compared to previous quarters (Chart 9). Demand for new farm loans and renewals or extensions on existing loans also increased at a slower rate than in previous quarters. Despite signs of stabilizing in the fourth quarter, bankers’ expectations were for loan demand to strengthen and loan repayment rates to weaken slightly in the first quarter of 2018.

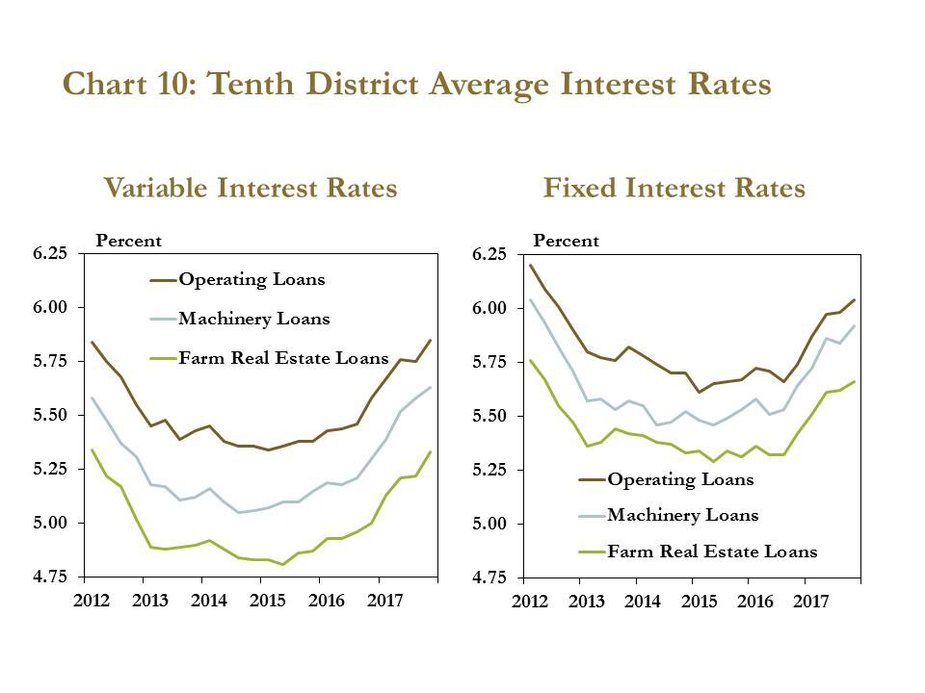

Although farm financial conditions have stabilized somewhat, higher interest rates could heighten concerns for some farm borrowers. Fixed interest rates on all types of farm loans have increased since the first quarter of 2015, and variable interest rates have increased almost 40 basis points since 2016 (Chart 10). As farm loan demand remains strong, higher interest rates will lead to an increase in interest expenses for some borrowers. In addition, higher interest rates could put some downward pressure on farmland values over time.

Conclusion

Farm income declined in the fourth quarter and credit conditions remained relatively weak, but farm real estate continued to provide support for the District’s agricultural economy. Despite persistently low commodity prices, farmland values have remained relatively strong. Looking forward, fewer bankers expect farm income to decline in coming months, suggesting that economic conditions may continue to stabilize. Still, ongoing demand for financing amid a low income environment and slightly higher interest rates suggests that credit risks in the farm sector still remain a focus for 2018.

Disclaimer

A total of 212 banks responded to the Fourth Quarter Survey of Agricultural Credit Conditions in the Tenth Federal Reserve District—an area that includes Colorado, Kansas, Nebraska, Oklahoma, Wyoming, the northern half of New Mexico and the western third of Missouri. Please refer questions to External LinkNathan Kauffman, Omaha Branch executive or External LinkCortney Cowley, economist at 1-800-333-1040.

The views expressed in this article are those of the authors and do not necessarily reflect the views of the Federal Reserve Bank of Kansas City or the Federal Reserve System.

Authors

Nate Kauffman

Senior Vice President, Economist, and Omaha Branch Executive; Executive Director of the Center for Agriculture and the Economy